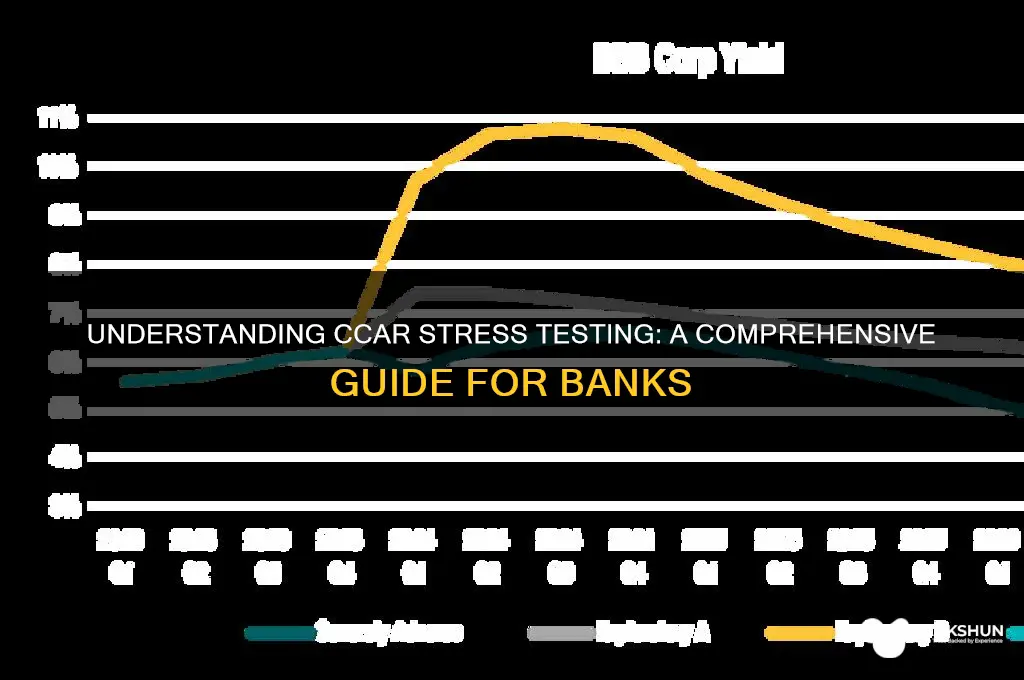

CCAR (Comprehensive Capital Analysis and Review) stress testing is a critical regulatory process conducted by the Federal Reserve to evaluate the resilience of large banks in the United States. It assesses whether banks have sufficient capital to withstand adverse economic scenarios, ensuring financial stability. The process involves banks projecting their revenues, losses, and capital levels under baseline, adverse, and severely adverse economic conditions over a nine-quarter horizon. The Federal Reserve reviews these submissions, focusing on both quantitative results and the quality of banks' methodologies, assumptions, and risk management practices. Banks that fail to meet the standards may face restrictions on capital distributions, such as dividends or share buybacks, making CCAR a vital tool for maintaining the health of the banking system.

Explore related products

What You'll Learn

- Scenario Design: Creating adverse economic scenarios to test bank resilience under stress conditions

- Data Collection: Gathering historical and current financial data for accurate stress test inputs

- Model Validation: Ensuring stress test models are reliable and reflect real-world risks

- Capital Adequacy: Assessing if banks maintain sufficient capital to absorb stress losses

- Regulatory Reporting: Submitting stress test results to comply with CCAR requirements

![]()

Scenario Design: Creating adverse economic scenarios to test bank resilience under stress conditions

Scenario design is a critical component of the Comprehensive Capital Analysis and Review (CCAR) stress testing process for banks. It involves creating adverse economic scenarios that challenge a bank’s resilience by simulating severe but plausible economic conditions. These scenarios are designed to assess how well a bank can withstand stress, maintain sufficient capital, and continue operations without posing a risk to financial stability. The process begins with a thorough analysis of historical economic data, current market trends, and potential risks that could impact the banking sector. Regulators, such as the Federal Reserve, collaborate with economists and financial experts to identify key risk factors, including GDP decline, unemployment spikes, asset price crashes, and interest rate shocks. The goal is to construct scenarios that are both severe and realistic, ensuring banks are tested under conditions that reflect potential future crises.

Once the key risk factors are identified, scenario designers quantify their impact by assigning specific values to economic variables. For example, an adverse scenario might include a 4% decline in GDP, a 10% drop in housing prices, and a 5% increase in the unemployment rate over a nine-quarter horizon. These variables are interlinked to create a coherent narrative that reflects how economic shocks could cascade through the financial system. For instance, a recession scenario might start with a global economic slowdown, leading to reduced consumer spending, corporate defaults, and a deterioration in asset quality for banks. The scenarios are often designed with multiple phases, such as an initial shock followed by a prolonged recovery period, to test banks’ ability to manage stress over time.

Customization is another important aspect of scenario design. While baseline scenarios are standardized across banks, regulators may tailor additional scenarios to reflect institution-specific risks. For example, a bank with significant exposure to commercial real estate might face a scenario with a sharper decline in property values. Similarly, banks with large international operations could be tested against scenarios involving global economic shocks or currency devaluations. This customization ensures that stress tests are relevant to each bank’s unique risk profile and business model, providing a more accurate assessment of their resilience.

Transparency and communication are essential in the scenario design process. Regulators publish detailed descriptions of the scenarios, including the assumptions and methodologies used, to ensure banks understand the parameters of the stress test. This transparency allows banks to prepare adequately and model the scenarios accurately in their internal stress testing frameworks. Additionally, regulators often engage in dialogue with banks during the design phase to address concerns and ensure the scenarios are both challenging and fair. This collaborative approach enhances the credibility of the stress testing process and fosters a shared understanding of the risks being assessed.

Finally, scenario design must evolve to reflect changing economic landscapes and emerging risks. For example, recent years have seen the incorporation of climate-related risks, cybersecurity threats, and geopolitical tensions into stress testing scenarios. Regulators continuously monitor global developments and update scenarios to ensure they remain relevant and forward-looking. By staying adaptive, scenario design ensures that banks are tested against the most pressing risks of the current and future economic environment, ultimately strengthening the resilience of the financial system as a whole.

Huntington Bank Business CD Rates: What You Need to Know

You may want to see also

Explore related products

![]()

Data Collection: Gathering historical and current financial data for accurate stress test inputs

Data collection is a critical first step in the CCAR (Comprehensive Capital Analysis and Review) stress testing process for banks. The accuracy and reliability of stress test results heavily depend on the quality of the data used as inputs. Banks must gather both historical and current financial data to ensure a comprehensive understanding of their financial health and potential vulnerabilities under adverse scenarios. This involves collecting data from various sources, including financial statements, regulatory filings, internal management reports, and market data. Historical data, typically spanning several years, provides a baseline for understanding past performance and trends, while current data reflects the bank’s most recent financial position and market conditions.

The process begins with identifying the key data elements required for stress testing, such as balance sheet items (e.g., loans, deposits, and equity), income statement components (e.g., revenues, expenses, and net income), and off-balance-sheet exposures (e.g., derivatives and contingent liabilities). Banks must ensure that the data is granular enough to capture the nuances of different business lines, products, and risk categories. For example, loan data should be segmented by type (e.g., mortgages, commercial loans) and risk characteristics (e.g., credit scores, loan-to-value ratios). Similarly, market risk data should include historical price movements, volatilities, and correlations for various asset classes.

Once the required data elements are identified, banks must establish robust data collection processes. This includes standardizing data formats, ensuring consistency across different sources, and validating the accuracy and completeness of the data. Data gaps or inconsistencies can lead to flawed stress test results, so banks often employ data reconciliation techniques and perform data quality checks. Additionally, banks may need to supplement internal data with external sources, such as macroeconomic indicators, market indices, and regulatory benchmarks, to account for systemic risks and broader economic conditions.

Timeliness is another crucial aspect of data collection. Stress tests often require up-to-date information to reflect the bank’s current financial position and market environment. Banks must have mechanisms in place to update data regularly, especially for dynamic variables like market prices, interest rates, and credit spreads. Delays in data collection can compromise the relevance of stress test results, particularly in rapidly changing economic conditions. Therefore, banks should invest in data infrastructure and automation tools to streamline the data collection process and minimize latency.

Finally, documentation and transparency are essential components of data collection for CCAR stress testing. Banks must maintain detailed records of the data sources, methodologies, and assumptions used in the process. This not only facilitates internal audit and review but also ensures compliance with regulatory requirements. Regulators often scrutinize the data collection process to assess the reliability of stress test inputs, so banks must be prepared to demonstrate the integrity and robustness of their data gathering practices. By prioritizing accuracy, granularity, timeliness, and transparency in data collection, banks can lay a solid foundation for effective CCAR stress testing.

The Rumored Romance of Matt Broome and Sasha Banks

You may want to see also

Explore related products

![]()

Model Validation: Ensuring stress test models are reliable and reflect real-world risks

Model validation is a critical component of the CCAR (Comprehensive Capital Analysis and Review) stress testing process for banks, ensuring that the models used to assess a bank's resilience under adverse scenarios are reliable, accurate, and reflective of real-world risks. The validation process involves a rigorous examination of the models' underlying assumptions, methodologies, and outputs to ensure they align with regulatory expectations and industry best practices. Validators must assess whether the models capture the complexity of the bank's risk profile, including credit, market, liquidity, and operational risks, while avoiding oversimplification or undue conservatism. This step is essential to build confidence in the stress test results, which inform capital planning, risk management, and regulatory decisions.

A key aspect of model validation is the evaluation of data quality and model calibration. Validators scrutinize the historical and hypothetical data used to develop and test the models, ensuring it is relevant, accurate, and representative of the bank's portfolio and market conditions. For instance, in credit risk models, validators check if the data includes a sufficient range of economic cycles to capture default behavior under stress. Model calibration is then assessed to ensure parameters are estimated robustly and reflect the bank's specific risk characteristics. Misaligned or poorly calibrated models can lead to inaccurate projections, undermining the credibility of the stress test results.

Another critical element is the assessment of model assumptions and their alignment with real-world risks. Stress test models often rely on assumptions about correlations, market dynamics, and behavioral patterns, which must be justified and periodically updated. Validators examine whether these assumptions hold under extreme but plausible scenarios and whether they account for emerging risks, such as climate change or cybersecurity threats. For example, a liquidity risk model must realistically simulate depositor behavior during a financial crisis, avoiding overly optimistic or pessimistic assumptions. This ensures the models remain relevant and capable of identifying vulnerabilities in the bank's balance sheet.

Model validation also involves benchmarking and sensitivity analysis to test the robustness of the models. Validators compare the bank's models against industry standards, regulatory benchmarks, or alternative methodologies to identify discrepancies or weaknesses. Sensitivity tests are conducted by varying key inputs or assumptions to assess how changes impact the model outputs. For instance, a validator might adjust interest rate projections in a market risk model to see if the bank's capital adequacy remains sufficient under different rate environments. This helps identify potential blind spots and ensures the models perform consistently across a range of scenarios.

Finally, documentation and governance are integral to the model validation process. Validators require clear, comprehensive documentation of the model development, testing, and implementation processes to assess compliance with regulatory guidelines and internal policies. This includes records of data sources, methodological choices, and validation findings. Robust governance ensures that model risks are identified, escalated, and mitigated effectively. Banks must establish independent validation teams, separate from model developers, to provide objective assessments and maintain accountability. Through these measures, model validation strengthens the integrity of CCAR stress testing, enabling banks and regulators to make informed decisions about capital adequacy and risk management.

Exploring Syria's Central Banking System: Structure, Function, and Challenges

You may want to see also

Explore related products

![]()

Capital Adequacy: Assessing if banks maintain sufficient capital to absorb stress losses

Capital adequacy is a cornerstone of CCAR stress testing, ensuring banks maintain sufficient capital to withstand severe economic shocks. The process begins with the projection of capital levels under both baseline and stressed scenarios. Banks must estimate their risk-weighted assets (RWAs) and capital ratios, such as Common Equity Tier 1 (CET1), Tier 1, and Total Capital, over a nine-quarter planning horizon. These projections incorporate expected losses, revenue growth, and management actions like dividend payments or share buybacks. Regulatory guidelines require banks to use standardized methodologies for calculating RWAs, ensuring consistency across institutions.

Under the stress scenario, banks assess whether their capital remains above regulatory minimums despite significant losses. Stress losses are derived from adverse macroeconomic conditions, such as a severe recession, unemployment spikes, or asset price crashes. The Federal Reserve provides specific scenarios, including severely adverse and adverse conditions, which banks use to model the impact on their portfolios. For instance, a bank’s loan portfolio may face higher defaults, reducing its capital base. The goal is to determine if the bank’s capital buffer is sufficient to absorb these losses without breaching regulatory thresholds.

A critical aspect of capital adequacy assessment is the comprehensive capital analysis and review (CCAR) buffer. Banks must maintain a capital conservation buffer and, if applicable, a countercyclical buffer, in addition to regulatory minimums. During stress testing, banks evaluate whether their projected capital levels remain above these buffers under stress. If a bank’s capital falls below required levels, it may face restrictions on capital distributions, such as dividends or bonuses, to preserve financial stability. This ensures banks prioritize capital retention during periods of stress.

Management actions play a significant role in capital adequacy assessments. Banks submit their capital plans, which outline strategies for maintaining capital ratios under stress. These plans may include reducing dividends, issuing new capital, or adjusting risk exposure. The Federal Reserve evaluates the reasonableness and feasibility of these actions, ensuring they do not undermine the bank’s ability to lend or operate effectively. Banks must demonstrate that their capital planning processes are robust and forward-looking.

Finally, the quantitative and qualitative assessments of capital adequacy are intertwined. While the quantitative aspect focuses on capital ratios and loss absorption capacity, the qualitative review examines the bank’s capital planning processes, risk management framework, and governance. Banks must provide detailed documentation of their methodologies, assumptions, and controls. Deficiencies in either area can lead to supervisory actions, such as capital distribution restrictions or requirements to improve internal processes. This dual approach ensures banks not only meet capital requirements but also maintain sound practices to manage risks effectively.

Protecting Your Millions: Strategies for Financial Security

You may want to see also

Explore related products

![]()

Regulatory Reporting: Submitting stress test results to comply with CCAR requirements

Comprehensive Capital Analysis and Review (CCAR) stress testing is a critical regulatory requirement for banks, particularly those designated as Large Institution Supervision Coordinating Committee (LISCC) firms. As part of this process, banks must conduct rigorous stress tests to evaluate their capital adequacy and resilience under adverse economic scenarios. Regulatory Reporting: Submitting stress test results to comply with CCAR requirements is a multifaceted task that demands precision, transparency, and adherence to strict timelines. The Federal Reserve mandates that banks submit detailed stress test results, including projections of revenues, losses, and capital ratios under baseline, adverse, and severely adverse scenarios. These submissions must align with the CCAR guidelines, which are updated periodically to reflect evolving economic conditions and regulatory expectations.

The first step in submitting stress test results involves ensuring data integrity and methodological consistency. Banks must use standardized templates provided by the Federal Reserve to report their findings. These templates require granular data on various financial metrics, such as risk-weighted assets, pre-provision net revenue, and total losses. Institutions must also document the methodologies used for their stress testing models, including assumptions about macroeconomic variables, portfolio behaviors, and risk correlations. Transparency in methodology is crucial, as regulators scrutinize these models to ensure they accurately reflect a bank’s risk profile and are not overly optimistic.

Once the data is compiled and validated, banks must prepare a comprehensive submission package. This package typically includes quantitative results, qualitative assessments, and narrative explanations. The quantitative results detail the bank’s projected financial performance under each scenario, while the qualitative assessments provide insights into the governance, policies, and processes that underpin the stress testing framework. Narrative explanations are essential to clarify any unusual trends, deviations from expectations, or significant assumptions made during the analysis. Banks must also address any weaknesses identified in their capital planning processes and outline steps taken to remediate them.

Timely submission is a critical aspect of CCAR compliance. The Federal Reserve sets strict deadlines for both the initial submission and any subsequent resubmissions or additional information requests. Missing these deadlines can result in regulatory penalties, including restrictions on capital distributions such as dividends or share buybacks. Banks must therefore establish robust project management frameworks to ensure all components of the submission are completed accurately and on time. This often involves cross-functional collaboration between risk management, finance, and compliance teams, as well as external auditors who may provide independent validation of the stress test results.

Finally, banks must be prepared for regulatory feedback and potential supervisory actions following the submission of their stress test results. The Federal Reserve reviews the submissions to assess whether a bank’s capital plan is credible and whether the institution maintains sufficient capital to continue operations under stress. If deficiencies are identified, the regulator may require the bank to revise its capital plan, restrict capital distributions, or take other corrective actions. Therefore, banks must remain proactive in addressing regulatory concerns and continuously enhancing their stress testing frameworks to meet CCAR requirements. Effective regulatory reporting not only ensures compliance but also strengthens a bank’s overall risk management and capital planning capabilities.

Financial Affiliates: Who's Who in the Money World

You may want to see also