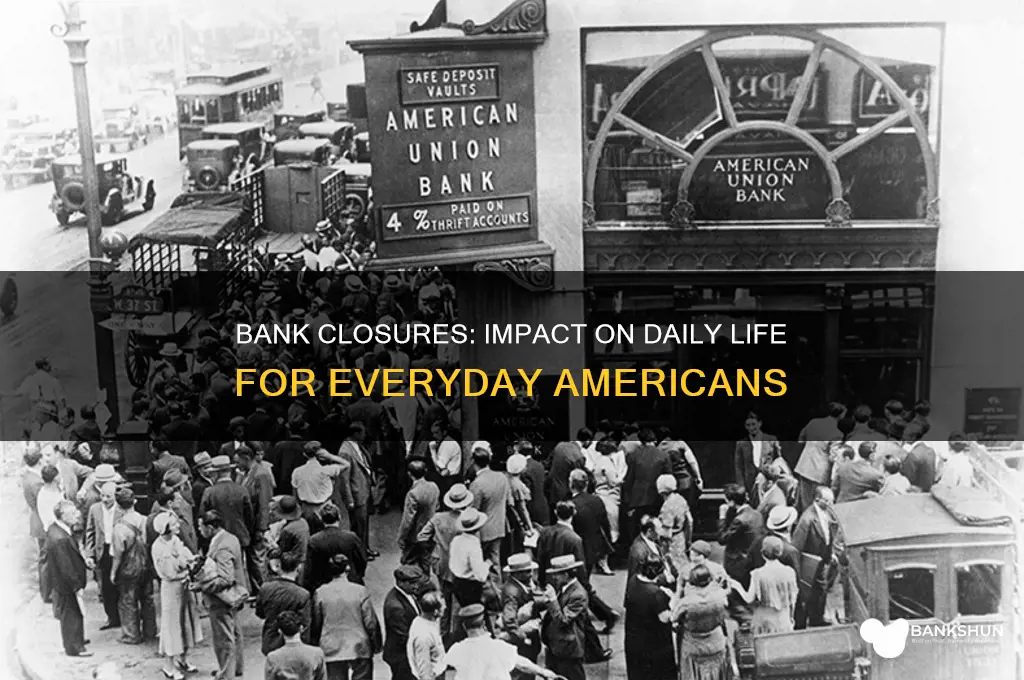

Bank closures during the 2008 financial crisis and subsequent economic downturns had profound and immediate effects on everyday Americans, disrupting their financial stability and daily lives. Many individuals lost access to essential banking services, such as checking and savings accounts, loans, and ATMs, forcing them to rely on alternative, often costlier, financial options like check-cashing services or payday lenders. Small businesses faced challenges accessing credit, hindering their ability to operate or expand, which in turn impacted local economies and employment. Additionally, the loss of community banks eroded trust in the financial system, leaving many Americans feeling vulnerable and uncertain about their economic future. These closures exacerbated existing inequalities, disproportionately affecting low-income communities and communities of color, who often had fewer resources to weather the financial storm.

Explore related products

What You'll Learn

- Job Losses and Unemployment: Many lost jobs in banking and related sectors, increasing unemployment rates nationwide

- Access to Cash and Services: Limited cash withdrawals and reduced banking services disrupted daily financial activities

- Small Business Struggles: Businesses faced difficulties accessing credit and managing cash flow, leading to closures

- Housing Market Impact: Foreclosures rose as homeowners struggled to pay mortgages without banking support

- Consumer Confidence Decline: Trust in financial institutions plummeted, affecting spending and saving behaviors

![]()

Job Losses and Unemployment: Many lost jobs in banking and related sectors, increasing unemployment rates nationwide

The wave of bank closures during the financial crisis had a profound and immediate impact on employment, particularly within the banking industry and its associated sectors. As banks shut their doors, a significant number of employees found themselves without jobs, often with little to no warning. This sudden surge in job losses contributed to a sharp rise in unemployment rates across the country, affecting not just those directly employed by the banks but also creating a ripple effect throughout the economy. The banking sector, once a stable source of employment, became a major contributor to the growing unemployment crisis.

Bank closures led to massive layoffs, as these institutions were forced to downsize or cease operations entirely. Tellers, loan officers, financial advisors, and administrative staff were among the first to be let go, as banks streamlined their operations or closed branches. For example, the collapse of major investment banks resulted in thousands of high-paying jobs disappearing overnight, leaving highly skilled professionals in a state of uncertainty. The impact was not limited to front-line staff; even executives and specialized roles in risk management, compliance, and IT were not spared, as the entire banking ecosystem contracted.

The effects of these job losses extended far beyond the banking industry. Related sectors, such as financial services, real estate, and insurance, also experienced significant downturns. Mortgage brokers, real estate agents, and insurance brokers saw their businesses suffer as the flow of credit dried up and consumer confidence plummeted. Additionally, businesses that relied on bank financing, from small startups to large corporations, faced challenges in maintaining their operations, leading to further job cuts. This interconnectedness of industries meant that the unemployment crisis spread rapidly, affecting a diverse range of occupations and skill sets.

Unemployment rates soared as a direct consequence of these bank closures and the subsequent job losses. Local communities, especially those heavily reliant on banking and financial services, were hit hard. Cities like New York, Charlotte, and San Francisco, which had thriving financial districts, witnessed a dramatic increase in unemployment claims. The loss of high-paying jobs in these sectors had a multiplier effect, reducing consumer spending and further depressing local economies. Many Americans found themselves struggling to find new employment, as the job market became increasingly competitive, with fewer opportunities available.

The long-term implications of this unemployment crisis were significant. Many workers had to settle for lower-paying jobs or change careers entirely, leading to a skilled labor shortage in the financial sector once the economy began to recover. The psychological impact on individuals and families cannot be overstated, as prolonged unemployment often results in financial strain, stress, and a decline in overall well-being. Government intervention, through stimulus packages and unemployment benefits, provided some relief, but the road to recovery for those affected by bank-related job losses was often long and challenging. This period highlighted the vulnerability of certain sectors to economic shocks and the need for diverse employment opportunities to safeguard against such crises.

ExamSoft and NCLEX Test Banks: Are They Included Together?

You may want to see also

Explore related products

![]()

Access to Cash and Services: Limited cash withdrawals and reduced banking services disrupted daily financial activities

During the periods of bank closures, particularly those seen during the Great Depression and more recently during economic crises or pandemics, everyday Americans faced significant disruptions in their access to cash and essential banking services. One of the most immediate impacts was the imposition of limits on cash withdrawals. Banks, fearing a run on their reserves, often restricted how much money customers could withdraw daily or weekly. This limitation forced individuals to carefully ration their cash, making it difficult to cover routine expenses like groceries, rent, or medical bills. For those living paycheck to paycheck, this constraint exacerbated financial stress, as they could no longer rely on their savings to meet immediate needs.

Reduced banking services further compounded the challenges. Many banks cut back on operating hours or temporarily closed branches, leaving customers with fewer options to conduct in-person transactions. Services like check cashing, loan applications, and account management became harder to access, particularly for those in rural or underserved areas. This reduction in services disproportionately affected older adults and individuals without access to digital banking, as they relied heavily on physical bank locations for their financial needs. The inability to perform basic transactions disrupted daily life and added layers of inconvenience and uncertainty.

The limited access to cash also hindered small businesses and self-employed individuals, who often needed cash on hand to pay employees, purchase supplies, or manage day-to-day operations. Without sufficient liquidity, many were forced to delay payments or scale back their activities, leading to a ripple effect of economic hardship. Additionally, the inability to deposit cash or checks meant that income streams were interrupted, further straining financial stability. These disruptions underscored the critical role banks play in facilitating economic activity and highlighted the vulnerability of communities when such services are curtailed.

For families and individuals, the reduced access to cash and banking services often meant making difficult choices about how to allocate their limited funds. Prioritizing essential expenses like food and utilities became paramount, while discretionary spending was virtually eliminated. This shift in spending patterns not only affected personal budgets but also had broader implications for local economies, as reduced consumer spending impacted businesses and jobs. The psychological toll of financial uncertainty and the inability to plan for the future added another layer of stress, making the impact of bank closures far-reaching and deeply personal.

In response to these challenges, some Americans turned to alternative financial sources, such as payday lenders or informal borrowing networks, which often came with high costs and risks. Others relied on government assistance programs or community support systems, though these were not always sufficient to meet the scale of need. The experience of limited cash access and reduced banking services during bank closures highlighted the importance of a stable and accessible financial system in maintaining economic security and underscored the need for policies that protect consumers during times of crisis.

Height Requirements: Sperm Bank Donors' Unseen Criteria

You may want to see also

Explore related products

![]()

Small Business Struggles: Businesses faced difficulties accessing credit and managing cash flow, leading to closures

The wave of bank closures during the Great Depression had a devastating impact on small businesses across America. With banks shutting their doors, a critical lifeline for these enterprises was severed. Access to credit, essential for purchasing inventory, covering operational costs, and investing in growth, became nearly impossible. Small business owners, already struggling in a contracting economy, found themselves unable to secure loans or lines of credit. This meant they couldn't restock shelves, pay employees on time, or adapt to changing market demands. The inability to access credit effectively paralyzed many small businesses, forcing them to operate on a day-to-day basis, constantly teetering on the edge of collapse.

Without a reliable source of funding, managing cash flow became a herculean task. Customers, themselves facing financial hardship, were slow to pay invoices, further straining already tight budgets. Small businesses, often operating on thin margins, couldn't absorb these delays. They were forced to make difficult choices: lay off employees, reduce hours, or even close their doors permanently. The ripple effect was profound, as these closures meant lost jobs for local communities, reduced spending power, and a further decline in economic activity.

The impact wasn't limited to immediate financial struggles. The lack of credit also stifled innovation and growth. Small businesses, traditionally engines of innovation and job creation, were unable to invest in new products, expand their operations, or explore new markets. This stagnation had long-term consequences, hindering economic recovery and limiting opportunities for both business owners and their employees.

The human cost of these closures was immeasurable. For many, their small business was not just a source of income but a lifelong dream and a legacy to pass on. The loss of their livelihood meant financial ruin, shattered dreams, and a profound sense of uncertainty about the future. The emotional toll of seeing years of hard work disappear overnight was devastating, leaving deep scars on individuals and families.

The struggles of small businesses during this period highlight the crucial role banks play in the health of local economies. When banks fail, the consequences extend far beyond Wall Street. They reach into Main Street, affecting the livelihoods of ordinary Americans and the very fabric of communities. Understanding this interconnectedness is vital to preventing such devastating economic downturns in the future.

Green Dot Bank: Legit or a Scam?

You may want to see also

Explore related products

![]()

Housing Market Impact: Foreclosures rose as homeowners struggled to pay mortgages without banking support

The closure of banks during the Great Depression and other financial crises had a profound impact on the housing market, particularly in terms of foreclosures. As banks shut their doors, many homeowners found themselves without access to essential financial services, including mortgage support. This disruption created a cascade of challenges, making it increasingly difficult for families to keep up with their mortgage payments. Without the ability to withdraw savings, secure loans, or even deposit earnings, homeowners were left financially vulnerable. The sudden absence of banking services meant that even those who had been diligently managing their finances were now at risk of losing their homes.

Foreclosures began to rise sharply as homeowners defaulted on their mortgages. The inability to pay was not always a result of poor financial management but rather a direct consequence of the economic environment created by bank closures. With unemployment rates soaring and businesses failing, many Americans saw their incomes shrink or disappear entirely. Those who relied on banks for paycheck deposits or small loans to cover temporary shortfalls were particularly hard-pressed. The lack of liquidity in the financial system meant that there were no safety nets for homeowners, leading to a wave of foreclosures that destabilized communities and eroded household wealth.

The housing market impact extended beyond individual homeowners, affecting entire neighborhoods and local economies. As foreclosures increased, property values plummeted, creating a vicious cycle of declining home equity. This devaluation made it even harder for homeowners to refinance or sell their properties to avoid foreclosure. Additionally, vacant homes became more common, leading to neighborhood blight and reduced property tax revenues for local governments. The ripple effects of these foreclosures contributed to a broader economic downturn, as the housing market was a key pillar of the American economy.

Banks' inability to provide mortgage relief or restructuring options further exacerbated the situation. During normal economic times, lenders might offer modified payment plans or temporary forbearance to struggling homeowners. However, with banks closed or operating under severe restrictions, such options were largely unavailable. This lack of flexibility left homeowners with few alternatives to foreclosure. The emotional and financial toll on families was immense, as losing a home often meant the loss of personal belongings, community ties, and long-term financial stability.

In response to the crisis, government interventions eventually aimed to stabilize the housing market and provide relief to homeowners. Programs such as the Home Owners' Loan Corporation (HOLC) during the Great Depression offered refinancing options to prevent foreclosures. However, these measures came too late for many families who had already lost their homes. The lessons from this period underscored the critical role of banks in maintaining housing market stability and the need for robust financial systems to support homeowners during economic downturns. The impact of bank closures on foreclosures remains a stark reminder of the interconnectedness of financial institutions and everyday Americans' livelihoods.

Central Blood Banks: HIV Testing Protocols and Safety Measures Explained

You may want to see also

Explore related products

![]()

Consumer Confidence Decline: Trust in financial institutions plummeted, affecting spending and saving behaviors

The wave of bank closures during the Great Depression had a profound and immediate impact on consumer confidence, triggering a sharp decline in trust toward financial institutions. As banks shuttered their doors, often without warning, millions of Americans lost access to their savings, leaving them financially vulnerable and disillusioned. This sudden loss of wealth eroded faith in the banking system, as people realized that institutions they had trusted to safeguard their money could fail overnight. The resulting skepticism led many to question the stability and reliability of banks, fostering a deep-seated mistrust that would linger for years.

This plummeting trust directly influenced spending and saving behaviors across the nation. With uncertainty about the safety of their deposits, many Americans adopted a more cautious approach to finances. Instead of depositing money in banks, they began hoarding cash at home or investing in tangible assets like gold and real estate, which were perceived as safer stores of value. This shift away from traditional banking disrupted the flow of capital, as banks relied on deposits to fund loans and stimulate economic activity. As a result, the economy experienced a contraction in credit availability, further exacerbating the economic downturn.

Consumer spending also took a significant hit as households prioritized survival over discretionary purchases. Fear of further bank failures and economic instability led many to cut back on non-essential spending, focusing instead on essentials like food, shelter, and utilities. This reduction in consumer demand had a ripple effect across industries, causing businesses to reduce production, lay off workers, and close down. The decline in spending deepened the economic crisis, creating a vicious cycle of unemployment, poverty, and reduced purchasing power.

Saving behaviors were equally affected, as the trauma of bank closures reshaped financial attitudes. Many Americans became wary of saving in banks, opting instead to live hand-to-mouth or rely on informal lending networks. This aversion to formal financial institutions hindered long-term savings and investment, which are critical for economic growth and personal financial security. The lack of trust in banks also discouraged participation in financial markets, limiting opportunities for wealth accumulation and economic mobility.

In response to the crisis, the government introduced measures like the Federal Deposit Insurance Corporation (FDIC) to restore confidence in the banking system. However, the psychological scars of bank closures persisted, influencing financial behaviors for generations. The decline in consumer confidence underscored the importance of trust in maintaining economic stability, highlighting the need for robust regulatory frameworks to protect depositors and prevent future crises. Ultimately, the bank closures of the Great Depression served as a stark reminder of the interconnectedness of trust, spending, saving, and economic health.

How Banks Make Wild Cats Lazy

You may want to see also

Frequently asked questions

Bank closures during the Great Depression severely limited Americans' access to their savings, as many banks failed and depositors lost their money. Those who managed to withdraw funds before closures often hoarded cash, fearing further bank failures.

Bank closures led to a collapse in credit availability, forcing businesses to lay off workers or shut down entirely. This exacerbated unemployment and deepened the economic crisis for everyday Americans.

With limited access to money and widespread fear of further economic instability, Americans drastically reduced spending. This decline in consumer demand further weakened the economy and prolonged the Depression.

Yes, rural Americans were particularly hard-hit because they relied heavily on local banks for agricultural loans. Urban Americans faced similar challenges but had slightly more access to alternative financial resources in larger cities.

The U.S. government established the Federal Deposit Insurance Corporation (FDIC) in 1933 to insure bank deposits, restoring public confidence and preventing future bank runs. This measure helped stabilize the banking system and protect everyday Americans' savings.

![Principles of Political Economy and Taxation [1911 Edition]](https://m.media-amazon.com/images/I/81Xx2WBrKnL._AC_UL320_.jpg)