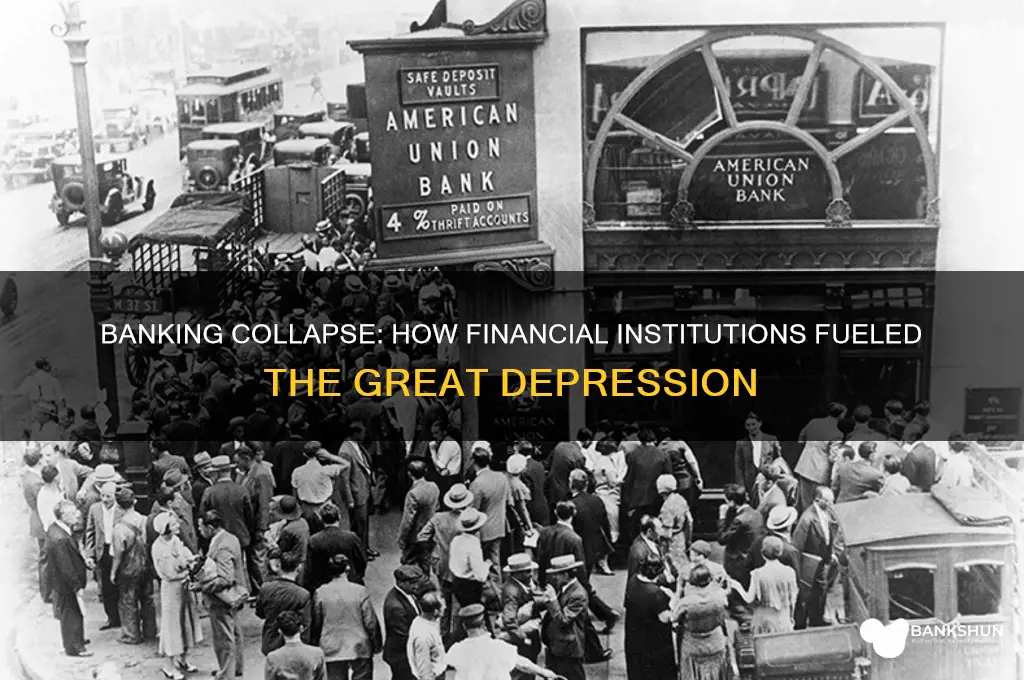

The Great Depression, a period of severe economic downturn in the 1930s, was significantly influenced by the actions and vulnerabilities of banks. In the years leading up to the crisis, banks engaged in speculative lending, particularly in the stock market and real estate, which created an unsustainable bubble. When the stock market crashed in 1929, banks faced a wave of loan defaults and a loss of depositor confidence, leading to widespread bank runs. The lack of deposit insurance and a fragile banking system exacerbated the panic, causing thousands of banks to fail. These bank failures wiped out savings, reduced credit availability, and deepened the economic contraction, as businesses and consumers struggled to access funds. The collapse of the banking sector not only accelerated the onset of the Great Depression but also prolonged its effects, highlighting the critical role of financial institutions in economic stability.

Explore related products

What You'll Learn

![]()

Bank failures and panic

The scale of bank failures during the Great Depression was unprecedented. Between 1929 and 1933, over 9,000 banks failed in the United States, wiping out billions of dollars in assets and erasing the savings of millions of Americans. These failures were not isolated incidents but part of a vicious cycle. Each bank closure eroded public trust further, fueling more panic and runs on other banks. The loss of banking institutions also meant that credit became scarce, stifling businesses and consumers who relied on loans to operate and spend. Without access to credit, businesses were forced to lay off workers or shut down entirely, exacerbating unemployment and economic contraction.

The banking crisis also had a profound psychological impact on the public. The sight of bank closures and long lines of desperate depositors created a sense of economic insecurity that discouraged spending and investment. Families and businesses hoarded cash instead of depositing it in banks or spending it in the economy, further reducing economic activity. This hoarding behavior deepened the deflationary spiral, as falling prices and wages made it even harder for borrowers to repay debts, leading to more defaults and bank failures.

Government responses to the banking panic were initially inadequate, worsening the situation. The Federal Reserve, tasked with stabilizing the financial system, failed to act decisively to provide liquidity to struggling banks or prevent runs. Additionally, the absence of federal deposit insurance meant that depositors had no guarantee their savings would be protected if their bank failed. It was not until 1933, when President Franklin D. Roosevelt declared a nationwide bank holiday and signed the Emergency Banking Act, that steps were taken to restore confidence. The subsequent creation of the Federal Deposit Insurance Corporation (FDIC) provided much-needed assurance to depositors, but by then, the damage from years of bank failures and panic had already been done.

In summary, bank failures and panic were critical factors in the severity of the Great Depression. The collapse of thousands of banks eroded public trust, destroyed savings, and tightened credit, choking economic activity. The psychological impact of these failures deepened the crisis, as fear and uncertainty led to reduced spending and investment. The initial lack of effective government intervention allowed the banking panic to spiral out of control, highlighting the need for stronger regulatory measures and deposit insurance. The lessons from this period underscore the importance of a stable banking system in maintaining economic health and the dangers of unchecked financial instability.

Zelle and Taxes: What the IRS Knows

You may want to see also

Explore related products

![]()

Credit contraction impact

The Great Depression was a period of severe economic downturn that began with the stock market crash of 1929 and lasted throughout the 1930s. One of the most significant ways banks exacerbated this crisis was through credit contraction, a process where the availability of loans and credit sharply decreased. During the 1920s, banks had expanded credit aggressively, fueling speculation in stocks and real estate. However, when the stock market crashed, banks faced widespread defaults on loans, leading them to adopt a more conservative lending approach. This sudden reduction in credit availability had a cascading effect on the economy, as businesses and consumers found it increasingly difficult to secure financing for operations, investments, or purchases.

The impact of credit contraction was particularly devastating for businesses, which relied heavily on bank loans to fund their operations and expansion. As banks tightened lending standards and called in outstanding loans, many businesses were forced to halt production, lay off workers, or declare bankruptcy. This, in turn, led to a sharp decline in industrial output and employment, further deepening the economic crisis. Small and medium-sized enterprises, which were less likely to have access to alternative sources of capital, were hit the hardest. The reduction in business activity also reduced tax revenues for governments, limiting their ability to implement stimulus measures or provide relief to struggling citizens.

Credit contraction also severely affected consumers, who found it nearly impossible to obtain loans for homes, automobiles, or other major purchases. This decline in consumer spending further weakened demand for goods and services, creating a vicious cycle of economic decline. As unemployment soared, households defaulted on existing loans, leading to additional bank losses and further tightening of credit. The housing market, in particular, suffered as mortgage lending dried up, causing home prices to plummet and construction activity to grind to a halt. This contraction in consumer credit not only deepened the Depression but also prolonged it, as the economy struggled to recover without the stimulus of consumer spending.

Another critical impact of credit contraction was the wave of bank failures it triggered. As businesses and consumers defaulted on loans, banks faced mounting losses and liquidity shortages. Between 1929 and 1933, over 9,000 banks failed in the United States, erasing billions of dollars in assets and destroying public confidence in the banking system. These failures further reduced the availability of credit, as surviving banks became even more risk-averse. The loss of deposits also wiped out the savings of millions of Americans, exacerbating poverty and reducing economic activity. The banking crisis deepened the Depression by undermining the financial infrastructure necessary for economic recovery.

Finally, the credit contraction had long-lasting effects on monetary policy and economic behavior. The Federal Reserve, which had failed to prevent the initial contraction, faced criticism for its inaction and lack of coordination. The crisis highlighted the need for a more proactive and stabilizing role for central banks in managing credit and liquidity. In response, the U.S. government implemented reforms such as the Glass-Steagall Act and the creation of the Federal Deposit Insurance Corporation (FDIC) to restore confidence in the banking system and prevent future contractions. However, the psychological scars of the Great Depression led to a more conservative approach to borrowing and lending, which persisted for decades and influenced economic behavior long after the Depression ended.

Exploring Barclays' Massive Assets: How Big is This Global Bank?

You may want to see also

Explore related products

![]()

Gold standard role

The Gold Standard played a pivotal role in exacerbating the banking crisis during the Great Depression. Under the Gold Standard, a country's currency was directly linked to a specific quantity of gold, ensuring fixed exchange rates between participating nations. This system, while intended to foster stability, became a rigid constraint during economic downturns. When the Great Depression hit, the demand for gold surged as investors sought a safe haven, leading to massive gold outflows from banks. This forced central banks to contract their money supply to maintain the gold-currency peg, which in turn reduced liquidity and tightened credit. The resulting scarcity of money deepened deflation, making it harder for borrowers to repay loans and triggering widespread bank runs.

Bank runs were a direct consequence of the Gold Standard's inflexibility. As depositors lost confidence in banks' ability to honor withdrawals, they rushed to convert their currency into gold or withdraw cash, depleting bank reserves. The Gold Standard prevented central banks from expanding the money supply to alleviate this pressure, as doing so would have risked devaluing the currency and breaking the gold peg. This inability to act as a lender of last resort left banks vulnerable to insolvency. For instance, in the United States, the Federal Reserve's adherence to the Gold Standard limited its capacity to inject liquidity into the banking system, contributing to the collapse of thousands of banks between 1929 and 1933.

Internationally, the Gold Standard amplified the global nature of the crisis. As countries struggled to maintain their gold reserves, they were forced to implement austerity measures, such as raising interest rates and cutting government spending, to balance their trade accounts. These deflationary policies not only deepened domestic economic woes but also reduced global trade, as nations prioritized protecting their gold stocks over international commerce. The interconnectedness of the Gold Standard meant that a financial shock in one country quickly spread to others, creating a vicious cycle of bank failures and economic contraction worldwide.

The eventual abandonment of the Gold Standard marked a turning point in the recovery from the Great Depression. Countries that left the Gold Standard earlier, such as the United Kingdom in 1931, were able to devalue their currencies, increase their money supply, and stimulate economic activity. This flexibility allowed central banks to act more decisively in stabilizing their banking systems and restoring public confidence. In contrast, nations that clung to the Gold Standard longer, like the United States until 1933, experienced more prolonged and severe banking crises. The Gold Standard's role in the Great Depression underscored the need for more adaptable monetary systems that could respond to economic shocks without triggering widespread financial collapse.

In summary, the Gold Standard's rigid framework significantly contributed to the banking crisis during the Great Depression. Its requirement for fixed gold-currency ratios constrained central banks' ability to manage liquidity, leading to deflation, bank runs, and global economic contagion. The system's eventual abandonment highlighted the importance of monetary flexibility in mitigating financial crises and laid the groundwork for modern central banking practices. Understanding the Gold Standard's role provides critical insights into how monetary policies can either stabilize or destabilize economies during times of distress.

The Bank of New York Mellon: A Comprehensive Overview

You may want to see also

Explore related products

![]()

Federal Reserve policies

The Federal Reserve's policies played a pivotal role in the onset and deepening of the Great Depression, primarily through their mismanagement of the money supply and banking system. Established in 1913 to stabilize the financial system, the Federal Reserve initially failed to act as a lender of last resort during the early stages of the crisis. As bank runs escalated in the late 1920s and early 1930s, the Fed did not inject sufficient liquidity into the banking system, allowing thousands of banks to fail. This widespread bank failure eroded public confidence, led to a sharp reduction in the money supply, and severely contracted credit availability. Without access to loans, businesses were forced to lay off workers or shut down, exacerbating unemployment and economic contraction.

One of the most criticized Federal Reserve policies was its adherence to the gold standard, which constrained its ability to expand the money supply. The gold standard required the Fed to back currency with gold reserves, limiting its capacity to print money or engage in expansive monetary policies. As the global economy deteriorated, the demand for gold increased, leading to deflationary pressures in the U.S. economy. The Fed's failure to counteract deflation by increasing the money supply further depressed prices, wages, and economic activity. This deflationary spiral made debts more burdensome for borrowers, leading to widespread defaults and further bank failures.

Additionally, the Federal Reserve's decision to raise interest rates in 1928 and 1929 to curb stock market speculation had unintended consequences. While the move aimed to cool an overheated stock market, it also tightened credit conditions for businesses and consumers. Higher interest rates reduced investment and spending, contributing to the economic slowdown. When the stock market crashed in October 1929, the Fed's tight monetary policy exacerbated the crisis by limiting the availability of credit needed to stabilize financial markets and support economic activity.

The Fed's lack of coordination with other central banks also contributed to the global spread of the Depression. As European countries faced financial crises, they repatriated gold from the U.S., further restricting the Fed's ability to expand the money supply. This international gold flow intensified deflationary pressures and deepened the economic downturn. The Fed's failure to collaborate with other central banks to stabilize the international financial system allowed the crisis to escalate into a global depression.

Finally, the Federal Reserve's inaction during the early years of the Depression allowed the banking crisis to worsen. Instead of providing emergency lending to struggling banks, the Fed allowed many to fail, leading to a collapse of the banking system. It was not until the establishment of the Reconstruction Finance Corporation in 1932 and the adoption of more expansionary policies under President Roosevelt that efforts were made to stabilize the banking sector. By then, however, the damage was done, and the economy had already suffered years of severe contraction. The Fed's initial policy failures underscored the need for more proactive and flexible monetary management in future crises.

Understanding Employee Preferences: Banked vs. Accrued PTO

You may want to see also

Explore related products

![]()

Banking system reforms

The Great Depression exposed critical vulnerabilities in the banking system, which played a significant role in both the onset and the severity of the crisis. In response, sweeping banking system reforms were implemented to restore confidence, stabilize financial institutions, and prevent future economic collapses. These reforms focused on regulation, deposit insurance, and structural changes to ensure banks operated more responsibly and transparently.

One of the most pivotal reforms was the establishment of the Federal Deposit Insurance Corporation (FDIC) in 1933. Prior to the Great Depression, bank runs were rampant as depositors feared losing their savings if a bank failed. The FDIC introduced deposit insurance, guaranteeing individual deposits up to a certain amount, which immediately restored public confidence in the banking system. This measure significantly reduced bank runs and provided a safety net for depositors, ensuring that a loss of confidence in one bank would not trigger a systemic collapse.

Another critical reform was the passage of the Glass-Steagall Act in 1933, which separated commercial and investment banking activities. Before the Depression, banks engaged in speculative investments with depositors' funds, leading to excessive risk-taking and instability. Glass-Steagall mandated that banks choose between commercial banking (accepting deposits and making loans) and investment banking (underwriting securities). This separation aimed to protect depositors' funds from being used for high-risk ventures and to prevent conflicts of interest within financial institutions.

The creation of the Securities and Exchange Commission (SEC) in 1934 was another cornerstone of banking system reforms. The SEC was tasked with regulating the stock market and ensuring transparency in financial transactions. During the 1920s, unchecked speculation and fraudulent practices had contributed to the stock market crash of 1929. The SEC introduced regulations requiring companies to disclose financial information, preventing insider trading, and enforcing fair practices. This restored investor confidence and reduced the likelihood of market manipulation.

Additionally, the Federal Reserve’s role was strengthened to better manage monetary policy and oversee the banking system. The Banking Act of 1935 enhanced the Fed’s authority to regulate banks and control the money supply, enabling it to respond more effectively to economic crises. The Fed was also given greater oversight over member banks, ensuring compliance with regulations and promoting financial stability. These measures aimed to prevent the excessive credit expansion and speculative lending that had fueled the economic bubble leading up to the Depression.

Finally, reforms emphasized the need for stricter capital requirements and risk management practices for banks. By mandating that banks maintain a certain level of capital relative to their assets, regulators aimed to ensure that banks had sufficient buffers to absorb losses during economic downturns. This reduced the likelihood of bank failures and minimized the risk of contagion across the financial system. Together, these banking system reforms laid the foundation for a more resilient and accountable financial sector, addressing the root causes of the Great Depression and safeguarding against future crises.

How Banks Are Safeguarding Users Against Fraudulent Activities

You may want to see also

Frequently asked questions

Bank failures during the Great Depression eroded public confidence in the financial system, leading to widespread panic and bank runs. As banks collapsed, depositors lost their savings, and the money supply contracted sharply, reducing consumer spending and investment, which deepened the economic downturn.

The Federal Reserve failed to act as a lender of last resort during the early stages of the crisis, allowing thousands of banks to fail. Additionally, the Fed's tight monetary policies, such as raising interest rates, restricted credit availability, further stifling economic activity and exacerbating the Depression.

The instability in the banking system made it difficult for businesses to obtain loans, leading to reduced production, layoffs, and widespread unemployment. Without access to credit, businesses could not invest in growth or maintain operations, contributing to the economic collapse.

After the Great Depression, the U.S. government implemented reforms like the Glass-Steagall Act (1933), which separated commercial and investment banking, and established the Federal Deposit Insurance Corporation (FDIC) to insure deposits, restoring public trust and preventing bank runs. These measures aimed to stabilize the banking system and prevent similar crises.