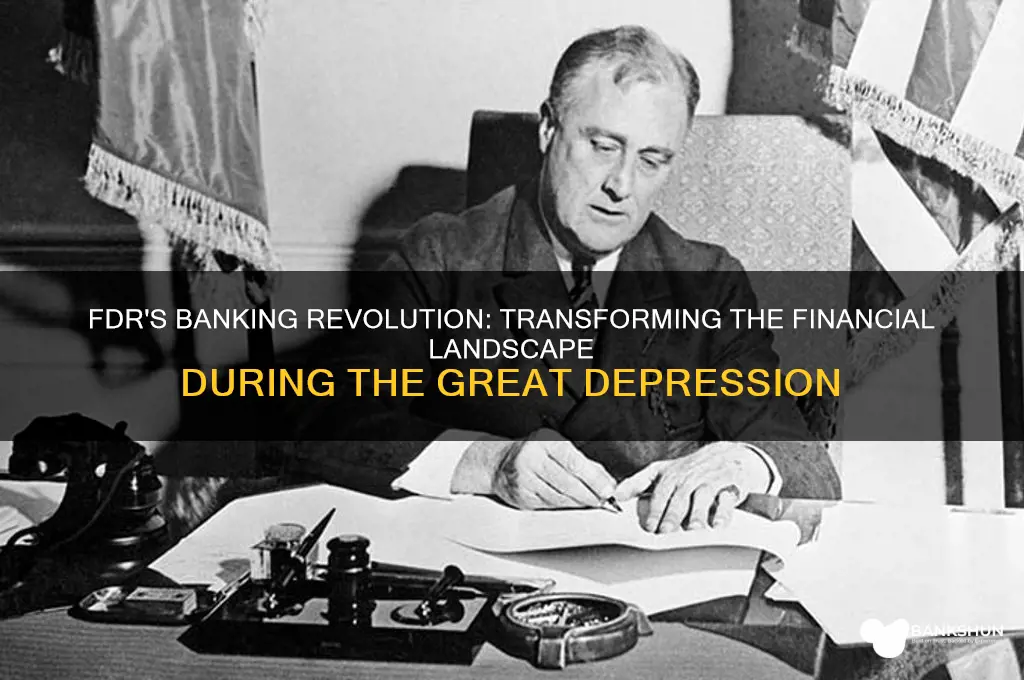

Franklin D. Roosevelt's reform of the banking industry during the Great Depression was a pivotal response to the widespread bank failures and financial panic that gripped the nation in early 1933. Upon taking office, FDR declared a national bank holiday, temporarily closing all banks to prevent further collapses and restore public confidence. This bold move was followed by the passage of the Emergency Banking Act, which allowed solvent banks to reopen and provided federal support to stabilize the system. FDR also signed the Glass-Steagall Act, which separated commercial and investment banking, established the Federal Deposit Insurance Corporation (FDIC) to insure deposits, and implemented stricter regulations to prevent reckless banking practices. These measures not only restored trust in the financial system but also laid the foundation for a more secure and regulated banking industry in the United States.

| Characteristics | Values |

|---|---|

| Emergency Banking Act (1933) | Authorized the Treasury Secretary to inspect banks and reopen solvent ones; restored confidence. |

| Federal Deposit Insurance Corporation (FDIC) | Created to insure bank deposits up to $5,000 (later increased), preventing bank runs. |

| Glass-Steagall Act (1933) | Separated commercial and investment banking to reduce risky speculation. |

| Securities Act (1933) | Required companies to provide accurate financial information when issuing securities. |

| Securities Exchange Act (1934) | Established the SEC to regulate stock markets and prevent fraud. |

| Truth in Securities Act | Mandated full disclosure of company finances to protect investors. |

| Banking Act (1935) | Strengthened the Federal Reserve's oversight and restricted bank affiliations. |

| Deposit Insurance Limit Increase | Initially $5,000, now $250,000 per depositor per insured bank (as of latest FDIC data). |

| Regulation of Speculative Practices | Prohibited banks from underwriting securities to minimize risk. |

| Public Confidence Restoration | FDR's fireside chats and reforms restored trust in the banking system. |

Explore related products

What You'll Learn

- Emergency Banking Act (1933): Temporary closure, inspection, and reopening of solvent banks to restore public trust

- FDIC Creation: Established Federal Deposit Insurance Corporation to insure deposits up to $5,000

- Glass-Steagall Act (1933): Separated commercial and investment banking to reduce risky financial practices

- Banking Act (1935): Strengthened Federal Reserve’s oversight and regulated bank branching and competition

- Securities Acts (1933-1934): Required registration and disclosure for securities to protect investors from fraud

![]()

Emergency Banking Act (1933): Temporary closure, inspection, and reopening of solvent banks to restore public trust

The Emergency Banking Act (1933) was a pivotal measure enacted by President Franklin D. Roosevelt (FDR) to address the banking crisis that had gripped the nation during the Great Depression. The act was part of FDR’s broader strategy to stabilize the financial system and restore public confidence in banks. At the time of its passage, thousands of banks had failed, and panicked depositors were withdrawing their funds en masse, exacerbating the crisis. The act’s primary goal was to distinguish between solvent and insolvent banks, ensuring that only financially viable institutions reopened, thereby safeguarding the public’s money and trust.

Under the Emergency Banking Act, FDR declared a four-day nationwide bank holiday, during which all banks were temporarily closed. This immediate action halted the bank runs and provided a critical pause to assess the financial health of each institution. During this period, federal inspectors worked swiftly to examine bank records, determine solvency, and identify which banks could safely reopen. The act authorized the Treasury Department and the Federal Reserve to provide emergency loans to solvent banks, enabling them to resume operations with sufficient liquidity to meet depositor demands. This process was designed to weed out weak banks while ensuring that sound institutions could continue serving the public.

The reopening of solvent banks was a carefully orchestrated process aimed at restoring public trust. FDR’s famous fireside chat on March 12, 1933, played a crucial role in this effort. He explained the purpose of the bank holiday and reassured Americans that their money was safe in reopened banks. By the end of the first week, thousands of banks had been inspected, and the majority of solvent banks reopened to the public. This swift action demonstrated the government’s commitment to stabilizing the banking system and protecting depositors, which was essential for rebuilding confidence in financial institutions.

The Emergency Banking Act also laid the groundwork for longer-term reforms by addressing immediate crises while signaling the government’s willingness to intervene in the banking sector. It was a precursor to the establishment of the Federal Deposit Insurance Corporation (FDIC) later in 1933, which provided permanent deposit insurance to prevent future bank runs. By temporarily closing, inspecting, and reopening solvent banks, the act not only resolved the immediate crisis but also set the stage for a more resilient banking system. FDR’s decisive action under this act marked a turning point in the Great Depression, as it halted the financial freefall and began the process of economic recovery.

In summary, the Emergency Banking Act (1933) was a bold and effective measure to restore public trust in the banking system during one of the darkest periods in American economic history. Through the temporary closure, inspection, and reopening of solvent banks, FDR’s administration demonstrated its ability to act swiftly and decisively in the face of crisis. This act not only stabilized the banking sector but also paved the way for enduring reforms that continue to shape the U.S. financial system today. Its success underscored the importance of government intervention in times of economic turmoil and remains a cornerstone of FDR’s legacy in reforming the banking industry.

Axis Bank: US Visa Fee Payment Options

You may want to see also

Explore related products

![]()

FDIC Creation: Established Federal Deposit Insurance Corporation to insure deposits up to $5,000

In response to the widespread bank failures during the Great Recession, President Franklin D. Roosevelt (FDR) took swift action to restore public confidence in the banking system. One of the most significant reforms was the creation of the Federal Deposit Insurance Corporation (FDIC) as part of the Emergency Banking Act of 1933 and further solidified by the Banking Act of 1935. The primary purpose of the FDIC was to provide a safety net for depositors by insuring their funds, thereby preventing the panic-induced bank runs that had become all too common. Initially, the FDIC insured deposits up to $5,000, a substantial amount at the time, which reassured small depositors that their savings were secure. This measure was crucial in stabilizing the banking sector and encouraging people to return their money to banks, which in turn helped to revive the economy.

The establishment of the FDIC marked a fundamental shift in the relationship between banks, depositors, and the federal government. Prior to its creation, depositors bore the risk of bank failures, often losing their entire savings if a bank collapsed. By insuring deposits, the FDIC transferred this risk to the federal government, which had the resources to absorb losses and protect individual depositors. The $5,000 insurance limit was carefully chosen to cover the majority of small depositors while ensuring the FDIC’s financial viability. This limit was a practical compromise that balanced the need for broad protection with the constraints of the federal budget during a time of economic crisis.

The FDIC’s creation was not just about insuring deposits; it was also about restoring trust in the banking system. FDR understood that economic recovery depended on a stable financial system, and the FDIC played a pivotal role in achieving this stability. By guaranteeing deposits, the FDIC eliminated the fear that had driven bank runs, allowing banks to operate with greater predictability and security. This, in turn, enabled banks to lend more freely, which was essential for businesses and individuals to access credit and stimulate economic growth. The FDIC’s insurance program became a cornerstone of FDR’s broader efforts to reform the banking industry and lay the foundation for a more resilient financial system.

Implementing the FDIC required a robust regulatory framework to ensure its effectiveness. Banks were required to become members of the FDIC and pay insurance premiums into the Deposit Insurance Fund (DIF), which would be used to compensate depositors in case of bank failures. This system created a self-sustaining mechanism where banks collectively funded the insurance pool, reducing the burden on taxpayers. The $5,000 insurance limit was periodically reviewed and adjusted over the years to reflect changes in the economy, but its initial establishment was a critical step in providing immediate relief to depositors and stabilizing the banking sector.

The impact of the FDIC’s creation extended far beyond its immediate effects on depositors. It represented a fundamental rethinking of the government’s role in financial regulation and consumer protection. By insuring deposits up to $5,000, the FDIC not only safeguarded individual savings but also fostered a culture of trust and confidence in the banking system. This trust was essential for the long-term health of the economy, as it encouraged savings, investment, and economic activity. FDR’s decision to establish the FDIC remains one of the most enduring and effective reforms of the banking industry, shaping the financial landscape for generations to come.

Banking Experts: Who to See and When

You may want to see also

Explore related products

![]()

Glass-Steagall Act (1933): Separated commercial and investment banking to reduce risky financial practices

The Glass-Steagall Act of 1933 stands as one of the most significant pieces of legislation enacted during Franklin D. Roosevelt’s (FDR) administration to reform the banking industry in the wake of the Great Depression. The act’s primary purpose was to address the widespread bank failures and financial instability that had plagued the nation by separating commercial and investment banking activities. Prior to Glass-Steagall, banks often engaged in both commercial banking (accepting deposits and making loans) and investment banking (underwriting securities and engaging in speculative trading). This dual role created conflicts of interest and encouraged risky practices, as banks used depositors’ funds to underwrite speculative investments, often leading to significant losses when the market crashed.

Glass-Steagall directly tackled this issue by erecting a firewall between commercial and investment banking. Commercial banks were restricted to traditional banking activities, such as accepting deposits, making loans, and providing checking accounts, while investment banks were limited to underwriting securities, facilitating mergers, and trading in financial markets. This separation was designed to protect depositors’ funds from the inherent risks of investment banking. By prohibiting commercial banks from using customer deposits for speculative activities, the act aimed to restore public confidence in the banking system and prevent the kind of financial contagion that had led to thousands of bank failures in the early 1930s.

The act also established the Federal Deposit Insurance Corporation (FDIC), which insured bank deposits up to a certain amount, further stabilizing the banking system. This insurance provided a safety net for depositors, assuring them that their money was secure even if their bank failed. Combined with the separation of banking activities, the FDIC played a crucial role in restoring trust in the financial system. Glass-Steagall’s provisions were enforced through strict regulatory oversight, ensuring that banks complied with the new rules and did not engage in prohibited activities.

Critics of the banking practices prior to Glass-Steagall argued that the lack of separation between commercial and investment banking had contributed to the speculative excesses of the 1920s, which ultimately led to the stock market crash of 1929 and the ensuing Depression. By separating these functions, the act sought to prevent banks from taking on excessive risk and to ensure that their primary focus remained on serving the needs of ordinary depositors and borrowers. This reform was a cornerstone of FDR’s broader efforts to stabilize the economy and protect consumers from predatory financial practices.

The Glass-Steagall Act remained in effect for over six decades, shaping the American financial landscape until its partial repeal in 1999. During its tenure, it successfully reduced risky banking practices and contributed to a period of relative financial stability. Its legacy continues to influence discussions about financial regulation, particularly in the aftermath of the 2008 financial crisis, when many argued for a return to stricter separation between commercial and investment banking. FDR’s implementation of Glass-Steagall remains a testament to his administration’s commitment to reforming the banking industry and safeguarding the economy from the dangers of unchecked financial speculation.

Bank Branches: How and Why They Work

You may want to see also

Explore related products

![]()

Banking Act (1935): Strengthened Federal Reserve’s oversight and regulated bank branching and competition

The Banking Act of 1935, also known as the Banking Act of 1935: Strengthened Federal Reserves oversight and regulated bank branching and competition, was a pivotal piece of legislation enacted during Franklin D. Roosevelt's (FDR) New Deal era. This act built upon the earlier Glass-Steagall Act of 1933, which had established the Federal Deposit Insurance Corporation (FDIC) and separated commercial and investment banking. The 1935 Act further solidified the federal government's role in regulating the banking industry, with a particular focus on enhancing the Federal Reserve's authority and addressing issues related to bank branching and competition.

One of the primary objectives of the Banking Act of 1935 was to strengthen the Federal Reserve's oversight capabilities. The act granted the Federal Reserve greater authority to regulate member banks, including the power to examine their financial condition, approve mergers and acquisitions, and set reserve requirements. This increased oversight aimed to prevent the excessive risk-taking and speculative practices that had contributed to the banking crises of the early 1930s. By empowering the Federal Reserve to more effectively monitor and regulate banks, the act sought to promote financial stability and prevent future bank failures.

In addition to bolstering Federal Reserve oversight, the Banking Act of 1935 also addressed the issue of bank branching. Prior to the act, state laws had restricted the ability of banks to establish branches, often limiting them to a single location. This had resulted in a highly fragmented banking system, with numerous small, local banks operating in isolation. The 1935 Act authorized the Federal Reserve to approve bank branching applications, allowing banks to expand their operations and serve a wider geographic area. However, the act also imposed restrictions on branching to prevent the creation of banking monopolies and ensure fair competition. Banks were required to obtain Federal Reserve approval for new branches, and the act established criteria for evaluating branching applications, including the financial condition of the bank, the need for additional banking services in the community, and the potential impact on competition.

The regulation of bank competition was another key aspect of the Banking Act of 1935. The act sought to prevent unfair competitive practices, such as predatory pricing and excessive risk-taking, which could undermine the stability of the banking system. To achieve this, the act granted the Federal Reserve the authority to regulate interest rates, establish fair lending practices, and enforce anti-trust laws in the banking industry. The act also prohibited banks from engaging in certain types of speculative activities, such as investing in stocks and other risky assets. By regulating competition and promoting fair practices, the act aimed to create a level playing field for banks and protect the interests of depositors and consumers.

Furthermore, the Banking Act of 1935 established the Federal Open Market Committee (FOMC), which is responsible for overseeing the Federal Reserve's open market operations, including the buying and selling of government securities. The FOMC plays a crucial role in implementing monetary policy, and its creation marked a significant step towards centralizing control over the money supply and credit conditions. The act also required the Federal Reserve to submit regular reports to Congress, enhancing transparency and accountability in the central banking system. Overall, the Banking Act of 1935 represented a comprehensive effort to reform the banking industry, strengthen Federal Reserve oversight, and promote a more stable and competitive banking environment. By addressing issues related to bank branching, competition, and regulation, the act helped to restore public confidence in the banking system and laid the foundation for a more resilient financial sector.

The impact of the Banking Act of 1935 was far-reaching, shaping the development of the U.S. banking system for decades to come. The act's provisions on Federal Reserve oversight, bank branching, and competition regulation helped to prevent future banking crises and promote financial stability. Moreover, the act's emphasis on transparency, accountability, and fair practices contributed to a more trustworthy and efficient banking system. As a key component of FDR's New Deal reforms, the Banking Act of 1935 demonstrated the federal government's commitment to addressing the underlying causes of the Great Depression and creating a more robust and equitable financial system. By strengthening the Federal Reserve's role and regulating bank branching and competition, the act played a vital role in restoring the health of the U.S. banking industry and supporting economic recovery.

Venmo's Banking Partner: What You Need to Know

You may want to see also

![]()

Securities Acts (1933-1934): Required registration and disclosure for securities to protect investors from fraud

The Securities Acts of 1933 and 1934 were cornerstone reforms enacted during Franklin D. Roosevelt’s administration to restore investor confidence and stabilize the financial system following the 1929 stock market crash. The Securities Act of 1933, also known as the "Truth in Securities" law, mandated that companies issuing securities (stocks and bonds) must register with the federal government and provide detailed information about their operations, financial condition, and the securities being offered. This requirement aimed to ensure that investors had access to accurate and complete information before making investment decisions, thereby protecting them from fraudulent schemes and misleading practices that were rampant in the 1920s.

The Securities Exchange Act of 1934 built upon the 1933 Act by establishing the Securities and Exchange Commission (SEC), a federal agency tasked with enforcing securities laws and regulating the securities industry. The 1934 Act required companies with publicly traded securities to disclose regular and ongoing financial information, such as quarterly and annual reports. This transparency was designed to prevent insider trading, market manipulation, and other fraudulent activities that had eroded trust in the financial markets. By holding companies accountable for their disclosures, the Act aimed to create a fair and informed trading environment for all investors.

A key provision of these Acts was the anti-fraud provisions, which explicitly prohibited deceptive practices in the sale and trading of securities. This included false statements, material misrepresentations, and omissions of critical information. The SEC was empowered to investigate and prosecute violations, imposing penalties on individuals and companies engaged in fraudulent behavior. These measures were instrumental in deterring the kind of speculative excesses and deceitful practices that had contributed to the market crash and subsequent Great Depression.

The Securities Acts also introduced registration requirements for brokers and dealers, ensuring that only qualified and regulated professionals could participate in the securities market. This helped to weed out unscrupulous operators and establish a more professional and ethical industry. Additionally, the Acts required prospectus disclosures for new securities offerings, providing investors with detailed information about the investment risks, management backgrounds, and financial health of the issuing companies. This level of transparency was unprecedented and marked a significant shift toward investor protection.

In summary, the Securities Acts of 1933 and 1934 were pivotal in FDR’s banking and financial reforms, addressing the root causes of market instability and investor distrust. By mandating registration, disclosure, and ongoing transparency, these Acts established a regulatory framework that protected investors from fraud and ensured the integrity of the securities markets. The creation of the SEC further institutionalized these reforms, providing a permanent mechanism for oversight and enforcement. Together, these measures laid the foundation for a more stable and trustworthy financial system, which remains a cornerstone of U.S. financial regulation today.

Does the World Bank Group Offer Internet Service Provider Support?

You may want to see also

Frequently asked questions

FDR reformed the banking industry by declaring a nationwide "bank holiday" in March 1933 to prevent further bank runs and stabilize the financial system. He also signed the Emergency Banking Act, which allowed solvent banks to reopen and provided federal support to struggling institutions.

The Glass-Steagall Act of 1933 separated commercial and investment banking to prevent conflicts of interest and risky speculation. It also established the Federal Deposit Insurance Corporation (FDIC) to insure bank deposits, restoring public confidence in the banking system.

FDR's reforms addressed bank failures by creating the FDIC, which insured deposits up to $5,000 (later increased), reducing the risk of bank runs. Additionally, the Emergency Banking Act and the Reconstruction Finance Corporation provided federal assistance to stabilize banks and restore trust in the financial system.

FDR's banking reforms established a regulatory framework that ensured greater stability and accountability in the financial system. The FDIC, Glass-Steagall Act, and other measures restored public confidence, prevented widespread bank failures, and laid the foundation for modern banking regulations in the United States.