The Dust Bowl, a severe drought and dust storm disaster that ravaged the American and Canadian prairies during the 1930s, had profound and far-reaching consequences, particularly on the banking sector. As farmers struggled to maintain their livelihoods amidst crop failures and soil erosion, many were unable to repay loans, leading to widespread bank failures across the affected regions. The financial strain on agricultural communities resulted in a significant increase in loan defaults, which, in turn, eroded banks' capital reserves and undermined public confidence in the banking system. This crisis exacerbated the ongoing Great Depression, forcing many banks to close their doors and leaving farmers and rural communities with limited access to credit, further deepening the economic hardship of the era.

| Characteristics | Values |

|---|---|

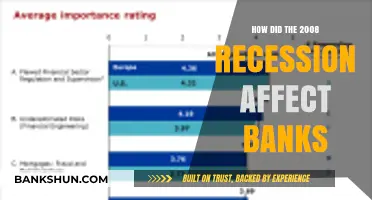

| Bank Failures | The Dust Bowl, combined with the Great Depression, led to a significant increase in bank failures. Between 1929 and 1933, over 9,000 banks failed in the United States, many in agricultural regions affected by the Dust Bowl. |

| Loan Defaults | Farmers were unable to repay loans due to crop failures and declining land values, leading to widespread loan defaults. This eroded banks' capital and liquidity. |

| Depositor Withdrawals | Panic and economic uncertainty caused depositors to withdraw funds, further straining banks' liquidity and contributing to bank runs. |

| Agricultural Loan Exposure | Banks heavily exposed to agricultural loans suffered disproportionately as farm incomes plummeted, leading to higher delinquency rates and losses. |

| Decline in Asset Values | Land values in affected areas dropped sharply, reducing the collateral value of loans and weakening banks' balance sheets. |

| Government Interventions | The Emergency Banking Act (1933) and the establishment of the FDIC helped stabilize the banking system by insuring deposits and restoring public confidence. |

| Long-Term Economic Impact | The Dust Bowl exacerbated the economic downturn, prolonging the recovery of banks and the broader financial system. |

| Migration and Local Economies | Mass migration from Dust Bowl regions reduced local economic activity, further diminishing bank deposits and lending opportunities. |

| Regulatory Changes | The crisis led to stricter banking regulations and oversight to prevent future collapses, including the Glass-Steagall Act (1933). |

| Recovery Timeline | Banks in affected regions took longer to recover compared to those in less impacted areas, reflecting the severity of local economic conditions. |

Explore related products

$17.16 $19.99

What You'll Learn

![]()

Bank closures due to farmer loan defaults during the Dust Bowl

The Dust Bowl, a period of severe dust storms and drought in the 1930s, had a devastating impact on American agriculture, particularly in the Great Plains region. As crops failed and farmland became unusable, farmers faced insurmountable financial challenges. Many had taken out loans to purchase land, equipment, and seeds, expecting to repay these debts with the proceeds from their harvests. However, the prolonged drought and dust storms led to widespread crop failures, leaving farmers unable to generate income. This dire situation resulted in a sharp increase in farmer loan defaults, which directly contributed to the financial instability of banks, especially those in rural areas heavily dependent on agricultural loans.

Bank closures became a common occurrence during the Dust Bowl as farmer loan defaults eroded the financial foundations of these institutions. When farmers were unable to repay their loans, banks faced significant losses, depleting their capital reserves. This was exacerbated by the fact that many banks had a high concentration of agricultural loans in their portfolios, making them particularly vulnerable to the economic downturn in the farming sector. As defaults mounted, banks struggled to maintain liquidity, leading to a loss of depositor confidence. Panicked depositors began withdrawing their funds en masse, triggering bank runs that further destabilized these institutions. Without sufficient reserves to meet withdrawal demands, many banks were forced to close their doors permanently.

The closure of banks due to farmer loan defaults had far-reaching consequences for both rural communities and the broader economy. Farmers lost access to credit, making it nearly impossible to invest in their operations or recover from the Dust Bowl’s effects. Local businesses that relied on bank financing also suffered, as the availability of loans dried up. The economic ripple effects extended beyond agriculture, as reduced spending in rural areas impacted industries such as retail, transportation, and manufacturing. Additionally, bank closures contributed to the overall financial crisis of the Great Depression, as the failure of rural banks added to the strain on the national banking system.

Government intervention eventually played a role in addressing the crisis, though it came too late for many banks. The establishment of the Federal Deposit Insurance Corporation (FDIC) in 1933 helped restore depositor confidence by insuring bank deposits, but this measure did little to revive the banks that had already failed. The Reconstruction Finance Corporation (RFC) also provided emergency loans to struggling banks, but the scale of the crisis overwhelmed these efforts. For the banks that had closed due to farmer loan defaults, the damage was irreversible, leaving a lasting scar on the financial landscape of Dust Bowl-affected regions.

In conclusion, bank closures due to farmer loan defaults during the Dust Bowl were a direct consequence of the agricultural collapse caused by severe environmental and economic conditions. The inability of farmers to repay loans led to significant financial losses for banks, triggering a chain reaction of bank runs and closures. These closures not only devastated rural communities by cutting off access to credit but also contributed to the broader economic turmoil of the Great Depression. The Dust Bowl’s impact on banks underscores the interconnectedness of agriculture, finance, and the economy, highlighting the vulnerability of financial institutions to sector-specific shocks.

Exploring Northpointe Bank's Grand Rapids Presence: Size and Impact

You may want to see also

Explore related products

![]()

Dust Bowl's impact on agricultural credit and banking stability

The Dust Bowl, a period of severe dust storms and drought in the 1930s, had profound effects on agricultural communities across the American Great Plains. One of the most significant consequences was its impact on agricultural credit and banking stability. As crops failed and farmland became unusable due to erosion, farmers faced devastating financial losses. Many were unable to repay loans they had taken out to purchase land, equipment, or seeds. This widespread default on agricultural loans placed immense strain on rural banks, which were heavily exposed to the farming sector. The inability of farmers to meet their financial obligations led to a cascade of bank failures, particularly in the hardest-hit regions.

Agricultural credit, which was essential for farmers to operate and invest in their land, virtually dried up during the Dust Bowl. Banks became increasingly reluctant to extend loans to farmers due to the heightened risk of default. This credit crunch further exacerbated the economic plight of farmers, as they lacked the necessary funds to adapt to the changing conditions or even to sustain their operations. The reduction in credit availability also stifled agricultural innovation and productivity, deepening the economic crisis in rural areas. As a result, the Dust Bowl not only destroyed farmland but also undermined the financial infrastructure that supported agricultural communities.

Banking stability was severely compromised as rural banks faced a surge in loan defaults and a decline in deposits. Farmers, who were the primary customers of these banks, withdrew their savings to cover immediate expenses or simply lost their financial resources due to crop failures. With liabilities far exceeding assets, many banks were forced to close their doors, eroding public confidence in the banking system. The failure of these banks had a ripple effect, as it reduced the overall liquidity in the financial system and limited the availability of credit for both agricultural and non-agricultural borrowers. This instability contributed to the broader economic challenges of the Great Depression.

The Dust Bowl also highlighted the interconnectedness of agricultural credit and regional economic health. As banks failed, local economies suffered, leading to reduced spending and further economic decline. The federal government eventually intervened through programs like the Agricultural Adjustment Act (AAA) and the establishment of the Farm Credit Administration (FCA) to provide financial assistance and stabilize the agricultural credit system. These measures aimed to restore confidence in rural banking and ensure that farmers had access to the credit needed to recover from the devastation of the Dust Bowl.

In conclusion, the Dust Bowl's impact on agricultural credit and banking stability was profound and far-reaching. It exposed the vulnerabilities of a financial system heavily reliant on agriculture and led to significant reforms in how agricultural credit was managed. The crisis underscored the need for a more resilient banking system and highlighted the critical role of government intervention in stabilizing rural economies during times of extreme distress. The lessons learned from this period continue to influence agricultural finance and banking policies to this day.

Banking Benefits: Why You Need a Bank Account

You may want to see also

Explore related products

![]()

Rural bank failures linked to crop losses and debt

The Dust Bowl, a period of severe dust storms and drought in the 1930s, had a devastating impact on agriculture in the American Great Plains, which in turn led to significant financial strain on rural communities and their banking systems. As crops failed due to the harsh environmental conditions, farmers faced drastic reductions in income, leaving them unable to repay loans they had taken out to purchase land, equipment, and seeds. This widespread crop loss created a ripple effect throughout the rural economy, as farmers defaulted on their debts en masse. Rural banks, heavily dependent on agricultural loans for their revenue, found themselves with a growing portfolio of non-performing loans, which severely undermined their financial stability.

The inability of farmers to meet their financial obligations directly contributed to the wave of rural bank failures during this period. Banks that had extended credit to farmers were now left with insufficient collateral, as the value of farmland plummeted alongside crop yields. With limited cash reserves and a lack of incoming loan repayments, many rural banks were forced to close their doors. Between 1929 and 1933, over 9,000 banks failed nationwide, with a disproportionate number located in agricultural regions hardest hit by the Dust Bowl. These bank failures further eroded trust in the financial system, exacerbating the economic crisis in rural areas.

The interconnectedness of rural banks and local agriculture meant that the collapse of one often precipitated the decline of the other. As banks failed, farmers lost access to credit, making it impossible to finance future planting seasons or sustain their operations. This vicious cycle deepened the economic depression in rural communities, as both farmers and banks struggled to recover. The loss of banking services also hindered economic activity in these areas, as businesses and individuals relied on local banks for everyday transactions and loans. Without a functioning banking system, rural economies became increasingly stagnant, prolonging the recovery process.

Government intervention eventually played a role in stabilizing the banking sector, but the damage to rural banks had already been done. The Emergency Banking Act of 1933 and the establishment of the Federal Deposit Insurance Corporation (FDIC) helped restore confidence in the banking system, but many rural banks never reopened. The Dust Bowl exposed the vulnerabilities of rural banking systems heavily reliant on a single industry, leading to long-term changes in agricultural lending practices and risk management. The lessons from this period underscored the need for diversification in rural economies and greater financial safeguards to prevent similar crises in the future.

In summary, the Dust Bowl's catastrophic impact on agriculture triggered a chain reaction of crop losses, farmer debt defaults, and rural bank failures. The collapse of these banks not only deepened the economic hardship of farmers but also destabilized entire rural communities. This era highlighted the precarious relationship between agricultural productivity and financial stability, prompting reforms to strengthen the resilience of both the farming and banking sectors. The legacy of the Dust Bowl serves as a reminder of the importance of sustainable economic practices and robust financial systems in safeguarding rural livelihoods.

Which Banks Are at Risk of Collapse?

You may want to see also

Explore related products

![]()

Economic ripple effects on urban and regional banks

The Dust Bowl, a severe drought and dust storm event that ravaged the American Great Plains during the 1930s, had profound economic ripple effects on urban and regional banks. As agricultural productivity plummeted, farmers faced widespread crop failures and livestock losses, leading to a sharp decline in their income. This reduction in farm revenue directly impacted local economies, as farmers had less money to spend on goods and services. Regional banks, heavily reliant on agricultural loans, saw a surge in loan defaults as farmers were unable to repay their debts. The resulting financial strain on these banks triggered a chain reaction, limiting their ability to lend to other sectors and stifling economic growth in rural communities.

Urban banks, though less directly exposed to agricultural risks, were not immune to the Dust Bowl's economic fallout. As rural economies collapsed, migration to cities surged, with millions of displaced farmers and rural workers seeking employment in urban areas. This influx strained urban resources and increased demand for housing, food, and social services. While some urban banks initially benefited from the increased economic activity, the overall financial instability and widespread unemployment eroded consumer confidence. Reduced consumer spending and business investments led to lower deposit levels and decreased loan demand, weakening the financial health of urban banks.

The interconnectedness of the banking system further amplified the Dust Bowl's impact. Regional bank failures reduced the overall liquidity in the financial system, making it harder for urban banks to access funds for lending and operations. This liquidity crunch forced many banks to adopt more conservative lending practices, tightening credit availability for businesses and individuals. The reduced flow of credit stifled economic activity across both rural and urban areas, exacerbating the economic downturn. Additionally, the loss of confidence in the banking system led to bank runs, further destabilizing financial institutions and deepening the economic crisis.

Another significant ripple effect was the increased regulatory scrutiny and policy changes that emerged in response to the banking sector's vulnerabilities. The Dust Bowl highlighted the risks of over-reliance on a single economic sector, such as agriculture, and the need for greater financial stability. This led to the implementation of new banking regulations and the establishment of federal programs aimed at stabilizing the agricultural sector and preventing future bank failures. While these measures helped mitigate some risks, they also imposed additional compliance costs on banks, further straining their resources during an already challenging period.

In summary, the Dust Bowl's economic ripple effects on urban and regional banks were far-reaching and multifaceted. Regional banks faced direct financial losses due to agricultural loan defaults, while urban banks grappled with the indirect consequences of rural migration and reduced economic activity. The interconnected nature of the banking system amplified these effects, leading to widespread liquidity issues and tightened credit markets. The crisis also spurred regulatory reforms that, while necessary, added operational burdens to banks. Ultimately, the Dust Bowl underscored the fragility of the financial system and its vulnerability to environmental and economic shocks, leaving a lasting impact on banking practices and policies.

Barclays Bank: Italian Branches and Services

You may want to see also

Explore related products

![]()

Government interventions to rescue banks during the Dust Bowl crisis

The Dust Bowl, a period of severe dust storms and economic hardship in the 1930s, had a profound impact on the banking sector in the United States. As agricultural productivity plummeted and farmers defaulted on loans, banks, particularly in the Great Plains region, faced a wave of loan defaults and financial instability. Recognizing the systemic risks posed by widespread bank failures, the federal government implemented several interventions to stabilize the banking system and restore public confidence. One of the earliest and most significant measures was the establishment of the Reconstruction Finance Corporation (RFC) in 1932. The RFC provided emergency loans to banks, railroads, and other financial institutions to prevent insolvency. By injecting capital into struggling banks, the RFC aimed to maintain liquidity and prevent a cascade of bank failures that could further destabilize the economy.

Another critical intervention was the Emergency Banking Act of 1933, enacted during the first 100 days of President Franklin D. Roosevelt's administration. This legislation granted the federal government the authority to inspect banks and reopen those deemed solvent, while also providing federal guarantees for bank deposits. The act was followed by the creation of the Federal Deposit Insurance Corporation (FDIC), which insured individual bank deposits up to $5,000 (later increased). This measure was designed to restore public trust in the banking system by assuring depositors that their savings were safe, thereby reducing the likelihood of bank runs. These actions were instrumental in stabilizing banks during the Dust Bowl crisis, as they provided a safety net for both financial institutions and their customers.

The government also addressed the root causes of bank distress by implementing agricultural relief programs. The Agricultural Adjustment Act (AAA) of 1933 sought to reduce crop surplus and raise prices by paying farmers to limit production. While the AAA primarily targeted farmers, it indirectly benefited banks by improving the financial condition of their agricultural borrowers. Additionally, the Farm Credit Administration (FCA) was established to provide low-interest loans to farmers, helping them avoid defaulting on existing bank loans. By alleviating the financial strain on farmers, these programs reduced the burden on rural banks and contributed to their recovery.

To further support banks, the government introduced regulatory reforms aimed at preventing future crises. The Glass-Steagall Act of 1933 separated commercial and investment banking activities, reducing speculative risks that had contributed to bank failures. This act also established the Federal Deposit Insurance Corporation (FDIC) as a permanent institution, ensuring long-term stability in the banking sector. These regulatory measures, combined with direct financial assistance, created a framework that helped banks weather the Dust Bowl crisis and laid the groundwork for future economic resilience.

In summary, government interventions during the Dust Bowl crisis were multifaceted and targeted at both immediate stabilization and long-term reform. Through agencies like the RFC and FDIC, the government provided critical financial support and deposit insurance, while agricultural programs like the AAA and FCA addressed the underlying economic challenges. Regulatory reforms, such as the Glass-Steagall Act, further strengthened the banking system. These measures collectively played a pivotal role in rescuing banks from the brink of collapse and restoring stability to the financial sector during one of the most challenging periods in American history.

Bancorp Bank and Venmo: What's the Connection?

You may want to see also

Frequently asked questions

The Dust Bowl caused widespread crop failures and economic hardship, leading farmers to default on loans. This resulted in significant financial losses for banks, many of which were forced to close due to insufficient assets.

Yes, the Dust Bowl exacerbated bank failures during the Great Depression. The agricultural collapse reduced farmers' incomes, making it impossible for them to repay loans, which further destabilized already struggling banks.

Banks tightened lending practices, reduced loan availability, and increased interest rates to mitigate risks. Some sought government assistance or merged with larger institutions to survive.

The Dust Bowl accelerated the decline of rural banks by decimating their primary customer base—farmers. As agricultural incomes plummeted, rural banks lost their main source of revenue and deposits, leading to widespread closures.

Government programs like the Agricultural Adjustment Act (AAA) and the establishment of the Farm Credit Administration provided some relief by restructuring farm debts and offering financial assistance, but many banks still struggled to recover fully.