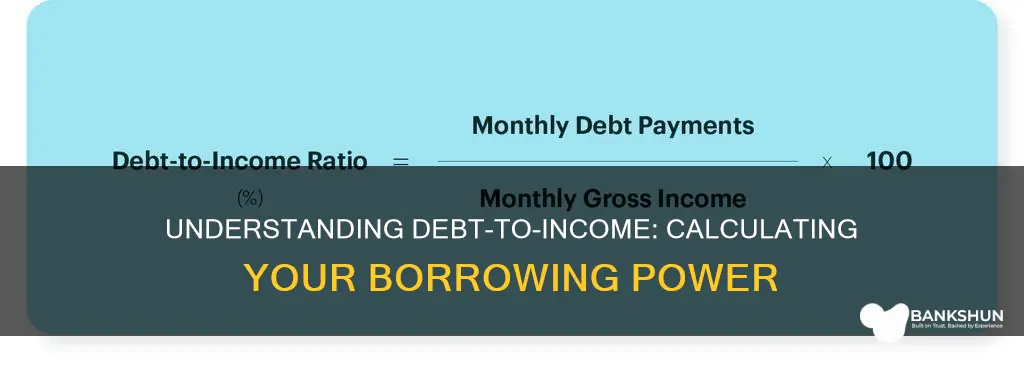

When applying for a loan, mortgage, or credit card, lenders will evaluate your creditworthiness by calculating your debt-to-income (DTI) ratio. This simple formula compares your monthly debt payments to your gross monthly income. It is a critical indicator of your financial health and can help you make informed decisions about your finances and debt management goals. A high DTI ratio may suggest that you are stretched too thin financially, while a lower ratio indicates that you can likely take on more debt.

| Characteristics | Values |

|---|---|

| Purpose | To determine an individual's financial health and ability to make payments |

| Calculation | Total monthly debt obligations / Gross monthly income |

| Gross income | Income before taxes or deductions |

| Monthly debt obligations | Credit cards, mortgages, student loans, car loans, rent, etc. |

| Lenders' preference | Below 36% |

| Borrowing options | Limited if DTI is above 43% |

Explore related products

What You'll Learn

![]()

Calculating the debt-to-income ratio

Calculating your debt-to-income ratio is a simple process. Firstly, you must identify your monthly debt payments. These include credit cards, mortgages, student loans, car loans, and rent, among others. Next, you must calculate your gross monthly income. This is your income before any taxes or deductions are taken out. It can include wages, salaries, tips, bonuses, pensions, and social security payments.

Once you have these two figures, you divide your monthly debt payments by your gross monthly income. This will give you a decimal number, which can be converted into a percentage by multiplying it by 100. For example, if your monthly debt payments are $2,000 and your monthly income is $6,000, your debt-to-income ratio is 33%.

This ratio is an important indicator of your financial health and can help you make informed decisions about your finances. It is also used by lenders to evaluate your creditworthiness and determine whether to lend you money. A lower ratio indicates that you have room in your budget for additional obligations, while a higher ratio may suggest that you are stretched too thin financially.

It is important to note that your debt-to-income ratio does not account for non-debt expenses, such as groceries, utilities, and insurance. It also does not include discretionary expenses like utilities, groceries, or subscriptions.

Mobile Banking: Weekend Refunds?

You may want to see also

Explore related products

![]()

How lenders use the ratio

Lenders use the debt-to-income (DTI) ratio to assess a borrower's ability to manage monthly payments and repay the money. The DTI ratio is a significant factor in determining a borrower's creditworthiness. It is a key factor in mortgage approval, with most lenders seeing DTI ratios of 36% or below as ideal. Lenders commonly use DTI ratios to review applications for mortgages, car loans, personal loans, and credit cards.

DTI ratios are also used by lenders to evaluate the risk of extending credit to a borrower. A low DTI ratio reflects a good balance between income and debt, making a borrower a more attractive candidate for loans. Lenders consider a borrower's DTI ratio alongside their overall income, debt, and credit rating. While standards vary, most lenders prefer a DTI ratio below 35-36%.

The DTI ratio is calculated by dividing the borrower's total recurring monthly debt payments by their gross monthly income (income before taxes or other deductions). This percentage represents the proportion of income left after making monthly debt payments. Lenders typically focus on two types of DTI ratios: the front-end ratio and the back-end ratio. The front-end ratio, or housing ratio, shows what percentage of the borrower's income would go towards housing expenses if the mortgage were approved. The back-end ratio includes all types of debt and shows how much of the borrower's income is required to pay all monthly debt obligations.

If a borrower's DTI ratio is too high to qualify for a loan, they can take steps to lower it. This can include increasing their income, reducing their total debt, or both. Checking credit reports is essential, as errors can make a DTI ratio seem higher than it is. Additionally, borrowers can lower their spending to avoid increasing their overall debt and free up more income for debt repayment.

BSA in Banking: What Does It Mean?

You may want to see also

Explore related products

![]()

What counts as debt

When calculating your debt-to-income (DTI) ratio, it is important to understand what counts as debt. Your monthly debt includes secured and unsecured debt payments. Secured debts are collateralised, meaning the borrower has pledged property that can be seized if payments are defaulted. Unsecured debts, such as credit card debt and student loans, are not collateralised.

Mortgages are a type of secured debt used to purchase real estate, such as a house or condo. They are usually paid back over long periods, such as 15 or 30 years, and often constitute the largest debt consumers will ever take on. Auto loans are another example of secured debt, where the car acts as collateral. If the borrower defaults on their payments, the lender can repossess the car and sell it to recoup their losses.

Credit cards fall under the category of revolving and unsecured debt. Borrowers can repeatedly borrow money as long as they pay the minimum amount and do not exceed their credit limit. Credit card companies charge interest, or a fee for using their services, which is represented as an annual percentage rate (APR). As of winter 2021, the average APR on credit cards was 17.13%.

Student loans can be private or federal and are also considered unsecured, non-revolving debt. While there are penalties for defaulting on student loans, no one will come to repossess your degree. Federal student loans have a current interest rate of 6.53%, and the standard repayment plan requires fixed monthly payments for 10 years until the debt is completely paid off.

Personal loans are another form of debt, often used to cover specific expenses or consolidate other debts. They are lump-sum borrowings from a bank, credit union, or online lender.

When calculating your DTI ratio, lenders will also consider any rent or mortgage payments, alimony or child support payments, and other recurring loan payments as part of your monthly debt.

Calculating Yield Percentages: A Banking Guide

You may want to see also

Explore related products

![]()

What counts as income

When calculating your debt-to-income ratio, it is important to understand what counts as income. This is typically your gross monthly income, or the amount you earn each month before taxes and any other deductions. Sources of income include:

- Wages

- Salaries

- Tips and bonuses

- Pensions

- Social security payments

- Rental income

- Child support (if you're receiving these payments)

- Alimony (if you're receiving these payments)

Money earned from a side hustle that isn’t documented on a tax return may not be eligible for consideration as part of your debt-to-income calculation. However, some lenders may accept bank statements that show regular deposits.

Commercial Banks: Profiting Through Lending and Fees

You may want to see also

Explore related products

![]()

Improving your debt-to-income ratio

DTI is calculated by dividing your total monthly debt payments by your gross monthly income (before tax). To improve your DTI, you can either reduce your debt or increase your income. Here are some ways to do this:

Reduce Your Debt

- Focus on paying off existing debt, especially credit cards.

- Avoid applying for new credit or loans, as this can negatively impact your DTI.

- Pay more than the minimum monthly payment to reduce overall debt faster.

- Avoid making large purchases that will use up your available credit.

- Consider a debt consolidation loan to lower your monthly debt payments.

- Create a personal monthly budget and stick to it to reduce spending and increase debt payments.

- Revisit your budget to understand where your money is going each month and cut back on non-essential spending.

Increase Your Income

- Take on a side hustle or ask for a pay increase to boost your income.

- Include any income from bonuses or overtime pay when reporting your income to lenders.

- If you have rental properties, include this income in your DTI calculation.

It is important to note that improving your DTI takes time and consistent effort. By regularly paying off debt and increasing your income, you can achieve a healthier financial situation and improve your chances of loan approval.

Fanduel Withdrawals: How Long Until They Reach Your Bank?

You may want to see also

Frequently asked questions

The debt-to-income ratio (DTI) is a number that measures how much of your income goes towards debt payments each month. It compares your monthly debts to your monthly earnings.

Your debt-to-income ratio is an important indicator of your financial health. It helps lenders determine whether to lend you money and how much. It can also help you make informed decisions about your finances and debt management goals.

To calculate your debt-to-income ratio, add up all your monthly payments that are related to debt (such as credit cards, mortgages, student loans, etc.) and divide them by your gross monthly income (i.e. your income before taxes and other deductions). Multiply the result by 100 to get your DTI percentage.

A lower debt-to-income ratio is generally better as it suggests you have room in your budget for additional obligations. Most lenders consider DTIs below 36% to be ideal, while a DTI above 43% may be considered high.