Unauthorized transactions are a major concern for both banks and customers, and fraudsters have a variety of tools at their disposal to exploit vulnerabilities. ACH fraud is a type of unauthorized transaction that involves the use of the Automated Clearing House (ACH) network to facilitate illegitimate transactions. When investigating ACH fraud, banks follow a systematic process that begins with detection and evidence gathering. This includes collecting transaction records, account statements, digital logs, and communication records. Forensic techniques are then employed to analyze the evidence, and specialized digital tools may be used to locate additional information. Understanding how banks investigate unauthorized ACH transactions is crucial for individuals and businesses to protect their finances and prevent fraud.

| Characteristics | Values |

|---|---|

| How it starts | The investigation process begins when a bank is alerted to potential fraud, either by a customer’s report of an unauthorized transaction or through automated systems that flag unusual activity. |

| Information gathering | The bank collects all available information, including transaction records, account statements, digital logs, and communication records. |

| Customer action | If a customer suspects fraud, they should report it immediately, providing transaction details to assist in the investigation. |

| Forensic analysis | Investigators employ forensic techniques to analyze the collected evidence, identifying patterns, anomalies, or inconsistencies. |

| Advanced tools | Banks use advanced tools and strict procedures to detect fraud, determine liability, and implement preventive measures. |

| Fraud types | ACH fraud includes insider threats, ACH kiting, ACH lapping, payroll fraud, check kiting, and phishing. |

| Fraud prevention | Banks hold fraud education sessions, send educational warnings during transactions, and implement security measures like two-factor authentication. |

| Liability | Liability for ACH fraud often falls on merchants and financial institutions processing the transactions. |

| Dispute window | Personal account holders have up to 60 days to dispute an unauthorized ACH transaction, while businesses have 24 hours. |

Explore related products

What You'll Learn

![]()

Detection and prevention tools

ACH fraud is any unauthorized transfer from a bank account using the Automated Clearing House network. Banks play a pivotal role in safeguarding financial assets and maintaining the trust of their customers. Unauthorized transactions, ranging from minor discrepancies to substantial fraudulent activities, pose a significant threat to the financial stability of individuals and institutions.

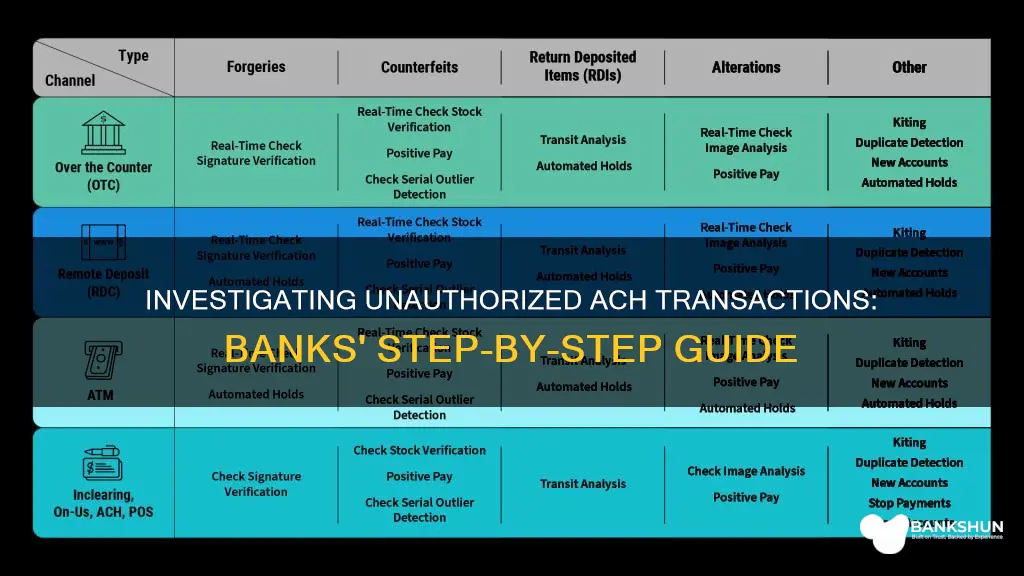

To combat fraud, banks employ comprehensive investigation procedures and advanced detection systems to monitor transactions and flag anomalies based on frequency, amount, and location. They also rely heavily on automated systems to detect fraudulent activities early. These systems use algorithms to monitor transactions for red flags, such as irregular spending patterns, unexpected changes in transaction locations, mismatched IP addresses, or sudden large withdrawals.

Some specific detection tools and techniques used by banks include:

- Transaction monitoring tools: These tools can be fine-tuned to detect specific ACH red flags, such as transactions taking place across different geographic areas or customers using a different device or account than usual.

- Secure API: Application Programming Interfaces (APIs) enable faster and more efficient fraud detection by facilitating communication and integration between different systems.

- Biometrics: Biometric modalities help identify the actual human interacting with a device or service, aiding in fraud detection.

- Enhanced behavioural analytics: Machine learning capabilities help build an accurate picture of "expected" versus "unexpected" account behaviour, enabling near real-time risk mitigation.

- Forensic techniques: Investigators employ specialized digital tools to locate hard-to-find information, identify patterns and hidden connections, and analyse evidence.

In addition to detection, banks also focus on prevention by educating customers about fraud prevention. They hold fraud education sessions, provide warnings during transactions, and encourage the use of security measures such as strong passwords, multi-factor authentication, and transaction alerts.

Customers can also take proactive measures, such as regularly monitoring their accounts for any unusual or unauthorized transactions, updating passwords, and enabling two-factor authentication. Additionally, tools like ACH filters and blocks allow customers to specify authorized individuals and entities for debits, helping prevent unauthorized transactions.

Bank Reconciliation: A Daily, Weekly, or Monthly Task?

You may want to see also

Explore related products

![]()

Customer liability

Unauthorized transactions are a significant concern for both banks and customers, threatening the financial stability of both parties. In the case of ACH fraud, consumers are generally not liable for unauthorized transactions, as long as they report them within 60 days of the bank providing a statement showing the transaction. This is because consumer electronic transactions are governed by the Federal Reserve Regulation E and the National ACH Association (NACHA).

However, if a consumer fails to notify the bank within 60 days, they may be liable for any transfers that occur after this period. The amount of liability is determined by the first two tiers of liability: up to $50 if the consumer notifies the financial institution within two business days of learning of the loss or theft, and up to $500 if they notify the institution after two business days. For example, if $600 was taken on Tuesday and $100 on Thursday, the consumer's maximum liability would be $150 ($50 of the $600, plus $100).

If a customer was grossly negligent, such as by sharing their PIN or password, they may bear some or all of the loss. The organization where the insider operates typically bears the liability for these losses, especially if inadequate controls or oversight facilitated the fraud. In some cases, banks might pursue legal action against the individual perpetrator.

To prevent unauthorized transactions, customers should regularly monitor their accounts and update passwords and enable two-factor authentication. Tools such as ACH filters and blocks allow account holders to specify which individuals and entities are authorized to make transactions.

DCI Banks Filming Locations: Where is it Shot?

You may want to see also

Explore related products

![]()

Fraud types

ACH fraud is any unauthorized transfer from a bank account using the Automated Clearing House network. The ACH network is a financial transaction network and central clearing facility for all electronic fund transfers (EFTs) in the US. Fraudsters only need two pieces of stolen information to commit ACH fraud: a checking account and a bank routing number.

There are several types of ACH fraud:

- ACH kiting: Moving funds back and forth between accounts and financial institutions. This usually happens within a company, often at the end of the year.

- ACH lapping: A payment from a bank account is diverted or marked as received. Subsequent payments from other accounts are made to cover up the fraud.

- Insider threats: Someone within a company uses legitimate credentials to steal money via ACH or pass it to another fraudster.

- Phishing: An employee or authorized individual is tricked into providing their credentials, and a fraudster uses them to impersonate the individual and withdraw funds.

- Check kiting: Moving money back and forth between accounts at different banks. When the transfer is approved by the clearing house, it looks like the money is in the account, but it has already been moved.

- Loss or theft of a debit card: Criminals can use this window of time to carry out an unauthorized ACH withdrawal.

- Account takeover: Fraudsters gain unauthorized access to a bank account's digital platforms.

To prevent ACH fraud, banks offer "positive pay" ACH fraud protection, which allows them to compare electronic account transactions against previously authorized payments and suspend unmatched items. Account holders can also use tools such as ACH filters and blocks that allow them to specify which individuals and entities are authorized to make debits.

OnlyFans Payouts: Which Banks Are Compatible?

You may want to see also

Explore related products

![]()

Bank investigation process

Banks employ comprehensive investigation procedures to combat fraud, protect their customers, and preserve their credibility. The investigation process can vary in length and complexity, but there are several common steps.

Firstly, the bank must be alerted to potential fraud, either by a customer reporting an unauthorized transaction or through automated systems that flag unusual activity. Automated systems use algorithms to monitor transactions for red flags, such as irregular spending patterns, mismatched IP addresses, or sudden large withdrawals.

Once the bank is alerted, they will begin to gather information and evidence. This includes transaction records, account statements, digital logs, and communication records. Customers may be asked to provide additional documentation to support their claim, such as proving that the transaction was unauthorized. Forensic techniques are then employed to analyze the evidence, identifying patterns, anomalies, or inconsistencies.

Specialized digital tools can be used to add rigor to the investigation, helping to identify hidden connections and patterns that could indicate fraudulent activity. In severe cases of fraud or identity theft, law enforcement agencies may be involved, especially if the investigation has broader implications beyond the bank's jurisdiction.

Understanding liability is also crucial. In the case of ACH fraud, liability often falls on merchants and financial institutions processing transactions. Consumers must report ACH fraud within 60 days of receiving a statement or the settlement date to be reimbursed by the bank. After this time, the bank is no longer liable.

To prevent ACH fraud, customers can use tools such as ACH filters and blocks, which allow them to specify which entities are authorized to make debits. Regularly updating passwords, enabling two-factor authentication, and monitoring accounts can also help prevent unauthorized access and aid investigators.

Expired Food: Can Food Banks Accept It?

You may want to see also

Explore related products

![]()

Fraud prevention

Bank Collaboration and Education:

- Banks should maintain open communication with their fraud prevention departments, staying alert to emerging fraud patterns and collaborating on investigations.

- Banks often hold fraud education sessions for small business owners and customers, highlighting physical security measures and educating them on protecting themselves online.

- Banks embed educational warnings into transactions, alerting customers to be cautious of strangers or companies demanding immediate payments.

Customer Verification and Monitoring:

- Before initiating recurring payments or adding beneficiaries, banks should conduct due diligence by verifying addresses, business legitimacy, and checking against sanctions lists and fraud databases.

- Regularly monitor for changes in recipient behavior, communication style, or updated bank account information that could indicate a compromised account.

- Customers should regularly monitor their accounts for any unauthorized transactions.

Advanced Technology and Automated Systems:

- Banks rely on advanced technology and automated systems to detect fraudulent activities early. These systems use algorithms to monitor transactions for red flags, including irregular spending patterns, unexpected location changes, mismatched IP addresses, or large withdrawals.

- Advanced technologies like unsupervised machine learning, transaction monitoring, and device fingerprinting can also be used to detect ACH scams.

Security Measures:

- Customers should update passwords, enable two-factor authentication, and monitor accounts to prevent unauthorized access and aid investigators in mitigating risks.

- Regular audits, segregation of duties, and monitoring unusual activity can help mitigate insider fraud risks.

- Establishing a culture of security and ethical behavior within the bank is essential.

Tracing ACH Payments:

- Tracing ACH payments can help resolve issues such as non-receipt of funds, errors, or suspected fraud. Collecting relevant information, such as transaction amounts, dates, reference numbers, and account details, is crucial for accurate tracing.

- ACH filters and blocks allow account holders to specify authorized entities for debits, helping prevent unauthorized transactions.

FIA Question Bank: How Extensive?

You may want to see also

Frequently asked questions

ACH fraud is any unauthorized transfer from a bank account using the Automated Clearing House (ACH) network. Fraudsters only need two pieces of information: a checking account and a bank routing number.

Banks use advanced detection systems and automated systems to monitor transactions and flag anomalies based on frequency, amount, and location. They also use algorithms to monitor transactions for red flags, such as irregular spending patterns, unexpected changes in transaction locations, mismatched IP addresses, or sudden large withdrawals.

If a customer suspects fraud, they should report it immediately, providing transaction details to assist in the investigation. Updating passwords, enabling two-factor authentication, and monitoring accounts can help prevent further unauthorized access while aiding investigators in mitigating risks.

The investigation process begins when a bank is alerted to potential fraud, either by a customer report or through automated systems. The bank then gathers information, including transaction records, account statements, communication logs, and digital logs. Investigators analyze the evidence to identify patterns, anomalies, or inconsistencies, employing specialized digital tools to locate hard-to-find information.

Liability for ACH fraud often falls on merchants and financial institutions processing the transactions. Financial institutions are liable for ACH fraud and must compensate consumers for fraudulent ACH transactions. However, consumers must report the fraud within 60 days of receiving a statement listing the transaction to be reimbursed.