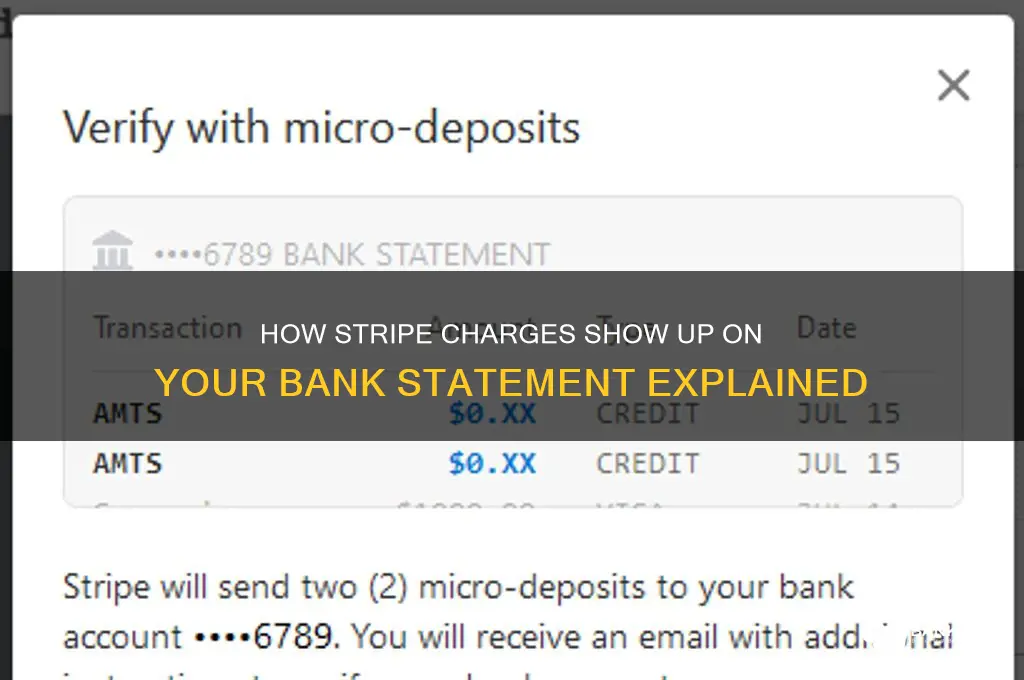

When making a purchase through a merchant that uses Stripe as their payment processor, the transaction will typically appear on your bank statement with a description that includes the merchant's name or business identifier, followed by via Stripe or a similar notation. This is because Stripe acts as the intermediary between the merchant and your bank, processing the payment securely. The charge amount will reflect the total cost of your purchase, including any taxes or fees, and may take a few days to post to your account, depending on your bank's processing times. Understanding how these charges appear can help you recognize and reconcile transactions more easily.

Explore related products

![Battery Case for iPhone 13/13 Pro/14, [2025 Upgraded] 7500mAh Slim Portable Smart Charging Case Rechargeable Protective Extended Charging Cover for iPhone 13/13 Pro/14 Battery Pack (6.1 Inch), Black](https://m.media-amazon.com/images/I/61nsU7nuevL._AC_UY218_.jpg)

What You'll Learn

- Charge Descriptor Format: How Stripe displays merchant names and transaction details on bank statements

- Timing of Charges: When Stripe transactions appear on bank statements after processing

- Currency Conversion: How foreign currency charges are displayed and converted on bank statements

- Disputes & Refunds: How disputed or refunded Stripe charges are reflected on bank statements

- Recurring Payments: How subscription or recurring Stripe charges appear on bank statements over time

![]()

Charge Descriptor Format: How Stripe displays merchant names and transaction details on bank statements

When a transaction processed by Stripe appears on a customer's bank statement, it follows a specific Charge Descriptor Format designed to clearly identify the merchant and provide essential transaction details. This format is crucial for both merchants and customers to recognize and reconcile payments. Typically, the charge descriptor includes the merchant’s business name, which is truncated or abbreviated if it exceeds the character limit imposed by banks (usually 22–25 characters). For example, if a merchant’s name is "EcoFriendly Products LLC," it might appear as "ECOFRIENDLY PROD" or "ECOFRIENDLY*LLC" on the statement. Merchants can customize this descriptor within their Stripe dashboard, but it must adhere to bank regulations and character limits.

In addition to the merchant name, the charge descriptor often includes a dynamic component that reflects the transaction details. This could be a location identifier, a service type, or a reference number. For instance, if a customer makes a purchase at a specific store location, the descriptor might include "NYC STORE" or "ONLINE SHOP." For subscriptions or recurring payments, terms like "SUBSCRIPTION" or "RECURRING" may be appended. Stripe also allows merchants to add a static suffix, such as "*STRIPE" or "*PAYMENT," to indicate the payment processor, though this is optional and depends on the merchant’s settings.

The format of the charge descriptor is influenced by the payment method and the customer’s bank. For credit card transactions, the descriptor typically appears as a single line item, while for bank transfers or ACH payments, it may include additional details like the account type or transaction type. Stripe ensures that the descriptor is consistent across transactions for the same merchant, but variations can occur due to differences in how banks interpret and display the data. For international transactions, currency codes or country abbreviations may also be included.

Merchants should be aware that the charge descriptor directly impacts customer recognition and trust. A clear and recognizable descriptor reduces confusion and chargebacks, as customers are more likely to identify the transaction. Stripe provides tools for merchants to preview how their descriptor will appear on statements, allowing them to make adjustments before processing payments. It’s also important to note that changes to the descriptor may take time to reflect on statements due to banking system delays.

Finally, customers encountering unfamiliar descriptors on their bank statements can often resolve confusion by checking their email receipts or logging into their Stripe-connected accounts. Stripe’s transparency in transaction details ensures that even abbreviated descriptors can be traced back to the original purchase. Understanding the Charge Descriptor Format helps both merchants and customers navigate Stripe transactions with confidence, ensuring a seamless payment experience.

Nurses' Role in Sperm Banks: Essential Support or Unnecessary Assistance?

You may want to see also

Explore related products

![]()

Timing of Charges: When Stripe transactions appear on bank statements after processing

When it comes to understanding how Stripe charges appear on bank statements, the timing of these transactions is a crucial aspect for both businesses and customers. After a payment is processed through Stripe, the time it takes for the charge to appear on a bank statement can vary depending on several factors, including the type of payment method used, the bank's processing times, and the specific settings of the Stripe account. Generally, the process begins immediately after a transaction is authorized, but the actual posting to the bank statement may take a bit longer.

For credit and debit card transactions, the initial authorization typically occurs within seconds of the payment being made. However, the settlement process, where funds are transferred from the customer's bank to the merchant's account, usually takes 2 to 7 business days. During this period, the charge may appear as a pending transaction on the customer's bank statement. The exact timing can also depend on the bank's policies and the time of day the transaction was processed. For instance, transactions made after business hours or on weekends might not start the settlement process until the next business day.

Bank transfers and ACH payments processed through Stripe follow a slightly different timeline. These transactions often take longer to clear, typically ranging from 3 to 5 business days, but can sometimes extend up to 7 business days. The delay is due to the nature of the ACH network, which processes transactions in batches rather than in real-time. During this period, the charge may not appear on the bank statement until the funds have been fully debited from the customer's account. It’s important for customers to be aware of this delay to avoid confusion or overdraft fees.

For international transactions, the timing can be even more variable. Currency conversions, additional bank processing steps, and differences in banking systems across countries can extend the time it takes for a charge to appear on a bank statement. In some cases, international transactions may take up to 10 business days to fully process and appear on the statement. Merchants using Stripe for international payments should communicate these potential delays to their customers to manage expectations effectively.

Finally, it’s worth noting that Stripe’s dashboard provides real-time updates on transaction statuses, which can help merchants and customers track payments. However, the actual appearance on the bank statement is ultimately controlled by the banks involved. Customers who notice discrepancies or delays should first check the Stripe transaction details and then contact their bank if necessary. Understanding these timelines ensures smoother financial management and reduces the likelihood of disputes or misunderstandings related to payment processing.

Does China Have a Federal Reserve Bank? Exploring Its Monetary System

You may want to see also

Explore related products

![]()

Currency Conversion: How foreign currency charges are displayed and converted on bank statements

When dealing with international transactions processed through Stripe, understanding how foreign currency charges appear on your bank statement is crucial. Typically, if a transaction involves a currency different from your bank account’s default currency, the charge will be displayed in both the original currency and your local currency. For example, if you’re based in the U.S. and make a purchase in Euros, your bank statement will show the amount in Euros followed by the equivalent amount in USD. This dual display ensures transparency and helps you verify the transaction details.

The conversion rate used for these transactions is determined by the card network (such as Visa, Mastercard, or American Express) at the time of the transaction. Stripe itself does not set the exchange rate; it relies on the rates provided by the card networks. On your bank statement, the converted amount in your local currency will reflect this rate, which may include a small markup by the card issuer or bank. It’s important to note that the rate applied may differ slightly from real-time market rates due to these markups or processing delays.

Foreign currency charges on your bank statement may also include additional fees related to currency conversion. These fees, often referred to as foreign transaction fees, are typically a percentage of the transaction amount and are charged by your bank or card issuer. For instance, if your bank charges a 3% foreign transaction fee, this will be added to the converted amount on your statement. Always review your bank’s fee schedule to understand these additional costs.

To reconcile Stripe charges involving currency conversion, look for descriptors on your statement that include "Stripe" or the merchant’s name, followed by the original and converted amounts. Some banks may also include a reference number or transaction ID that can be cross-referenced with your Stripe dashboard for further details. If you notice discrepancies between the expected and displayed amounts, consider the exchange rate fluctuations and any applicable fees.

Finally, if you frequently deal with foreign currency transactions, consider using a bank account or credit card that offers favorable exchange rates or waives foreign transaction fees. Additionally, Stripe provides tools for businesses to manage currency conversions efficiently, such as allowing customers to pay in their local currency. By understanding how these charges are displayed and converted, you can better manage your finances and avoid unexpected costs.

Does Simple Bank Charge ATM Fees? A Comprehensive Guide

You may want to see also

Explore related products

![]()

Disputes & Refunds: How disputed or refunded Stripe charges are reflected on bank statements

When a Stripe charge is disputed or refunded, the transaction will appear differently on your bank statement compared to a standard charge. Disputes, also known as chargebacks, occur when a customer questions a transaction with their bank, often resulting in the funds being temporarily reversed. On your bank statement, a disputed charge may appear as a debit (negative amount) with a description that includes terms like "chargeback," "dispute," or "reversal." This indicates that the funds have been removed from your account pending resolution. The description may also include the original transaction date and a reference to Stripe or the customer’s bank.

Refunds, on the other hand, are initiated by the merchant or through Stripe’s dashboard when a customer requests their money back. A refunded Stripe charge will typically appear as a credit (positive amount) on your bank statement, often with a description that includes "refund," "Stripe refund," or the original transaction details. The refund may be listed as a separate line item or paired with the original charge, depending on your bank’s formatting. It’s important to note that refunds can take several business days to process and appear on your statement, depending on your bank and the payment method used.

In the case of a dispute, the bank statement may show additional entries if the dispute is resolved in your favor or against you. If the dispute is resolved in your favor, the funds may be returned to your account, and the statement will reflect a credit with a description like "chargeback reversal" or "dispute resolved." If the dispute is lost, the initial debit for the chargeback remains, and no further entries are added. These descriptions help you track the status of disputed transactions and understand the flow of funds.

For businesses, it’s crucial to monitor bank statements closely during disputes and refunds to ensure accuracy and manage cash flow effectively. Stripe provides detailed reporting within its dashboard, which can be cross-referenced with bank statements to reconcile transactions. If discrepancies arise, such as a refund not appearing or a dispute being incorrectly processed, contact Stripe’s support team for assistance. Understanding how these transactions are reflected on bank statements can help you address customer inquiries and maintain financial transparency.

Lastly, keep in mind that the exact wording and formatting of disputed or refunded charges on bank statements can vary depending on the bank and the country. Some banks may include additional identifiers, such as the customer’s name or a unique transaction code, to help you match the entry with Stripe’s records. Regularly reviewing both Stripe’s dashboard and your bank statements ensures you stay informed about the status of disputed or refunded transactions and can take appropriate action when needed.

Regional vs. Universal Banks: Key Differences and Unique Roles Explained

You may want to see also

Explore related products

![]()

Recurring Payments: How subscription or recurring Stripe charges appear on bank statements over time

When you sign up for a subscription or recurring service that uses Stripe for payment processing, understanding how these charges appear on your bank statement is essential for tracking your expenses. Recurring payments through Stripe typically manifest as regular, periodic deductions from your account, often with a consistent descriptor that includes the merchant’s name or a shortened version of it. For example, if you subscribe to a fitness app called "FitLife," the charge might appear as "FITLIFE*SUBSCRIPTION" or "STRIPE * FITLIFE" on your statement. This descriptor helps you identify the charge as a recurring payment rather than a one-time purchase.

The frequency of these charges depends on the subscription plan you’ve chosen—monthly, quarterly, or annually. For instance, a monthly subscription will appear as a charge every 30 or 31 days, depending on the month. Stripe ensures that the billing date remains consistent, so you can anticipate when the charge will occur. If the subscription includes a free trial period, the first charge will appear on your bank statement immediately after the trial ends, followed by regular charges at the agreed-upon intervals. It’s important to note that some banks may group recurring charges under a single entry if they occur within a short timeframe, so always check the transaction details for clarity.

Over time, recurring Stripe charges may include additional information, such as the billing cycle or invoice number, especially if the merchant uses Stripe’s invoicing feature. This can help you match the charge to a specific period or invoice sent by the merchant. For example, a charge might appear as "STRIPE * FITLIFE INV#12345" to indicate it corresponds to a particular invoice. If the subscription amount changes—due to a price increase, added taxes, or discounts—the updated amount will reflect on your statement, often accompanied by a note or descriptor explaining the change.

Disputing or canceling a recurring Stripe charge requires understanding its appearance on your statement. If you need to contest a charge, look for the merchant’s name or Stripe descriptor, along with the date and amount, to provide accurate information to your bank. Canceling a subscription typically stops future charges, but pending charges may still appear if the cancellation occurs after the billing cycle has started. Always review your bank statement regularly to ensure all recurring charges are accurate and authorized.

Finally, international subscriptions processed through Stripe may include additional details, such as currency conversion rates or foreign transaction fees, which can affect the final amount appearing on your statement. For example, a subscription billed in euros might appear in your local currency with a conversion rate applied. Familiarizing yourself with these patterns ensures you can manage and track recurring payments effectively, avoiding surprises and maintaining control over your finances.

Expired Food: Can You Donate to UK Food Banks?

You may want to see also

Frequently asked questions

Stripe charges typically appear on your bank statement with a descriptor that includes "Stripe" or the name of the business processing the payment, followed by a transaction ID or other identifying details.

Stripe charges usually appear as individual transactions on your bank statement, reflecting each payment processed separately, unless the business has set up batch payouts.

Discrepancies can occur due to currency conversions, fees, refunds, or partial payments. Always check the transaction details or contact the merchant for clarification.

Stripe charges typically appear on your bank statement within 1-3 business days after the transaction is processed, depending on your bank’s processing times.

![iPhone Charger Fast Charging,[MFi Certified] 2Pack 20W Type C Fast Charger Block with 6FT USB C to Lightning Cable Compatible for iPhone 14/13/12/11 Pro Max/Xs Max/XR/X,iPad(White)](https://m.media-amazon.com/images/I/61efNzZpXML._AC_UY218_.jpg)

![[4 Pack] USB C Charger Block Fast Charging Multiport Adpater [PD 20W USB-C & QC 3.0 USB-A Port] for i Phone 17/16/15/14/13/12/11/X/8, i Pad, Galaxy, Google, Galaxy & More](https://m.media-amazon.com/images/I/51eAnSUfXSL._AC_UY218_.jpg)

![iPhone Charger Fast Charging 2 Pack Type C Wall Charger Block with 2 Pack [6FT&10FT] Long USB C to Lightning Cable for iPhone 14/13/12/12 Pro Max/11/Xs Max/XR/X,AirPods Pro](https://m.media-amazon.com/images/I/61D9UFpTAEL._AC_UY218_.jpg)