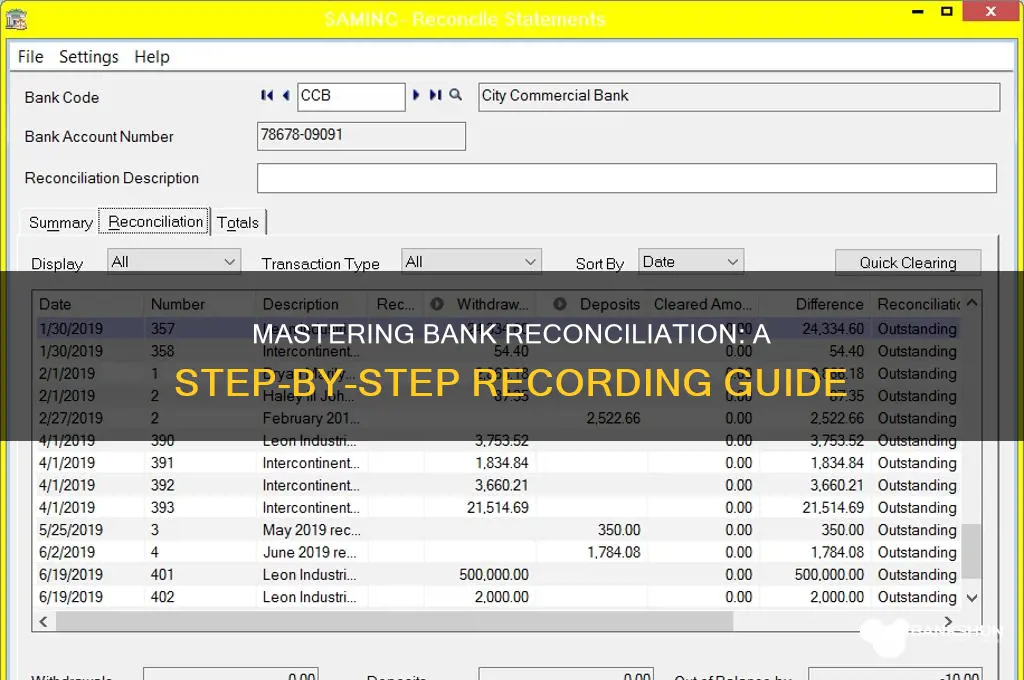

Recording a bank reconciliation is a critical process in accounting that ensures the accuracy and integrity of financial records by comparing a company's internal financial records with the bank statement provided by the financial institution. It involves identifying and explaining any discrepancies, such as outstanding checks, deposits in transit, bank fees, or errors, to align both sets of records. The process typically begins by gathering the company's ledger and the bank statement for the same period, then systematically matching transactions and documenting adjustments. Properly recording a bank reconciliation helps detect fraud, errors, or irregularities, and ensures that the company's cash balance is correctly reflected, supporting informed financial decision-making.

| Characteristics | Values |

|---|---|

| Purpose | To ensure the accuracy of a company's cash records by comparing the internal financial records with the information on the bank statement. |

| Frequency | Typically performed monthly, but can be done more frequently depending on transaction volume and business needs. |

| Key Documents | Bank statement, company's cash book (or general ledger), outstanding checks/deposits list. |

| Steps | 1. Compare Opening Balances: Ensure the ending balance from the previous reconciliation matches the beginning balance on the current bank statement. 2. Record Bank Statement Transactions: Add deposits and subtract withdrawals from the bank statement to the company's cash book. 3. Record Outstanding Items: Account for checks issued but not yet cleared by the bank (outstanding checks) and deposits in transit (not yet reflected on the bank statement). 4. Identify Discrepancies: Highlight any differences between the adjusted cash book balance and the bank statement balance. 5. Investigate Discrepancies: Research and resolve any discrepancies, such as bank errors, uncleared checks, or unrecorded transactions. 6. Make Adjusting Entries: Record necessary adjustments in the company's accounting system to reflect the correct cash balance. 7. Prepare Reconciliation Statement: Document the reconciliation process, including adjustments and explanations for discrepancies. |

| Outcome | A reconciled cash balance that matches between the company's records and the bank statement, ensuring financial accuracy and identifying potential errors. |

| Tools | Manual reconciliation (spreadsheets), accounting software with built-in reconciliation features. |

| Importance | Prevents fraud, detects errors, ensures accurate financial reporting, and maintains good cash flow management. |

Explore related products

What You'll Learn

- Gather Statements: Collect bank and accounting records for the reconciliation period

- Compare Balances: Match ending balances from both bank and accounting records

- Identify Discrepancies: Note unmatched transactions, outstanding checks, or deposits in transit

- Adjust Entries: Record corrections for errors, fees, or interest in accounting books

- Finalize Reconciliation: Document adjustments, ensure balances match, and sign off

![]()

Gather Statements: Collect bank and accounting records for the reconciliation period

To begin the bank reconciliation process, the first critical step is to Gather Statements: Collect bank and accounting records for the reconciliation period. This involves obtaining both the bank statement and the internal accounting records for the same time frame. Start by requesting the bank statement directly from your financial institution, ensuring it covers the exact period you intend to reconcile. Most banks provide monthly statements, but you can also access interim statements through online banking platforms. Verify that the statement includes all transactions, such as deposits, withdrawals, fees, and interest earned, as these details are essential for accurate reconciliation.

Simultaneously, compile your internal accounting records for the corresponding period. This typically includes the general ledger, cash book, or any other accounting system where cash transactions are recorded. Ensure these records are up-to-date and reflect all transactions that should have impacted your bank account during the reconciliation period. Cross-check the dates to confirm alignment between the bank statement and your accounting records, as discrepancies in the time frame can lead to errors in the reconciliation process.

Organize both sets of documents in a clear and accessible manner. For the bank statement, highlight or list key transactions such as opening and closing balances, deposits, checks issued, and bank charges. Similarly, for your accounting records, identify and list all cash transactions, including those that may not yet have appeared on the bank statement, such as outstanding checks or deposits in transit. This structured approach ensures that you have a comprehensive view of all relevant financial activities.

If your business uses accounting software, export or print the relevant reports for the reconciliation period. Double-check that the software’s date range matches the bank statement’s period to avoid missing or duplicating transactions. For manual systems, ensure all entries in the cash book or ledger are complete and accurately dated. This step is crucial, as incomplete or misdated records can complicate the reconciliation process and lead to incorrect adjustments.

Finally, before proceeding to the next step, verify the integrity of both the bank statement and accounting records. Confirm that the opening balance on the bank statement matches the closing balance from the previous reconciliation period. Similarly, ensure the opening balance in your accounting records aligns with the previous period’s closing balance. This verification step helps identify any discrepancies early on and ensures a smooth and accurate reconciliation process. By meticulously gathering and organizing these statements, you lay a solid foundation for the subsequent steps in recording a bank reconciliation.

Currency Exchange: AIB Bank's Services in Ireland

You may want to see also

Explore related products

![]()

Compare Balances: Match ending balances from both bank and accounting records

When performing a bank reconciliation, the first critical step is to compare balances by matching the ending balances from both the bank statement and the accounting records. This process ensures that the financial records align and helps identify any discrepancies. Begin by obtaining the most recent bank statement, which typically provides the ending balance as of the statement’s cutoff date. Simultaneously, pull up the corresponding ending balance from the company’s accounting records, such as the general ledger or cash account, for the same period. Both balances should reflect the same date to ensure an accurate comparison. If the dates do not align, adjust the accounting records by adding or subtracting transactions that have not yet cleared the bank.

Once the dates are synchronized, directly compare the ending balance from the bank statement to the adjusted ending balance in the accounting records. If the balances match, it indicates that the records are in agreement, and no further adjustments are needed for this step. However, if the balances do not match, it signals the presence of discrepancies that require investigation. Common reasons for mismatches include outstanding checks, unrecorded deposits, bank fees, or interest income that has not been accounted for in the company’s records. At this stage, the goal is to identify the source of the discrepancy, not to resolve it, as subsequent steps in the reconciliation process will address these issues.

To facilitate the comparison, create a reconciliation worksheet or use accounting software that includes a bank reconciliation module. List the ending balance from the bank statement on one side and the ending balance from the accounting records on the other. If the balances do not match, note the difference between the two amounts. This difference will guide the next steps in identifying and reconciling the discrepancies. For example, if the bank statement shows a higher balance, it may indicate deposits in transit that have not yet been recorded in the accounting system. Conversely, if the accounting records show a higher balance, it could be due to outstanding checks that have not yet cleared the bank.

It is essential to approach this step methodically, ensuring that all transactions are accounted for and properly timed. Double-check that all deposits and withdrawals are recorded accurately in both the bank statement and the accounting records. Pay close attention to timing differences, such as transactions that occurred just before or after the statement cutoff date. These transactions may need to be adjusted in the accounting records to align with the bank statement. By meticulously comparing the balances and identifying discrepancies, you lay the foundation for a thorough and accurate bank reconciliation.

Finally, document the comparison process clearly, noting any discrepancies and the steps taken to identify them. This documentation is crucial for audit purposes and ensures transparency in the reconciliation process. If using accounting software, ensure that the reconciliation module captures all adjustments and discrepancies for future reference. Once the balances are compared and discrepancies are identified, proceed to the next steps of the reconciliation process, such as accounting for outstanding checks, deposits in transit, and other reconciling items. Accurate comparison of balances is the cornerstone of a successful bank reconciliation, providing a clear starting point for resolving any discrepancies and ensuring the integrity of financial records.

BMO Harris Bank: What Does the Name Stand For?

You may want to see also

Explore related products

![]()

Identify Discrepancies: Note unmatched transactions, outstanding checks, or deposits in transit

When identifying discrepancies during a bank reconciliation, the first step is to carefully compare the company’s internal records (such as the general ledger) with the bank statement. Unmatched transactions are a common issue and should be noted immediately. These occur when a transaction appears on one record but not the other. For example, a payment recorded in the company’s books might not yet be reflected on the bank statement, or vice versa. To identify these, list all transactions from both sources side by side and mark any entries that do not align. This process ensures no transaction is overlooked and helps in pinpointing the exact nature of the discrepancy.

Outstanding checks are another critical area to examine. These are checks issued by the company but not yet cleared by the bank. To identify them, compile a list of all checks written during the period and compare it with the bank statement. Any checks that have not been presented to the bank for payment should be noted as outstanding. This step is crucial because outstanding checks reduce the company’s available bank balance, even if they are not yet reflected in the bank’s records. Tracking these ensures the reconciled balance accurately reflects the company’s true financial position.

Deposits in transit are equally important to identify. These are deposits made by the company but not yet credited by the bank. Review the company’s records for any deposits recorded during the period and cross-reference them with the bank statement. If a deposit appears in the company’s books but not on the bank statement, it is considered in transit. Note these deposits separately, as they increase the company’s book balance but are not yet part of the bank’s recorded balance. Properly accounting for deposits in transit ensures the reconciliation process is accurate and complete.

To systematically note these discrepancies, create a reconciliation worksheet or use accounting software that allows for detailed tracking. For unmatched transactions, document the date, amount, and description of each missing entry. For outstanding checks, list the check number, payee, and amount. For deposits in transit, record the date, amount, and source of the deposit. This organized approach ensures that all discrepancies are clearly identified and can be investigated further. Once noted, these discrepancies will need to be adjusted to align the company’s records with the bank statement, bringing the reconciliation process one step closer to completion.

Finally, it’s essential to verify the accuracy of the identified discrepancies. Double-check the dates and amounts to ensure no errors were made during the initial comparison. For instance, confirm that outstanding checks and deposits in transit fall within the reconciliation period. If any discrepancies remain unclear, investigate further by reviewing supporting documents such as check stubs or deposit slips. This meticulous approach minimizes the risk of errors and ensures the bank reconciliation is reliable and trustworthy. By thoroughly identifying and documenting unmatched transactions, outstanding checks, and deposits in transit, the reconciliation process becomes a powerful tool for maintaining accurate financial records.

Stadium Seating Capacity: US Bank Stadium

You may want to see also

Explore related products

![]()

Adjust Entries: Record corrections for errors, fees, or interest in accounting books

When performing a bank reconciliation, one critical step is to adjust entries to ensure that the accounting records accurately reflect the true financial position. Adjusting entries are necessary to correct errors, account for bank fees, or record interest income that may not yet be captured in the company’s books. These adjustments are essential for aligning the bank statement with the internal accounting records. To begin, identify discrepancies between the bank statement and the company’s cash account. Common discrepancies include uncleared checks, unrecorded deposits, bank service charges, and interest earned on the account. Once identified, these items must be recorded in the accounting system through journal entries.

To record corrections for errors, first determine the nature of the mistake. For example, if a payment was recorded twice in the company’s books but only once on the bank statement, a reversing entry is required. Debit the expense account and credit the cash account to remove the duplicate entry. Conversely, if a transaction was omitted, record it by debiting or crediting the appropriate account and adjusting the cash balance accordingly. Ensure that supporting documentation, such as invoices or receipts, is available to justify the correction. Accuracy is crucial, as errors can distort financial statements and lead to misinformed business decisions.

Bank fees are another common adjustment during reconciliation. These fees, such as monthly service charges or overdraft fees, are typically deducted directly from the bank account but may not be recorded in the company’s books. To account for these fees, debit the appropriate expense account (e.g., "Bank Fees") and credit the cash account. This entry reduces both the expense category and the cash balance, ensuring the books reflect the actual outflow of funds. Regularly reviewing the bank statement for such charges helps maintain up-to-date financial records and prevents discrepancies in future reconciliations.

Interest income earned on bank balances is often credited to the account by the bank but not recorded in the company’s books until the reconciliation process. To capture this income, debit the cash account and credit the interest income account. This entry increases both the cash balance and the revenue, accurately reflecting the company’s financial position. It is important to verify the interest amount on the bank statement and ensure it aligns with the account’s terms. Recording interest income promptly ensures compliance with accrual accounting principles and provides a complete picture of the company’s earnings.

Finally, after making all necessary adjustments, update the accounting records and reconcile the bank statement again to confirm that both balances match. This step ensures that all discrepancies have been addressed and that the financial statements are accurate. Proper documentation of each adjusting entry is vital for audit purposes and transparency. By meticulously recording corrections for errors, fees, and interest, businesses can maintain reliable financial records and make informed decisions based on accurate data. Adjusting entries are a fundamental aspect of bank reconciliation, reinforcing the integrity of the accounting process.

Do Netherlands Banks Accept Foreign Cheque Payments? A Comprehensive Guide

You may want to see also

Explore related products

![]()

Finalize Reconciliation: Document adjustments, ensure balances match, and sign off

Once all discrepancies between the bank statement and the company's records have been identified and investigated, the next critical step is to finalize the reconciliation. This phase involves documenting adjustments, ensuring balances match, and formally signing off on the process. Begin by recording all necessary adjustments in the company's accounting system. For example, if an outstanding deposit or uncleared check was identified, update the cash account to reflect these changes. Similarly, if errors such as duplicate entries or omitted transactions were found, correct them in the ledger. Each adjustment should be clearly documented with a detailed explanation, including the date, amount, and reason for the change. This ensures transparency and provides a clear audit trail for future reference.

After making all adjustments, verify that the adjusted book balance matches the bank statement balance. Double-check the calculations to ensure accuracy, as even a small discrepancy can indicate an unresolved issue. Use a reconciliation worksheet or software to compare the two balances side by side, making it easier to spot any remaining differences. If the balances still do not match, revisit the earlier steps to identify any overlooked items, such as interest earned, bank fees, or outstanding transactions. It is crucial to resolve all discrepancies before proceeding to the final sign-off.

Once the balances match, prepare a formal reconciliation report summarizing the process. This report should include the beginning and ending bank statement balances, the company's beginning and adjusted book balances, and a list of all adjustments made during the reconciliation. Attach supporting documentation, such as the bank statement, canceled checks, and deposit slips, to the report for completeness. The reconciliation report serves as a formal record of the process and is essential for internal controls and external audits.

The final step is to sign off on the reconciliation, indicating that the process has been completed accurately and thoroughly. The person responsible for the reconciliation, typically the accountant or bookkeeper, should sign and date the report. In some organizations, a second person, such as a supervisor or manager, may also be required to review and sign off on the reconciliation to ensure accountability and accuracy. Once signed, file the reconciliation report in a secure location, either physically or digitally, for easy access during audits or future reference.

By meticulously documenting adjustments, verifying matching balances, and formally signing off, the reconciliation process is finalized effectively. This ensures the company's financial records are accurate, reliable, and compliant with accounting standards. Finalizing the reconciliation not only maintains the integrity of the company's financial data but also provides confidence to stakeholders that the company's cash management is under control.

Bank CDs vs Brokered CDs: Which is the Better Investment?

You may want to see also

Frequently asked questions

A bank reconciliation is the process of comparing a company's internal financial records with the bank statement to ensure accuracy and identify discrepancies. It is important for detecting errors, fraud, or unrecorded transactions, and for maintaining accurate financial records.

You will need the company's internal cash book or ledger, the bank statement for the period, and any supporting documents like deposit slips, canceled checks, or electronic transaction records.

Begin by ensuring both the company's records and the bank statement cover the same period. Then, compare the opening balances of both records to ensure they match before proceeding with the reconciliation.

Investigate the discrepancies by reviewing supporting documents and transaction details. Common issues include outstanding deposits, uncleared checks, bank fees, or errors in recording. Adjust the company's records or note unresolved items for follow-up.

It is best practice to perform a bank reconciliation monthly, as it helps catch and resolve discrepancies promptly and ensures financial records remain accurate and up-to-date.