A bank can become a trustee by meeting specific legal and regulatory requirements, typically outlined in the jurisdiction where it operates. This process involves obtaining the necessary licenses and approvals from financial authorities, demonstrating robust fiduciary capabilities, and ensuring compliance with trust laws. Banks must establish a dedicated trust department staffed with qualified professionals who can manage trust assets responsibly. Additionally, they must adhere to strict ethical standards, maintain transparency, and safeguard the interests of beneficiaries. Becoming a trustee allows a bank to offer specialized services such as estate planning, asset management, and trust administration, thereby expanding its financial offerings and serving clients with complex wealth management needs.

| Characteristics | Values |

|---|---|

| Legal Framework | Banks must comply with local trust laws and regulations (e.g., Trust Law, Banking Act). |

| Licensing & Authorization | Requires approval from regulatory bodies (e.g., Central Bank, Financial Services Authority). |

| Capital Requirements | Must meet minimum capital adequacy ratios to ensure financial stability. |

| Expertise & Infrastructure | Needs specialized trust departments, trained staff, and robust systems. |

| Fiduciary Responsibility | Must act in the best interest of beneficiaries, adhering to fiduciary duties. |

| Compliance & Reporting | Obligated to maintain transparency, file reports, and undergo audits. |

| Risk Management | Must implement policies to mitigate risks associated with trust management. |

| Client Due Diligence (CDD) | Required to perform thorough KYC (Know Your Customer) checks on clients. |

| Separation of Assets | Trust assets must be segregated from the bank's proprietary assets. |

| Fee Structure | Transparent fee schedules for trust services must be established. |

| Dispute Resolution | Mechanisms for resolving conflicts between trustees, beneficiaries, and settlors. |

| International Standards | Adherence to global standards (e.g., FATF, Basel III) if operating cross-border. |

| Ethical Conduct | Commitment to ethical practices and avoidance of conflicts of interest. |

| Technology & Security | Use of secure digital platforms to manage trust accounts and data. |

| Succession Planning | Clear policies for trustee succession in case of bank mergers or closures. |

Explore related products

What You'll Learn

![]()

Legal Requirements and Eligibility Criteria

To become a trustee, a bank must adhere to a stringent set of legal requirements and eligibility criteria that ensure it can fulfill the fiduciary responsibilities associated with the role. Firstly, the bank must be a legally recognized financial institution, typically chartered under federal or state banking laws. This charter serves as the foundational legal framework, ensuring the bank operates within the boundaries of financial regulations. Additionally, the bank must demonstrate compliance with the laws governing trusts, which vary by jurisdiction but often include adherence to the Uniform Trust Code (UTC) in the United States. Compliance with these laws is critical, as trustees are held to a high standard of care and loyalty in managing trust assets.

Secondly, banks seeking to act as trustees must meet specific regulatory requirements imposed by financial oversight bodies such as the Office of the Comptroller of the Currency (OCC) or the Federal Reserve in the U.S., or equivalent authorities in other countries. These regulators often require banks to obtain specific approvals or licenses to offer trust services. For instance, in the U.S., a bank must file an application with the OCC to engage in fiduciary activities, including acting as a trustee. The application process involves demonstrating the bank’s financial stability, operational capacity, and internal controls to ensure it can manage trust assets effectively and ethically.

Another critical aspect of eligibility is the bank’s organizational structure and expertise. Banks must have a dedicated trust department staffed with professionals who possess the necessary legal, financial, and administrative expertise to manage trusts. This includes trust officers, legal advisors, and compliance specialists who understand the complexities of trust administration, tax implications, and beneficiary rights. The bank must also establish robust internal policies and procedures to prevent conflicts of interest and ensure transparency in trust management.

Furthermore, banks must meet capital and financial stability requirements to qualify as trustees. Regulatory bodies often mandate minimum capital thresholds to ensure the bank has sufficient resources to withstand financial challenges without compromising trust assets. Banks are also required to maintain adequate insurance, such as fidelity bonds, to protect trust assets from losses due to fraud or mismanagement. Financial stability is crucial, as trustees are often responsible for long-term management of assets, and beneficiaries rely on the bank’s ability to safeguard their interests over time.

Lastly, banks must satisfy ethical and reputational standards to be eligible as trustees. Regulatory bodies assess the bank’s history of compliance, litigation, and customer complaints to gauge its reliability and integrity. A bank with a record of unethical practices or regulatory violations may be disqualified from acting as a trustee. Maintaining a strong reputation for trustworthiness and ethical conduct is essential, as trustees are entrusted with sensitive and valuable assets, often involving vulnerable beneficiaries such as minors or elderly individuals.

In summary, becoming a trustee requires a bank to navigate a complex web of legal, regulatory, and ethical requirements. From obtaining the necessary licenses and approvals to maintaining financial stability and ethical standards, the eligibility criteria are designed to ensure banks can fulfill their fiduciary duties with competence and integrity. Banks must invest in the right infrastructure, expertise, and compliance mechanisms to meet these demands and earn the trust of clients and regulators alike.

Are Asha Banks and Matthew Broome Dating?

You may want to see also

Explore related products

![]()

Regulatory Compliance and Licensing Process

To become a trustee, a bank must navigate a rigorous Regulatory Compliance and Licensing Process that ensures it meets the legal, ethical, and operational standards required to manage trust assets responsibly. This process involves multiple steps, each designed to safeguard the interests of beneficiaries and maintain the integrity of the financial system.

The first step in this process is understanding the regulatory framework governing trust services. In most jurisdictions, banks must comply with laws such as the Trust Indenture Act (in the U.S.) or equivalent regulations in other countries. These laws outline the fiduciary duties of a trustee, including loyalty, prudence, and impartiality. Banks must also adhere to guidelines set by financial regulators, such as the Office of the Comptroller of the Currency (OCC) in the U.S. or the Financial Conduct Authority (FCA) in the UK. Familiarity with these regulations is essential to ensure compliance from the outset.

Next, the bank must obtain the necessary licenses to operate as a trustee. This typically involves submitting a detailed application to the relevant regulatory authority, which may include information about the bank’s financial stability, internal controls, and risk management practices. The application often requires a business plan outlining how the bank intends to fulfill its trustee obligations, including the management of trust assets and the resolution of potential conflicts of interest. Regulatory authorities may also conduct on-site inspections or interviews to verify the bank’s readiness.

Ongoing compliance is a critical component of the process. Once licensed, the bank must adhere to strict reporting requirements, including regular financial disclosures and audits. Trustees are often required to maintain separate accounts for trust assets to prevent commingling with the bank’s own funds. Additionally, banks must implement robust internal policies and procedures to ensure compliance with anti-money laundering (AML) laws, know-your-customer (KYC) regulations, and data protection standards. Failure to meet these requirements can result in penalties, license revocation, or legal action.

Finally, banks must demonstrate expertise and ethical conduct in trust administration. This includes employing qualified personnel with specialized knowledge in trust law, estate planning, and asset management. Trustees are held to a high ethical standard, and banks must establish mechanisms to address potential conflicts of interest, such as independent review boards or ethical guidelines. Continuous training and professional development for staff are also essential to stay updated on regulatory changes and best practices.

In summary, the Regulatory Compliance and Licensing Process for a bank to become a trustee is comprehensive and demanding. It requires a deep understanding of legal obligations, meticulous preparation for licensing, ongoing adherence to regulatory standards, and a commitment to ethical trust administration. By successfully navigating this process, a bank can establish itself as a trusted fiduciary, capable of managing trust assets with integrity and competence.

Notary Services: Banks and Beyond

You may want to see also

Explore related products

![]()

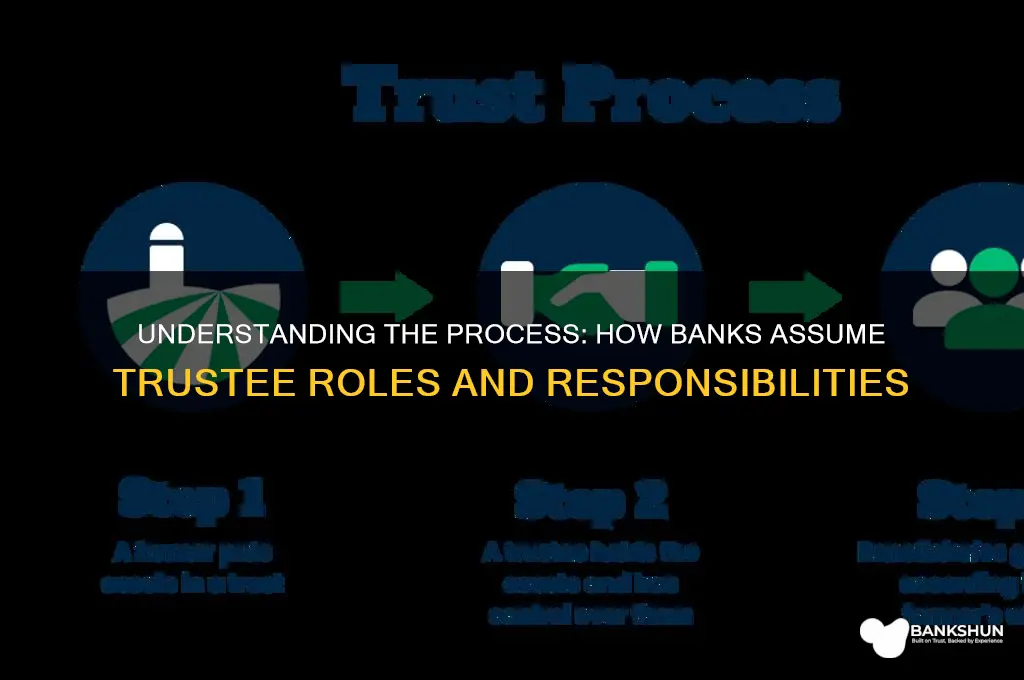

Trustee Roles and Responsibilities

A bank can become a trustee by meeting specific legal and regulatory requirements, demonstrating expertise in trust administration, and adhering to fiduciary standards. Once appointed, the bank assumes critical roles and responsibilities as a trustee, which are governed by the terms of the trust agreement and applicable laws. The primary role of a bank as trustee is to act as a fiduciary, meaning it must prioritize the best interests of the trust’s beneficiaries above all else. This involves managing trust assets with diligence, prudence, and loyalty, ensuring compliance with the trust’s objectives and legal obligations.

One of the key responsibilities of a bank trustee is asset management. This includes investing trust assets in accordance with the trust document, beneficiary needs, and prudent investment practices. The bank must diversify investments to minimize risk while maximizing returns, all within the framework of the trust’s goals and the beneficiaries’ long-term interests. Regular monitoring and adjustment of the investment portfolio are essential to ensure alignment with changing market conditions and beneficiary circumstances.

Another critical responsibility is trust administration, which involves handling day-to-day operations such as record-keeping, tax filings, and distribution of income or principal to beneficiaries. The bank must maintain accurate and transparent records of all transactions, ensuring compliance with tax laws and trust provisions. Additionally, the trustee is responsible for interpreting the trust document and making discretionary decisions when necessary, always acting in good faith and within the scope of its authority.

Communication with beneficiaries is a vital aspect of a bank’s trustee role. The bank must keep beneficiaries informed about the trust’s status, investment performance, and any significant decisions affecting their interests. This includes providing regular reports, responding to inquiries, and addressing concerns in a timely and transparent manner. Effective communication builds trust and ensures beneficiaries understand their rights and the trustee’s actions.

Finally, a bank trustee must exercise impartiality when managing trusts with multiple beneficiaries or conflicting interests. This involves balancing the needs of current and future beneficiaries, as well as those with differing priorities. The bank must avoid conflicts of interest and, if they arise, disclose and manage them appropriately. Upholding ethical standards and acting with integrity are paramount to maintaining trust and fulfilling fiduciary duties.

In summary, a bank’s roles and responsibilities as a trustee encompass fiduciary duty, asset management, trust administration, beneficiary communication, and impartial decision-making. By adhering to these responsibilities, a bank ensures the trust is managed effectively, beneficiaries’ interests are protected, and legal and ethical standards are upheld. Becoming a trustee requires not only the necessary qualifications but also a commitment to acting in the best interests of those the trust serves.

Does Bend Schwab Bank Offer ATM Access? Find Out Here

You may want to see also

Explore related products

![]()

Capital and Operational Infrastructure Needs

To become a trustee, a bank must meet stringent regulatory, financial, and operational requirements. One of the critical aspects of this transformation is addressing Capital and Operational Infrastructure Needs. These needs are multifaceted, encompassing financial stability, technological capabilities, and robust operational frameworks to ensure compliance and effective trust administration.

Capital Requirements are paramount for a bank aspiring to act as a trustee. Regulatory bodies, such as the Office of the Comptroller of the Currency (OCC) in the U.S. or equivalent authorities globally, mandate that banks maintain sufficient capital to absorb potential losses and ensure the safety of trust assets. This involves not only meeting Basel III capital adequacy ratios but also allocating additional reserves specifically for trust operations. The bank must demonstrate the ability to manage fiduciary risks, including those associated with asset custody, investment management, and beneficiary interests. Capital planning should include stress testing to ensure resilience under adverse economic conditions, as trustees are often responsible for long-term asset management.

In addition to capital, Operational Infrastructure must be robust and scalable. This includes investing in secure, compliant, and efficient systems for trust accounting, asset management, and reporting. The bank needs to implement specialized software that can handle complex trust structures, tax reporting, and beneficiary communications. Cybersecurity is another critical component, as trustees are entrusted with sensitive client data and assets. Infrastructure must be designed to prevent breaches and ensure business continuity in the face of cyber threats or operational disruptions.

Human Capital and Expertise form another layer of operational infrastructure needs. The bank must employ or train professionals with expertise in trust law, estate planning, tax regulations, and investment management. These individuals are responsible for interpreting complex legal documents, making discretionary decisions in the best interest of beneficiaries, and ensuring compliance with fiduciary standards. Continuous training and development programs are essential to keep staff updated on regulatory changes and industry best practices.

Finally, Compliance and Risk Management Frameworks are integral to the operational infrastructure. The bank must establish a comprehensive compliance program that includes regular audits, risk assessments, and reporting mechanisms. This framework should align with both banking regulations and trust-specific laws, such as the Uniform Trust Code in the U.S. The bank must also implement policies to manage conflicts of interest, ensure transparency, and maintain the integrity of trust operations. Investing in these areas not only satisfies regulatory requirements but also builds trust with clients and beneficiaries.

In summary, becoming a trustee requires a bank to address significant Capital and Operational Infrastructure Needs. From maintaining adequate financial reserves to building advanced technological systems, employing skilled professionals, and establishing robust compliance frameworks, each component is essential for fulfilling fiduciary responsibilities effectively. By strategically investing in these areas, a bank can position itself as a reliable and competent trustee in the eyes of regulators and clients alike.

Tick Presence at High Banks Metro Park: What You Need to Know

You may want to see also

Explore related products

$14.99

![]()

Application and Approval by Authorities

To become a trustee, a bank must undergo a rigorous application and approval process overseen by regulatory authorities. This process ensures that the bank meets the necessary legal, financial, and operational standards to act as a fiduciary. The first step involves submitting a formal application to the relevant regulatory body, which in many jurisdictions is the banking or financial services authority. This application typically includes detailed documentation about the bank’s financial stability, operational capabilities, and compliance history. The bank must demonstrate its ability to manage trust assets responsibly, adhere to fiduciary duties, and protect the interests of beneficiaries.

Upon submission, the regulatory authority conducts a thorough review of the application. This review often includes an assessment of the bank’s internal policies, risk management frameworks, and the qualifications of its personnel responsible for trust operations. The authority may also evaluate the bank’s track record in handling similar financial responsibilities and its adherence to anti-money laundering (AML) and know-your-customer (KYC) regulations. In some cases, the regulator may require additional information or conduct on-site inspections to verify the bank’s readiness to act as a trustee.

Once the initial review is complete, the bank may be required to participate in interviews or hearings with regulatory officials. These interactions allow the authority to clarify any concerns, assess the bank’s commitment to fiduciary responsibilities, and gauge its understanding of the legal and ethical obligations involved. The bank must also provide evidence of its capacity to segregate trust assets from its own assets and maintain accurate records to ensure transparency and accountability.

Following the assessment, the regulatory authority makes a decision on the application. If approved, the bank is granted a license or authorization to act as a trustee. This approval is often conditional, requiring the bank to comply with ongoing regulatory requirements, such as regular reporting, audits, and adherence to specific fiduciary standards. Failure to meet these conditions can result in the revocation of the trustee status.

In some jurisdictions, the approval process may involve coordination with multiple authorities, especially if the bank operates across different regions or handles international trust arrangements. For instance, cross-border trusts may require additional approvals from tax authorities or international financial regulators. Throughout this process, the bank must remain transparent and cooperative with all relevant bodies to ensure a smooth approval.

Finally, after obtaining approval, the bank must formally accept the trustee role and begin fulfilling its fiduciary duties. This includes setting up the necessary infrastructure, appointing qualified trust officers, and establishing procedures to manage trust assets effectively. The bank’s transition into a trustee role marks the culmination of a detailed and stringent application and approval process, ensuring it is well-equipped to handle the responsibilities entrusted to it.

Wells Fargo Mobile Banking App: Features, Benefits, and How to Use

You may want to see also

Frequently asked questions

A bank must meet regulatory requirements, including being licensed as a financial institution, demonstrating financial stability, and having the necessary expertise in trust administration, legal compliance, and fiduciary responsibilities.

As a trustee, a bank manages assets held in trust on behalf of beneficiaries, ensuring compliance with the trust agreement, making distributions, and acting in the best interest of the beneficiaries while adhering to legal and ethical standards.

A bank typically applies through the relevant regulatory authority, such as the Office of the Comptroller of the Currency (OCC) in the U.S., by submitting an application, demonstrating compliance with trust laws, and undergoing a review of its operational and financial capabilities.

A bank trustee is legally obligated to act with prudence, loyalty, and impartiality, avoid conflicts of interest, maintain accurate records, and comply with the terms of the trust document and applicable laws.