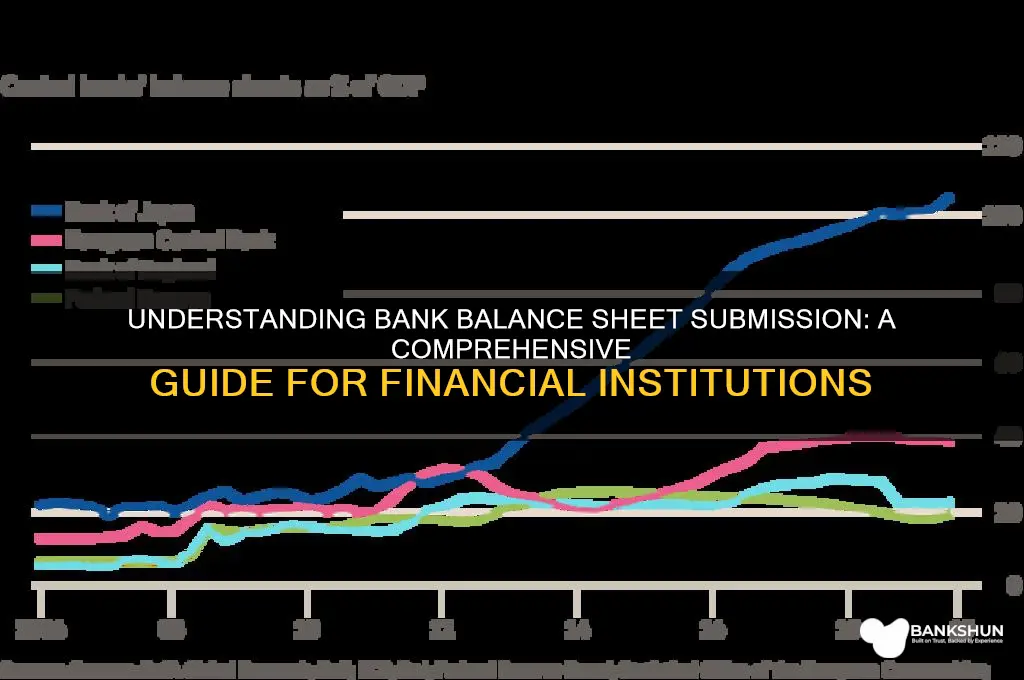

Banks submit their balance sheets as part of their regulatory reporting requirements to ensure transparency, accountability, and financial stability. Typically, this process involves preparing a detailed statement that outlines the bank's assets, liabilities, and equity at a specific point in time, often quarterly or annually. The balance sheet is compiled in accordance with accounting standards such as GAAP (Generally Accepted Accounting Principles) or IFRS (International Financial Reporting Standards) and is audited by external auditors to ensure accuracy and compliance. Banks then submit these documents to regulatory bodies like the Federal Reserve in the U.S., the European Central Bank in the EU, or other relevant authorities, depending on their jurisdiction. Additionally, banks may also disclose their balance sheets to shareholders and the public through financial reports to maintain investor confidence and market trust.

Explore related products

What You'll Learn

- Regulatory Requirements: Banks must adhere to specific guidelines for balance sheet submission to regulatory bodies

- Frequency of Submission: Quarterly or annual filings depend on regulatory and internal policies

- Data Accuracy: Ensuring all financial data is precise and reflects the bank’s true position

- Audit Compliance: Balance sheets must be audited by external firms for transparency and accuracy

- Reporting Standards: Adherence to GAAP, IFRS, or other accounting standards is mandatory

![]()

Regulatory Requirements: Banks must adhere to specific guidelines for balance sheet submission to regulatory bodies

Banks are subject to stringent regulatory requirements when submitting their balance sheets to ensure transparency, accuracy, and compliance with financial laws. Regulatory bodies such as the Federal Reserve in the United States, the European Central Bank (ECB) in the Eurozone, or the Reserve Bank of India (RBI) mandate specific guidelines that banks must follow. These guidelines often include standardized formats, reporting frequencies, and disclosure requirements to maintain consistency across the banking sector. For instance, banks may be required to submit their balance sheets quarterly, semi-annually, or annually, depending on the jurisdiction and the size of the institution.

One critical aspect of regulatory requirements is the adherence to accounting standards, such as the International Financial Reporting Standards (IFRS) or the Generally Accepted Accounting Principles (GAAP). These standards dictate how assets, liabilities, and equity are classified, measured, and reported on the balance sheet. Banks must ensure that their financial statements are prepared in accordance with these standards to provide a true and fair view of their financial position. Regulatory bodies often conduct audits or reviews to verify compliance, imposing penalties for discrepancies or non-compliance.

In addition to accounting standards, banks must comply with specific regulatory frameworks designed to monitor and mitigate financial risks. For example, Basel III, an international regulatory framework, sets minimum capital requirements, liquidity ratios, and leverage ratios that banks must maintain. When submitting their balance sheets, banks are required to include detailed breakdowns of capital adequacy, risk-weighted assets, and liquidity positions to demonstrate compliance with these regulations. Failure to meet these requirements can result in regulatory intervention, including restrictions on operations or financial penalties.

Regulatory bodies also mandate the submission of supplementary reports alongside the balance sheet to provide a comprehensive view of a bank's financial health. These reports may include profit and loss statements, cash flow statements, and notes to the financial statements that explain significant accounting policies, contingent liabilities, and off-balance-sheet exposures. Banks must ensure that these documents are accurate, complete, and submitted within the stipulated deadlines. Timely and transparent reporting is essential to maintain market confidence and regulatory trust.

Furthermore, banks operating across multiple jurisdictions must navigate varying regulatory requirements, as different countries or regions may have distinct reporting standards and timelines. For instance, a multinational bank may need to submit its balance sheet in compliance with both local regulations and the standards of its parent country. This complexity necessitates robust internal processes and systems to ensure consistent and accurate reporting across all regulatory environments. Banks often invest in advanced financial reporting tools and compliance teams to manage these obligations effectively.

Lastly, regulatory requirements for balance sheet submission are continually evolving to address emerging risks and challenges in the financial sector. Banks must stay abreast of regulatory updates and adapt their reporting practices accordingly. This includes implementing new data collection methods, enhancing risk management frameworks, and ensuring that their balance sheets reflect the latest regulatory expectations. By adhering to these guidelines, banks not only fulfill their legal obligations but also contribute to the stability and integrity of the broader financial system.

Does Nirvana Seed Bank Ship to the US? Find Out Here

You may want to see also

Explore related products

![]()

Frequency of Submission: Quarterly or annual filings depend on regulatory and internal policies

Banks are required to submit their balance sheets at regular intervals, with the frequency of submission depending on both regulatory requirements and internal policies. Regulatory bodies, such as central banks or financial authorities, typically mandate the submission of balance sheets to ensure transparency, monitor financial health, and maintain stability within the banking sector. These submissions are crucial for regulatory oversight, allowing authorities to assess a bank's liquidity, solvency, and overall risk exposure. The frequency of these filings can vary significantly across jurisdictions, with some regulators requiring quarterly submissions, while others may mandate annual reports.

In many countries, banks are obligated to submit their balance sheets on a quarterly basis. This frequent reporting is often necessitated by the dynamic nature of banking operations and the need for regulators to stay abreast of any significant changes in a bank's financial position. Quarterly filings enable regulators to identify potential risks early, such as asset quality deterioration or liquidity shortages, and take corrective actions promptly. For instance, in the United States, banks are required to file the Consolidated Reports of Condition and Income (Call Reports) quarterly, providing detailed information on their balance sheets, income statements, and other key financial metrics.

Annual filings, on the other hand, are more common in jurisdictions where regulatory frameworks prioritize a broader, long-term view of a bank's financial health. Annual submissions typically provide a comprehensive overview of a bank's financial performance and position over the entire fiscal year. This approach allows regulators to analyze trends, assess the effectiveness of a bank's risk management strategies, and evaluate its compliance with prudential norms. In the European Union, for example, banks are required to submit annual financial statements, including balance sheets, as part of their supervisory reporting obligations under the Capital Requirements Regulation (CRR).

Internal policies also play a significant role in determining the frequency of balance sheet submissions. Banks often maintain their own reporting schedules, which may be more frequent than regulatory requirements, to facilitate internal decision-making, risk management, and strategic planning. For instance, a bank's management may require monthly or even weekly updates on key balance sheet metrics to monitor liquidity, manage capital adequacy, and ensure compliance with internal risk limits. These internal submissions are typically more detailed and tailored to the bank's specific needs, providing a granular view of its financial position.

The interplay between regulatory and internal policies can result in a multi-tiered reporting structure, where banks submit balance sheets at different frequencies to various stakeholders. For example, a bank may file quarterly reports to regulators, monthly updates to its board of directors, and weekly snapshots to senior management. This layered approach ensures that all relevant parties have access to timely and accurate financial information, enabling them to fulfill their respective roles effectively. Ultimately, the frequency of balance sheet submissions reflects a balance between regulatory oversight, internal governance, and the need for timely financial information in the fast-paced banking industry.

Navigating Inflation: How Banks Adapt and Thrive in Rising Costs

You may want to see also

Explore related products

$8.5

![]()

Data Accuracy: Ensuring all financial data is precise and reflects the bank’s true position

Banks must prioritize data accuracy when submitting their balance sheets to ensure compliance with regulatory requirements and maintain stakeholder trust. This involves implementing robust processes to verify the precision of all financial data, from asset and liability valuations to equity and reserve calculations. Every figure reported must reflect the bank’s true financial position at the time of submission. To achieve this, banks employ automated systems and manual checks to cross-verify data, ensuring consistency across all financial statements. Discrepancies, no matter how minor, are investigated and resolved before submission to prevent misrepresentations that could lead to regulatory penalties or reputational damage.

One critical aspect of ensuring data accuracy is the use of standardized accounting principles, such as GAAP (Generally Accepted Accounting Principles) or IFRS (International Financial Reporting Standards). These frameworks provide clear guidelines for recording transactions, valuing assets and liabilities, and recognizing revenue and expenses. Banks must adhere strictly to these standards to ensure uniformity and comparability in their financial reporting. Additionally, internal controls play a vital role in maintaining accuracy. These controls include segregation of duties, regular reconciliations, and periodic audits to identify and rectify errors or irregularities in the data.

Technology is another cornerstone of data accuracy in balance sheet submissions. Banks leverage advanced software and data analytics tools to automate data collection, processing, and validation. These systems reduce the risk of human error and enable real-time monitoring of financial data. For instance, automated reconciliation tools can flag inconsistencies between the general ledger and subsidiary records, prompting immediate corrective action. Furthermore, banks often use data warehouses to centralize financial information, ensuring that all departments work with the same accurate and up-to-date data.

Regular training and accountability measures are essential to reinforce the importance of data accuracy among bank employees. Staff involved in financial reporting must be well-versed in accounting principles, internal policies, and regulatory expectations. Banks should also establish clear accountability frameworks, where individuals or teams are responsible for specific data inputs and validations. This fosters a culture of precision and ownership, reducing the likelihood of errors. Periodic performance reviews and audits can further ensure that employees adhere to the highest standards of accuracy.

Finally, external audits and regulatory oversight provide an additional layer of assurance regarding data accuracy. Independent auditors review the bank’s financial statements to verify their accuracy and compliance with accounting standards. Regulatory bodies, such as central banks or financial authorities, scrutinize balance sheet submissions to ensure they reflect the bank’s true financial health. Banks must be prepared to provide detailed documentation and explanations to support their reported figures. By embracing these measures, banks can confidently submit balance sheets that are accurate, transparent, and reflective of their financial reality.

Who Bailed Out Whom? Taxpayers and Big Banks

You may want to see also

Explore related products

![]()

Audit Compliance: Balance sheets must be audited by external firms for transparency and accuracy

Banks are required to submit their balance sheets as part of their regulatory reporting obligations, ensuring transparency and maintaining public trust in the financial system. A critical aspect of this process is Audit Compliance, which mandates that balance sheets be audited by external firms to guarantee accuracy and reliability. This external audit is not merely a formality but a cornerstone of financial integrity, providing an independent assessment of a bank's financial position. External auditors, typically from reputable accounting firms, scrutinize the balance sheet to verify that assets, liabilities, and equity are accurately reported and comply with accounting standards such as GAAP (Generally Accepted Accounting Principles) or IFRS (International Financial Reporting Standards). Their role is to ensure that the financial statements reflect a true and fair view of the bank's financial health, free from material misstatements or errors.

The process of auditing a bank's balance sheet involves a comprehensive review of its financial records, transactions, and internal controls. Auditors examine the valuation of assets, such as loans, investments, and cash reserves, to confirm they are recorded at their fair market value. Similarly, liabilities, including customer deposits and borrowings, are assessed to ensure they are appropriately classified and valued. Equity accounts, such as retained earnings and shareholders' capital, are also verified for accuracy. Auditors may request supporting documentation, conduct interviews with bank personnel, and perform analytical procedures to identify discrepancies or irregularities. This meticulous process helps uncover potential issues like overstated assets, understated liabilities, or non-compliance with regulatory requirements.

External audits also play a vital role in enhancing transparency, which is essential for stakeholders such as investors, regulators, and customers. A clean audit opinion provides assurance that the bank's balance sheet is free from material misstatements and complies with applicable laws and regulations. Conversely, a qualified or adverse opinion can signal significant issues that require immediate attention. For instance, if auditors identify weaknesses in internal controls or non-compliance with accounting standards, they must report these findings, prompting the bank to take corrective actions. This transparency fosters trust and confidence in the bank's operations and financial stability.

To ensure audit compliance, banks must maintain robust internal processes and documentation. This includes keeping accurate records of all financial transactions, implementing strong internal controls to prevent fraud and errors, and adhering to accounting policies consistently. Banks often establish audit committees comprising independent directors to oversee the audit process and ensure its integrity. Additionally, banks must cooperate fully with external auditors, providing unrestricted access to financial records and addressing any concerns raised during the audit. Failure to comply with audit requirements can result in regulatory penalties, reputational damage, and loss of stakeholder confidence.

In summary, Audit Compliance is a critical component of how banks submit their balance sheets, ensuring transparency and accuracy through external audits. By engaging independent auditors to review their financial statements, banks demonstrate their commitment to financial integrity and regulatory compliance. This process not only safeguards the interests of stakeholders but also strengthens the overall stability and credibility of the financial system. As such, banks must prioritize audit compliance, maintaining rigorous standards in their financial reporting and internal controls.

International Banking Regulations: Standardization Attempts Examined

You may want to see also

Explore related products

![]()

Reporting Standards: Adherence to GAAP, IFRS, or other accounting standards is mandatory

Banks, as critical financial institutions, are subject to stringent regulatory requirements when submitting their balance sheets. Central to this process is adherence to established reporting standards, which ensure transparency, comparability, and accuracy in financial reporting. Reporting Standards: Adherence to GAAP, IFRS, or other accounting standards is mandatory for banks to maintain credibility and comply with legal obligations. Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS) are the two most widely recognized frameworks globally. Banks operating in the United States typically follow GAAP, as mandated by the Securities and Exchange Commission (SEC), while those with international operations often adopt IFRS to facilitate cross-border comparability. Regardless of the standard chosen, strict compliance is non-negotiable, as deviations can lead to regulatory penalties, loss of investor confidence, and legal consequences.

Adhering to GAAP or IFRS involves more than just applying rules; it requires a deep understanding of the principles underlying these standards. For instance, GAAP emphasizes consistency, conservatism, and materiality, ensuring that financial statements reflect a true and fair view of the bank’s financial position. Similarly, IFRS focuses on providing a globally consistent framework that enhances transparency and comparability across jurisdictions. Banks must ensure that their balance sheets are prepared in accordance with these principles, including proper classification of assets and liabilities, accurate valuation of financial instruments, and appropriate disclosure of contingent liabilities and off-balance-sheet items. Failure to comply with these standards can result in misstated financial statements, which may mislead stakeholders and undermine the bank’s integrity.

In addition to GAAP and IFRS, banks may also be required to comply with industry-specific regulations or local accounting standards, depending on their geographic location and regulatory environment. For example, banks in the European Union must adhere to the EU’s Accounting Directive, which aligns closely with IFRS but includes certain modifications tailored to the regional context. Similarly, banks in emerging markets may follow national accounting standards that are gradually converging with IFRS to promote global harmonization. Regardless of the specific standard, banks must ensure that their reporting practices align with the applicable framework, often involving rigorous internal controls, audits, and reviews by external auditors to validate compliance.

The process of adhering to reporting standards extends beyond the balance sheet itself to include comprehensive disclosures in the notes to the financial statements. These disclosures provide additional context and detail, such as accounting policies, significant judgments, and potential risks, enabling stakeholders to better understand the bank’s financial health. For example, banks must disclose their methodologies for impairment assessments, hedge accounting treatments, and fair value measurements, all of which are critical to interpreting the balance sheet. Transparency in these areas is essential, as it helps regulators, investors, and other stakeholders assess the bank’s risk management practices and financial stability.

Finally, banks must stay abreast of evolving reporting standards and regulatory changes, as both GAAP and IFRS are periodically updated to address emerging issues and improve financial reporting quality. For instance, recent changes have focused on areas such as lease accounting, revenue recognition, and financial instruments, requiring banks to adapt their systems and processes accordingly. Proactive compliance with these updates not only ensures ongoing adherence to mandatory standards but also demonstrates the bank’s commitment to best practices in financial reporting. In summary, adherence to GAAP, IFRS, or other accounting standards is a cornerstone of bank balance sheet submission, underpinning the reliability and integrity of financial information in the banking sector.

IBAN Numbers: Are They Used in the US Banking System?

You may want to see also

Frequently asked questions

Banks typically submit their balance sheets on a quarterly and annual basis, as required by regulatory authorities such as the central bank or financial oversight bodies.

Banks submit their balance sheets to regulatory authorities like the central bank, financial regulators, and in some cases, to shareholders and the public as part of their financial reporting obligations.

Banks use standardized formats prescribed by regulatory bodies, such as the International Financial Reporting Standards (IFRS) or Generally Accepted Accounting Principles (GAAP), to ensure consistency and comparability.

Most banks submit their balance sheets electronically through designated regulatory portals or platforms, though some jurisdictions may still accept physical submissions in specific cases.

Failure to submit a balance sheet on time can result in penalties, fines, or regulatory action, as timely submission is critical for maintaining transparency and ensuring compliance with financial regulations.