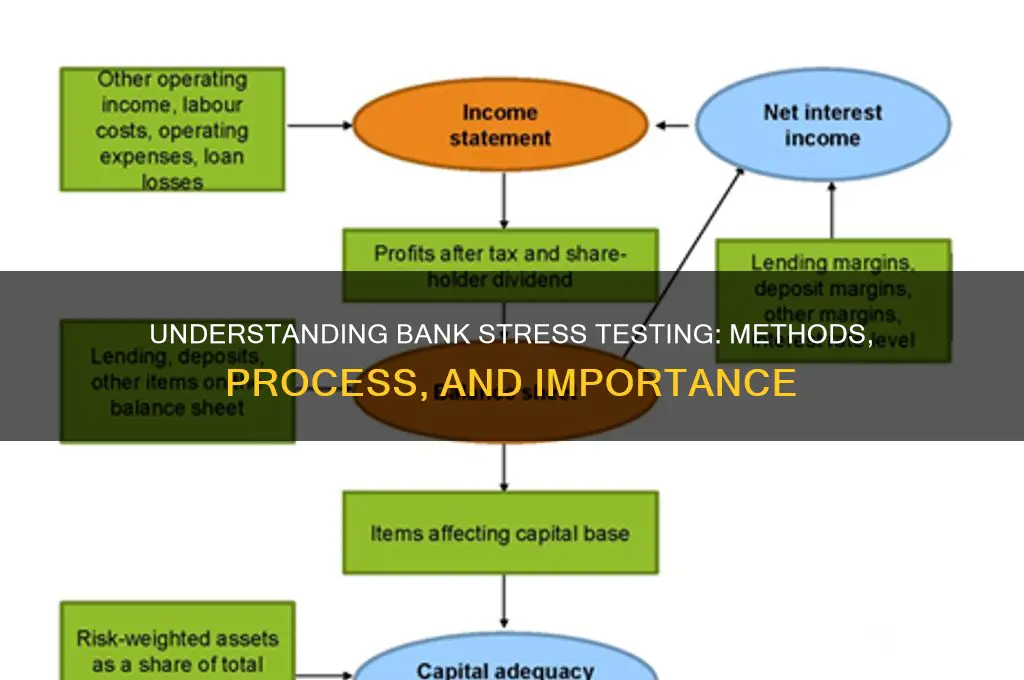

Stress testing in banks is a critical risk management tool used to assess a financial institution’s resilience to adverse economic scenarios. It involves simulating extreme but plausible events, such as severe recessions, market crashes, or geopolitical crises, to evaluate how a bank’s capital, liquidity, and overall financial health would fare under stress. Banks typically use quantitative models to project losses, revenue declines, and balance sheet impacts across various business lines. Regulatory bodies, like the Federal Reserve in the U.S. or the European Central Bank, often mandate stress tests to ensure banks maintain sufficient capital buffers to absorb shocks without destabilizing the financial system. Results from these tests inform strategic decisions, regulatory capital requirements, and contingency planning, helping banks and regulators mitigate systemic risks effectively.

Explore related products

What You'll Learn

- Scenario Design: Creating extreme but plausible scenarios to assess bank resilience under stress

- Data Collection: Gathering historical and current financial data for accurate stress test inputs

- Modeling Techniques: Using quantitative models to simulate impacts on bank portfolios and capital

- Regulatory Compliance: Ensuring stress tests meet standards set by financial authorities

- Results Analysis: Evaluating outcomes to identify risks and improve risk management strategies

![]()

Scenario Design: Creating extreme but plausible scenarios to assess bank resilience under stress

Scenario design is a critical component of stress testing in banks, as it involves crafting extreme but plausible scenarios to evaluate a bank's resilience under adverse conditions. The process begins with identifying key risk factors that could significantly impact the bank’s financial health, such as macroeconomic shocks, market volatility, geopolitical events, or systemic failures. These factors are then used to construct scenarios that simulate severe but realistic stress conditions. For instance, a scenario might include a deep recession, a sharp rise in unemployment, a collapse in asset prices, or a sudden increase in interest rates. The goal is to ensure that the scenarios are challenging enough to test the bank’s capital adequacy, liquidity, and overall stability without being overly hypothetical or impossible.

To create these scenarios, banks often collaborate with regulatory bodies, economists, and risk management experts to ensure they align with historical data, current market trends, and potential future risks. Historical precedents, such as the 2008 financial crisis or the COVID-19 pandemic, serve as benchmarks for designing stress scenarios. However, scenarios are not merely replications of past events; they are forward-looking and incorporate emerging risks, such as cybersecurity threats, climate change, or technological disruptions. Each scenario must be detailed, specifying variables like GDP growth, inflation rates, unemployment levels, and asset price movements over a defined time horizon, typically one to three years.

Once the scenarios are designed, they are quantified to assess their impact on the bank’s balance sheet, income statement, and key risk metrics. This involves modeling how the bank’s portfolio of loans, investments, and other assets would perform under stress. For example, a severe recession scenario might lead to higher loan defaults, reduced customer deposits, and lower revenue from fee-based services. The bank’s risk models are then used to calculate potential losses, capital erosion, and liquidity shortfalls under each scenario. This quantification ensures that the stress test provides actionable insights into the bank’s vulnerabilities and areas for improvement.

Scenario design also requires a degree of customization to reflect the bank’s unique risk profile, business model, and geographic exposure. A global bank with diverse operations may face different risks compared to a regional bank focused on retail lending. Therefore, scenarios must be tailored to account for specific risk concentrations, such as exposure to particular industries, regions, or asset classes. For instance, a bank heavily reliant on commercial real estate lending might face greater stress under a scenario involving a property market crash.

Finally, scenario design must balance severity with plausibility to ensure the stress test remains credible and useful. Scenarios that are too mild may fail to identify weaknesses, while those that are overly extreme may lead to unnecessary panic or regulatory overreaction. Regulators often provide guidelines or benchmarks for scenario design, such as the adverse and severely adverse scenarios used in the Federal Reserve’s Comprehensive Capital Analysis and Review (CCAR). Banks must also document their scenario design process transparently to demonstrate its robustness and adherence to regulatory standards. Effective scenario design ultimately enables banks to proactively manage risks, strengthen their resilience, and maintain financial stability even in the face of extreme stress.

Capital City Bank Review: Rating Its Services, Fees, and Customer Experience

You may want to see also

Explore related products

![]()

Data Collection: Gathering historical and current financial data for accurate stress test inputs

Data collection is a critical first step in conducting stress tests for banks, as the accuracy and reliability of the test results heavily depend on the quality of the input data. The process begins with gathering historical financial data, which provides a baseline for understanding the bank’s performance under various economic conditions. This includes historical balance sheets, income statements, and cash flow statements, typically spanning the past 5 to 10 years. Historical data helps identify trends, vulnerabilities, and resilience patterns in the bank’s financial health. For instance, loan default rates during past recessions or revenue fluctuations during economic downturns are essential inputs for stress scenarios.

In addition to historical data, current financial data is equally vital to ensure the stress test reflects the bank’s present condition. This involves collecting up-to-date information on the bank’s assets, liabilities, capital structure, and off-balance-sheet exposures. Current data includes loan portfolios, deposit levels, market valuations of securities, and derivative positions. Banks often use internal systems, such as core banking platforms and risk management tools, to extract this data. External sources, like regulatory filings and market data providers, may also be utilized to validate and supplement internal records. Timeliness is key, as even minor delays in data collection can lead to outdated inputs, compromising the stress test’s relevance.

Another critical aspect of data collection is ensuring granularity and consistency. Stress tests require detailed data at the product, customer, and geographic levels to accurately model risks. For example, loan data should be segmented by type (e.g., mortgages, corporate loans), credit quality, and maturity. Similarly, deposit data should distinguish between retail and wholesale deposits and their stability. Consistency in data formats and definitions across time periods and business units is essential to avoid discrepancies. Banks often establish data governance frameworks to standardize data collection processes and ensure compliance with regulatory requirements.

External economic and market data also play a significant role in stress testing. Banks must gather macroeconomic indicators such as GDP growth, unemployment rates, interest rates, and inflation projections from reputable sources like central banks, statistical agencies, and financial institutions. Market data, including equity prices, bond yields, and foreign exchange rates, are used to simulate adverse scenarios. This external data is combined with internal financial data to create realistic stress scenarios that reflect potential economic shocks. Collaboration with industry peers and participation in regulatory data-sharing initiatives can enhance the robustness of this data.

Finally, data validation and quality assurance are indispensable steps in the data collection process. Banks must verify the accuracy, completeness, and integrity of the collected data to ensure it is fit for stress testing purposes. This involves cross-checking data against multiple sources, identifying and rectifying anomalies, and addressing missing or inconsistent values. Advanced analytics and data validation tools are often employed to automate these checks. Regular audits and reviews of the data collection process help maintain high standards and align with regulatory expectations. Accurate and reliable data inputs are the foundation of credible stress test results, enabling banks to assess their resilience and make informed risk management decisions.

Life Insurance as Loan Collateral: What Banks Accept

You may want to see also

Explore related products

![]()

Modeling Techniques: Using quantitative models to simulate impacts on bank portfolios and capital

Stress testing in banks is a critical process that evaluates a bank's resilience to adverse economic scenarios. Within this process, modeling techniques play a pivotal role in quantifying the potential impact of stress scenarios on bank portfolios and capital adequacy. These techniques leverage quantitative models to simulate how various risk factors, such as economic downturns, market volatility, or credit defaults, could affect a bank's financial health. By doing so, banks can identify vulnerabilities, ensure compliance with regulatory requirements, and make informed strategic decisions.

One of the primary modeling techniques used in stress testing is scenario analysis, where predefined adverse scenarios are applied to a bank's portfolio. These scenarios are often based on historical events or hypothetical shocks, such as a severe recession, a sharp rise in interest rates, or a collapse in asset prices. Quantitative models, such as those based on Monte Carlo simulations or macroeconomic models, are employed to project the bank's financial performance under these scenarios. For instance, a credit risk model might estimate loan defaults and losses under stressed economic conditions, while a market risk model could assess the impact of asset price declines on trading portfolios. These models incorporate variables like GDP growth, unemployment rates, and interest rates to provide a comprehensive view of potential outcomes.

Another key technique is sensitivity analysis, which measures how changes in specific risk factors affect the bank's portfolio and capital. This approach helps banks understand their exposure to individual risks and identify areas of concentration. For example, a bank might analyze the impact of a 100-basis-point increase in interest rates on its net interest margin or the effect of a 20% decline in property prices on its mortgage portfolio. Sensitivity analysis is often complemented by value-at-risk (VaR) models, which quantify the maximum potential loss within a given confidence interval under stressed conditions. These models are particularly useful for assessing market and liquidity risks.

Dynamic stochastic general equilibrium (DSGE) models are also employed to simulate the interplay between macroeconomic variables and bank performance. Unlike static models, DSGE models capture the feedback loops between the economy and the financial system, providing a more realistic representation of stress scenarios. For instance, a DSGE model can simulate how a banking crisis might deepen a recession by restricting credit supply, which in turn exacerbates loan defaults and capital erosion. This holistic approach allows banks to assess systemic risks and their broader implications.

Finally, reverse stress testing is a modeling technique that identifies the extreme scenarios under which a bank would fail. Unlike traditional stress tests, which apply predefined scenarios, reverse stress testing starts with the failure outcome and works backward to determine the conditions that would cause it. This approach helps banks understand their "breaking point" and take proactive measures to strengthen their resilience. Quantitative models in reverse stress testing often involve iterative simulations and stress thresholds to identify critical risk drivers.

In conclusion, modeling techniques are indispensable in stress testing as they provide a rigorous, data-driven framework to assess the impact of adverse scenarios on bank portfolios and capital. By employing scenario analysis, sensitivity analysis, DSGE models, and reverse stress testing, banks can quantify risks, ensure compliance, and enhance their ability to withstand financial shocks. These techniques not only support regulatory requirements but also enable banks to make strategic decisions that safeguard their long-term stability.

Is Coldwell Banker Operating with a Lean Staff? Insights and Analysis

You may want to see also

Explore related products

![]()

Regulatory Compliance: Ensuring stress tests meet standards set by financial authorities

Stress testing in banks is a critical process designed to assess a financial institution's resilience to adverse economic scenarios. Ensuring that these stress tests meet the standards set by financial authorities is paramount for regulatory compliance. Financial regulators, such as the Federal Reserve in the United States, the European Central Bank (ECB), and the Bank of England, have established stringent guidelines to ensure that stress tests are robust, consistent, and reflective of potential risks. Compliance with these standards is not only a legal requirement but also a cornerstone of maintaining financial stability and public confidence in the banking system.

To achieve regulatory compliance, banks must adhere to specific methodologies and scenarios prescribed by financial authorities. For instance, the Federal Reserve’s Comprehensive Capital Analysis and Review (CCAR) and the ECB’s Stress Test Framework outline detailed requirements for scenario design, risk modeling, and capital adequacy assessments. These frameworks mandate the use of both macroeconomic and institution-specific data to simulate severe but plausible stress scenarios, such as economic recessions, market crashes, or geopolitical crises. Banks are required to demonstrate how their balance sheets, income statements, and capital positions would fare under such conditions, ensuring that they remain solvent and operational.

Transparency and documentation are critical components of regulatory compliance in stress testing. Banks must provide clear and detailed reports on their methodologies, assumptions, and results to financial authorities. This includes disclosing the models used, data sources, and any limitations in their stress testing frameworks. Regulators often conduct independent reviews to validate the accuracy and reliability of these tests, ensuring that banks are not underestimating risks or overstating their resilience. Failure to meet transparency standards can result in penalties, reputational damage, and increased regulatory scrutiny.

Another key aspect of regulatory compliance is the integration of stress test results into risk management and strategic decision-making processes. Financial authorities require banks to use stress test outcomes to inform their capital planning, risk appetite frameworks, and contingency plans. For example, if a stress test reveals a potential capital shortfall under adverse conditions, the bank must take proactive measures, such as raising additional capital, reducing risk exposure, or adjusting its business strategy. Regulators monitor these actions to ensure that banks are not only compliant on paper but also actively enhancing their resilience.

Finally, staying abreast of evolving regulatory requirements is essential for maintaining compliance in stress testing. Financial authorities frequently update their guidelines to address emerging risks, such as climate change, cybersecurity threats, or technological disruptions. Banks must invest in continuous training, technology, and expertise to adapt their stress testing frameworks accordingly. Engaging with regulators through consultations and feedback mechanisms can also help banks better understand expectations and align their practices with regulatory standards. By prioritizing regulatory compliance, banks not only fulfill their legal obligations but also strengthen their ability to withstand shocks and protect stakeholders’ interests.

Does Coldwell Banker Offer In-House Mortgage Services? Find Out Here

You may want to see also

Explore related products

![]()

Results Analysis: Evaluating outcomes to identify risks and improve risk management strategies

Stress testing in banks involves subjecting financial institutions to hypothetical adverse scenarios to assess their resilience and identify potential risks. Once the stress tests are conducted, the Results Analysis phase becomes critical for evaluating outcomes, identifying vulnerabilities, and enhancing risk management strategies. This phase requires a systematic approach to interpret data, draw actionable insights, and implement improvements. Below is a detailed breakdown of how results analysis is performed in the context of bank stress testing.

The first step in results analysis is quantifying the impact of stress scenarios on key financial metrics such as capital adequacy ratios, liquidity positions, and profitability. Banks compare these metrics against regulatory thresholds and internal risk appetite frameworks to determine if they remain within acceptable limits under stress. For instance, a severe economic downturn scenario might reveal a significant decline in capital ratios, indicating a potential breach of regulatory requirements. By quantifying these impacts, banks can prioritize areas that require immediate attention and allocate resources effectively.

Next, identifying risk concentrations is essential to understanding where vulnerabilities lie. Stress test results often highlight specific portfolios, asset classes, or geographic regions that are disproportionately affected by adverse scenarios. For example, a bank heavily exposed to commercial real estate loans might face higher credit losses during a property market crash. Analyzing these concentrations allows banks to diversify their portfolios, reduce overexposure, and implement targeted risk mitigation strategies. Tools such as sensitivity analysis and scenario comparisons are commonly used to pinpoint these concentrations.

A critical aspect of results analysis is benchmarking performance against peers and historical data. Banks compare their stress test outcomes with those of similar institutions to assess their relative resilience. This benchmarking helps identify gaps in risk management practices and highlights areas where the bank may be underperforming. Additionally, comparing current results with historical stress test data provides insights into trends and improvements over time. Such analysis fosters a culture of continuous improvement and ensures that risk management strategies remain robust in evolving market conditions.

Finally, developing actionable recommendations is the ultimate goal of results analysis. Based on the insights gained, banks must formulate strategies to address identified risks. This could include enhancing capital buffers, improving liquidity management, revising credit policies, or investing in risk modeling capabilities. Recommendations should be specific, measurable, and aligned with the bank’s strategic objectives. Regular monitoring and reporting mechanisms are also established to track the implementation of these strategies and ensure their effectiveness.

In conclusion, results analysis in bank stress testing is a multifaceted process that involves quantifying impacts, identifying risk concentrations, benchmarking performance, and developing actionable recommendations. By rigorously evaluating stress test outcomes, banks can strengthen their risk management frameworks, enhance financial stability, and better prepare for future challenges. This proactive approach not only safeguards the institution but also contributes to the overall resilience of the financial system.

The Mortgage Marketplace: Banks and Loan Buyers

You may want to see also

Frequently asked questions

Stress testing in banks is a risk management tool used to evaluate a bank’s financial resilience under extreme but plausible scenarios, such as economic downturns, market crashes, or geopolitical crises. It is important because it helps banks identify potential vulnerabilities, ensure sufficient capital and liquidity buffers, and meet regulatory requirements to maintain financial stability.

Stress testing is conducted by simulating adverse scenarios and assessing their impact on a bank’s balance sheet, income statement, and capital adequacy. Banks use quantitative models, historical data, and expert judgment to project losses, revenues, and capital levels under stress. Regulatory bodies, such as the Federal Reserve or ECB, often mandate specific scenarios and methodologies for consistency and comparability.

The key components include scenario design (adverse and severely adverse conditions), data collection and validation, model development and calibration, impact assessment (e.g., credit, market, liquidity risks), and reporting. Banks also incorporate governance processes to ensure transparency, accountability, and alignment with regulatory expectations.