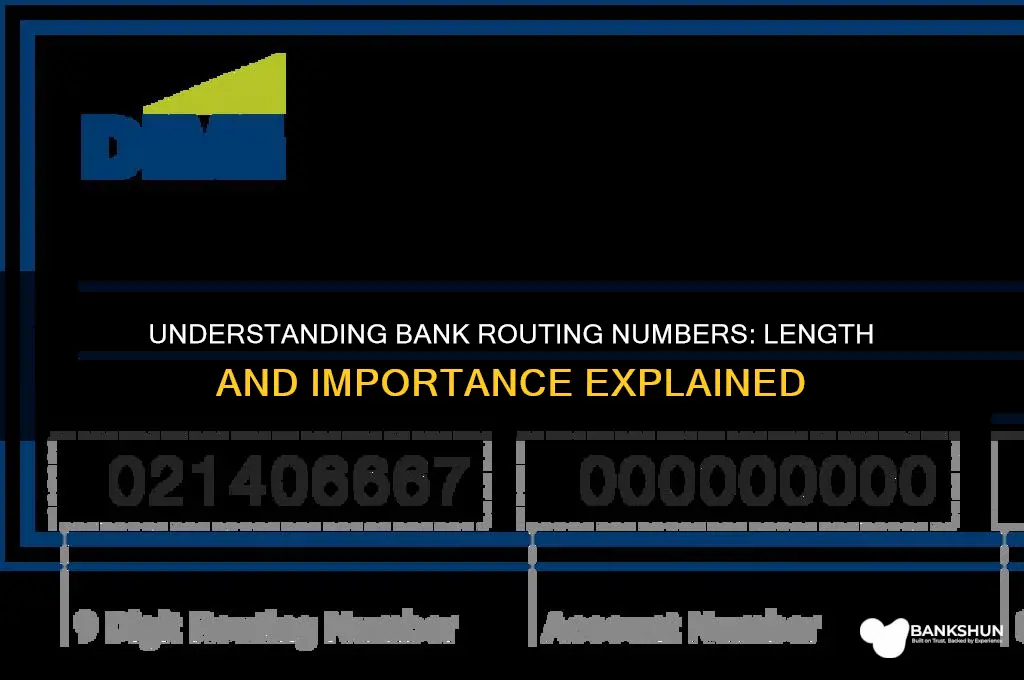

Routing numbers, also known as ABA routing transit numbers, are nine-digit codes used in the United States to identify financial institutions in transactions such as direct deposits, wire transfers, and automatic bill payments. These numbers are essential for ensuring that funds are accurately directed to the correct bank or credit union. The length of a routing number is consistently nine digits, with no variations, making it a standardized identifier across all U.S. banking institutions. Understanding the structure and purpose of routing numbers is crucial for anyone involved in financial transactions, as it helps prevent errors and ensures the smooth processing of payments.

| Characteristics | Values |

|---|---|

| Length | 9 digits |

| Purpose | Identifies the financial institution in the United States |

| Format | Numeric (0-9) |

| Uniqueness | Unique to each financial institution |

| Usage | Used for domestic wire transfers, direct deposits, and automatic bill payments |

| Also Known As | ABA routing number, routing transit number (RTN) |

| Regulation | Assigned and regulated by the American Bankers Association (ABA) |

| Example | 021000021 (Wells Fargo Bank, N.A.) |

| Validation | Checksum validation is used to ensure accuracy |

| International Equivalent | Not applicable (used only in the United States) |

Explore related products

What You'll Learn

![]()

Standard Routing Number Length

A routing number, also known as an ABA routing transit number (RTN), is a nine-digit code used in the United States to identify financial institutions, such as banks and credit unions. The standard routing number length is a crucial aspect of this identification system, ensuring seamless and accurate transactions between banks. This standardized length plays a vital role in facilitating various financial operations, including direct deposits, wire transfers, and automatic bill payments.

The standard routing number length consists of exactly nine digits, with no exceptions or variations. This uniform length is essential for maintaining consistency and compatibility across the entire banking system. Each digit within the routing number serves a specific purpose, contributing to the overall identification and routing process. The first four digits represent the Federal Reserve routing symbol, which identifies the Federal Reserve Bank district and the type of financial institution. The next four digits denote the ABA institution identifier, uniquely assigned to each bank or credit union. The final digit is a checksum, calculated using a specific algorithm to ensure the accuracy and validity of the entire routing number.

When dealing with bank transactions, it is essential to understand the significance of the standard routing number length. A routing number with an incorrect length or format can lead to transaction failures, delays, or even financial losses. Financial institutions and consumers alike must verify the accuracy of routing numbers to avoid such issues. This verification process typically involves cross-referencing the routing number with official bank records or using online validation tools provided by reputable sources. By adhering to the standard routing number length, banks can ensure that their transactions are processed efficiently and securely.

In addition to its role in transaction processing, the standard routing number length also facilitates bank account verification and fraud prevention. Financial institutions use routing numbers to confirm the authenticity of bank accounts and detect potential fraudulent activities. By analyzing the routing number's structure and length, banks can identify discrepancies or anomalies that may indicate unauthorized access or malicious intent. Furthermore, regulatory bodies and government agencies rely on the standard routing number length to monitor and regulate financial transactions, ensuring compliance with applicable laws and regulations.

It is worth noting that while the standard routing number length remains consistent across the United States, some international transactions may involve different identification codes or formats. For instance, international wire transfers often require a SWIFT code or BIC (Bank Identifier Code), which serves a similar purpose to routing numbers but follows a distinct structure. However, within the US banking system, the nine-digit standard routing number length remains the universal standard. As such, individuals and businesses conducting financial transactions within the United States should always ensure that they are using the correct routing number length to avoid complications and ensure the smooth processing of their transactions.

Does Capital One Bank Accept Foreign Currency? A Comprehensive Guide

You may want to see also

Explore related products

![]()

Variations in Routing Number Digits

Routing numbers are a critical component of the banking system, serving as unique identifiers for financial institutions during transactions. While the standard length of a routing number is 9 digits in the United States, variations can exist based on the type of transaction, the financial institution, and the country in question. Understanding these variations is essential for ensuring accurate and efficient processing of payments, transfers, and other banking operations.

In the United States, the 9-digit routing number is the most common format, comprising four components: the first four digits represent the Federal Reserve Routing Symbol, the next four digits identify the American Bankers Association (ABA) institution, and the last digit is a checksum to validate the number. However, certain specialized transactions, such as those involving government agencies or international payments, may use abbreviated or modified routing numbers. For instance, some government transactions use an 8-digit routing number, omitting the checksum digit, while still maintaining compatibility with the standard system.

Internationally, routing number equivalents vary significantly in length and structure. In Canada, for example, routing numbers are 9 digits long, similar to the U.S., but they are formatted differently and are often referred to as "transit numbers." In the United Kingdom, the equivalent identifier is the Sort Code, which consists of 6 digits divided into three pairs. Meanwhile, countries like India use an 11-digit International Financial Services Code (IFSC) for identifying bank branches, highlighting the diversity in global banking standards.

Another variation arises in the context of wire transfers and Automated Clearing House (ACH) transactions. While both rely on routing numbers, ACH transactions typically use the standard 9-digit format, whereas wire transfers may require additional codes or a slightly different structure depending on the bank and the destination country. This distinction underscores the importance of verifying the correct routing number format for the specific type of transaction being conducted.

Lastly, it’s worth noting that some financial institutions may have multiple routing numbers based on their geographic location or the services they offer. For example, a bank with branches in different Federal Reserve districts may have distinct routing numbers for each region. Similarly, credit unions often use unique routing numbers that differ from those of traditional banks. These variations emphasize the need for customers to confirm the appropriate routing number with their bank to avoid errors in transactions.

In summary, while the standard U.S. routing number is 9 digits, variations exist based on transaction type, geographic location, and international banking systems. Understanding these differences ensures smooth processing of financial transactions and highlights the complexity of global banking infrastructure. Always verify the correct routing number format for your specific needs to maintain accuracy and efficiency in your banking operations.

Egg Inc: Best Time to Prestige Your Farm

You may want to see also

Explore related products

![]()

International vs. Domestic Routing Numbers

Routing numbers are essential identifiers used in banking systems to ensure that financial transactions are directed to the correct institution. When comparing International vs. Domestic Routing Numbers, it’s crucial to understand their structure, purpose, and length. Domestically, in the United States, routing numbers are 9 digits long and are used for transactions like direct deposits, wire transfers, and ACH payments within the country. These numbers are standardized by the American Bankers Association (ABA) and are unique to each financial institution or bank branch. They are also known as ABA routing numbers or RTNs (Routing Transit Numbers).

In contrast, International Routing Numbers operate differently and are not standardized to a specific length like their domestic counterparts. International transactions rely on codes such as the SWIFT (Society for Worldwide Interbank Financial Telecommunication) code, which is 8 to 11 characters long, including letters and numbers. SWIFT codes identify banks and financial institutions globally and are essential for cross-border wire transfers. Unlike domestic routing numbers, SWIFT codes are not used for internal transactions within a single country but are specifically designed for international financial communication.

Another key difference between International vs. Domestic Routing Numbers is their application. Domestic routing numbers are used exclusively within a country’s banking system, ensuring funds are routed correctly within national borders. For example, in the U.S., a routing number is required for setting up direct deposits or transferring funds between accounts in different banks. Internationally, however, SWIFT codes and other identifiers like IBAN (International Bank Account Number) are used to facilitate transactions across borders, ensuring accuracy and security in a global context.

The length and format of these numbers also reflect their purpose. Domestic routing numbers are shorter and more straightforward because they operate within a single, standardized system. International identifiers, on the other hand, are longer and more complex to accommodate the diversity of global banking systems and to prevent errors in cross-border transactions. For instance, an IBAN can be up to 34 characters long, depending on the country, and includes country codes, checksum digits, and bank account numbers.

In summary, when discussing International vs. Domestic Routing Numbers, the primary distinctions lie in their length, format, and use. Domestic routing numbers are 9 digits long and are used for transactions within a single country, while international identifiers like SWIFT codes and IBANs are longer and more complex, designed to facilitate secure and accurate cross-border transactions. Understanding these differences is crucial for anyone involved in both domestic and international banking activities.

Finance, Banking, and Technology: The Convergence Shaping Modern Economy

You may want to see also

Explore related products

![]()

ACH vs. Wire Transfer Routing Numbers

Routing numbers are essential in the banking system, serving as unique identifiers for financial institutions during transactions. When it comes to ACH (Automated Clearing House) vs. Wire Transfer Routing Numbers, understanding their differences is crucial for accurate and efficient transactions. Both types of transfers rely on routing numbers, but they serve distinct purposes and operate under different systems.

ACH Routing Numbers are specifically used for ACH transactions, which include direct deposits, bill payments, and electronic funds transfers (EFTs). These routing numbers are typically 9 digits long, matching the standard length of a bank's routing number. ACH transfers are processed in batches, making them cost-effective for routine, non-urgent transactions. The routing number in this context ensures that funds are directed to the correct bank and account. It’s important to note that ACH routing numbers are often the same as the bank’s general routing number found on checks or deposit slips.

On the other hand, Wire Transfer Routing Numbers are used for wire transfers, which are real-time, high-priority transactions often used for large or time-sensitive payments. Wire transfers require a different set of routing information, including a SWIFT code for international wires or an ABA routing number for domestic wires. While domestic wire transfers still use a 9-digit routing number, international wires rely on the SWIFT code, which is 8 to 11 characters long and includes letters and numbers. This distinction is critical, as using the wrong routing information can delay or fail the transfer.

A key difference between ACH and wire transfer routing numbers lies in their application and processing speed. ACH routing numbers are used for transactions that are processed in batches over 1–2 business days, whereas wire transfer routing numbers facilitate immediate transfers, often completed within hours or even minutes. This makes wire transfers ideal for urgent payments, despite typically incurring higher fees compared to ACH transfers.

When initiating a transaction, it’s essential to verify whether you need an ACH or wire transfer routing number. For ACH transactions, the standard 9-digit routing number from your bank will suffice. For wire transfers, you’ll need to obtain the specific wire routing information, which may include additional details like the recipient’s bank name, account number, and, for international wires, the SWIFT code. Always double-check the routing details to avoid errors, as mistakes can lead to delays or misdirected funds.

In summary, while both ACH and wire transfer routing numbers are 9 digits long for domestic transactions, their usage and context differ significantly. ACH routing numbers are for batch-processed, cost-effective transfers, while wire transfer routing numbers are for real-time, high-priority payments. Understanding these differences ensures smooth and accurate financial transactions, whether you’re sending money domestically or internationally.

US Banks and Canadian Currency: Who Accepts What?

You may want to see also

Explore related products

![]()

Historical Changes in Routing Number Format

Routing numbers, also known as ABA (American Bankers Association) numbers, have undergone several changes since their inception in 1910. Initially, routing numbers were designed as a 7- or 8-digit code to identify the financial institution responsible for processing a transaction. This early format was sufficient for the limited banking network of the time, where transactions were primarily paper-based and processed manually. The 7- or 8-digit structure allowed for a clear distinction between banks, ensuring that funds were directed to the correct institution.

In the mid-20th century, as banking systems expanded and transaction volumes increased, the need for a more standardized and scalable routing number format became apparent. By the 1960s, the 9-digit routing number format was introduced to accommodate the growing number of banks and credit unions. This change was driven by the adoption of automated clearinghouses and electronic processing systems, which required a more precise and uniform identification method. The 9-digit format included a checksum digit, enhancing accuracy and reducing errors in transaction routing.

The transition to the 9-digit routing number was a significant milestone, as it standardized the format across the United States banking system. The first four digits of the new format represented the Federal Reserve routing symbol, the next four identified the specific bank or institution, and the final digit served as the checksum. This structure not only improved efficiency but also laid the groundwork for the integration of electronic banking systems, which would become prevalent in the following decades.

In the late 20th and early 21st centuries, routing numbers remained largely unchanged in terms of length, but their application expanded with the rise of digital banking. The 9-digit format was seamlessly integrated into online banking platforms, direct deposits, wire transfers, and automated bill payments. Despite advancements in technology, the core structure of routing numbers has proven resilient, demonstrating its effectiveness in identifying financial institutions accurately.

While the length of routing numbers has remained consistent at 9 digits since the 1960s, there have been discussions and proposals for potential future changes. With the advent of global banking networks and cross-border transactions, some experts have suggested the need for a more universal identification system. However, as of now, the 9-digit routing number remains the standard in the United States, reflecting its historical evolution and continued relevance in modern banking operations. Understanding these historical changes highlights the adaptability and enduring importance of routing numbers in the financial ecosystem.

Can You Use Bank of England Notes in Scotland?

You may want to see also

Frequently asked questions

Routing numbers for banks in the United States are 9 digits long.

Yes, all banks in the United States use a standardized 9-digit routing number format.

No, routing numbers are 9 digits long and identify the bank, while account numbers vary in length and identify the specific account.

No, routing numbers in the U.S. are always exactly 9 digits long as per the American Bankers Association (ABA) standards.

![Lucky Number Slevin - BLURAY [Blu-ray]](https://m.media-amazon.com/images/I/81pSGbISaxL._AC_UY218_.jpg)