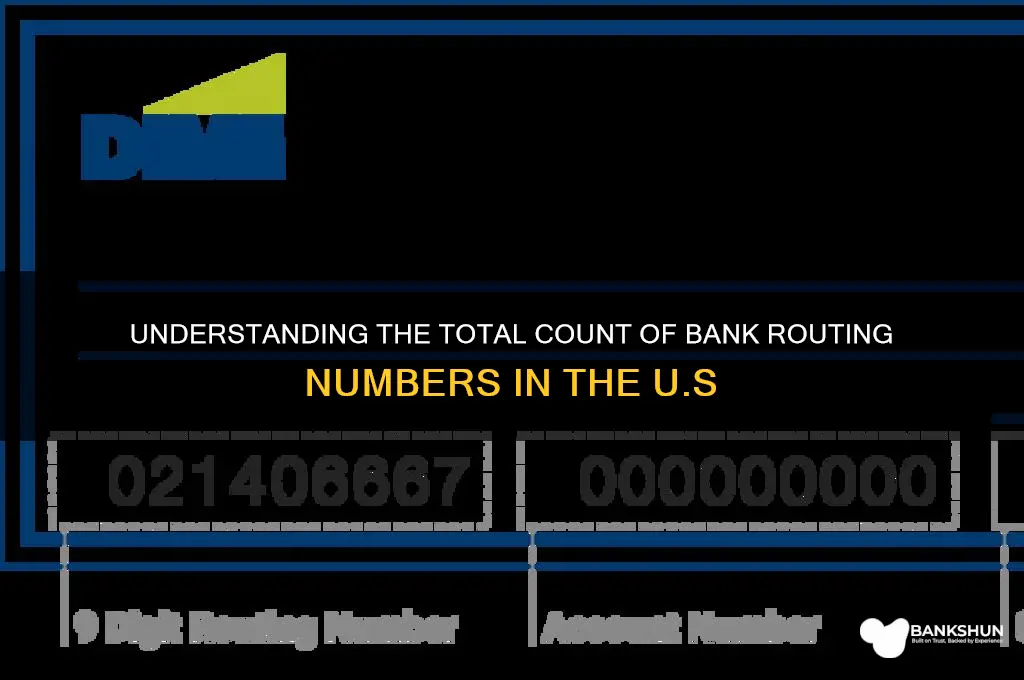

Bank routing numbers, also known as ABA routing transit numbers, are nine-digit codes used in the United States to identify financial institutions in transactions such as direct deposits, wire transfers, and automatic bill payments. These numbers are essential for ensuring that funds are directed to the correct bank and account. As of the latest data, there are approximately 26,000 unique bank routing numbers in use across the United States, each corresponding to a specific bank or credit union. The number of routing numbers can fluctuate due to bank mergers, acquisitions, or the establishment of new financial institutions, making it a dynamic aspect of the banking system. Understanding the scope and distribution of these numbers is crucial for both consumers and businesses to navigate financial transactions efficiently.

| Characteristics | Values |

|---|---|

| Total Number of Routing Numbers | Approximately 26,000 |

| Type of Routing Numbers | ABA Routing Transit Numbers (RTNs) |

| Purpose | Used for identifying banks and financial institutions in the U.S. for transactions like ACH transfers, wire transfers, and check processing |

| Format | 9-digit numeric code |

| Assignment | Assigned by the American Bankers Association (ABA) |

| Uniqueness | Each routing number is unique to a specific bank or financial institution |

| Geographic Distribution | Routing numbers are not geographically restricted; a bank can have multiple routing numbers for different branches or services |

| Updates | Routing numbers can change due to bank mergers, acquisitions, or operational adjustments |

| Verification | Can be verified through the ABA's routing number registry or online banking platforms |

| International Use | Not used internationally; SWIFT codes are used for international transactions |

| Last Updated | Data as of October 2023 (latest available information) |

Explore related products

What You'll Learn

- Total U.S. Routing Numbers: Approximately 26,000 active ABA routing numbers exist in the United States

- International Variations: Other countries use different systems, like BIC/SWIFT codes, instead of routing numbers

- ACH vs. Wire Transfers: Routing numbers differ for ACH transactions and wire transfers within the same bank

- Credit Unions: Credit unions also have unique routing numbers distinct from traditional banks

- Routing Number Structure: A 9-digit code identifying financial institutions for transactions

![]()

Total U.S. Routing Numbers: Approximately 26,000 active ABA routing numbers exist in the United States

In the United States, the total number of active bank routing numbers, also known as ABA routing numbers, is approximately 26,000. These unique nine-digit codes are essential for identifying financial institutions during transactions, such as direct deposits, wire transfers, and automatic bill payments. The American Bankers Association (ABA) originally developed this system to streamline the processing of paper checks, but it has since become a cornerstone of electronic banking as well. Each routing number corresponds to a specific bank or credit union, ensuring that funds are directed to the correct institution.

The existence of roughly 26,000 active ABA routing numbers highlights the vastness and diversity of the U.S. banking system. These numbers are not randomly assigned; they follow a structured format that includes a Federal Reserve prefix, an ABA institution identifier, and a check digit for accuracy. Financial institutions, including commercial banks, credit unions, and thrift institutions, are assigned these numbers by the ABA or the Federal Reserve. The total count reflects the dynamic nature of the banking industry, with new institutions entering the market and others merging or ceasing operations over time.

Understanding the scope of approximately 26,000 active routing numbers is crucial for consumers and businesses alike. When setting up direct deposits, transferring funds, or verifying account information, knowing the correct routing number ensures transactions are processed efficiently and without errors. While the total number may seem overwhelming, routing numbers are typically easy to locate on checks, bank statements, or through online banking portals. This accessibility ensures that individuals and organizations can navigate the financial system with confidence.

The maintenance of 26,000 active ABA routing numbers is a collaborative effort involving the ABA, the Federal Reserve, and individual financial institutions. As banks merge, rebrand, or close, routing numbers may be retired or reassigned, keeping the system up-to-date. This ongoing management is vital to prevent confusion and ensure the integrity of financial transactions. For example, if a bank acquires another institution, the acquiring bank may inherit the routing numbers of the acquired bank or consolidate them under a single number.

In conclusion, the fact that there are approximately 26,000 active ABA routing numbers in the United States underscores the complexity and efficiency of the nation’s banking infrastructure. These numbers serve as a critical tool for identifying financial institutions and facilitating seamless transactions. Whether for personal or business use, understanding and correctly utilizing routing numbers is essential for participating in the modern financial ecosystem. As the banking industry continues to evolve, the system of routing numbers will remain a fundamental component of financial operations.

Bank Records: What You Need to Disclose

You may want to see also

Explore related products

![]()

International Variations: Other countries use different systems, like BIC/SWIFT codes, instead of routing numbers

While the United States relies on routing numbers to identify banks and facilitate domestic transactions, other countries employ distinct systems for similar purposes. One of the most widely recognized alternatives is the Bank Identifier Code (BIC) or SWIFT code, used predominantly in international banking. SWIFT (Society for Worldwide Interbank Financial Telecommunication) codes are a unique combination of letters and numbers (8 to 11 characters) that identify a specific bank or financial institution globally. Unlike routing numbers, which are primarily domestic, SWIFT codes are essential for cross-border transactions, ensuring funds are directed to the correct bank and branch. For instance, a SWIFT code like "DEUTDEFF" identifies Deutsche Bank in Germany, with each segment providing specific information about the bank's country, location, and branch.

In addition to SWIFT codes, some countries use IBAN (International Bank Account Number) systems, which incorporate bank and account details into a single standardized format. IBANs are widely used in Europe and other regions to streamline international payments and reduce errors. For example, a UK IBAN might look like "GB82 WEST 1234 5698 7654 32", where "GB" denotes the country, "82" is a checksum, and the following characters identify the bank and account. While IBANs are not bank identifiers themselves, they often include codes that reference the bank, making them a critical component of international banking systems.

Another variation is the Sort Code system used in the United Kingdom. Sort codes are 6-digit numbers that identify both the bank and the specific branch where an account is held. For instance, a sort code like "12-34-56" would correspond to a particular branch of a UK bank. While similar in function to routing numbers, sort codes are not used for international transactions, where SWIFT codes or IBANs take precedence. This highlights the importance of understanding the specific system used in each country for accurate financial transactions.

In Canada, banks use Institution Numbers and Transit Numbers instead of routing numbers. The Institution Number (3 digits) identifies the bank, while the Transit Number (5 digits) specifies the branch. For example, "001" might represent the Royal Bank of Canada, with "00040" identifying a specific branch. These numbers are used domestically, and for international transactions, Canadian banks rely on SWIFT codes. This dual-system approach ensures efficiency in both local and global banking operations.

In Australia, the BSB (Bank-State-Branch) code is the primary identifier for banks and branches. A BSB code consists of 6 digits (e.g., "062-000") and is used for domestic transactions. For international payments, Australian banks also utilize SWIFT codes. Similarly, India employs IFSC (Indian Financial System Code), an 11-character alphanumeric code that identifies banks and branches for electronic transfers. Each country's system reflects its unique banking infrastructure and regulatory environment, emphasizing the need for standardized international codes like SWIFT for cross-border transactions.

Understanding these international variations is crucial for businesses and individuals engaging in global financial activities. While the U.S. routing number system is straightforward for domestic transfers, familiarity with SWIFT codes, IBANs, and other country-specific identifiers ensures seamless international transactions. As global banking continues to evolve, these systems play a vital role in maintaining accuracy, security, and efficiency across borders.

Andrew Jackson's Bold Veto: Dismantling the Second National Bank

You may want to see also

Explore related products

![]()

ACH vs. Wire Transfers: Routing numbers differ for ACH transactions and wire transfers within the same bank

When it comes to transferring funds electronically, two common methods are ACH (Automated Clearing House) transfers and wire transfers. While both rely on routing numbers to identify the financial institution involved, it’s important to understand that routing numbers differ for ACH transactions and wire transfers within the same bank. This distinction is crucial because each system operates differently and requires specific routing information to ensure accurate and efficient processing. ACH transfers, typically used for domestic transactions like direct deposits, bill payments, and peer-to-peer transfers, use a standard nine-digit routing number assigned by the American Bankers Association (ABA). On the other hand, wire transfers, which are often used for larger, time-sensitive, or international transactions, require a separate routing number known as a SWIFT code (for international wires) or a wire routing number (for domestic wires).

The reason for this difference lies in how the two systems function. ACH transactions are processed in batches through the ACH network, which is managed by the Federal Reserve and the Electronic Payments Network. This system is cost-effective and efficient for high-volume, low-value transactions. Wire transfers, however, are processed individually in real-time through networks like the Society for Worldwide Interbank Financial Telecommunication (SWIFT) or the Fedwire Funds Service. Because wire transfers prioritize speed and security, they often come with higher fees and require more specific routing information. For example, a bank’s ACH routing number might be used for setting up direct deposits, while its wire routing number is necessary for sending or receiving large sums of money domestically or internationally.

To illustrate, consider a bank like Bank of America. Its ACH routing number is typically a nine-digit ABA number, such as 026009593, which is used for domestic ACH transactions. However, for domestic wire transfers, the routing number changes to a Fedwire routing number, such as 026009593, while international wire transfers require the bank’s SWIFT code, BOFAUS3N. This highlights the importance of using the correct routing number for the specific type of transaction to avoid delays or errors. Customers must verify the appropriate routing number with their bank to ensure funds are directed accurately.

Another key difference is the structure and purpose of the routing numbers. ACH routing numbers are standardized and universally used within the United States for electronic transactions. Wire transfer routing numbers, however, can vary depending on whether the transfer is domestic or international. For instance, domestic wire transfers use a Fedwire routing number, while international wires rely on SWIFT codes, which are unique to each bank and country. This complexity underscores why banks maintain separate routing numbers for ACH and wire transfers, even though they may appear similar at first glance.

In summary, while a single bank may have multiple routing numbers, ACH and wire transfers require different routing numbers due to the distinct systems and processes they utilize. ACH transactions use a standard nine-digit ABA routing number, while wire transfers require a Fedwire routing number for domestic transfers or a SWIFT code for international ones. Understanding this difference is essential for ensuring smooth and accurate fund transfers. Always confirm the correct routing number with your bank to avoid complications, as using the wrong number can result in delays, additional fees, or failed transactions. This knowledge not only helps individuals and businesses navigate electronic payments effectively but also highlights the intricacies of the banking system’s infrastructure.

Bank Teller Jobs: Resume Builder or Dead End?

You may want to see also

Explore related products

![]()

Credit Unions: Credit unions also have unique routing numbers distinct from traditional banks

Credit unions, as member-owned financial cooperatives, operate differently from traditional banks, and this distinction extends to their routing numbers. While both banks and credit unions use routing numbers to identify themselves in financial transactions, credit unions have their own unique set of routing numbers that are distinct from those used by banks. This uniqueness is essential for ensuring that transactions are processed accurately and securely within the credit union system. Routing numbers for credit unions typically follow the same nine-digit format as those for banks, but they are assigned specifically to credit unions by the American Bankers Association (ABA) or other relevant authorities, depending on the country.

The number of routing numbers assigned to credit unions is part of the broader pool of routing numbers available for financial institutions. In the United States, for example, there are approximately 26,000 active routing numbers, which include both banks and credit unions. While the exact number of routing numbers exclusively assigned to credit unions is not publicly disclosed, it is a significant portion of the total, reflecting the widespread presence of credit unions in the financial landscape. Each credit union is assigned at least one routing number, and larger credit unions with multiple branches or service centers may have additional routing numbers to manage their operations effectively.

One key reason credit unions have distinct routing numbers is to maintain their identity and operational independence within the financial system. These routing numbers are used for various transactions, including direct deposits, electronic payments, wire transfers, and ACH (Automated Clearing House) transactions. By having unique routing numbers, credit unions can ensure that funds are directed to the correct institution and that members’ transactions are processed seamlessly. This distinction also helps prevent confusion and errors in transactions between credit unions and banks, as each type of institution operates under its own set of regulatory and operational guidelines.

Members of credit unions should be aware of their institution’s routing number, as it is required for many financial activities. This number can typically be found on the credit union’s website, mobile banking app, or printed on checks. Unlike banks, which may have more widespread brand recognition, credit unions often rely on their unique routing numbers to facilitate transactions and maintain their member-focused services. It’s important for members to verify the correct routing number with their credit union to avoid delays or errors in transactions, especially when setting up direct deposits or electronic payments.

In summary, credit unions have unique routing numbers that set them apart from traditional banks, ensuring their transactions are processed accurately within the financial system. While the total number of routing numbers for credit unions is not separately published, they are part of the broader pool of routing numbers assigned to financial institutions. These distinct routing numbers are crucial for maintaining the operational independence of credit unions and facilitating seamless transactions for their members. Understanding and using the correct routing number is essential for credit union members to manage their finances effectively.

Deutsche Bank's Application Acceptance Rate: Insights and Analysis

You may want to see also

Explore related products

![]()

Routing Number Structure: A 9-digit code identifying financial institutions for transactions

The routing number, a 9-digit code, is a critical component in the U.S. banking system, serving as a unique identifier for financial institutions during transactions. This structure is not arbitrary; each digit and segment within the number carries specific information. The first four digits, known as the Federal Reserve Routing Symbol, identify the Federal Reserve Bank district and the specific bank within that district. This segment ensures that transactions are routed to the correct geographic region and institution. Understanding this structure is essential for anyone involved in financial transactions, as it guarantees accuracy and efficiency in processing payments, transfers, and other banking operations.

The next four digits in the routing number represent the American Bankers Association (ABA) Institution Identifier. This segment uniquely identifies the specific bank or financial institution within the Federal Reserve district. Given the vast number of banks in the U.S., this portion of the code is crucial for distinguishing between institutions that might otherwise share similar names or locations. The combination of the Federal Reserve Routing Symbol and the ABA Institution Identifier ensures that each bank has a distinct routing number, preventing errors in transaction processing.

The final digit in the routing number is the check digit, which serves as a verification tool. This digit is calculated using a specific algorithm applied to the first eight digits of the routing number. Its purpose is to detect errors in the routing number, such as typos or transpositions, ensuring the integrity of the transaction. Without this check digit, even a small mistake in entering the routing number could lead to significant issues, such as funds being sent to the wrong institution. Thus, the check digit is a vital safeguard in the routing number structure.

Given the structured and standardized nature of routing numbers, the total number of possible combinations is finite but vast. With 9 digits, each ranging from 0 to 9, the theoretical maximum number of unique routing numbers is 10 billion. However, not all combinations are used, as certain patterns or sequences may be reserved or restricted. As of current estimates, there are approximately 26,000 active routing numbers in use across the United States. This number reflects the diversity of financial institutions, including commercial banks, credit unions, and other entities that participate in the ACH (Automated Clearing House) network or wire transfer systems.

The routing number structure is designed to accommodate the needs of a complex and dynamic financial system. While the total number of possible routing numbers is large, the actual number in use is a fraction of this, tailored to the existing banking landscape. Financial institutions are assigned routing numbers by the ABA, ensuring that each new bank or credit union receives a unique identifier. This assignment process is carefully managed to avoid duplication and maintain the system's integrity. As the banking sector evolves, with mergers, acquisitions, and new institutions entering the market, the pool of active routing numbers adjusts accordingly, reflecting the current state of the industry.

In conclusion, the routing number structure, with its 9-digit format, is a meticulously designed system that facilitates secure and efficient financial transactions. Each segment of the number—the Federal Reserve Routing Symbol, the ABA Institution Identifier, and the check digit—plays a distinct role in ensuring accuracy and reliability. While the theoretical maximum number of routing numbers is vast, the actual number in use is carefully managed to meet the needs of the U.S. banking system. Understanding this structure is key to appreciating how financial institutions are uniquely identified and how transactions are processed seamlessly across the country.

Reviving Trust: How the New Deal Stabilized Banks and the Economy

You may want to see also

Frequently asked questions

There are over 26,000 unique bank routing numbers (also known as ABA routing numbers) in the United States, as assigned by the American Bankers Association (ABA).

Not always. Larger banks may have multiple routing numbers based on the region or state where the account was opened, while smaller banks typically have only one routing number.

No, the number of routing numbers varies by country. For example, the U.S. uses ABA routing numbers, while other countries have their own systems, such as sort codes in the UK or IFSC codes in India.

Yes, a bank can have multiple routing numbers, especially if it operates in different regions or has merged with other institutions. Each routing number corresponds to a specific location or function.