The Federal Reserve System, often referred to as the Fed, plays a crucial role in the United States' financial landscape, overseeing monetary policy, regulating banks, and maintaining economic stability. A key aspect of its structure is the division of the country into 12 distinct banking districts, each with its own Federal Reserve Bank. These districts, established by the Federal Reserve Act of 1913, are strategically located across the nation to ensure regional representation and address the diverse economic needs of different areas. Understanding how many banking districts the Fed operates and their functions provides insight into the decentralized yet coordinated approach of the U.S. central banking system.

| Characteristics | Values |

|---|---|

| Number of Banking Districts | 12 |

| Official Name | Federal Reserve Districts |

| Headquarters Locations | Boston, New York, Philadelphia, Cleveland, Richmond, Atlanta, Chicago, St. Louis, Minneapolis, Kansas City, Dallas, San Francisco |

| Purpose | To oversee monetary policy, regulate banks, and provide financial services within their regions |

| Governing Body | Federal Reserve System (The Fed) |

| Established | December 23, 1913 (Federal Reserve Act) |

| Key Functions | Monetary policy implementation, bank supervision, financial stability |

| District Banks | Each district has a Federal Reserve Bank with a president and board |

| Geographical Coverage | Each district covers multiple states or parts of states |

| Latest Data Year | 2023 |

Explore related products

What You'll Learn

- Federal Reserve Structure: Overview of the Fed's 12 regional banking districts across the U.S

- District Responsibilities: Roles in monetary policy, bank supervision, and financial stability

- District Locations: Cities housing the 12 Federal Reserve Banks nationwide

- District Leadership: Presidents and their influence on Federal Open Market Committee decisions

- Historical Context: Evolution of the 12 districts since the Fed's establishment in 1913

![]()

Federal Reserve Structure: Overview of the Fed's 12 regional banking districts across the U.S

The Federal Reserve System, often referred to as "the Fed," is the central banking system of the United States. Established by the Federal Reserve Act of 1913, it was designed to provide the nation with a safer, more flexible banking system. A key aspect of the Fed's structure is its division into 12 regional banking districts, each with its own Federal Reserve Bank. These districts were created to ensure that the central banking system is responsive to the diverse economic conditions across the country. The 12 Federal Reserve Banks are located in major cities, including Boston, New York, Philadelphia, Cleveland, Richmond, Atlanta, Chicago, St. Louis, Minneapolis, Kansas City, Dallas, and San Francisco. Each bank operates independently but under the oversight of the Board of Governors in Washington, D.C.

The 12 regional banking districts are not uniform in size or economic focus, as they were designed to reflect the economic landscapes of their respective regions. For example, the Federal Reserve Bank of New York, which serves the Second District, plays a unique role due to its jurisdiction over Wall Street and its responsibility for implementing monetary policy through open market operations. In contrast, the Federal Reserve Bank of Minneapolis, serving the Ninth District, focuses on the economies of states like Minnesota, Montana, and the Dakotas, which are heavily influenced by agriculture and natural resources. Each district is governed by a board of directors, including representatives from the banking industry and the public, ensuring local input into the Fed's operations.

The structure of these districts allows the Federal Reserve to gather localized economic data and insights, which are critical for formulating effective monetary policy. Each Federal Reserve Bank conducts research, supervises member banks, and provides financial services within its district. Additionally, the banks play a role in distributing currency, processing payments, and managing the nation's money supply. The decentralized nature of the 12 districts ensures that regional economic disparities are considered in the Fed's decision-making process, promoting a more balanced approach to national economic stability.

Another important aspect of the 12 regional banking districts is their role in the Federal Open Market Committee (FOMC), the body responsible for setting monetary policy. The president of the Federal Reserve Bank of New York is a permanent voting member of the FOMC, while the other 11 bank presidents rotate voting rights annually. This structure ensures that regional perspectives are represented in policy discussions. The Board of Governors, which consists of seven members appointed by the President of the United States, also plays a central role in overseeing the entire system and ensuring consistency across districts.

In summary, the Federal Reserve's 12 regional banking districts are a cornerstone of its structure, enabling the central bank to address the unique economic needs of different parts of the country. By decentralizing operations and incorporating local input, the Fed maintains a flexible and responsive approach to monetary policy and banking supervision. This regional framework has been instrumental in fostering economic stability and growth across the United States since the Fed's inception. Understanding these districts provides valuable insight into how the Federal Reserve operates as a unified yet regionally attuned institution.

Does ICICI Bank Call for Transaction Inquiries? Facts You Need to Know

You may want to see also

Explore related products

![]()

District Responsibilities: Roles in monetary policy, bank supervision, and financial stability

The Federal Reserve System, often referred to as "the Fed," is structured into 12 regional banking districts, each with its own Federal Reserve Bank. These districts play a critical role in implementing monetary policy, supervising banks, and ensuring financial stability. Each district operates independently but collaborates closely with the Federal Reserve Board in Washington, D.C., to achieve the Fed's overarching goals of price stability, maximum employment, and a stable financial system. The district responsibilities are multifaceted, encompassing monetary policy execution, bank supervision, and financial stability oversight.

In the realm of monetary policy, each Federal Reserve Bank contributes to the formulation and implementation of policies aimed at controlling inflation, managing interest rates, and fostering economic growth. District banks gather economic data and insights from their regions, which are crucial for the Federal Open Market Committee (FOMC) when making decisions about interest rates and open market operations. Additionally, district banks execute monetary policy actions by buying or selling securities in the open market, thereby influencing the money supply and credit conditions. Their regional expertise ensures that monetary policy is tailored to the unique economic conditions of their respective areas.

Bank supervision is another key responsibility of the Federal Reserve districts. Each district oversees and regulates state-chartered banks that are members of the Federal Reserve System, as well as bank holding companies and financial institutions of systemic importance. District banks conduct on-site inspections, review financial reports, and ensure compliance with federal laws and regulations. They assess the safety and soundness of banking institutions, monitor risk management practices, and enforce consumer protection laws. By maintaining the integrity of the banking system, district banks contribute to overall financial stability and protect depositors and consumers.

The role of Federal Reserve districts in financial stability is equally vital. Districts monitor emerging risks in their regions, such as asset bubbles, excessive leverage, or liquidity shortages, and report these risks to the Board of Governors. They also participate in stress testing and scenario analysis to evaluate the resilience of financial institutions and markets. During times of financial crisis, district banks serve as lenders of last resort, providing liquidity to banks and financial institutions to prevent systemic collapses. Their regional presence allows them to respond swiftly and effectively to local financial disruptions, ensuring the stability of the broader financial system.

Furthermore, Federal Reserve districts engage in community outreach and research, which indirectly supports their core responsibilities. They conduct studies on regional economic trends, labor markets, and industry dynamics, providing valuable insights for policymakers. Districts also collaborate with local stakeholders, including businesses, nonprofits, and government agencies, to address economic challenges and promote financial literacy. This grassroots engagement enhances the Fed's understanding of regional economies and strengthens its ability to fulfill its mandate.

In summary, the 12 Federal Reserve districts are integral to the functioning of the U.S. financial system. Through their roles in monetary policy, bank supervision, and financial stability, they ensure that the Fed's policies are effectively implemented and adapted to regional needs. Their combined efforts contribute to a resilient banking system, a stable economy, and the overall well-being of the nation.

Can Banks Mortgage Foreclosed Homes?

You may want to see also

Explore related products

![]()

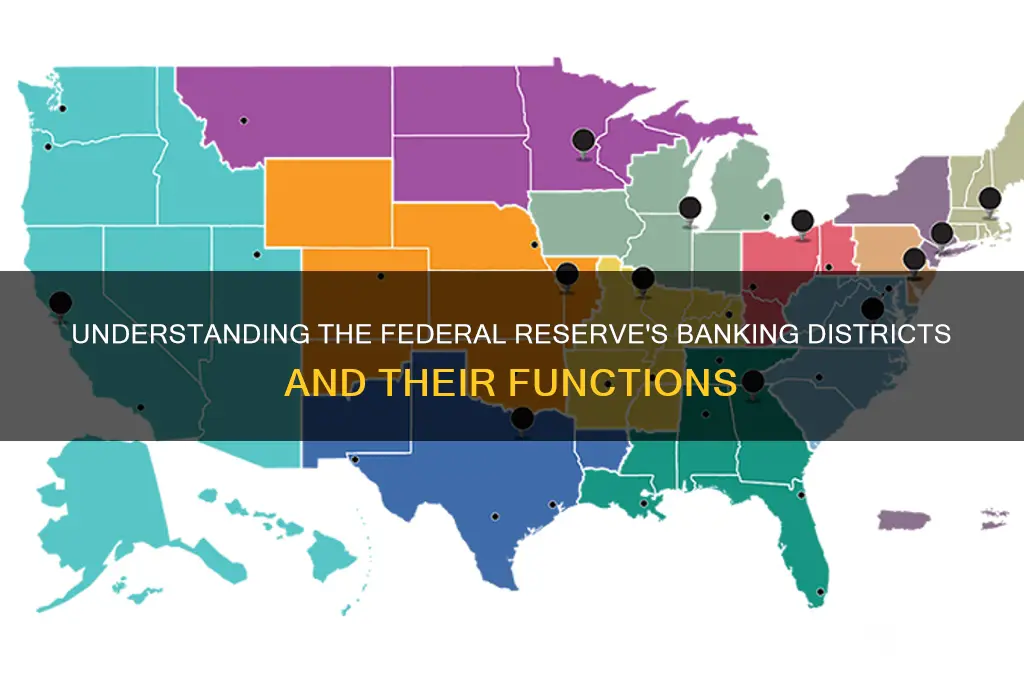

District Locations: Cities housing the 12 Federal Reserve Banks nationwide

The Federal Reserve System, often referred to as "the Fed," is the central banking system of the United States, and it is divided into 12 distinct banking districts, each housing a Federal Reserve Bank. These districts were established by the Federal Reserve Act of 1913 to ensure regional representation and responsiveness to local economic conditions. The cities housing these 12 Federal Reserve Banks are strategically located across the nation to cover diverse economic landscapes. Each district is identified by a number and a headquarters city, which serves as the central hub for its operations.

District 1: Boston, Massachusetts

The First District is headquartered in Boston, one of the oldest and most historically significant cities in the U.S. The Federal Reserve Bank of Boston serves New England, including states like Maine, Massachusetts, New Hampshire, Rhode Island, and Vermont, as well as parts of Connecticut. Boston's role as a financial and educational hub makes it an ideal location for overseeing the economic activities of this region.

District 2: New York, New York

The Second District, headquartered in New York City, is arguably the most influential due to its global financial significance. The Federal Reserve Bank of New York is responsible for the New York region, including parts of New Jersey and Connecticut, and plays a critical role in implementing monetary policy and regulating international financial markets. Its proximity to Wall Street underscores its importance in the global economy.

District 3: Philadelphia, Pennsylvania

Philadelphia, the birthplace of American independence, houses the Third District's Federal Reserve Bank. This bank serves eastern Pennsylvania, southern New Jersey, and Delaware. Philadelphia's historical and economic importance, coupled with its position as a major metropolitan area, makes it a key location for monitoring and supporting regional economic growth.

District 4: Cleveland, Ohio

The Fourth District is headquartered in Cleveland, a city known for its industrial heritage and economic resilience. The Federal Reserve Bank of Cleveland covers Ohio, western Pennsylvania, eastern Kentucky, and the northern panhandle of West Virginia. Cleveland's central location within this district allows it to effectively address the economic needs of a diverse and industrially significant region.

District 5: Richmond, Virginia

Richmond, the capital of Virginia, is home to the Fifth District's Federal Reserve Bank. This bank serves Virginia, Maryland, North Carolina, South Carolina, and parts of West Virginia. Richmond's historical and economic prominence in the Southeast makes it a strategic location for overseeing the economic activities of this rapidly growing region.

District 6: Atlanta, Georgia

Atlanta, a major economic and cultural hub in the Southeast, houses the Sixth District's Federal Reserve Bank. This bank covers Alabama, Florida, Georgia, and parts of Louisiana, Mississippi, and Tennessee. Atlanta's role as a center for business, technology, and transportation makes it an ideal location for monitoring and supporting the economic development of the region.

District 7: Chicago, Illinois

Chicago, the economic powerhouse of the Midwest, is home to the Seventh District's Federal Reserve Bank. This bank serves Illinois, Indiana, Iowa, Michigan, and Wisconsin. Chicago's status as a global financial center and its central location within the district enable it to effectively address the economic challenges and opportunities of the Midwest.

District 8: St. Louis, Missouri

St. Louis houses the Eighth District's Federal Reserve Bank, serving Arkansas, southern Indiana, southern Illinois, western Kentucky, eastern Missouri, and West Tennessee. St. Louis's position as a major inland port and its historical significance in American commerce make it a key location for overseeing the economic activities of this geographically diverse district.

District 9: Minneapolis, Minnesota

Minneapolis, a major city in the Upper Midwest, is home to the Ninth District's Federal Reserve Bank. This bank covers Minnesota, Montana, North Dakota, South Dakota, and parts of Michigan and Wisconsin. Minneapolis's economic importance and its role as a center for finance and industry make it well-suited to support the economic needs of this region.

District 10: Kansas City, Missouri

Kansas City houses the Tenth District's Federal Reserve Bank, serving Colorado, Kansas, Nebraska, Oklahoma, Wyoming, and western Missouri. Kansas City's central location within this district and its significance as a transportation and economic hub make it an ideal headquarters for monitoring and supporting regional economic activities.

District 11: Dallas, Texas

Dallas, a major economic center in the South, is home to the Eleventh District's Federal Reserve Bank. This bank covers Texas, northern Louisiana, and southern New Mexico. Dallas's role as a hub for finance, technology, and energy makes it a strategic location for overseeing the economic growth of this dynamic region.

District 12: San Francisco, California

San Francisco, a global financial and technological hub, houses the Twelfth District's Federal Reserve Bank. This bank serves Alaska, Arizona, California, Hawaii, Idaho, Nevada, Oregon, Utah, and Washington. San Francisco's position as a leader in innovation and its economic influence on the West Coast make it a critical location for addressing the unique economic challenges and opportunities of this region.

These 12 cities, each housing a Federal Reserve Bank, collectively ensure that the Fed's policies and operations are tailored to the specific economic conditions of their respective regions, fostering stability and growth across the nation.

Ally Bank Minimum Balance Requirements: What You Need to Know

You may want to see also

Explore related products

![]()

District Leadership: Presidents and their influence on Federal Open Market Committee decisions

The Federal Reserve System is structured into 12 regional banking districts, each with its own Federal Reserve Bank. At the helm of each district is a president, appointed by the respective bank's board of directors. These district presidents play a crucial role in shaping monetary policy through their participation in the Federal Open Market Committee (FOMC), the body responsible for setting key interest rates and managing the nation's money supply. While the Federal Reserve Chair holds significant influence, the district presidents contribute unique regional perspectives that can sway FOMC decisions.

District presidents bring to the FOMC table insights into the economic conditions of their respective regions. For instance, the president of the Federal Reserve Bank of New York, which is the most influential due to its role as the Fed's primary dealer in open market operations, often has a more global and financial market-oriented perspective. In contrast, the president of the Federal Reserve Bank of Dallas might emphasize the impact of oil prices on the regional economy, while the president of the Federal Reserve Bank of San Francisco could highlight technology sector trends. These diverse viewpoints are essential for crafting policies that address the nuanced needs of the entire nation.

The voting structure of the FOMC further underscores the influence of district presidents. While the seven members of the Board of Governors in Washington, D.C., have permanent voting rights, only five of the 12 district presidents vote in any given year, with the New York president being a permanent voter. The remaining four voting spots rotate annually among the other 11 district presidents. This rotating structure ensures that a variety of regional perspectives are represented in policy decisions, preventing any single region from dominating the discourse.

District presidents also influence FOMC decisions through their participation in committee discussions and their ability to shape the narrative around economic conditions. Even non-voting presidents attend FOMC meetings, contribute to debates, and provide critical input on regional economic trends. Their insights can sway the opinions of voting members, including the Fed Chair, particularly when regional issues have broader implications for the national economy. For example, a district president highlighting a sharp rise in unemployment in their region might prompt the committee to adopt a more accommodative monetary policy stance.

Beyond the FOMC, district presidents extend their influence through public speeches, research, and engagement with local business and community leaders. These activities help shape public and market expectations about future monetary policy actions. By articulating their views on economic conditions and policy, district presidents can influence financial markets and guide economic behavior. Their leadership is thus not confined to the FOMC room but extends to broader economic discourse, making them key figures in the Federal Reserve's mission to promote maximum employment, stable prices, and moderate long-term interest rates.

In summary, the district presidents of the Federal Reserve Banks are integral to the FOMC's decision-making process. Their regional expertise, voting roles, and ability to shape economic narratives ensure that monetary policy reflects the diverse needs of the U.S. economy. As leaders of their respective districts, they bridge the gap between national policy and local economic realities, playing a vital role in the Federal Reserve's dual mandate. Understanding their influence provides a deeper appreciation of the decentralized yet cohesive structure of the Federal Reserve System.

Does Renters Insurance Cover Stolen Bank Funds? What You Need to Know

You may want to see also

Explore related products

![]()

Historical Context: Evolution of the 12 districts since the Fed's establishment in 1913

The establishment of the Federal Reserve System in 1913 marked a pivotal moment in U.S. financial history, and the creation of its 12 banking districts was a cornerstone of this reform. The Federal Reserve Act, signed into law by President Woodrow Wilson, aimed to decentralize monetary authority and address the banking panics that had plagued the nation. The 12 districts were strategically designed to reflect the geographic and economic diversity of the United States, ensuring regional representation and responsiveness to local banking needs. Each district was assigned a Federal Reserve Bank, tasked with overseeing member banks, managing currency circulation, and implementing monetary policy within its jurisdiction. This structure was intended to balance centralized control with regional autonomy, a principle that remains fundamental to the Fed's operations today.

In the early years, the boundaries of these districts were drawn to align with major economic hubs and transportation routes of the time. For example, the Federal Reserve Bank of New York was established to oversee the nation's financial capital, while the Federal Reserve Bank of Chicago was positioned to serve the burgeoning industrial Midwest. Other districts, such as those in St. Louis, Minneapolis, and Dallas, were created to cater to the agricultural and resource-rich regions of the country. These initial boundaries were not static; they were adjusted periodically to account for shifting economic landscapes, population growth, and the rise of new financial centers. By the 1920s, the districts had largely stabilized, though minor changes continued to occur in response to regional developments.

The Great Depression of the 1930s tested the resilience of the Federal Reserve System and its district structure. The crisis highlighted the need for greater coordination among the districts and led to significant reforms under the Banking Act of 1935. This legislation strengthened the Federal Reserve Board's authority over the district banks, fostering a more unified approach to monetary policy. While the number of districts remained unchanged, their roles evolved to emphasize national economic stability alongside regional concerns. The district banks became critical in implementing the Fed's responses to the Depression, including managing interest rates, regulating bank activities, and stabilizing the financial system.

Post-World War II, the U.S. economy experienced rapid expansion, and the Federal Reserve districts adapted to support this growth. The rise of new industries, technological advancements, and globalization necessitated further adjustments in district operations. For instance, the Federal Reserve Bank of San Francisco became increasingly important as the West Coast economy boomed, driven by sectors like aerospace, technology, and international trade. Similarly, the Federal Reserve Bank of Atlanta played a key role in the economic development of the Southeast, particularly as manufacturing and services expanded in the region. Throughout this period, the districts maintained their core functions while modernizing their operations to address contemporary challenges.

In recent decades, the 12 Federal Reserve districts have continued to evolve in response to changing economic conditions and financial innovations. The advent of digital banking, the globalization of financial markets, and the increasing complexity of monetary policy have required the districts to enhance their capabilities. Today, each district conducts economic research, supervises banks, and engages with local communities to inform policy decisions. Despite technological advancements and economic shifts, the district structure has proven enduring, providing a framework that balances national objectives with regional perspectives. The historical evolution of these districts underscores their role as a vital component of the Federal Reserve's mission to promote economic stability and growth across the United States.

Routing Numbers: USAA Banks and Their Unique Identifiers

You may want to see also

Frequently asked questions

The Federal Reserve System has 12 banking districts, each with its own Federal Reserve Bank.

The 12 Federal Reserve Banks are located in Boston, New York, Philadelphia, Cleveland, Richmond, Atlanta, Chicago, St. Louis, Minneapolis, Kansas City, Dallas, and San Francisco.

The 12 districts were established to ensure regional representation and responsiveness to local economic conditions across the United States.

No, the districts vary in size and population. For example, the Federal Reserve Bank of San Francisco covers the largest geographic area, while the Federal Reserve Bank of New York serves the most populous region.