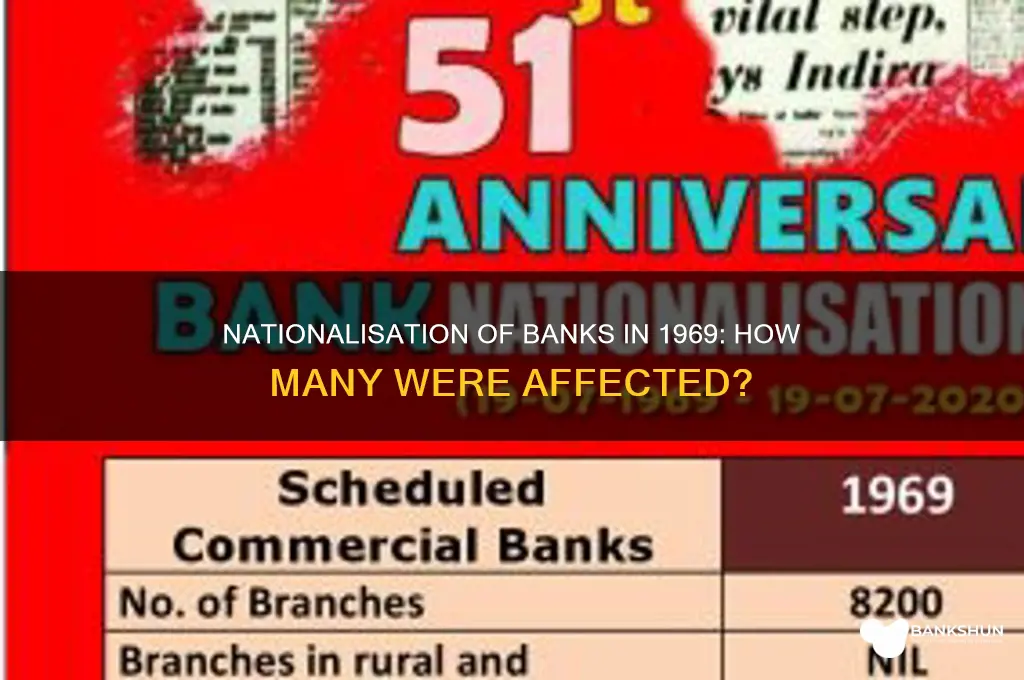

In 1969, the Indian government took a significant step towards economic reform by nationalizing 14 major commercial banks, a move aimed at extending credit facilities to rural areas, promoting agricultural development, and ensuring that banking services reached the underserved sectors of the population. This landmark decision, announced by then-Prime Minister Indira Gandhi, transformed the banking landscape by bringing these institutions under state control, thereby aligning them with the nation’s socio-economic objectives and reducing the concentration of economic power in the hands of a few. The nationalization of these banks marked a pivotal moment in India’s financial history, laying the foundation for a more inclusive and equitable banking system.

| Characteristics | Values |

|---|---|

| Number of banks nationalized in 1969 | 14 |

| Date of nationalization | July 19, 1969 |

| Government in power during nationalization | Indira Gandhi-led Indian National Congress government |

| Objective of nationalization | To extend credit to priority sectors, such as agriculture, small-scale industries, and other underserved areas |

| Banks nationalized in 1969 | Allahabad Bank, Bank of Baroda, Bank of India, Bank of Maharashtra, Central Bank of India, Canara Bank, Dena Bank, Indian Bank, Indian Overseas Bank, Punjab National Bank, Syndicate Bank, UCO Bank, Union Bank of India, and United Bank of India |

| Current status of nationalized banks (as of 2023) | Many have undergone mergers and consolidations; for example, Allahabad Bank merged with Indian Bank, and Syndicate Bank merged with Canara Bank |

| Total number of nationalized banks in India (as of 2023) | 12 (after mergers and consolidations) |

| Role of nationalized banks in Indian economy | Continue to play a significant role in financial inclusion, priority sector lending, and supporting government initiatives |

Explore related products

What You'll Learn

![]()

List of 14 banks nationalized in 1969

In 1969, the Indian government took a significant step towards consolidating the banking sector by nationalizing 14 major banks. This move was aimed at ensuring that banking services reached all segments of society, particularly the rural and underserved areas, and to align the banking sector with the country's developmental goals. The nationalization was carried out under the Banking Companies (Acquisition and Transfer of Undertakings) Act, 1969, which came into effect on July 19, 1969. This act brought 14 prominent banks under government control, marking a pivotal moment in India's economic history.

The List of 14 banks nationalized in 1969 includes some of the most influential banking institutions of that time. These banks were selected based on their size, reach, and impact on the economy. The first bank on the list is the Central Bank of India, established in 1911, which was one of the oldest and most respected banks in the country. Another notable bank is the Bank of Baroda, founded in 1908, which had a strong presence in both urban and rural areas. The Punjab National Bank, established in 1894, was also nationalized, further strengthening the government's control over the northern regions of India.

The list also includes the Canara Bank, founded in 1906, which had a significant presence in South India. The Bank of India, established in 1906, and the Union Bank of India, founded in 1919, were also nationalized, ensuring broader coverage across the country. Other banks in the list are the Syndrome Bank (now known as Syndicate Bank), Allahabad Bank, Indian Bank, United Bank of India, Dena Bank, United Commercial Bank, Bank of Maharashtra, and Indian Overseas Bank. Each of these banks had unique strengths and regional focuses, which collectively contributed to the diversification and expansion of banking services nationwide.

The nationalization of these 14 banks led to a significant increase in the number of bank branches, particularly in rural and semi-urban areas. It also resulted in a shift in lending priorities, with a greater emphasis on agriculture, small-scale industries, and other priority sectors. The government's control over these banks allowed for better regulation and alignment with national economic policies. However, it also sparked debates about efficiency, bureaucracy, and the role of the private sector in banking.

In conclusion, the List of 14 banks nationalized in 1969 represents a landmark event in India's banking history. These banks, including the Central Bank of India, Bank of Baroda, Punjab National Bank, and others, played a crucial role in expanding financial inclusion and supporting the country's developmental agenda. The nationalization of these institutions not only transformed the banking landscape but also laid the foundation for a more inclusive and regulated financial system in India. This move remains a key reference point in discussions about the role of government in the economy and the evolution of the banking sector.

Citibank and US Bank: What's the Difference?

You may want to see also

Explore related products

![]()

Objectives behind the 1969 bank nationalization policy

The 1969 bank nationalization policy in India was a landmark decision that aimed to transform the country's banking sector and align it with the broader goals of economic development and social justice. On July 19, 1969, the Indian government nationalized 14 major commercial banks, a move that significantly altered the financial landscape. This policy was driven by several key objectives, each addressing specific economic and social challenges of the time.

One of the primary objectives behind the 1969 bank nationalization was to extend credit to priority sectors that were previously underserved by private banks. Before nationalization, private banks tended to concentrate their lending activities in urban areas and favored large industries and wealthy individuals. The government aimed to redirect credit towards agriculture, small-scale industries, and other rural sectors, which were critical for inclusive growth. By nationalizing banks, the government sought to ensure that financial resources were allocated more equitably, fostering balanced regional development and reducing economic disparities between urban and rural areas.

Another crucial objective was to promote financial inclusion and make banking services accessible to the masses. At the time, a significant portion of the Indian population, particularly in rural areas, had no access to formal banking services. Nationalization was seen as a means to expand the banking network into remote and underserved regions, enabling more people to participate in the formal economy. This move was aligned with the government's broader goal of poverty alleviation and empowering marginalized communities through access to credit and savings facilities.

The policy also aimed to curb the concentration of economic power in the hands of a few business houses that controlled major private banks. Prior to nationalization, these banks often served the interests of their owners and associated industrial groups, leading to monopolistic practices and unequal distribution of wealth. By bringing these banks under public control, the government intended to democratize the financial system and prevent the exploitation of banking resources for private gain. This was part of a larger strategy to establish a more equitable economic order.

Furthermore, the 1969 bank nationalization sought to strengthen the stability and efficiency of the banking system. Private banks were often plagued by mismanagement, inadequate capitalization, and a lack of standardized practices. Nationalization allowed the government to implement uniform policies, improve regulatory oversight, and ensure the financial health of banks. This was essential for building public trust in the banking system and mobilizing savings on a larger scale, which could then be channeled into productive investments for national development.

Lastly, the policy was motivated by the goal of aligning the banking sector with national planning objectives. India's planned economy required a financial system that could support the government's Five-Year Plans and other developmental initiatives. Nationalized banks were expected to act as instruments of economic policy, channeling funds into sectors identified as priorities by the government. This integration of banking with national planning was seen as vital for achieving self-reliance and accelerating India's industrialization and agricultural growth.

In summary, the 1969 bank nationalization policy was driven by a multifaceted set of objectives aimed at addressing economic inequalities, promoting inclusive growth, and aligning the financial sector with national developmental goals. By nationalizing 14 major banks, the Indian government sought to create a more equitable, accessible, and efficient banking system that could serve as a catalyst for broader socioeconomic transformation.

Has FaZe Banks Ever Won an MLG Tournament? The Truth Revealed

You may want to see also

Explore related products

![]()

Impact of 1969 nationalization on Indian banking sector

The nationalization of banks in India in 1969 marked a pivotal moment in the country's financial history, with 14 major banks being brought under government control. This move was driven by the objective of expanding banking services to rural areas, promoting financial inclusion, and aligning the banking sector with the goals of socialist economic policies. The immediate impact was a significant shift in the banking landscape, as these nationalized banks now accounted for a substantial portion of the sector's assets and branches. This transformation laid the foundation for a more inclusive and regulated banking system, but it also brought about challenges and long-term consequences.

One of the most notable impacts of the 1969 nationalization was the expansion of banking services to rural and underserved areas. Prior to nationalization, banks were largely concentrated in urban centers, catering primarily to industrialists and wealthy individuals. With the government taking control, there was a deliberate push to open branches in rural and semi-urban areas, ensuring that banking services reached the masses. This led to increased financial inclusion, as farmers, small traders, and low-income groups gained access to credit, savings, and other banking facilities. The priority sector lending norms, introduced post-nationalization, further mandated banks to allocate a certain percentage of their loans to sectors like agriculture, small-scale industries, and weaker sections of society.

However, the nationalization also had economic and operational implications for the banking sector. While the intent was to democratize credit, the lack of market-driven efficiency led to inefficiencies in loan disbursement and recovery. Banks often faced political pressure to extend loans without adequate risk assessment, leading to a rise in non-performing assets (NPAs) over time. Additionally, the absence of competition and profit-oriented goals resulted in slower technological adoption and innovation compared to private banks. This created a gap in service quality and efficiency, which became more evident in the decades following nationalization.

Another significant impact was the shift in the role of banks from profit-making entities to instruments of social and economic policy. Nationalized banks were increasingly used to implement government schemes and priorities, such as poverty alleviation programs and subsidized credit for priority sectors. While this aligned with the broader goals of reducing economic inequality, it often came at the cost of financial health and sustainability of the banks. The capital adequacy of these banks was frequently compromised, requiring periodic recapitalization by the government to keep them afloat.

In the long term, the 1969 nationalization reshaped the Indian banking sector's structure and functioning, but it also highlighted the need for reforms. By the 1990s, the inefficiencies and financial weaknesses of nationalized banks became evident, prompting the government to introduce banking sector reforms. These reforms aimed to enhance competitiveness, improve governance, and encourage private participation. Despite the challenges, the nationalization of 1969 remains a critical chapter in India's banking history, as it laid the groundwork for a more inclusive financial system while underscoring the importance of balancing social objectives with financial viability.

Westpac Bank Transfer Timelines: How Long Do Transactions Take?

You may want to see also

![]()

Criteria for selecting banks for nationalization in 1969

In 1969, the Indian government nationalized 14 major banks, a move that significantly reshaped the country's banking sector. The selection of these banks was not arbitrary but based on specific criteria aimed at achieving broader economic and social objectives. One of the primary criteria was the size and reach of the banks. The government targeted banks with a substantial deposit base and a wide network of branches, as these institutions had the potential to influence a larger segment of the population. Banks like the State Bank of India, Punjab National Bank, and Canara Bank were chosen due to their extensive presence across the country, ensuring that nationalization could effectively serve the goal of financial inclusion.

Another critical criterion was the financial health and stability of the banks. While the government aimed to bring key financial institutions under public control, it was essential to select banks that were financially viable and capable of contributing to the economy without immediate risk of collapse. Banks with a strong balance sheet, adequate capital, and manageable non-performing assets were prioritized. This ensured that the nationalized banks could continue to function efficiently and support the government's developmental agenda without becoming a burden on public finances.

The ownership structure of the banks also played a significant role in their selection. Banks with concentrated ownership, particularly those controlled by a few business families or industrial houses, were prime candidates for nationalization. The government sought to curb the influence of private interests in the banking sector and prevent the misuse of banking resources for personal or corporate gains. By nationalizing such banks, the government aimed to align banking operations with national priorities rather than private profits.

A fourth criterion was the potential for social and economic development. The government selected banks that could be effectively utilized to channel credit into priority sectors such as agriculture, small-scale industries, and rural development. Banks with a history of lending to these sectors or those operating in regions with significant developmental needs were given preference. This criterion ensured that nationalization would serve as a tool for reducing regional disparities and promoting balanced economic growth.

Lastly, the strategic importance of the banks in the financial ecosystem was considered. Banks that played a pivotal role in the money market, foreign exchange operations, or industrial financing were targeted to ensure that the government could gain control over critical financial functions. This criterion was essential for enabling the government to implement monetary and fiscal policies more effectively and to mobilize resources for national development projects.

In summary, the criteria for selecting banks for nationalization in 1969 were multifaceted, focusing on size, financial stability, ownership structure, developmental potential, and strategic importance. These criteria ensured that the nationalization process aligned with the government's objectives of fostering financial inclusion, curbing private monopolies, and promoting economic development across India.

Understanding Debt-to-Income Ratio: How Banks Assess Your Financial Health

You may want to see also

![]()

Comparison of pre- and post-1969 nationalized banking systems

The nationalization of banks in India in 1969 marked a significant turning point in the country's banking sector, transforming it from a largely private, unorganized system to a more centralized, government-controlled framework. Prior to 1969, the Indian banking system was dominated by private banks, many of which were owned by wealthy industrialists and business families. These banks primarily catered to the needs of urban, affluent customers, leaving rural and agricultural sectors underserved. The pre-1969 era was characterized by limited branch networks, restricted access to credit for small farmers and rural entrepreneurs, and a lack of focus on priority sector lending. This led to regional disparities in economic development and hindered the overall growth of the agricultural and rural economies.

Post-1969, the nationalization of 14 major banks brought about a paradigm shift in the banking landscape. The primary objective was to align the banking sector with the goals of socialist economic policies, ensuring that credit was directed towards priority sectors such as agriculture, small-scale industries, and exports. The nationalized banks were mandated to expand their branch networks into rural and semi-urban areas, thereby increasing financial inclusion. This period saw a significant rise in the number of bank branches, particularly in underserved regions, which facilitated greater access to banking services for the rural population. The focus on priority sector lending ensured that a substantial portion of bank credit was allocated to agriculture, small businesses, and other socially important sectors, fostering more equitable economic growth.

One of the most notable differences between the pre- and post-1969 banking systems was the role of the government. Before nationalization, the government had limited control over banking operations, and monetary policies were less effective in influencing credit flow. After 1969, the government gained direct control over a significant portion of the banking sector, enabling it to implement policies aimed at reducing regional disparities and promoting balanced economic development. The Reserve Bank of India (RBI) could now more effectively regulate the banking system, ensuring that banks adhered to priority sector lending targets and other social objectives.

However, the nationalized banking system also faced challenges. The increased government control led to bureaucratic inefficiencies, with banks often prioritizing political directives over commercial viability. This resulted in mounting non-performing assets (NPAs), particularly in the agricultural sector, where loan waivers and subsidized credit schemes were common. Additionally, the lack of competition and innovation in the nationalized banking system led to slower adoption of technology and customer-centric services compared to private banks. Despite these drawbacks, the post-1969 era achieved its primary goal of expanding banking services to rural areas and promoting financial inclusion, which had long-term positive impacts on the Indian economy.

In comparison, the pre-1969 banking system, while more efficient and commercially oriented, failed to address the needs of the majority of the population, particularly in rural areas. The nationalization of banks in 1969 was a corrective measure aimed at bridging this gap and ensuring that the banking sector contributed to the broader goals of economic and social development. While the post-1969 system had its shortcomings, it laid the foundation for a more inclusive and socially responsive banking framework. The subsequent liberalization of the banking sector in the 1990s built upon this foundation, introducing competition and technological advancements while retaining the focus on financial inclusion and priority sector lending.

In conclusion, the comparison of pre- and post-1969 nationalized banking systems highlights the trade-offs between commercial efficiency and social equity. The pre-1969 era was characterized by private dominance and limited reach, while the post-1969 period brought government control, expanded access, and a focus on priority sectors. Both systems had their strengths and weaknesses, but the 1969 nationalization was a pivotal step in aligning the banking sector with the socio-economic objectives of a developing nation. It set the stage for future reforms that sought to balance inclusion, efficiency, and innovation in India's banking landscape.

Step-by-Step Guide to Accessing Your Schwab Bank Account Online

You may want to see also

Frequently asked questions

In 1969, 14 major banks were nationalized in India.

The primary goal was to extend credit to priority sectors like agriculture, small industries, and marginalized communities, ensuring inclusive economic growth.

The 14 banks included Central Bank of India, Bank of India, Punjab National Bank, Canara Bank, Bank of Baroda, and Union Bank of India, among others.

Indira Gandhi was the Prime Minister of India when the banks were nationalized in 1969.

It led to a significant expansion of banking services in rural areas, increased credit availability for priority sectors, and laid the foundation for a more inclusive financial system.