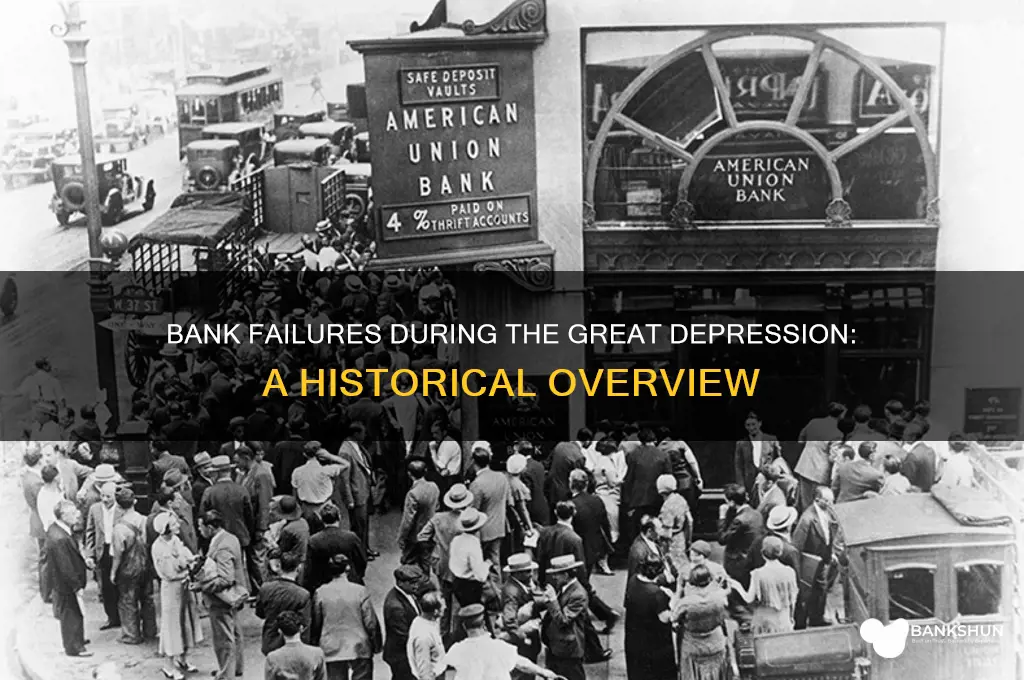

The Great Depression, a period of severe economic downturn that began with the Wall Street crash in 1929, had a devastating impact on the global financial system, particularly in the United States. One of the most striking manifestations of this crisis was the unprecedented number of bank failures. Between 1929 and 1933, over 9,000 banks closed their doors, leaving millions of Americans without access to their savings and exacerbating the economic hardship. This wave of failures was driven by a combination of factors, including widespread panic, speculative investments, and a lack of deposit insurance, which eroded public confidence in the banking system. The collapse of so many banks not only deepened the Depression but also prompted significant financial reforms, including the establishment of the Federal Deposit Insurance Corporation (FDIC) in 1933, to prevent such a catastrophe from recurring.

| Characteristics | Values |

|---|---|

| Total number of bank failures (1929-1933) | Approximately 9,000 |

| Peak year of bank failures | 1933 (around 4,000 banks failed) |

| Percentage of banks that failed | About 40% of all banks in existence at the start of the Great Depression |

| Total deposits lost | Estimated at $1.3 billion (in 1933 dollars) |

| Number of banks at the start of the Great Depression | Around 25,000 |

| Number of banks remaining by 1934 | Approximately 14,000 |

| Primary causes of bank failures | Panic-induced bank runs, deflation, and economic contraction |

| Impact on public trust | Significant erosion of confidence in the banking system |

| Government response | Establishment of the Federal Deposit Insurance Corporation (FDIC) in 1933 |

| Long-term effect on banking regulations | Increased federal oversight and deposit insurance to prevent future crises |

Explore related products

What You'll Learn

- Bank Failures by Year: Annual breakdown of bank closures during the Great Depression

- Causes of Failures: Key factors leading to widespread bank collapses

- Regional Impact: Geographic distribution of bank failures across the U.S

- Government Response: Policies and measures to address banking crises

- Economic Consequences: Long-term effects of bank failures on the economy

![]()

Bank Failures by Year: Annual breakdown of bank closures during the Great Depression

The Great Depression, which began with the stock market crash in October 1929, had a devastating impact on the U.S. banking system. Bank failures became a hallmark of this period, eroding public confidence and exacerbating economic hardship. To understand the scale of the crisis, it’s essential to examine the annual breakdown of bank closures during the 1930s. The data reveals a pattern of escalating failures, peaking in the early years of the Depression, followed by a gradual decline as recovery measures took effect.

In 1930, the first full year of the Great Depression, 1,350 banks failed, marking the beginning of a dire trend. This was a significant increase from previous years, as the economic downturn exposed the fragility of many financial institutions. The closures were widespread, affecting both rural and urban banks, and were driven by a combination of factors, including declining agricultural prices, industrial slowdowns, and panic among depositors. The lack of federal deposit insurance meant that bank runs were common, as customers rushed to withdraw their funds before their bank collapsed.

The year 1931 saw an even more alarming rise in bank failures, with 2,294 banks closing their doors. This surge was fueled by the deepening economic crisis and the contagion effect, where the failure of one bank triggered panic in others. The Hoover administration attempted to stabilize the situation through measures like the Reconstruction Finance Corporation (RFC), which provided loans to struggling banks, but these efforts were insufficient to stem the tide of failures. By the end of 1931, the banking system was in a state of near-collapse, with thousands of communities losing access to financial services.

The peak of bank failures occurred in 1933, when 4,004 banks failed. This year was particularly catastrophic due to a nationwide banking panic in March, which prompted President Franklin D. Roosevelt to declare a "bank holiday" shortly after taking office. During this period, all banks were closed to prevent further runs, and only those deemed solvent were allowed to reopen. The passage of the Glass-Steagall Act and the establishment of the Federal Deposit Insurance Corporation (FDIC) in 1933 were pivotal in restoring confidence and reducing failures. By the end of the year, the rate of closures began to decline.

From 1934 onward, the number of bank failures decreased significantly, reflecting the impact of New Deal policies and the gradual economic recovery. In 1934, 1,456 banks failed, less than half the number in 1933. By 1935, the figure dropped further to 295, and by 1936, only 37 banks failed. This trend continued through the remainder of the decade, as federal regulations and improved economic conditions stabilized the banking sector. By the late 1930s, the crisis of bank failures had largely subsided, though the Great Depression’s effects lingered in other areas of the economy.

In total, approximately 9,000 banks failed during the Great Depression, representing about one-third of all banks in operation in 1929. This unprecedented wave of closures highlighted the need for stronger financial regulations and safety nets, lessons that shaped U.S. banking policy for decades to come. The annual breakdown of bank failures underscores the severity of the crisis and the transformative impact of the reforms implemented in its wake.

Discovering Erie Bank Sports Park: Distance and Directions Guide

You may want to see also

Explore related products

![]()

Causes of Failures: Key factors leading to widespread bank collapses

The Great Depression witnessed an unprecedented wave of bank failures, with approximately 9,000 banks closing their doors between 1929 and 1933. This widespread collapse was not the result of a single cause but rather a combination of interconnected factors that exposed vulnerabilities within the banking system. One of the primary causes was the speculative lending practices prevalent in the 1920s. Banks had extended loans to finance stock market speculation and real estate ventures, often with little regard for borrowers' ability to repay. When the stock market crashed in October 1929, investors defaulted on loans, leaving banks with significant losses and illiquid assets.

Another critical factor was the lack of deposit insurance, which eroded public confidence in the banking system. During the Great Depression, bank deposits were not guaranteed by the federal government, leading to widespread panic as depositors rushed to withdraw their funds. This phenomenon, known as a bank run, drained banks of their cash reserves, forcing many to close their doors. The absence of a safety net exacerbated the crisis, as even solvent banks were unable to withstand the sudden outflow of deposits.

The agricultural crisis of the 1920s and early 1930s also played a significant role in bank failures. Farmers, already struggling with falling crop prices and mounting debts, were unable to repay loans to rural banks. This led to a cascade of failures, particularly in agricultural regions, where local banks were heavily dependent on farm loans. The Dust Bowl further compounded these issues, displacing farmers and worsening economic conditions in rural areas.

Additionally, the deflationary spiral that characterized the Great Depression severely impacted banks. As prices fell, the real value of debts increased, making it harder for borrowers to repay loans. This reduced banks' asset values and eroded their capital bases. Deflation also discouraged borrowing and spending, leading to a contraction in economic activity and further weakening banks' financial positions.

Lastly, the fragmented and unregulated banking system of the time contributed to the widespread failures. Thousands of small, independent banks operated with limited resources and inadequate risk management practices. Many lacked diversification in their loan portfolios, making them vulnerable to localized economic shocks. The absence of a centralized regulatory framework meant there were no mechanisms to stabilize the banking system or provide emergency liquidity during the crisis.

In summary, the bank failures during the Great Depression were the result of a complex interplay of factors, including speculative lending, lack of deposit insurance, agricultural distress, deflation, and a weak regulatory environment. These issues exposed deep-seated vulnerabilities in the banking system, leading to a crisis of confidence and widespread collapses. The lessons from this period underscored the need for reforms, such as deposit insurance and stronger regulation, to prevent future banking crises.

Unveiling the NCLEX Question Bank: Size, Scope, and Study Strategies

You may want to see also

Explore related products

![]()

Regional Impact: Geographic distribution of bank failures across the U.S

The Great Depression had a profound and uneven impact on the U.S. banking system, with bank failures concentrated in specific regions due to economic vulnerabilities and local conditions. The Midwest and Great Plains states, often referred to as the "Dust Bowl" region, experienced some of the highest rates of bank failures. States like Iowa, Kansas, Nebraska, and Oklahoma were particularly hard-hit due to a combination of agricultural distress, drought, and declining commodity prices. Farmers defaulted on loans en masse, leaving banks with insufficient collateral and liquidity, ultimately leading to widespread closures. This regional concentration of failures exacerbated the economic downturn, as local communities lost access to credit and financial services, further stifling recovery efforts.

The Southeast also suffered significant bank failures, though for somewhat different reasons. States such as Alabama, Georgia, and Mississippi were already economically fragile due to their reliance on agriculture and low industrialization. The collapse of cotton prices and the lack of economic diversification left banks in these areas highly exposed. Additionally, the region's financial institutions were often smaller and less capitalized, making them more susceptible to runs and insolvency. The ripple effects of these failures deepened poverty and unemployment in an already struggling region, creating long-lasting economic scars.

In contrast, the Northeast and parts of the Midwest, particularly urban centers like New York, Chicago, and Boston, saw fewer bank failures relative to their economic size. These regions benefited from greater economic diversification, stronger industrial bases, and larger, more resilient financial institutions. However, even in these areas, smaller banks and those heavily exposed to speculative investments or real estate suffered disproportionately. The concentration of larger banks in these regions also meant that their failures, though fewer in number, had a more significant systemic impact, contributing to the erosion of public confidence in the banking system nationwide.

The West Coast, particularly California, experienced a mixed impact. While California's economy was more diversified than the Dust Bowl states, its banks were not immune to the crisis. The collapse of real estate markets and the decline of industries tied to agriculture and manufacturing led to bank failures, particularly in rural areas. However, the region's relative economic strength and the emergence of new industries, such as entertainment and aerospace, helped mitigate the overall impact compared to other regions.

Finally, the South Central states, including Texas and Arkansas, faced a unique set of challenges. Texas, despite its oil wealth, saw numerous bank failures due to over-reliance on the energy sector and speculative lending. Arkansas and other neighboring states struggled with agricultural defaults and a lack of economic diversification. The geographic distribution of bank failures across the U.S. during the Great Depression highlights the interplay between regional economies, local industries, and the vulnerability of financial institutions to systemic shocks. Understanding this distribution is crucial for comprehending the uneven impact of the crisis and the lessons it offers for modern financial stability.

Green Dot Bank: Legit or a Scam?

You may want to see also

Explore related products

![]()

Government Response: Policies and measures to address banking crises

During the Great Depression, a staggering number of banks failed, with estimates ranging from 9,000 to 10,000 bank closures between 1929 and 1933. This widespread collapse of the banking system necessitated swift and comprehensive government intervention to restore public confidence and stabilize the financial sector. The government’s response to the banking crisis during this period involved a combination of immediate relief measures, regulatory reforms, and long-term policies aimed at preventing future crises. These actions were critical in addressing the root causes of bank failures and rebuilding the nation’s financial infrastructure.

One of the most immediate and impactful government responses was the establishment of the Reconstruction Finance Corporation (RFC) in 1932 under President Herbert Hoover. The RFC was designed to provide emergency loans to banks, railroads, and other financial institutions to prevent further insolvencies. By injecting capital into struggling banks, the RFC aimed to shore up their balance sheets and restore liquidity to the financial system. While the RFC’s initial impact was limited due to its cautious lending practices, it laid the groundwork for more aggressive intervention under President Franklin D. Roosevelt’s administration.

Upon taking office in 1933, President Roosevelt declared a national bank holiday, temporarily closing all banks to prevent further runs and assess their solvency. This bold measure was followed by the passage of the Emergency Banking Act, which allowed federal inspectors to evaluate banks and reopen those deemed solvent. Simultaneously, the government launched a public awareness campaign to reassure depositors, emphasizing the safety of their funds through the newly established Federal Deposit Insurance Corporation (FDIC). The FDIC provided insurance for bank deposits up to $5,000 (later increased), effectively ending widespread bank runs by guaranteeing the security of depositors’ money.

In addition to these immediate measures, the government implemented long-term regulatory reforms to prevent future banking crises. The Glass-Steagall Act of 1933 was a cornerstone of these reforms, separating commercial and investment banking activities to reduce risk-taking by deposit-holding institutions. The act also established the Federal Deposit Insurance Corporation (FDIC) as a permanent entity, ensuring deposit insurance remained a fixture of the banking system. These reforms aimed to restore trust in banks, protect depositors, and create a safer financial environment.

Another critical aspect of the government’s response was the Federal Reserve’s role in monetary policy. The Fed took steps to increase liquidity in the banking system, lowering interest rates and expanding the money supply to encourage lending and stimulate economic activity. However, critics argue that the Fed’s actions during the early years of the Depression were insufficient, as it failed to prevent deflation and the collapse of numerous banks. Lessons from this period led to a more proactive approach by central banks in future crises, emphasizing the importance of swift and decisive monetary intervention.

In summary, the government’s response to the banking crisis during the Great Depression was multifaceted, involving immediate relief measures, regulatory reforms, and long-term policies to stabilize the financial system. The establishment of the RFC, the creation of the FDIC, the passage of the Glass-Steagall Act, and the Federal Reserve’s monetary actions were all pivotal in addressing the crisis. These measures not only helped restore public confidence in banks but also laid the foundation for a more resilient and regulated financial system, shaping the way governments respond to banking crises to this day.

Does US Bank Offer a Christmas Club Savings Account?

You may want to see also

Explore related products

![]()

Economic Consequences: Long-term effects of bank failures on the economy

The Great Depression witnessed an unprecedented wave of bank failures, with approximately 9,000 banks closing their doors between 1929 and 1933. This massive collapse of financial institutions had profound and lasting economic consequences, reshaping the American economy and influencing global financial systems for decades. One of the most immediate long-term effects was the erosion of public trust in the banking sector. As depositors lost their savings due to bank failures, confidence in financial institutions plummeted. This distrust persisted well beyond the 1930s, leading to a cautious approach to banking and investment that stifled economic growth. The psychological impact of these failures created a generation of risk-averse individuals and businesses, slowing the recovery process and altering consumer behavior for years to come.

Another significant long-term consequence was the contraction of credit availability, which severely hampered economic activity. Banks that survived the Great Depression became overly conservative in their lending practices, fearing further instability. This credit crunch made it difficult for businesses to secure loans for expansion or even day-to- العمليات, stifling entrepreneurship and innovation. Small businesses, in particular, struggled to access capital, leading to widespread closures and high unemployment rates. The reduced flow of credit also affected consumers, who found it harder to obtain mortgages or personal loans, further depressing demand for goods and services. This cycle of reduced spending and investment perpetuated economic stagnation, delaying recovery and exacerbating the Depression's effects.

The bank failures also led to significant structural changes in the financial system, prompting government intervention to prevent future crises. The establishment of the Federal Deposit Insurance Corporation (FDIC) in 1933 was a direct response to the widespread loss of depositor funds. By insuring bank deposits, the FDIC aimed to restore public confidence and stabilize the banking sector. Additionally, the Glass-Steagall Act of 1933 separated commercial and investment banking, reducing risky financial practices that had contributed to the bank failures. While these reforms were necessary, they also introduced long-term regulatory frameworks that altered the way banks operated. The increased oversight and regulation, while beneficial for stability, sometimes constrained financial innovation and efficiency, shaping the banking industry's trajectory for decades.

The long-term effects of bank failures during the Great Depression also extended to macroeconomic policies and global economic relations. The crisis highlighted the need for active government intervention in economic affairs, leading to the rise of Keynesian economics and the development of countercyclical fiscal and monetary policies. Governments began to take a more proactive role in managing economic downturns, a shift that continues to influence policy decisions today. However, the Depression also fostered economic nationalism and protectionist policies, as countries sought to shield their economies from external shocks. The collapse of international trade and financial cooperation during this period had lasting implications for global economic integration, contributing to the fragmentation of the world economy in the 1930s and beyond.

Finally, the bank failures during the Great Depression had a profound impact on income inequality and social welfare. As wealth stored in banks vanished, the middle class was disproportionately affected, leading to a widening wealth gap. The loss of savings and the subsequent economic hardship deepened poverty and exacerbated social tensions. In response, governments expanded social safety nets and introduced programs to support the unemployed and vulnerable populations. While these measures provided immediate relief, they also established long-term expectations for government assistance during economic crises. The legacy of these policies continues to shape debates about the role of government in addressing economic inequality and ensuring financial stability.

Do Restricted Donations Require a Separate Bank Account?

You may want to see also

Frequently asked questions

Approximately 9,000 banks failed during the Great Depression, with over 4,000 closing in 1933 alone.

About one-third to one-half of all U.S. banks failed during the Great Depression, depending on the source and timeframe considered.

Bank failures were caused by a combination of factors, including the stock market crash of 1929, widespread panic, bank runs, deflation, and a lack of deposit insurance.

Bank failures led to a loss of savings for millions of Americans, reduced lending, and a severe contraction in the money supply, exacerbating the economic downturn.

The U.S. government established the Federal Deposit Insurance Corporation (FDIC) in 1933 to insure deposits, restore public confidence, and prevent future bank runs.