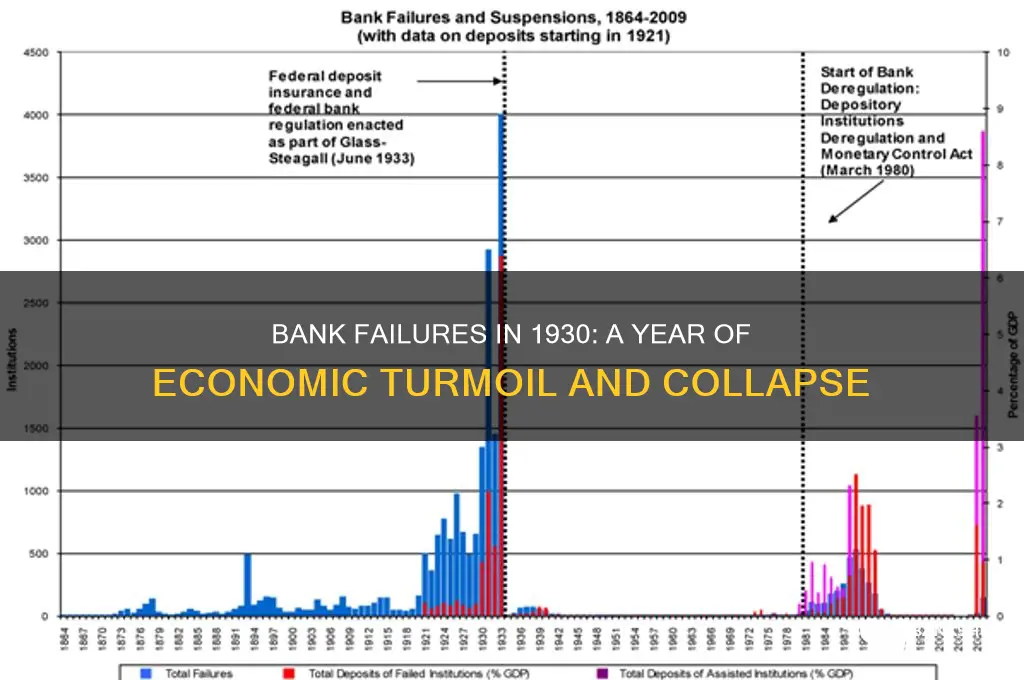

The year 1930 marked a critical period in the Great Depression, during which the U.S. banking system faced unprecedented strain. As economic conditions deteriorated, thousands of banks across the nation were forced to close their doors, leaving millions of Americans without access to their savings and exacerbating the financial crisis. By the end of 1930, over 1,300 banks had shut down, a stark indicator of the deepening economic turmoil that would persist throughout the decade. This wave of bank failures not only eroded public trust in financial institutions but also highlighted the urgent need for systemic reforms to stabilize the banking sector.

| Characteristics | Values |

|---|---|

| Number of bank failures in 1930 (USA) | Approximately 1,350 |

| Total number of banks in the USA (1930) | Around 25,000 |

| Failure rate (1930) | ~5.4% |

| Primary cause of failures | Economic downturn, agricultural depression, and bank runs |

| Total deposits lost (estimate) | Over $500 million (in 1930 dollars) |

| Number of bank failures in the following year (1931) | 2,293 |

| Peak year for bank failures during the Great Depression | 1933 (4,004 failures) |

| Total bank failures during the Great Depression (1930-1933) | Over 9,000 |

| Percentage of banks that failed during the Great Depression | ~40% |

| Source of data | Federal Reserve, FDIC, and historical records |

Explore related products

What You'll Learn

- Bank Failures by Region: Breakdown of bank closures across different U.S. regions in 1930

- Causes of Shutdowns: Key factors leading to widespread bank failures during the Great Depression

- Impact on Economy: Effects of 1930 bank closures on unemployment, businesses, and consumer trust

- Government Response: Measures taken by the government to address the banking crisis in 1930

- Comparison to Other Years: How 1930 bank failures compare to closures in surrounding years

![]()

Bank Failures by Region: Breakdown of bank closures across different U.S. regions in 1930

The year 1930 marked a significant escalation in bank failures across the United States, a trend that would deepen as the Great Depression worsened. While exact figures vary depending on the source, estimates suggest that approximately 1,350 banks closed their doors in 1930 alone. This widespread collapse of financial institutions had a devastating impact on communities nationwide, eroding public confidence and exacerbating economic hardship. To understand the scope of this crisis, it is crucial to examine the regional distribution of bank failures, as certain areas were disproportionately affected.

The Midwest emerged as one of the hardest-hit regions in 1930. States like Illinois, Indiana, and Ohio saw a surge in bank closures, largely due to their heavy reliance on agriculture and manufacturing. The collapse of commodity prices and industrial production left many banks in these states unable to meet depositor demands, leading to a wave of failures. For instance, Illinois alone witnessed the closure of over 200 banks in 1930, a staggering number that underscored the region's vulnerability. The Midwest's economic dependence on sectors severely impacted by the Depression made it a focal point of the banking crisis.

The South also experienced a significant number of bank failures in 1930, though the impact varied across states. Rural areas, particularly those dependent on cotton and other cash crops, were especially vulnerable. The decline in agricultural prices left farmers unable to repay loans, straining local banks. States like Arkansas, Mississippi, and Alabama reported high failure rates, with many small, rural banks unable to survive. However, the South's overall failure rate was slightly lower than the Midwest's, partly due to the region's less industrialized economy and the presence of larger, more stable banks in urban centers like Atlanta and New Orleans.

In contrast, the Northeast and West regions experienced fewer bank failures in 1930, though they were not immune to the crisis. The Northeast, home to major financial hubs like New York and Boston, benefited from a more diversified economy and stronger banking institutions. While some smaller banks in rural areas of New England and the Mid-Atlantic states failed, the region's larger banks generally withstood the initial shock. Similarly, the West, though less industrialized than the Midwest, saw a relatively lower number of failures, particularly in states like California, where the banking sector was more resilient. However, the crisis would eventually catch up to these regions as the Depression deepened in subsequent years.

A breakdown by region reveals the uneven impact of the 1930 banking crisis. The Midwest bore the brunt of the failures, followed by the South, while the Northeast and West were comparatively less affected. This regional disparity highlights the interconnectedness of local economies and their vulnerability to broader economic shocks. The bank closures of 1930 were not just a financial crisis but a reflection of the underlying economic weaknesses that the Great Depression exposed across different parts of the United States. Understanding this regional breakdown provides valuable insights into the origins and spread of one of the most devastating economic periods in American history.

How to Access Funds During Probate

You may want to see also

Explore related products

![]()

Causes of Shutdowns: Key factors leading to widespread bank failures during the Great Depression

The Great Depression was a period of severe economic downturn that had a profound impact on the banking sector, leading to widespread bank failures. According to historical records, approximately 1,350 banks failed in the United States in 1930 alone, marking a significant increase from previous years. This trend continued throughout the early 1930s, with a total of over 9,000 banks closing their doors by 1933. The causes of these shutdowns were multifaceted and interconnected, stemming from a combination of economic, financial, and regulatory factors. One of the primary factors was the overextension of credit by banks, which had fueled speculative investments in the stock market and real estate. When the stock market crashed in 1929, many borrowers defaulted on their loans, leaving banks with significant losses and a shortage of liquidity.

Another key factor contributing to bank failures was the widespread panic and loss of confidence among depositors. As news of bank closures spread, customers rushed to withdraw their funds, triggering a self-fulfilling prophecy of bank runs. This phenomenon, known as a "bank run," occurred when a large number of customers withdrew their deposits simultaneously, depleting the bank's reserves and rendering it insolvent. The lack of deposit insurance at the time exacerbated the situation, as depositors had no guarantee that their funds would be protected in the event of a bank failure. Consequently, banks were forced to liquidate assets at a rapid pace, often at a loss, to meet the demands of withdrawing customers, further straining their financial stability.

The fragile state of the agricultural sector also played a significant role in the wave of bank closures during the Great Depression. Many banks, particularly in rural areas, had a substantial portion of their loan portfolios tied to agricultural activities. The decline in crop prices and the resulting financial distress among farmers led to widespread loan defaults, undermining the financial health of these banks. As farmers struggled to repay their debts, banks were left with non-performing loans, eroding their capital base and reducing their ability to absorb losses. This situation was particularly acute in the Midwest and Southern regions of the United States, where agriculture was a dominant industry.

In addition to these factors, the regulatory environment of the time failed to provide adequate safeguards against bank failures. The absence of a central banking authority with the power to regulate and supervise banks allowed for risky lending practices and inadequate risk management. Many banks were undercapitalized, with insufficient reserves to withstand financial shocks. Furthermore, the lack of diversification in their loan portfolios made them vulnerable to sector-specific risks, such as the decline in agriculture. The Glass-Steagall Act, which separated commercial and investment banking, would not be enacted until 1933, leaving banks free to engage in speculative activities that ultimately contributed to their downfall. The combination of these factors created a perfect storm, leading to the widespread bank failures that characterized the early years of the Great Depression.

The economic contraction and deflationary pressures of the Great Depression also contributed to the financial distress of banks. As economic activity slowed, businesses and consumers reduced their spending, leading to a decline in demand for loans. This reduction in lending activity further strained bank revenues, making it difficult for them to generate sufficient income to cover their operating expenses. Deflation, characterized by a general decline in prices, exacerbated the situation by increasing the real value of debts, making it harder for borrowers to repay their loans. The resulting wave of bankruptcies and loan defaults put additional pressure on banks, eroding their asset quality and undermining their financial stability. This vicious cycle of economic decline, deflation, and bank failures would continue until the implementation of significant policy reforms and economic recovery measures in the mid-1930s.

Understanding Bank Interchange Income: How Transaction Fees Generate Revenue

You may want to see also

Explore related products

$6.79 $11.99

![]()

Impact on Economy: Effects of 1930 bank closures on unemployment, businesses, and consumer trust

The wave of bank closures in 1930, a pivotal year in the early stages of the Great Depression, had profound and far-reaching effects on the economy, particularly in terms of unemployment, businesses, and consumer trust. As the banking system crumbled, thousands of banks suspended operations or closed permanently, leading to a severe contraction in credit availability. This credit crunch directly impacted businesses, which relied heavily on loans to finance operations, purchase inventory, and invest in growth. Without access to capital, many businesses were forced to lay off workers or shut down entirely, exacerbating the unemployment crisis. By the end of 1930, unemployment rates had surged, leaving millions of Americans jobless and unable to contribute to economic activity.

The closure of banks also disrupted the flow of money within the economy, stifling business transactions and consumer spending. Small and medium-sized enterprises, which were the backbone of local economies, were particularly vulnerable. Many lacked the financial reserves to weather the crisis, and the loss of banking services meant they could not process payments, manage cash flow, or secure loans to stay afloat. This domino effect led to widespread business failures, further deepening the economic downturn. As businesses closed, suppliers and service providers also suffered, creating a ripple effect that touched nearly every sector of the economy.

Consumer trust in the financial system plummeted as bank closures became commonplace. Depositors, fearing the loss of their savings, rushed to withdraw funds in a phenomenon known as bank runs. This panic not only accelerated bank failures but also reduced the overall money supply, as cash was hoarded rather than spent. The erosion of trust in banks and financial institutions had long-term consequences, as consumers became more cautious with their spending and less willing to invest in the economy. This decline in consumer confidence contributed to a self-reinforcing cycle of economic decline, as reduced spending further weakened businesses and led to additional job losses.

The impact on unemployment was particularly devastating, as the bank closures directly and indirectly eliminated millions of jobs. Laid-off workers had limited opportunities to find new employment, given the widespread economic distress. This surge in unemployment reduced aggregate demand, as households had less disposable income to spend on goods and services. The resulting decline in consumer spending further strained businesses, leading to additional closures and job cuts. The unemployment rate, which had been rising since the stock market crash of 1929, spiked dramatically in 1930, reaching levels that would persist for years and define the Great Depression.

In summary, the bank closures of 1930 had a catastrophic impact on the economy, driving up unemployment, crippling businesses, and eroding consumer trust. The credit crunch and disruption of financial services paralyzed economic activity, while the loss of jobs and income reduced consumer spending. The collapse of trust in the banking system created a lasting psychological scar, shaping financial behavior for decades. These effects were not isolated but interconnected, forming a vicious cycle that deepened and prolonged the economic crisis. The events of 1930 underscored the critical role of banks in stabilizing the economy and highlighted the devastating consequences of their failure.

Exploring the Vast Number of Banks Operating in the United States

You may want to see also

Explore related products

![]()

Government Response: Measures taken by the government to address the banking crisis in 1930

In response to the escalating banking crisis of 1930, the U.S. government implemented a series of measures aimed at stabilizing the financial system and restoring public confidence. One of the earliest actions was the establishment of the Reconstruction Finance Corporation (RFC) in January 1932, though its roots and planning began in the earlier years of the crisis. The RFC was designed to provide emergency loans to banks, railroads, and other financial institutions to prevent further failures. By injecting capital into struggling banks, the government aimed to halt the wave of bank closures that had seen thousands of institutions shut down by 1930. The RFC’s efforts were part of a broader strategy to shore up the banking sector and prevent a complete collapse of the financial system.

Another critical measure was the passage of the Glass-Steagall Act in 1933, which, while enacted slightly after the peak of the 1930 bank closures, was a direct response to the crisis. This legislation separated commercial and investment banking activities to reduce risky speculation and protect depositors. It also established the Federal Deposit Insurance Corporation (FDIC), which insured bank deposits up to a certain amount, thereby reassuring the public that their savings were safe. This move was instrumental in stemming bank runs, as depositors no longer feared losing their money if a bank failed. The FDIC’s creation was a pivotal government response to the crisis, addressing one of its root causes: the lack of public trust in the banking system.

The government also took steps to regulate the banking industry more closely. The Federal Reserve, the nation’s central bank, was given expanded powers to oversee and stabilize the financial system. It was tasked with monitoring banks’ liquidity and ensuring they maintained sufficient reserves to meet withdrawal demands. Additionally, the Federal Reserve began to act as a lender of last resort, providing emergency funds to banks facing temporary shortages. These regulatory measures were designed to prevent the kind of unchecked risk-taking and insolvency that had contributed to the wave of bank closures in 1930.

To address the broader economic impact of the banking crisis, the government launched public works programs and relief efforts. The Emergency Banking Act of 1933 allowed the President to declare a bank holiday, temporarily closing banks to assess their solvency and reopen only those that were financially stable. This immediate action helped to stabilize the situation and prevent further panic. Simultaneously, the New Deal programs initiated by President Franklin D. Roosevelt aimed to stimulate economic recovery by creating jobs and providing financial assistance to those hardest hit by the crisis. These measures, while not directly focused on banks, were essential in restoring overall economic stability and reducing the strain on the financial system.

Finally, the government worked to improve transparency and accountability in the banking sector. Stricter reporting requirements were imposed on banks, and audits became more frequent to ensure compliance with regulations. The Securities Act of 1933 and the Securities Exchange Act of 1934 were also enacted to regulate the stock market and prevent the fraudulent practices that had exacerbated the banking crisis. These legislative actions were part of a comprehensive effort to rebuild the financial system on a more stable and trustworthy foundation, ensuring that the conditions leading to the 1930 bank closures would not recur.

Does Jeff Davis Bank Offer Notary Services? Find Out Here

You may want to see also

Explore related products

![]()

Comparison to Other Years: How 1930 bank failures compare to closures in surrounding years

The year 1930 marked a significant period of bank failures in the United States, but it is essential to place this figure in context by comparing it to the surrounding years. According to historical data, 1930 saw approximately 1,350 bank failures, a staggering number that reflects the deepening economic crisis of the Great Depression. However, this figure was not an isolated incident but part of a trend that began in the late 1920s and continued into the early 1930s. For instance, in 1929, around 659 banks failed, a number that nearly doubled in 1930, indicating a rapid deterioration of the banking sector.

When comparing 1930 to the following years, the trend of bank failures continued to escalate. In 1931, the number of bank closures rose to about 2,294, nearly double the figure from 1930. This sharp increase highlights the worsening economic conditions and the loss of public confidence in the banking system. By 1932, the situation had become even more dire, with approximately 1,454 banks failing, though this was slightly lower than 1931, it still represented a significant number of closures. These years collectively underscore the severity of the banking crisis during the early years of the Great Depression.

In contrast, the years immediately preceding 1930 had far fewer bank failures. For example, in 1928, only about 68 banks failed, a number that pales in comparison to the thousands that closed in the early 1930s. This disparity illustrates how the economic landscape shifted dramatically within a short period. The relatively stable banking environment of the late 1920s gave way to unprecedented turmoil by 1930, setting the stage for the massive failures that followed.

To further contextualize 1930, it is useful to examine the latter half of the 1930s, when the banking sector began to stabilize. By 1934, the number of bank failures had dropped to around 121, a significant decline from the peak years. This reduction can be attributed to the implementation of various government measures, such as the establishment of the Federal Deposit Insurance Corporation (FDIC) in 1933, which restored public trust in banks. The comparison between 1930 and these later years highlights the effectiveness of policy interventions in mitigating the banking crisis.

In summary, 1930 stands out as a pivotal year in the history of bank failures, with 1,350 closures representing a sharp increase from previous years and a precursor to even greater failures in 1931 and 1932. When compared to both the years leading up to and following 1930, it becomes clear that this period was the epicenter of the banking crisis during the Great Depression. The surrounding years provide essential context, showing the rapid decline and eventual recovery of the banking sector, making 1930 a critical point of reference in understanding the broader economic turmoil of the era.

How Long Does Your Bank History Remain Visible on Reports?

You may want to see also

Frequently asked questions

In 1930, approximately 1,350 banks failed in the United States, marking a significant increase in bank closures due to the onset of the Great Depression.

The bank closures in 1930 were primarily caused by economic instability, declining agricultural prices, and a lack of confidence in the banking system, exacerbated by the stock market crash of 1929.

No, bank closures in 1930 were not limited to the United States. The global economic downturn led to bank failures in other countries as well, though the U.S. experienced one of the highest numbers.

Bank shutdowns in 1930 led to widespread loss of savings for many Americans, as deposit insurance did not yet exist. This deepened economic hardship and eroded trust in financial institutions.

While some state and local governments attempted to stabilize banks, federal intervention was limited in 1930. Significant reforms, such as the creation of the FDIC, came later in the 1930s.