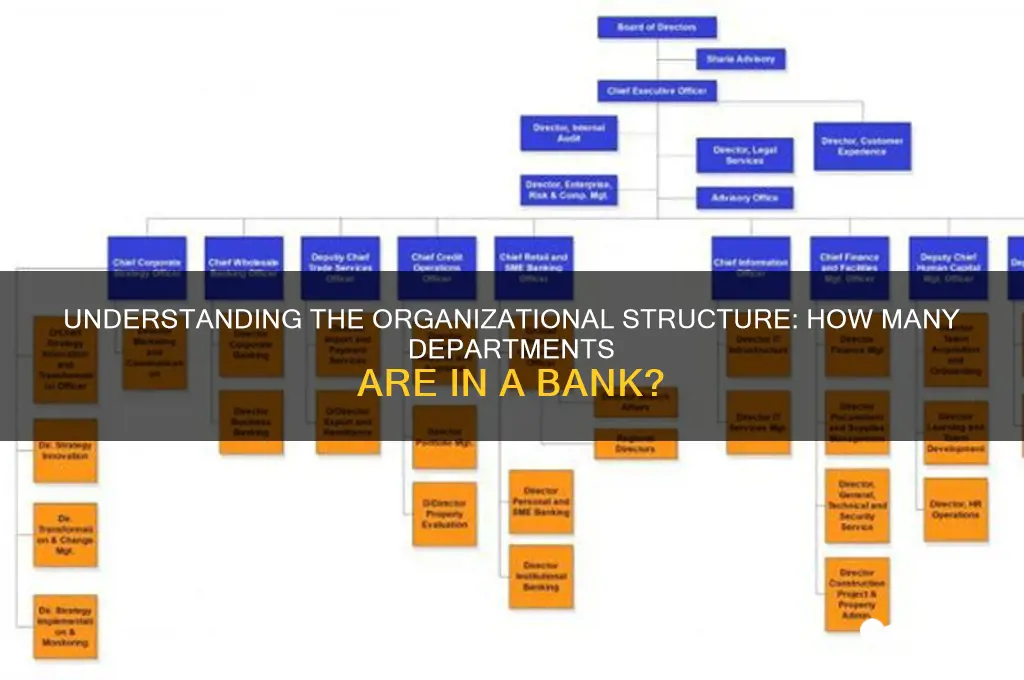

Banks typically operate with a structured organizational framework comprising multiple departments, each specializing in distinct functions to ensure efficient operations and comprehensive service delivery. The exact number of departments can vary depending on the bank’s size, scope, and business model, but common divisions include Retail Banking, Corporate Banking, Investment Banking, Wealth Management, Risk Management, Compliance, Human Resources, Information Technology, and Finance. These departments work collaboratively to manage customer accounts, process transactions, assess and mitigate risks, ensure regulatory adherence, and drive strategic growth, collectively contributing to the bank’s overall success and stability.

Explore related products

What You'll Learn

![]()

Retail Banking Operations

Within Retail Banking Operations, there are specialized units that focus on specific tasks to streamline processes and enhance service quality. For instance, the Customer Service Unit handles inquiries, resolves issues, and provides information about banking products. The Account Management Unit oversees the opening, maintenance, and closure of customer accounts, ensuring compliance with regulatory requirements. Additionally, the Transactions Processing Unit is responsible for the accurate and timely execution of financial transactions, including fund transfers, bill payments, and direct deposits. These units work collaboratively to ensure seamless operations and a positive customer experience.

Another critical aspect of Retail Banking Operations is the management of financial products tailored to individual customers. This includes offering personal loans, mortgages, credit cards, and investment products such as certificates of deposit (CDs) and mutual funds. The Product Management Unit within this department designs, markets, and administers these products, ensuring they meet customer needs and align with the bank's strategic goals. Sales and relationship managers play a vital role in promoting these products, providing personalized advice, and assisting customers in making informed financial decisions.

Technology plays a pivotal role in modern Retail Banking Operations, enabling banks to offer convenient and secure services. The Digital Banking Unit focuses on developing and maintaining online and mobile banking platforms, ensuring they are user-friendly, secure, and equipped with the latest features. This unit also oversees the integration of emerging technologies such as artificial intelligence and blockchain to enhance operational efficiency and customer engagement. Cybersecurity is a top priority, with dedicated teams working to protect customer data and prevent fraud.

Lastly, compliance and risk management are integral components of Retail Banking Operations. The Compliance Unit ensures that all activities adhere to local and international banking regulations, mitigating legal and reputational risks. The Risk Management Unit assesses and monitors potential risks associated with retail banking activities, implementing strategies to minimize financial losses. These units work closely with other departments to maintain the integrity of the bank's operations and safeguard customer interests. Together, these functions ensure that Retail Banking Operations remain robust, customer-centric, and aligned with the bank's overall objectives.

Does US Bank Offer Foreign Currency Exchange Services? Find Out Here

You may want to see also

Explore related products

![]()

Corporate Banking Structure

A typical bank's corporate banking structure is designed to efficiently manage a wide range of financial services tailored to businesses and large corporations. While the exact number and names of departments can vary between banks, there are several core divisions that are commonly found within the corporate banking sector. These departments work in tandem to provide comprehensive financial solutions, risk management, and strategic support to corporate clients.

One of the primary departments in corporate banking is the Corporate Relationship Management division. This team is responsible for building and maintaining relationships with corporate clients, understanding their financial needs, and offering customized banking solutions. Relationship managers act as the main point of contact for clients, ensuring that all their banking requirements are met, from loans and credit facilities to cash management services. This department plays a crucial role in client retention and business development.

Corporate Lending and Credit is another vital component of the corporate banking structure. This department focuses on evaluating and approving loan applications from businesses, assessing credit risk, and structuring financing solutions. It involves analyzing financial statements, industry trends, and the overall creditworthiness of corporate entities. The team here works closely with relationship managers to provide tailored lending products, including term loans, working capital facilities, and syndicated loans.

Treasury and Capital Markets is a specialized department that deals with a bank's own financial management and market-related activities. In the context of corporate banking, this team assists corporate clients in managing their treasury operations, foreign exchange risks, and investment portfolios. They offer services such as currency exchange, interest rate hedging, and investment advice, helping businesses optimize their financial strategies and mitigate market risks. This department often includes traders, analysts, and financial experts who monitor global markets and provide insights to both the bank and its corporate clients.

Additionally, Risk Management and Compliance is a critical function within corporate banking. This department ensures that the bank's corporate lending and investment activities adhere to regulatory requirements and internal risk policies. They assess and monitor credit, market, and operational risks associated with corporate clients and transactions. The team develops risk models, sets risk limits, and provides oversight to ensure the bank's corporate portfolio remains healthy and compliant. Given the complexity and scale of corporate banking operations, robust risk management is essential to safeguard the bank's assets and reputation.

Lastly, Corporate Advisory and Investment Banking services are often offered as part of a comprehensive corporate banking structure. This department provides strategic advice to corporate clients on mergers and acquisitions, initial public offerings (IPOs), debt restructuring, and other corporate finance activities. They assist businesses in raising capital, structuring deals, and navigating complex financial transactions. The advisory team typically includes financial analysts, industry experts, and legal professionals who work together to deliver tailored solutions for corporate clients' long-term growth and strategic objectives.

In summary, the corporate banking structure of a bank is organized into several specialized departments, each playing a unique role in serving the diverse needs of business clients. From relationship management and credit assessment to treasury services, risk control, and strategic advisory, these departments collaborate to offer a full suite of financial products and expertise to corporate entities. Understanding this structure is essential for businesses seeking to navigate the banking system and access the most relevant services for their financial goals.

Missouri Food Banks: Administration, Operations, and Community Support Explained

You may want to see also

Explore related products

![]()

Investment Banking Divisions

Another essential component of Investment Banking Divisions is Capital Markets, which is further segmented into equity capital markets (ECM) and debt capital markets (DCM). ECM professionals assist companies in issuing shares to the public or private investors, while DCM experts help clients raise funds through bond issuances or other debt instruments. These teams collaborate with underwriters, legal advisors, and regulators to ensure compliance and successful execution of transactions. The ability to navigate complex regulatory environments and market conditions is crucial in these roles, as they directly impact a client's ability to secure financing.

Sales and Trading is another vital division within investment banking, focusing on facilitating transactions in financial markets. This area is divided into sales, trading, and research. Sales teams act as intermediaries between the bank and institutional clients, providing market insights and executing trades. Traders manage the bank's proprietary positions or execute client orders, often using sophisticated strategies to hedge risks. Research analysts produce reports and recommendations on securities, industries, or macroeconomic trends, which are used internally and shared with clients to inform investment decisions.

Additionally, Asset Management and Wealth Management services may fall under the broader umbrella of investment banking, depending on the bank's organizational structure. These divisions cater to high-net-worth individuals and institutional investors, offering portfolio management, investment advisory, and financial planning services. While these areas may sometimes operate as separate departments, their integration within the investment banking division allows for cross-selling opportunities and a more comprehensive suite of financial solutions for clients.

Lastly, Risk Management and Compliance are integral to the Investment Banking Division, ensuring that all activities adhere to internal policies and external regulations. Risk managers assess and mitigate potential financial and operational risks associated with transactions, while compliance officers monitor adherence to legal and regulatory requirements. These functions are critical in maintaining the bank's reputation and avoiding costly penalties or legal disputes. Together, these divisions within investment banking work synergistically to provide clients with tailored financial solutions while managing the inherent complexities and risks of the global financial markets.

CIS Framework: A Secure Banking Future?

You may want to see also

Explore related products

![]()

Risk Management Departments

The number of departments in a bank can vary widely depending on the bank's size, scope of operations, and strategic focus. However, one critical department that is universally present in banks is the Risk Management Department. This department plays a pivotal role in identifying, assessing, monitoring, and mitigating risks that could impact the bank's financial health, reputation, and compliance with regulatory requirements. Risk management is not a monolithic function; it is often segmented into specialized areas to address different types of risks effectively.

Credit Risk Management is a core component of the Risk Management Department. This team focuses on evaluating the creditworthiness of borrowers and managing the risk of default on loans and other credit facilities. They use sophisticated models and analytics to assess the likelihood of repayment, set credit limits, and monitor portfolios for early signs of distress. Credit risk managers also work closely with the lending departments to ensure that credit policies align with the bank's risk appetite and regulatory guidelines.

Another critical area is Market Risk Management, which deals with risks arising from fluctuations in financial markets, such as interest rates, foreign exchange rates, and commodity prices. Market risk managers use quantitative models to measure and manage the bank's exposure to these risks, ensuring that potential losses are within acceptable limits. They also play a key role in hedging strategies to protect the bank's balance sheet from adverse market movements. This function is particularly vital for banks with significant trading activities or investment portfolios.

Operational Risk Management focuses on risks stemming from internal processes, people, systems, and external events. This includes fraud, cybersecurity threats, process failures, and natural disasters. Operational risk managers implement controls, conduct audits, and develop business continuity plans to minimize the impact of such risks. They also ensure compliance with internal policies and external regulations, working closely with other departments like IT, compliance, and internal audit.

Liquidity Risk Management is another essential function within the Risk Management Department. This team ensures that the bank maintains sufficient liquid assets to meet its short-term obligations, such as customer withdrawals and debt repayments. Liquidity risk managers monitor cash flows, manage funding sources, and develop contingency plans to address liquidity shortages. Their work is critical in maintaining the bank's stability, especially during times of financial stress.

Finally, Regulatory and Compliance Risk Management ensures that the bank adheres to all applicable laws, regulations, and industry standards. This team stays abreast of regulatory changes, conducts risk assessments, and implements policies to prevent legal and compliance breaches. They also coordinate with external regulators and auditors, providing reports and documentation to demonstrate compliance. This function is vital for avoiding penalties, protecting the bank's reputation, and maintaining the trust of stakeholders.

In summary, the Risk Management Department is a multifaceted and indispensable part of a bank's organizational structure. Its specialized teams work collaboratively to safeguard the bank from a wide array of risks, ensuring its long-term sustainability and success. While the exact structure may vary, these functions collectively form the backbone of a robust risk management framework in banking.

Girlsway Bank Statement: Understanding Charges and Discretion on Your Bill

You may want to see also

Explore related products

![]()

Support and Compliance Units

Banks typically operate with a complex structure comprising various departments, each playing a crucial role in ensuring smooth operations, customer satisfaction, and regulatory adherence. Among these, Support and Compliance Units are indispensable, forming the backbone that sustains the bank's integrity, efficiency, and legal conformity. These units are not revenue-generating but are vital for risk management, operational stability, and adherence to laws and regulations. Below is a detailed exploration of these critical functions.

Compliance Department is arguably the most critical unit within the Support and Compliance framework. Its primary responsibility is to ensure the bank adheres to all relevant laws, regulations, and internal policies. Compliance officers monitor regulatory changes, update bank policies, and conduct audits to identify and mitigate risks. They also oversee anti-money laundering (AML) programs, know-your-customer (KYC) procedures, and sanctions screening to prevent illegal activities. This department acts as a safeguard against legal penalties, reputational damage, and financial losses, making it a cornerstone of ethical banking practices.

Internal Audit is another key unit that works closely with compliance but maintains independence to provide objective evaluations. Internal auditors assess the effectiveness of the bank's risk management, control, and governance processes. They conduct systematic reviews of operations, financial reporting, and compliance programs to identify inefficiencies, fraud, or deviations from policies. By providing recommendations for improvement, internal audit ensures operational integrity and supports the bank's long-term sustainability. Their reports are often shared with the board of directors and senior management to drive strategic decision-making.

Risk Management is a support unit focused on identifying, assessing, and mitigating risks that could impact the bank's financial health and operations. This department analyzes credit, market, operational, and liquidity risks, developing strategies to minimize their impact. Risk managers use advanced analytics and modeling tools to forecast potential threats and ensure the bank maintains adequate capital reserves. They also play a crucial role in stress testing and scenario analysis, preparing the bank for economic downturns or unforeseen events. Effective risk management is essential for maintaining stakeholder confidence and regulatory compliance.

Legal and Regulatory Affairs is a specialized unit that handles legal matters and ensures the bank operates within the bounds of the law. This team drafts and reviews contracts, represents the bank in legal disputes, and advises on regulatory interpretations. They also coordinate with external legal counsel and regulatory bodies, acting as a liaison to address inquiries, investigations, or enforcement actions. Additionally, this unit stays updated on legislative changes that could impact banking operations, providing proactive guidance to other departments. Their expertise is vital for navigating complex legal landscapes and protecting the bank's interests.

Administrative and Operational Support units provide the logistical and infrastructural backbone necessary for the bank's daily operations. This includes facilities management, procurement, human resources, and IT support. While not directly involved in compliance, these functions ensure that employees have the tools, environment, and resources needed to perform their roles effectively. For instance, IT support maintains secure and efficient systems, while HR ensures staffing needs are met and employees are trained on compliance requirements. These units are essential for maintaining operational continuity and supporting the bank's overall mission.

In summary, Support and Compliance Units are integral to a bank's structure, providing the framework for ethical operations, risk mitigation, and regulatory adherence. While they may not directly generate revenue, their contributions are invaluable in safeguarding the bank's reputation, financial stability, and long-term success. Understanding these units highlights their interconnected roles in maintaining a robust and compliant banking ecosystem.

John Dillinger's Notorious Bank Robbery Spree

You may want to see also

Frequently asked questions

The number of departments in a bank varies depending on its size and services, but most banks have 8-12 core departments, including Retail Banking, Corporate Banking, Investment Banking, Risk Management, Human Resources, IT, Operations, and Compliance.

No, the number of departments in a bank depends on its size, scope of services, and organizational structure. Smaller banks may have fewer departments, while larger banks often have more specialized units.

The main departments in a commercial bank typically include Retail Banking, Corporate Banking, Loan Processing, Treasury, Risk Management, Operations, IT, and Customer Service.

Yes, large multinational banks or those offering a wide range of services can have more than 20 departments, including specialized units like Wealth Management, International Banking, Audit, Marketing, and Legal.