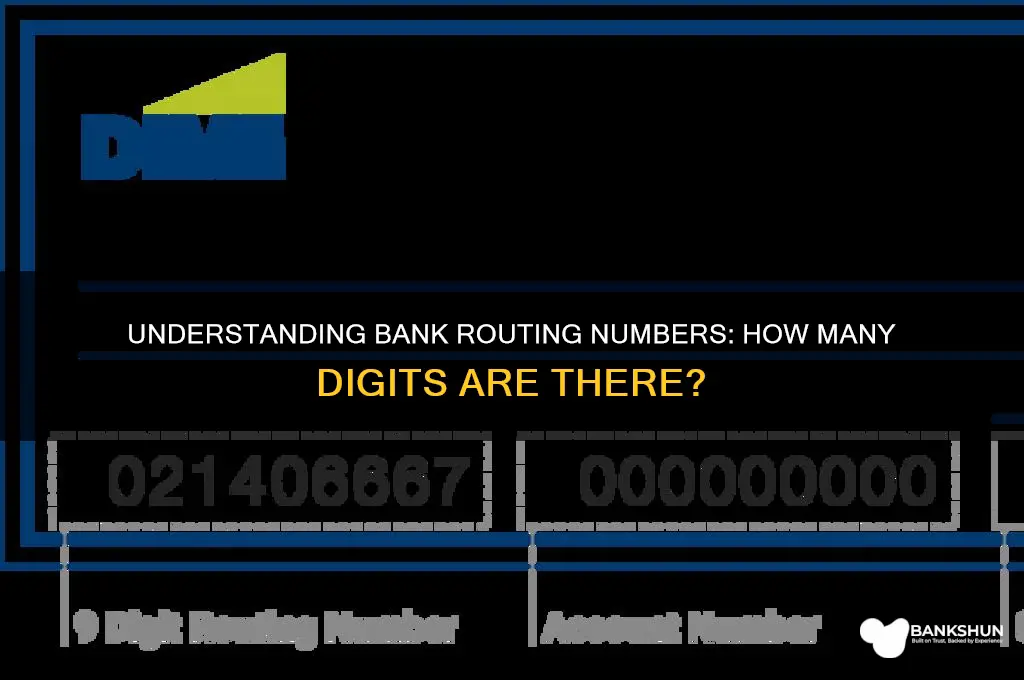

Bank routing numbers, also known as ABA routing transit numbers, are nine-digit codes used in the United States to identify financial institutions in transactions such as direct deposits, wire transfers, and automatic bill payments. These numbers are crucial for ensuring that funds are accurately directed to the correct bank and account. The structure of a routing number is standardized, with the first four digits representing the Federal Reserve routing symbol, the next four identifying the specific bank, and the final digit serving as a checksum to validate the number's accuracy. Understanding the components and purpose of a routing number is essential for anyone involved in financial transactions, as it helps prevent errors and ensures the smooth processing of payments.

| Characteristics | Values |

|---|---|

| Number of Digits in Bank Routing Number | 9 |

| Purpose | Identifies the financial institution in a transaction |

| Format | NNNNNNNNN (9 numeric characters) |

| Check Digit | The last digit is a checksum to validate the routing number |

| Usage | Used for ACH transfers, wire transfers, and check processing |

| Country | Primarily used in the United States |

| Regulation | Governed by the American Bankers Association (ABA) |

| Example | 021000021 (routing number for JPMorgan Chase Bank) |

| Electronic Transactions | Essential for electronic funds transfers |

| Uniqueness | Each financial institution has a unique routing number |

Explore related products

What You'll Learn

- Understanding Bank Routing Numbers: Definition, purpose, and structure of routing numbers in banking systems

- Routing Number Length: Standard number of digits in a bank routing number

- Domestic vs. International: Differences in routing numbers for domestic and international transactions

- Routing Number Components: Breakdown of the sections within a bank routing number

- Finding Your Routing Number: Methods to locate your bank’s routing number easily

![]()

Understanding Bank Routing Numbers: Definition, purpose, and structure of routing numbers in banking systems

Understanding Bank Routing Numbers: Definition, Purpose, and Structure

A bank routing number, also known as an ABA (American Bankers Association) routing transit number, is a unique nine-digit code assigned to financial institutions in the United States. This number serves as an identifier for banks, credit unions, and other financial entities during transactions. Its primary purpose is to ensure that funds are accurately directed to the correct institution during domestic transfers, such as wire transfers, direct deposits, and electronic payments. Without a routing number, the banking system would lack the precision needed to process millions of transactions daily.

The Purpose of Routing Numbers in Banking Systems

Routing numbers play a critical role in the efficiency and security of the banking system. They are essential for automating transactions, reducing errors, and preventing fraud. For instance, when an employer initiates a direct deposit, the routing number ensures the funds reach the employee’s bank account seamlessly. Similarly, during ACH (Automated Clearing House) transactions, such as bill payments or transfers between accounts, the routing number acts as a digital address, guiding the flow of money. In essence, it is the backbone of interbank communication, enabling smooth and reliable financial operations.

The Structure of Routing Numbers

A bank routing number consists of nine digits, each serving a specific purpose. The first four digits represent the Federal Reserve routing symbol, identifying the Federal Reserve Bank associated with the financial institution. The next four digits denote the ABA institution identifier, which uniquely identifies the bank or credit union. The final digit, known as the check digit, is a security measure calculated using a specific algorithm to validate the authenticity of the routing number. This structured format ensures uniformity and accuracy across all transactions, regardless of the institution involved.

How Routing Numbers Differ from Account Numbers

While routing numbers identify the financial institution, account numbers specify the individual account within that institution. Together, these two pieces of information enable precise transaction processing. For example, when setting up a direct deposit, both the routing number and account number are required to ensure funds are credited to the correct account. It’s important to note that routing numbers are public information, whereas account numbers are private and should be safeguarded to prevent unauthorized access.

Importance of Verifying Routing Numbers

Given the critical role of routing numbers in transaction processing, accuracy is paramount. Errors in entering the routing number can result in delayed or failed transactions, causing inconvenience and potential financial losses. To avoid such issues, individuals and businesses should always verify the routing number with their bank or through official sources. Many financial institutions provide this information on their websites, statements, or mobile apps. Additionally, tools like the Federal Reserve’s database can be used to confirm the validity of a routing number, ensuring transactions proceed without hiccups.

In summary, understanding bank routing numbers—their definition, purpose, and structure—is essential for anyone engaged in financial transactions. With nine digits that serve as a unique identifier, routing numbers streamline the banking process, ensuring funds are accurately and securely transferred between institutions. By grasping their significance and verifying their accuracy, individuals and businesses can navigate the banking system with confidence and efficiency.

Huntington Bank's Customer Base: Unveiling the Number of Account Holders

You may want to see also

Explore related products

![]()

Routing Number Length: Standard number of digits in a bank routing number

A bank routing number, also known as an ABA (American Bankers Association) routing transit number, is a crucial component of the U.S. banking system. It serves as a unique identifier for financial institutions, enabling the smooth processing of transactions such as direct deposits, wire transfers, and automatic bill payments. When discussing the Routing Number Length: Standard number of digits in a bank routing number, it is essential to understand that this number typically consists of 9 digits. This standardized length ensures consistency across all U.S. banks and credit unions, facilitating seamless communication between financial entities.

The 9-digit structure of a routing number is not arbitrary but follows a specific format designed by the ABA. The first four digits represent the Federal Reserve routing symbol, which identifies the Federal Reserve Bank associated with the financial institution. The next four digits denote the ABA institution identifier, unique to each bank or credit union. The final digit, known as the check digit, is used to validate the authenticity of the routing number through a mathematical algorithm. This standardized format ensures that routing numbers are both unique and verifiable, reducing the risk of errors in financial transactions.

Understanding the Routing Number Length: Standard number of digits in a bank routing number is particularly important for individuals and businesses conducting electronic transactions. For instance, when setting up direct deposits or automatic payments, the correct 9-digit routing number must be provided to ensure funds are directed to the right institution. Mistakes in entering the routing number can lead to delays, failed transactions, or even funds being sent to the wrong account. Thus, verifying the accuracy of the 9-digit routing number is a critical step in any financial transaction.

It is worth noting that while the standard routing number length is 9 digits, there are exceptions in specific contexts. For example, wire transfers may use an 8-digit routing number, with the first digit often being dropped for this purpose. However, these exceptions are limited and do not alter the general rule that a bank routing number is typically 9 digits long. Financial institutions and consumers alike must remain aware of these nuances to avoid confusion and ensure transactions are processed correctly.

In summary, the Routing Number Length: Standard number of digits in a bank routing number is 9 digits, following a structured format that includes a Federal Reserve routing symbol, an ABA institution identifier, and a check digit. This standardization is vital for the efficient and secure processing of financial transactions in the U.S. banking system. Whether for personal or business use, understanding and correctly utilizing the 9-digit routing number is essential for successful electronic banking operations. Always double-check the routing number to avoid errors and ensure smooth transaction processing.

Agent Cody Banks: Family-Friendly Fun?

You may want to see also

Explore related products

![]()

Domestic vs. International: Differences in routing numbers for domestic and international transactions

Bank routing numbers play a crucial role in identifying financial institutions during transactions, but their structure and usage differ significantly between domestic and international payments. Domestically, in the United States, a routing number consists of 9 digits, serving as a unique identifier for banks and credit unions. This number is essential for processing transactions such as direct deposits, wire transfers, and automatic bill payments within the country. It ensures that funds are directed to the correct institution and account efficiently. For domestic transactions, the routing number is standardized and works seamlessly within the Automated Clearing House (ACH) network and other domestic payment systems.

In contrast, international transactions do not rely on domestic routing numbers. Instead, they use SWIFT codes (Society for Worldwide Interbank Financial Telecommunication) or BIC codes (Bank Identifier Code), which are globally recognized identifiers. SWIFT codes are typically 8 to 11 characters long and include a combination of letters and numbers. These codes are designed to facilitate cross-border payments by identifying the specific bank and country involved in the transaction. Unlike domestic routing numbers, SWIFT codes are not standardized by length but follow a specific format to ensure global compatibility.

Another key difference lies in the purpose and scope of these identifiers. Domestic routing numbers are tailored for use within a single country’s financial system, focusing on efficiency and accuracy for local transactions. International transactions, however, require a more complex system due to the involvement of multiple currencies, regulatory frameworks, and banking systems. SWIFT codes not only identify the bank but also help in navigating the intricacies of international finance, including currency exchange and compliance with global regulations.

Additionally, the infrastructure supporting these numbers varies. Domestic routing numbers operate within a country’s centralized banking network, such as the Federal Reserve in the U.S., which oversees their issuance and maintenance. International transactions, on the other hand, rely on a decentralized global network managed by SWIFT, which connects over 11,000 financial institutions worldwide. This global network ensures that international payments are processed securely and accurately, despite the absence of a unified routing system like the one used domestically.

Lastly, while domestic routing numbers are often used alongside account numbers for direct transactions, international payments may require additional information, such as IBAN (International Bank Account Number) codes, depending on the destination country. This highlights the increased complexity of international transactions compared to domestic ones. Understanding these differences is essential for individuals and businesses to ensure smooth and error-free financial transactions, whether they are local or cross-border.

Personal Banker: Degree Needed or Not?

You may want to see also

Explore related products

![]()

Routing Number Components: Breakdown of the sections within a bank routing number

A bank routing number, also known as an ABA routing transit number (RTN), is a nine-digit code used in the United States to identify financial institutions in transactions such as ACH transfers, wire transfers, and check processing. Understanding the components of this number is essential for ensuring accurate and secure financial transactions. The routing number is divided into three main sections, each serving a specific purpose in identifying the bank and its location.

The first section of the routing number consists of the first four digits, which represent the Federal Reserve Routing Symbol. This part of the code is used to identify the Federal Reserve Bank district and the specific Federal Reserve Bank within that district. For instance, the first two digits correspond to the Federal Reserve Bank district, while the next two digits pinpoint the exact Federal Reserve Bank within that district. This segment is crucial for directing transactions to the correct geographical area and ensuring that funds are processed through the appropriate Federal Reserve Bank.

The second section comprises the next four digits, known as the ABA Institution Identifier. This segment uniquely identifies the specific bank or financial institution within the Federal Reserve district. Each bank is assigned a distinct set of numbers in this section, allowing for precise identification during transactions. This part of the routing number is particularly important for differentiating between banks that may have similar names or operate in the same region, ensuring that funds are routed to the correct institution.

The final section of the routing number is a single check digit, which serves as a security measure to verify the authenticity of the entire routing number. This digit is calculated using a specific algorithm that takes into account the first eight digits of the routing number. The purpose of the check digit is to detect errors in the routing number, such as typos or transpositions, by ensuring that the number passes a validity check. If the check digit does not match the calculated value, the transaction may be flagged or rejected, preventing potential fraud or misrouting of funds.

In summary, the nine-digit bank routing number is a carefully structured code that plays a vital role in the U.S. banking system. Its three main components—the Federal Reserve Routing Symbol, the ABA Institution Identifier, and the check digit—work together to ensure that financial transactions are accurately directed to the correct bank and location. Understanding these components not only helps in processing transactions efficiently but also enhances security by minimizing errors and preventing fraudulent activities. By breaking down the routing number into its sections, individuals and businesses can better navigate the complexities of electronic and paper-based financial transactions.

Can You Use Apple Pay at U.S. Bank ATMs?

You may want to see also

Explore related products

![]()

Finding Your Routing Number: Methods to locate your bank’s routing number easily

A bank routing number, also known as an ABA routing transit number (RTN), is a nine-digit code used in the United States to identify the financial institution involved in a transaction. This unique number is crucial for various banking activities, such as setting up direct deposits, transferring funds, or processing checks. Understanding how to locate your bank’s routing number is essential for managing your finances efficiently. Here are several straightforward methods to find your bank’s routing number easily.

One of the simplest ways to find your bank’s routing number is by checking your personal checks. If you have a checkbook, the routing number is typically printed on the bottom left corner. It is the first set of nine digits, followed by your account number and the check number. This method is quick and reliable, as the routing number is clearly labeled and easy to identify. If you don’t have physical checks, many banks provide digital check images through their online banking platforms, where you can also locate the routing number.

Another convenient method is to log in to your bank’s online banking portal or mobile app. Most banks display the routing number in the account summary or settings section. Look for tabs labeled “Account Information,” “Direct Deposit,” or “Wire Transfers,” as these sections often include the routing number. If you’re unsure where to find it, use the search function within the app or website by typing “routing number” to locate the relevant page. This digital approach is especially useful for those who prefer managing their finances online.

If you prefer a more direct approach, contact your bank’s customer service. You can call the number on the back of your debit or credit card, visit a local branch, or use the bank’s live chat feature on their website. Customer service representatives can quickly provide your bank’s routing number after verifying your identity. This method ensures accuracy and is ideal if you’re unsure about the information you’ve found through other means.

Lastly, your bank’s official website is a valuable resource. Visit the website and navigate to the “Help” or “FAQ” section, where you’ll often find a page dedicated to routing numbers. Some banks even provide a search tool where you can input your state or branch location to retrieve the correct routing number. Additionally, the Federal Reserve’s official website offers a Routing Number search tool, which can be used to verify the routing number associated with your bank.

In summary, finding your bank’s routing number is a straightforward process with multiple options available. Whether you check your personal checks, use online banking, contact customer service, or visit your bank’s website, each method ensures you can locate the nine-digit code efficiently. Knowing where and how to find your routing number simplifies various financial transactions and helps you manage your accounts with ease.

The 2008 Banking Crisis: Duration and Global Economic Impact

You may want to see also

Frequently asked questions

A bank routing number consists of 9 digits.

The 9-digit format is standardized by the American Bankers Association (ABA) to uniquely identify financial institutions in the United States.

No, a valid bank routing number always contains exactly 9 digits.

No, the 9-digit routing number is specific to the United States. Other countries use different systems and formats for identifying banks.