Overdraft fees are a common concern for bank account holders, as they can quickly add up and impact one's financial well-being. These fees are charged when a transaction exceeds the available balance in an account, essentially allowing the account to go into a negative balance. The frequency of overdraft fees varies depending on the bank's policies, the type of account, and the account holder's spending habits. Some banks charge overdraft fees for each transaction that overdraws the account, while others may limit the number of fees per day or month. Understanding how often banks charge overdraft fees is crucial for account holders to manage their finances effectively, avoid unnecessary charges, and maintain a healthy relationship with their financial institution.

| Characteristics | Values |

|---|---|

| Frequency of Overdraft Fees | Typically charged daily, but varies by bank. |

| Daily Overdraft Fee | Common practice; some banks charge $5-$15 per day after a grace period. |

| Grace Period | Many banks offer a grace period (e.g., $5 or 24-48 hours) before fees. |

| Maximum Daily Fees | Some banks cap daily fees (e.g., $36 per day or $125 per day). |

| Monthly Overdraft Fee Limit | Some banks limit monthly fees (e.g., $100-$200 per month). |

| Overdraft Fee Amount | Typically $35-$36 per transaction or per day, depending on the bank. |

| Extended Overdraft Fees | Additional fees if the account remains overdrawn for multiple days. |

| Fee Waivers | Some banks waive fees for accounts with direct deposits or minimum balances. |

| Overdraft Protection Plans | Optional services to avoid fees (e.g., linking to savings or credit line). |

| Regulations | Banks must obtain customer opt-in for overdraft coverage on debit/ATM transactions. |

| Fee Transparency | Banks are required to disclose fees clearly in account agreements. |

| Online and Mobile Alerts | Many banks offer real-time alerts to notify customers of low balances. |

| Fee-Free Banks | Some online banks (e.g., Chime, Ally) do not charge overdraft fees. |

| Trend | Increasing pressure on banks to reduce or eliminate overdraft fees. |

Explore related products

What You'll Learn

- Daily vs. Monthly Fees: Banks may charge overdraft fees daily or monthly, depending on their policies

- Fee Caps and Limits: Some banks limit the number of overdraft fees they charge per day or month

- Transaction Types: Fees can vary based on transaction type (e.g., ATM, debit card, checks)

- Overdraft Protection Plans: Optional services to avoid fees by linking accounts or lines of credit

- Fee Amounts by Bank: Overdraft fees differ by bank, typically ranging from $25 to $35 per occurrence

![]()

Daily vs. Monthly Fees: Banks may charge overdraft fees daily or monthly, depending on their policies

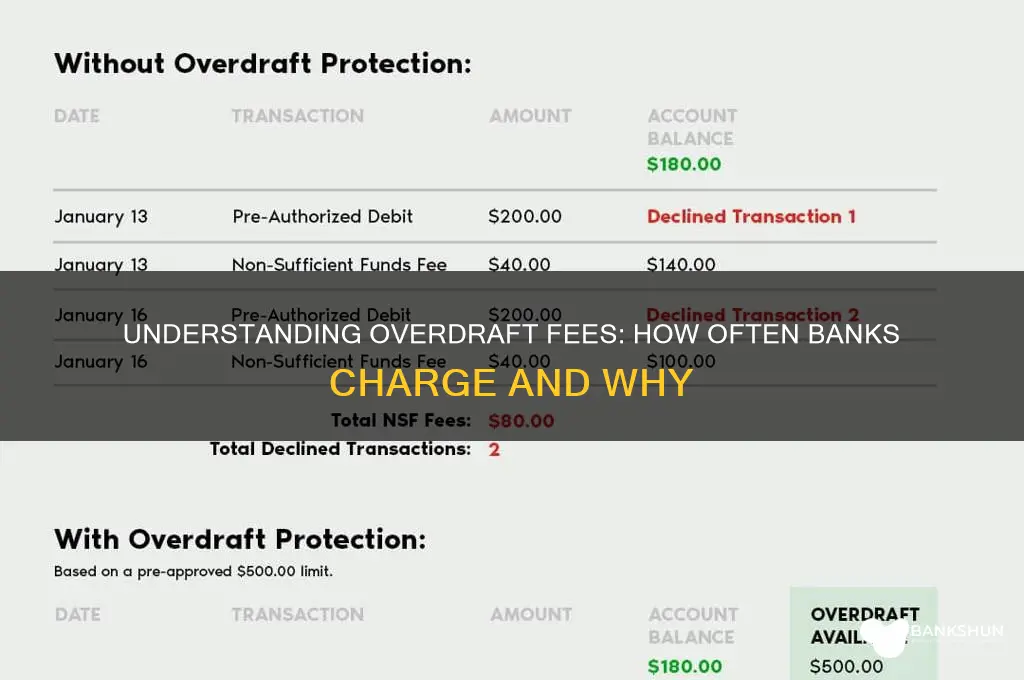

When it comes to overdraft fees, one of the critical distinctions is whether banks charge these fees daily or monthly. This difference can significantly impact the total amount a customer pays if their account remains overdrawn. Daily overdraft fees are applied each day the account stays in a negative balance. For example, if a bank charges a $5 daily fee and the account is overdrawn for 10 days, the total fee would be $50. This structure can quickly escalate costs, especially if the account holder is unaware or unable to rectify the overdrawn balance promptly. On the other hand, monthly overdraft fees are charged as a flat rate for the entire period the account is overdrawn, regardless of the number of days. For instance, a bank might charge a $35 monthly fee, which remains the same whether the account is overdrawn for one day or 30 days. This approach provides more predictability but can still be costly if the overdraft persists.

Understanding whether a bank employs daily or monthly fees is essential for account holders to manage their finances effectively. Daily fees are particularly punitive for those who cannot immediately resolve their overdrawn status, as the charges accumulate rapidly. For instance, someone who overdraws their account by a small amount but cannot cover it for several days may face fees that far exceed the initial overdraft. Conversely, monthly fees offer a capped cost, which can be advantageous for those who need more time to address their balance. However, this structure may incentivize customers to delay resolving the overdraft, as the fee does not increase with time. Both models highlight the importance of monitoring account balances and understanding a bank’s specific overdraft policies.

Banks often disclose their overdraft fee structures in their account agreements, but these details can be buried in fine print. Customers should proactively review these terms to determine if their bank charges daily or monthly fees. Additionally, some banks may combine both approaches, charging a daily fee up to a certain cap or switching to a monthly fee after a specific number of days. For example, a bank might charge $5 daily for the first five days and then impose a $35 monthly fee if the overdraft continues. Such hybrid models add complexity but can sometimes mitigate the harshest financial consequences for customers.

The frequency of overdraft fees also influences how customers should respond to an overdrawn account. With daily fees, the priority is to resolve the negative balance as quickly as possible to minimize accumulating charges. This might involve transferring funds from another account, depositing cash, or contacting the bank to discuss options. For monthly fees, while prompt action is still advisable, customers have more flexibility to plan how they will cover the overdraft without facing escalating costs. In either case, being aware of the fee structure allows account holders to make informed decisions and avoid unnecessary financial strain.

Lastly, it’s worth noting that some banks offer overdraft protection services or grace periods to help customers avoid fees altogether. These services may link a savings account or credit card to cover overdrafts or provide a short window to bring the account back into balance without penalties. However, such protections are not universal, and their availability depends on the bank’s policies. Whether facing daily or monthly fees, customers should explore all options to prevent overdrafts and understand the specific rules governing their accounts. By doing so, they can better navigate the potential pitfalls of overdraft charges and maintain healthier financial habits.

Do Banks Dispense Rare $500 Bills?

You may want to see also

Explore related products

![]()

Fee Caps and Limits: Some banks limit the number of overdraft fees they charge per day or month

Banks often impose overdraft fees when an account holder spends more than their available balance, but the frequency and structure of these charges can vary widely. One important aspect to consider is the implementation of fee caps and limits, which some banks use to restrict the number of overdraft fees they charge per day or month. These limits are designed to protect consumers from excessive fees and provide a degree of financial predictability. For example, a bank might cap overdraft fees at three per day, meaning that even if multiple transactions trigger overdrafts, the account holder will not be charged more than three times in a single day.

Fee caps can differ significantly between banks, making it essential for account holders to review their bank’s specific policies. Some institutions may limit overdraft fees to a certain number per month rather than per day, such as ten fees per month. This monthly cap can be particularly beneficial for individuals who occasionally overdraft but want to avoid accumulating fees over time. Additionally, a few banks may combine daily and monthly limits, offering a layered protection system. For instance, they might cap fees at three per day and ten per month, ensuring that customers are not penalized excessively in either the short or long term.

It’s also worth noting that some banks may waive overdraft fees entirely under certain conditions, such as if the overdraft amount is small or if the account is brought back into balance within a specified timeframe. However, fee caps remain a more common and structured approach to limiting charges. Account holders should be aware that not all banks impose these limits, and those that do may still charge other fees, such as extended overdraft fees or return item fees, which are not always subject to the same caps. Understanding these distinctions is crucial for managing overdraft costs effectively.

To take advantage of fee caps, customers should familiarize themselves with their bank’s overdraft policies, often found in account disclosures or online banking portals. Some banks may also allow customers to opt out of overdraft protection altogether, preventing overdraft fees but potentially leading to declined transactions. By comparing fee structures across different banks, individuals can choose an account that aligns with their financial habits and minimizes the risk of excessive charges. Proactive management of account balances and regular monitoring of transactions can further reduce the likelihood of triggering overdraft fees, even when caps are in place.

In summary, fee caps and limits are a critical component of how banks charge overdraft fees, offering a safeguard against repeated penalties. While these limits vary by institution, they generally restrict the number of fees charged per day or month, providing customers with greater financial stability. By understanding and leveraging these policies, account holders can better navigate their banking relationships and avoid unnecessary costs. Always review your bank’s specific rules and consider alternatives, such as opting out of overdraft protection or choosing a bank with more lenient fee structures, to maintain control over your finances.

Navigating Banking Challenges for Industrial Hemp Dealers: Strategies and Solutions

You may want to see also

Explore related products

![]()

Transaction Types: Fees can vary based on transaction type (e.g., ATM, debit card, checks)

Banks often charge overdraft fees when an account holder spends more money than is available in their account, but the frequency and amount of these fees can vary significantly based on the transaction type. Understanding how different transactions trigger overdraft fees is crucial for managing your finances effectively. Here’s a detailed breakdown of how fees can differ based on transaction types such as ATM withdrawals, debit card purchases, and checks.

ATM Transactions: When you withdraw cash from an ATM and your account balance is insufficient, banks may charge an overdraft fee. However, some banks offer overdraft protection specifically for ATM transactions, allowing you to link a savings account or credit card to cover the shortfall instead of incurring a fee. It’s important to check your bank’s policy, as some institutions may limit the number of ATM overdrafts allowed per day or month. Additionally, repeated ATM overdrafts can lead to higher fees or account restrictions.

Debit Card Purchases: Overdraft fees from debit card transactions are among the most common. When you swipe or insert your debit card for a purchase that exceeds your available balance, the bank may approve the transaction but charge an overdraft fee. Some banks allow customers to opt out of this service, meaning the transaction would be declined instead of incurring a fee. However, opting in can be risky, as multiple small purchases can trigger multiple overdraft fees in a single day, quickly adding up.

Check Transactions: Writing a check that exceeds your account balance can also result in an overdraft fee. Unlike debit card transactions, checks may take longer to process, so it’s easier to lose track of your balance. Banks typically charge a single overdraft fee per check, but if multiple checks are processed on the same day, each one could incur a separate fee. Some banks offer overdraft protection for checks by transferring funds from a linked account, but this often comes with a transfer fee that is lower than the overdraft fee.

Online and Mobile Payments: With the rise of digital banking, overdraft fees can also apply to online and mobile payments, such as bill payments or peer-to-peer transfers. These transactions are treated similarly to debit card purchases, and the same overdraft policies apply. It’s essential to monitor your account balance closely when making digital payments, as real-time updates may not always reflect pending transactions.

In summary, overdraft fees are not one-size-fits-all; they vary based on the transaction type. ATM withdrawals, debit card purchases, checks, and digital payments each have unique rules and potential fees. To minimize overdraft charges, consider opting out of overdraft coverage for debit card transactions, linking a savings account for protection, and regularly monitoring your account balance. Being proactive and understanding your bank’s policies can help you avoid unnecessary fees and maintain better financial health.

Haven Savings Bank Springfield Avenue Summit NJ: Your Local Financial Partner

You may want to see also

![]()

Overdraft Protection Plans: Optional services to avoid fees by linking accounts or lines of credit

Overdraft fees can be a significant source of frustration for bank customers, as they are often charged frequently and can add up quickly. Banks typically charge overdraft fees when an account holder spends more than their available balance, and these fees can range from $25 to $35 per transaction. According to a 2021 report by the Consumer Financial Protection Bureau (CFPB), banks can charge overdraft fees multiple times a day, often processing transactions from largest to smallest to maximize the number of fees. This practice can result in customers paying hundreds of dollars in fees for a single day of overdrafts. To avoid these costly charges, many banks offer Overdraft Protection Plans, which are optional services designed to prevent overdraft fees by linking accounts or lines of credit.

Overdraft Protection Plans work by automatically transferring funds from a linked account, such as a savings account or a line of credit, to cover transactions that would otherwise result in an overdraft. For example, if a customer has a checking account with a low balance and makes a purchase that exceeds their available funds, the bank will transfer money from their linked savings account to cover the transaction. This transfer typically incurs a lower fee, often around $10 to $12, compared to the standard overdraft fee. By enrolling in an Overdraft Protection Plan, customers can save money and avoid the stress of unexpected fees. It is essential to review the terms and conditions of these plans, as some banks may limit the number of transfers or charge additional fees for certain types of transactions.

When considering an Overdraft Protection Plan, customers should evaluate their banking habits and choose a plan that aligns with their needs. Some banks offer multiple options, such as linking to a savings account, a credit card, or a personal line of credit. Linking to a savings account is often the most cost-effective choice, as it usually involves the lowest fees. However, customers should ensure they maintain a sufficient balance in their savings account to avoid depleting their emergency funds. Alternatively, linking to a line of credit can provide a larger cushion but may involve higher interest rates and fees. It is crucial to compare the costs and benefits of each option to determine the most suitable plan.

Another important aspect of Overdraft Protection Plans is understanding the bank’s transaction processing order. Some banks prioritize transactions in a way that maximizes overdraft fees, even when an Overdraft Protection Plan is in place. Customers should inquire about their bank’s policies and consider switching to a bank that processes transactions chronologically or in a more consumer-friendly manner. Additionally, monitoring account activity regularly can help customers avoid overdrafts altogether. Many banks offer mobile apps and alerts that notify customers when their balance is low, allowing them to take proactive steps to prevent overdrafts.

Enrolling in an Overdraft Protection Plan is a straightforward process that can typically be completed online, through a mobile app, or by visiting a bank branch. Customers will need to provide information about the accounts or lines of credit they wish to link and review the associated fees and terms. Some banks may require a minimum balance or credit score to qualify for certain plans, so it is essential to check eligibility requirements. Once enrolled, customers can enjoy peace of mind knowing that their transactions are protected, and they are less likely to incur costly overdraft fees. By taking advantage of these optional services, bank customers can better manage their finances and avoid unnecessary charges.

EastWest Bank Philippines: Zelle Availability and Alternative Options

You may want to see also

![]()

Fee Amounts by Bank: Overdraft fees differ by bank, typically ranging from $25 to $35 per occurrence

Overdraft fees are a common concern for bank customers, and understanding how these charges vary across different financial institutions is essential for managing personal finances effectively. When it comes to Fee Amounts by Bank, there is a noticeable difference in the overdraft fees imposed by various banks. Typically, these fees fall within a specific range, providing customers with a general idea of what to expect. The standard overdraft fee charged by banks usually ranges from $25 to $35 for each instance of overdraft. This means that if a customer's account goes into the negative, they can anticipate a charge within this range, depending on their bank's policy.

The variation in overdraft fees can be attributed to the different strategies and policies adopted by banks. Some banks may opt for a slightly lower fee to attract customers, while others might charge towards the higher end of the spectrum. For instance, Bank of America is known to charge $35 for each overdraft transaction, which is on the higher side of the typical range. In contrast, some regional or community banks might offer a more competitive rate, charging closer to $25 for the same service. These differences highlight the importance of researching and comparing bank fees when choosing a financial institution.

It's worth noting that the frequency of overdraft fees is directly related to the fee amount. Banks often have daily or per-item limits on overdraft charges. For example, a bank might charge the overdraft fee for each transaction that exceeds the available balance, up to a certain daily limit. This means that multiple overdraft occurrences in a single day could result in multiple fees, quickly adding up to a substantial amount. Understanding these limits is crucial for customers to avoid excessive charges.

Customers should also be aware that some banks offer overdraft protection services, which can help mitigate these fees. Overdraft protection may involve linking a savings account or a line of credit to the checking account, ensuring that transactions are covered even if the primary account balance is insufficient. While this service might come with its own set of fees, it can be a valuable tool for those who frequently encounter overdraft situations. By opting for overdraft protection, customers can potentially save money compared to the standard overdraft fees.

In summary, when considering Fee Amounts by Bank, it is clear that overdraft fees are not standardized across the banking industry. The range of $25 to $35 per occurrence is a general guideline, but individual bank policies can result in significant variations. Customers should carefully review their bank's fee schedule and consider their spending habits to make informed decisions. Being mindful of these fees and exploring alternatives like overdraft protection can help individuals better manage their finances and avoid unnecessary charges.

Banking Crisis Update: Tracking Collapsed Institutions This Month

You may want to see also

Frequently asked questions

Banks can charge overdraft fees multiple times per day, depending on the number of transactions that exceed your available balance. There is typically no limit to how many fees they can assess in a single day.

Most banks do not have a daily limit on overdraft fees, but some may cap the number of fees per day (e.g., 4-6 fees). Policies vary by bank, so check your account agreement for specifics.

Overdraft fees are usually a one-time charge per transaction, but banks may impose additional fees (e.g., extended overdraft fees) if your account remains negative for several days, often after 5 or more consecutive days.