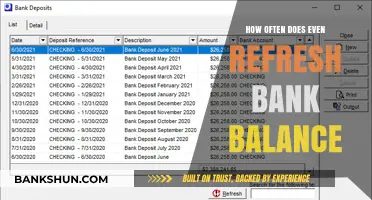

Bank reconciliations are a critical process for maintaining accurate financial records and ensuring the integrity of a company's cash position. The frequency at which bank reconciliations should be prepared depends on the volume of transactions, the complexity of the business, and regulatory requirements. For most businesses, monthly reconciliations are standard, as they align with the typical accounting cycle and provide timely detection of discrepancies, errors, or fraudulent activities. However, high-volume or high-risk businesses may benefit from more frequent reconciliations, such as weekly or even daily, to minimize the risk of financial misstatements and maintain tighter control over cash flow. Ultimately, the goal is to strike a balance between operational efficiency and financial accuracy, ensuring that bank reconciliations are performed often enough to safeguard assets and support informed decision-making.

Explore related products

What You'll Learn

![]()

Monthly Reconciliation Benefits

Monthly bank reconciliations offer a multitude of benefits that contribute to the financial health and operational efficiency of any business. One of the primary advantages is the early detection of errors and discrepancies. By reconciling accounts on a monthly basis, businesses can quickly identify and rectify issues such as unauthorized transactions, bank errors, or internal accounting mistakes. This proactive approach minimizes the risk of financial losses and ensures that discrepancies do not compound over time, which can be more challenging and costly to resolve if left unattended for longer periods.

Another significant benefit of monthly reconciliations is the enhancement of cash flow management. Regularly reviewing bank statements against internal records provides a clear and up-to-date picture of the company's cash position. This visibility allows businesses to make informed decisions about expenditures, investments, and budgeting. For instance, identifying unrecorded deposits or outstanding checks can help optimize liquidity and avoid unnecessary overdraft fees or missed payment deadlines. Effective cash flow management is critical for maintaining financial stability and supporting growth initiatives.

Monthly reconciliations also strengthen internal controls and reduce fraud risks. The consistent review of bank transactions acts as a deterrent to fraudulent activities, as irregularities are more likely to be caught promptly. Additionally, the process reinforces accountability within the finance team, ensuring that all transactions are properly authorized, recorded, and reconciled. This systematic approach not only safeguards assets but also fosters a culture of transparency and compliance, which is essential for building trust with stakeholders, including investors and auditors.

Furthermore, compliance with regulatory and accounting standards is facilitated through monthly reconciliations. Many financial regulations and accounting principles require businesses to maintain accurate and timely financial records. By reconciling bank accounts monthly, companies can ensure they meet these obligations, reducing the risk of penalties, audits, or legal issues. Accurate financial reporting also enhances credibility with external parties, such as lenders or partners, who rely on reliable financial data to assess the business's performance and reliability.

Lastly, monthly reconciliations support better financial planning and forecasting. With a consistent and accurate understanding of the company's financial position, businesses can create more reliable budgets, forecasts, and strategic plans. This is particularly important in dynamic business environments where financial conditions can change rapidly. Regular reconciliations provide the data needed to identify trends, anticipate challenges, and capitalize on opportunities, ultimately driving informed decision-making and long-term success. In summary, the practice of monthly bank reconciliations is a cornerstone of sound financial management, offering immediate and long-term benefits that extend beyond mere record-keeping.

Who Owns FaZe? Banks' Role Explained

You may want to see also

Explore related products

![]()

Quarterly vs. Monthly Frequency

When deciding between quarterly vs. monthly frequency for bank reconciliations, it’s essential to weigh the benefits and drawbacks of each approach. Monthly reconciliations are widely recommended as a best practice because they provide timely detection of discrepancies, errors, or fraudulent activities. By reconciling accounts every month, businesses can ensure that their financial records align with bank statements, reducing the risk of accumulated errors over time. This frequency also supports better cash flow management, as it allows for immediate identification and correction of issues such as missed transactions, incorrect postings, or unauthorized activities. For small businesses or organizations with high transaction volumes, monthly reconciliations are particularly crucial to maintain accuracy and financial integrity.

On the other hand, quarterly reconciliations may seem less burdensome and time-consuming, but they come with significant risks. Waiting three months to reconcile accounts can lead to a backlog of discrepancies, making it harder to pinpoint and resolve issues promptly. Errors or fraudulent activities may go unnoticed for extended periods, potentially causing financial losses or compliance issues. Quarterly reconciliations are generally only suitable for businesses with minimal transaction activity or those operating in highly controlled environments where the risk of errors is low. However, even in such cases, the lack of timely oversight can still pose challenges, especially if unexpected discrepancies arise.

A key consideration in the quarterly vs. monthly debate is the impact on financial reporting and decision-making. Monthly reconciliations ensure that financial statements are accurate and up-to-date, providing stakeholders with reliable information for strategic planning. In contrast, quarterly reconciliations may result in outdated or incomplete financial data, which can hinder effective decision-making. For businesses that rely on real-time financial insights, monthly reconciliations are the more prudent choice, as they align with the need for current and accurate financial information.

Another factor to consider is regulatory and compliance requirements. Many industries and accounting standards mandate more frequent reconciliations to ensure transparency and accountability. For instance, publicly traded companies or organizations subject to audits may be required to perform monthly reconciliations to meet regulatory obligations. In such cases, opting for quarterly reconciliations could lead to non-compliance and potential penalties. Therefore, businesses must evaluate their specific regulatory environment before choosing a reconciliation frequency.

In conclusion, while quarterly reconciliations may offer convenience and reduced administrative burden, monthly reconciliations are generally the more effective and reliable approach. The benefits of timely error detection, accurate financial reporting, and compliance with regulatory requirements far outweigh the effort involved in monthly reconciliations. Businesses should carefully assess their transaction volume, risk exposure, and operational needs to determine the most appropriate frequency. For most organizations, monthly reconciliations remain the gold standard for maintaining financial accuracy and integrity.

Banks' CTR Filing: Do They Inform Customers?

You may want to see also

Explore related products

![]()

Daily Transaction Monitoring

The first step in daily transaction monitoring is establishing a systematic process to access and review bank statements or online banking platforms each day. This includes verifying deposits, withdrawals, transfers, and any fees or charges. Automated tools or software can streamline this process by flagging unusual or unexpected transactions for further investigation. For example, a sudden large withdrawal or a transaction from an unrecognized source should be immediately scrutinized to determine its legitimacy. This proactive approach helps prevent fraud and ensures that any discrepancies are addressed before they escalate.

Another key aspect of daily transaction monitoring is reconciling transactions with internal accounting records in real-time or near real-time. This involves cross-referencing bank transactions with the company’s general ledger, accounts payable, and accounts receivable systems. By doing this daily, businesses can quickly identify missing entries, duplicate payments, or posting errors. For instance, if a payment is recorded in the accounting system but not reflected in the bank statement, it could indicate a processing delay or an error that needs immediate correction. Timely reconciliation minimizes the accumulation of unresolved issues, making full bank reconciliations less cumbersome.

Daily monitoring also plays a vital role in cash flow management. By tracking transactions daily, businesses gain visibility into their cash position, enabling better decision-making regarding payments, investments, or funding needs. For organizations with high transaction volumes or tight cash flow margins, this level of oversight is indispensable. It ensures that funds are available for critical operations and helps avoid overdrafts or penalties associated with insufficient funds. Additionally, daily monitoring supports compliance with internal policies and external regulations, as it provides a continuous audit trail of financial activities.

Finally, daily transaction monitoring fosters accountability and transparency within the finance team. Assigning specific responsibilities for reviewing and approving transactions ensures that no activity goes unnoticed. Regular communication between team members about unusual findings or trends can further enhance the effectiveness of this process. For organizations that perform full bank reconciliations monthly or quarterly, daily monitoring acts as a safeguard, reducing the likelihood of significant discrepancies during the formal reconciliation process. In essence, while the frequency of full bank reconciliations may depend on organizational needs, daily transaction monitoring is a non-negotiable practice for maintaining financial integrity and operational efficiency.

Nico Walker's Bank Heists: Uncovering the True Robbery Count

You may want to see also

Explore related products

![]()

Annual Reconciliation Risks

Bank reconciliations are a critical process for maintaining accurate financial records and detecting discrepancies between a company's internal accounts and bank statements. While the frequency of reconciliations can vary depending on a business's size, transaction volume, and industry, performing them annually poses significant risks. Here’s a detailed exploration of the Annual Reconciliation Risks associated with this approach:

One of the primary risks of annual bank reconciliations is the delayed detection of errors or fraud. When reconciliations are conducted only once a year, discrepancies such as unauthorized transactions, posting errors, or fraudulent activities can go unnoticed for extended periods. This delay increases the difficulty of identifying and resolving issues, as the trail of evidence may grow cold, and responsible parties may no longer be traceable. For instance, a small embezzlement scheme could escalate over months, causing substantial financial loss before being discovered during the annual reconciliation.

Another risk is the accumulation of unresolved discrepancies, which can compound over time. Monthly or quarterly reconciliations allow businesses to address minor issues promptly, preventing them from snowballing into larger problems. In contrast, annual reconciliations force accountants to sift through a year’s worth of transactions, making it harder to pinpoint specific errors. This complexity increases the likelihood of overlooking discrepancies, leading to inaccurate financial statements and potential compliance violations.

Cash flow management also suffers under an annual reconciliation schedule. Regular reconciliations provide real-time insights into a company’s cash position, enabling better decision-making and liquidity management. Annual reconciliations, however, leave businesses in the dark for most of the year, increasing the risk of overdrafts, missed payments, or inefficient allocation of funds. This lack of visibility can hinder strategic planning and operational efficiency, particularly for businesses with fluctuating cash flows.

Furthermore, regulatory and audit risks are heightened with annual reconciliations. Many regulatory bodies and accounting standards, such as GAAP or IFRS, emphasize the importance of timely and accurate financial reporting. Auditors scrutinize the frequency and thoroughness of bank reconciliations as part of their assessments. Annual reconciliations may raise red flags, suggesting inadequate internal controls or non-compliance with reporting requirements. This can lead to adverse audit opinions, penalties, or reputational damage for the business.

Lastly, operational inefficiencies are a significant risk of annual reconciliations. Reconciling a year’s worth of transactions is a time-consuming and resource-intensive task, often requiring extensive manual effort. This not only increases the likelihood of human error but also diverts staff from more strategic activities. In contrast, frequent reconciliations streamline the process, making it more manageable and allowing for continuous improvement of financial controls.

In conclusion, while annual bank reconciliations may seem like a time-saver, the associated risks far outweigh the benefits. Delayed error detection, unresolved discrepancies, poor cash flow management, regulatory non-compliance, and operational inefficiencies are critical concerns that businesses cannot afford to ignore. Best practices recommend monthly or quarterly reconciliations to maintain financial accuracy, ensure compliance, and support informed decision-making.

Food Banks: Lifelines of Hope in Times of Catastrophe

You may want to see also

Explore related products

![]()

Automating Reconciliation Processes

The first step in automating reconciliation processes is selecting the right software or tool that aligns with your organization’s needs. Solutions like BlackLine, AutoRec, or even ERP systems with built-in reconciliation modules offer features such as transaction matching, exception handling, and audit trails. These tools can be configured to pull data directly from bank feeds and accounting systems, eliminating manual data entry and reducing the likelihood of human error. Additionally, automation allows for customizable rules and thresholds, ensuring that only relevant transactions are matched and exceptions are flagged for review. This not only saves time but also improves accuracy, making frequent reconciliations feasible and practical.

Implementing automated reconciliation processes requires careful planning and integration with existing systems. Begin by mapping out the reconciliation workflow, identifying key data sources, and defining the rules for matching transactions. For instance, criteria such as transaction dates, amounts, and reference numbers can be used to automate the matching process. Once the system is configured, it’s essential to test the automation thoroughly to ensure it functions as intended. Training staff to use the new tools and interpret the results is also critical, as automation shifts their role from manual data entry to analyzing exceptions and resolving discrepancies.

One of the most significant advantages of automating reconciliation processes is the ability to perform reconciliations more frequently, such as daily or weekly, without overwhelming staff. This increased frequency provides a real-time view of financial data, enabling businesses to identify and address issues promptly. For example, daily reconciliations can help detect unauthorized transactions or cash flow discrepancies immediately, rather than waiting until the end of the month. This proactive approach not only minimizes financial risks but also ensures compliance with regulatory requirements, as many standards recommend more frequent reconciliations for better financial oversight.

Finally, automating reconciliation processes contributes to long-term efficiency and scalability. As businesses grow, the volume of transactions increases, making manual reconciliations time-consuming and error-prone. Automation ensures that the process remains manageable, regardless of transaction volume. Moreover, automated systems often come with reporting and analytics capabilities, providing insights into reconciliation trends, common discrepancies, and areas for process improvement. By investing in automation, organizations can future-proof their reconciliation processes, ensuring they remain efficient, accurate, and aligned with best practices for determining how often bank reconciliations should be prepared.

Banks' Obligation: Notify Maturing CDs?

You may want to see also

Frequently asked questions

Bank reconciliations for small businesses should ideally be prepared monthly to ensure accuracy in financial records and detect discrepancies promptly.

While quarterly reconciliations are possible, monthly reconciliations are recommended to minimize errors, identify fraud early, and maintain up-to-date financial data.

Annual bank reconciliations are too infrequent and increase the risk of undetected errors or fraud. Monthly or quarterly reconciliations are more effective for maintaining financial integrity.