Australia's banks are often regarded as some of the most profitable and stable financial institutions globally, with a reputation for resilience even during economic downturns. Their wealth is underpinned by a dominant market share in a highly concentrated banking sector, significant revenue streams from lending, fees, and financial services, and a robust regulatory environment that fosters trust and stability. Despite recent challenges such as regulatory scrutiny, royal commissions, and global economic uncertainties, Australian banks continue to report substantial profits, maintain high credit ratings, and distribute generous dividends to shareholders. This raises questions about the extent of their wealth, their role in the national economy, and the implications for consumers, investors, and policymakers alike.

Explore related products

$21.95 $15.99

What You'll Learn

- Record Profits in 2023: Major banks report billions in profits despite economic challenges

- Dividend Payouts: Shareholders receive substantial returns, highlighting banks' financial strength

- Market Dominance: Big Four banks control 80% of Australia’s banking sector

- Executive Compensation: CEOs earn millions annually, sparking public debate on fairness

- Resilience to Crises: Banks maintain profitability through recessions and global uncertainties

![]()

Record Profits in 2023: Major banks report billions in profits despite economic challenges

Australia's major banks have once again demonstrated their financial resilience, reporting record-breaking profits in 2023, despite a challenging economic landscape. The "Big Four" banks—Commonwealth Bank (CBA), Westpac, National Australia Bank (NAB), and ANZ—have collectively posted extraordinary earnings, solidifying their position as some of the most profitable institutions in the country. This remarkable performance raises questions about the factors contributing to their success and the broader implications for the Australian economy.

Soaring Profits Amidst Economic Headwinds

In a year marked by rising interest rates, inflationary pressures, and global economic uncertainties, Australian banks have defied expectations. CBA, the nation's largest lender, led the pack with a staggering cash profit of AUD 10.2 billion for the 2023 financial year, surpassing pre-pandemic levels. Westpac followed suit, announcing a cash earnings growth of 15%, reaching AUD 7.1 billion. NAB and ANZ also reported impressive results, with NAB's cash earnings rising 8.6% to AUD 7.6 billion and ANZ's statutory profit increasing by 13% to AUD 7.4 billion. These figures highlight the banks' ability to thrive even in a less-than-favorable economic environment.

The primary driver of these record profits is the net interest margin (NIM) expansion. As central banks raised interest rates to combat inflation, Australian lenders benefited from higher lending rates while keeping deposit rates relatively low. This strategy significantly boosted their income from loans, particularly in the mortgage market, which constitutes a substantial portion of their business. Additionally, the banks' focus on cost-cutting measures and digital transformation has improved operational efficiency, further contributing to their bottom line.

Wealth Accumulation and Its Impact

The consistent profitability of Australia's major banks has led to a significant accumulation of wealth. Over the past decade, these institutions have consistently reported multi-billion-dollar profits, allowing them to build substantial capital reserves. This financial strength has enabled banks to weather economic downturns, invest in technology, and expand their operations. However, it also raises concerns about market concentration and the potential for reduced competition. With such dominant positions, there are calls for increased regulatory scrutiny to ensure fair practices and protect consumers.

Despite the impressive financial results, the banks' success story is not without its challenges. The Australian banking sector faces ongoing regulatory changes, including the implementation of the Consumer Data Right and open banking reforms, which aim to increase competition and give customers more control over their data. Moreover, the rise of fintech companies and digital disruptors is reshaping the industry, forcing traditional banks to adapt and innovate to meet evolving customer expectations.

In summary, the record profits of Australia's major banks in 2023 showcase their ability to navigate economic challenges and capitalize on market conditions. While their financial prowess is undeniable, it also underscores the need for a balanced approach to ensure a competitive and fair banking environment for all Australians. As these banks continue to dominate the financial landscape, policymakers and regulators play a crucial role in fostering a healthy and diverse banking sector.

How Banks Avoid Taxes on Foreclosed Homes

You may want to see also

Explore related products

![]()

Dividend Payouts: Shareholders receive substantial returns, highlighting banks' financial strength

Australia's major banks, often referred to as the "Big Four" (Commonwealth Bank, Westpac, ANZ, and NAB), are renowned for their financial robustness, a fact underscored by their consistent and substantial dividend payouts to shareholders. Dividends are a critical indicator of a company’s financial health, as they represent the portion of profits distributed to shareholders, and Australian banks have historically excelled in this area. For instance, despite economic fluctuations, these banks have maintained high dividend payout ratios, often exceeding 70% of their earnings. This commitment to returning value to shareholders not only reflects their strong profitability but also their ability to generate stable cash flows, even in challenging economic conditions.

The size and consistency of dividend payouts from Australian banks highlight their underlying financial strength. In the fiscal year 2022, Commonwealth Bank alone paid out over AUD 7 billion in dividends, while Westpac, ANZ, and NAB collectively distributed billions more. These figures are particularly impressive when compared to global peers, as Australian banks often offer higher dividend yields, typically ranging between 5% and 7%. Such yields are a testament to their ability to sustain profits and maintain a strong capital base, even while returning significant value to shareholders. This financial resilience is further reinforced by their strong credit ratings and robust regulatory frameworks, which ensure stability and reliability.

Another aspect of dividend payouts that underscores the wealth of Australian banks is their ability to maintain or even increase dividends during economic downturns. For example, during the COVID-19 pandemic, while many global banks reduced or suspended dividends, Australian banks were among the few that continued to pay substantial dividends. This was made possible by their strong capital positions, diversified revenue streams, and prudent risk management practices. The Australian Prudential Regulation Authority (APRA) also played a role by ensuring banks maintained sufficient capital buffers, further enabling them to support shareholders through consistent payouts.

The substantial dividend payouts also reflect the banks' dominant market position and oligopolistic structure within Australia. With limited competition and a captive customer base, these banks enjoy high profit margins, which are then partially distributed to shareholders. Additionally, their exposure to Australia’s resilient housing market and stable economy provides a steady stream of income, further bolstering their ability to pay dividends. Shareholders, particularly retail investors and superannuation funds, benefit significantly from these payouts, which often form a substantial part of their investment income.

In conclusion, the dividend payouts from Australia’s major banks are a clear indicator of their financial strength and wealth. The ability to consistently distribute substantial returns to shareholders, even in adverse economic conditions, highlights their robust profitability, strong capital bases, and strategic market positioning. For investors, these dividends not only provide attractive yields but also serve as a reliable measure of the banks' enduring financial health and stability in the Australian economy.

Exploring Sri Lanka's Banking Sector: Counting the Commercial Banks

You may want to see also

Explore related products

![]()

Market Dominance: Big Four banks control 80% of Australia’s banking sector

Australia's banking sector is characterized by an extraordinary level of concentration, with the 'Big Four' banks—Commonwealth Bank of Australia (CBA), Westpac, Australia and New Zealand Banking Group (ANZ), and National Australia Bank (NAB)—dominating the market. Collectively, these institutions control approximately 80% of the country's banking sector, a level of market dominance that is unparalleled in many other developed economies. This oligopoly has significant implications for competition, consumer choice, and the overall financial landscape in Australia. The Big Four's stranglehold on the market is evident across various segments, including retail banking, mortgages, business lending, and credit cards, where they consistently maintain a lion's share of the market.

The roots of this dominance lie in historical factors, strategic acquisitions, and a regulatory environment that has traditionally favored larger institutions. Over the decades, the Big Four have expanded through mergers and acquisitions, absorbing smaller banks and financial institutions to solidify their market positions. For instance, the Commonwealth Bank's acquisition of the State Bank of Victoria in the 1990s and Westpac's merger with St. George Bank in 2008 are prime examples of how these giants have grown. Their size and scale have allowed them to achieve economies of scope and leverage technology more effectively, further entrenching their dominance.

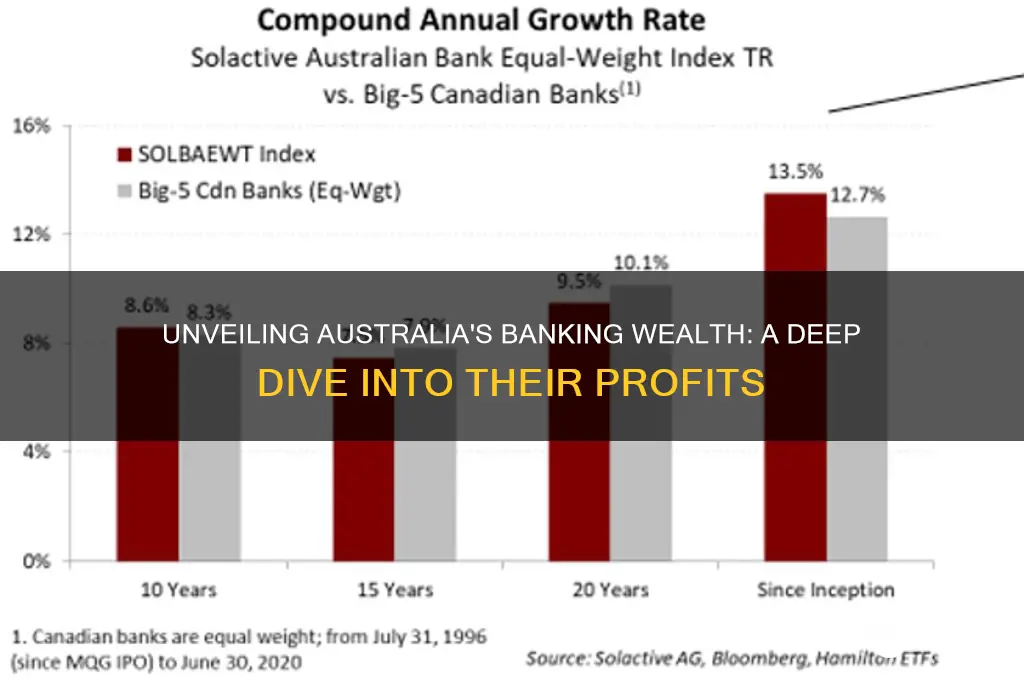

This market concentration has led to substantial profitability for the Big Four, contributing significantly to their wealth and Australia's reputation for having some of the richest banks in the world. Their combined annual profits often exceed AUD 30 billion, with return on equity (ROE) consistently higher than global peers. The banks' ability to maintain high profit margins is partly due to their market power, which enables them to charge higher fees and interest rates while offering less competitive deposit rates compared to smaller competitors. This dynamic has sparked debates about the fairness of the banking system and the need for greater competition.

The dominance of the Big Four also raises concerns about systemic risk and financial stability. With such a large portion of the banking sector controlled by a handful of institutions, any financial distress within one of these banks could have cascading effects on the entire economy. Regulators, including the Australian Prudential Regulation Authority (APRA) and the Australian Competition and Consumer Commission (ACCC), have implemented measures to mitigate these risks, such as higher capital requirements and inquiries into banking practices. However, the fundamental issue of market concentration remains largely unaddressed.

Efforts to challenge the Big Four's dominance have been limited, with smaller banks and non-bank financial institutions struggling to gain significant market share. While digital disruptors and neobanks have emerged in recent years, they have yet to make a substantial dent in the Big Four's market control. Government initiatives, such as the introduction of open banking and the Consumer Data Right, aim to foster competition by enabling customers to share their banking data with third parties more easily. However, the entrenched position of the Big Four continues to pose significant barriers to entry for new players.

In conclusion, the Big Four banks' control of 80% of Australia's banking sector underscores their unparalleled market dominance and wealth. This concentration has been driven by historical consolidation, strategic growth, and a regulatory environment that has favored large institutions. While their profitability is a testament to their success, it also highlights the challenges of fostering a more competitive and equitable banking system. Addressing this dominance will require sustained regulatory intervention, support for smaller competitors, and a shift toward greater financial inclusivity to ensure the long-term health of Australia's banking sector.

PNC Bank Pay Schedule: Weekly or Biweekly? Explained for Employees

You may want to see also

Explore related products

$21.22 $27.95

![]()

Executive Compensation: CEOs earn millions annually, sparking public debate on fairness

The wealth of Australia's banks is a topic of significant public interest, and at the heart of this discussion is the issue of executive compensation. CEOs of major Australian banks earn millions of dollars annually, a fact that has sparked intense debate about fairness and equity. For instance, in 2022, the CEOs of the "Big Four" banks—Commonwealth Bank, Westpac, ANZ, and NAB—collectively earned over $30 million in remuneration, including base salaries, bonuses, and long-term incentives. These figures stand in stark contrast to the average Australian salary, raising questions about whether such compensation is justified.

Proponents of high executive pay argue that these CEOs are responsible for managing multi-billion-dollar institutions, making decisions that impact the economy, shareholders, and employees. They contend that competitive compensation packages are necessary to attract and retain top talent in a global market. Additionally, a significant portion of CEO pay is often tied to performance metrics, such as shareholder returns and long-term growth, aligning their interests with those of the bank and its investors. However, critics counter that the disparity between CEO pay and average worker wages has widened significantly over the decades, contributing to income inequality.

The public debate is further fueled by instances where banks have faced scandals or controversies, such as those uncovered by the Royal Commission into Misconduct in the Banking, Superannuation, and Financial Services Industry. During these times, high executive pay is often seen as tone-deaf, especially when customers and employees bear the brunt of the fallout. For example, despite record profits, banks have been criticized for cutting jobs, increasing fees, or failing to pass on interest rate cuts to customers, all while CEOs continue to earn substantial bonuses. This disconnect has eroded public trust and intensified calls for greater transparency and accountability in executive compensation.

Another point of contention is the ratio of CEO pay to average employee earnings within the banks. In some cases, Australian bank CEOs earn upwards of 100 times the salary of their median employee, a ratio far higher than in many other industries. Advocates for pay restraint argue that such disparities are morally questionable and undermine workplace morale. They suggest that capping executive pay or linking it more closely to employee wages could help address these concerns. However, implementing such measures would require regulatory intervention, which remains a contentious issue in Australia's corporate governance landscape.

Ultimately, the debate over executive compensation in Australia's banking sector reflects broader societal concerns about wealth distribution and corporate responsibility. While banks argue that high CEO pay is essential for maintaining competitiveness and driving performance, critics emphasize the need for fairness and ethical leadership. Striking a balance between rewarding top executives and ensuring equitable outcomes for all stakeholders remains a complex challenge. As public scrutiny continues to grow, banks may need to reevaluate their compensation structures to align with evolving expectations of accountability and social responsibility.

How to Contact the World Bank: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Resilience to Crises: Banks maintain profitability through recessions and global uncertainties

Australia's banks have demonstrated remarkable resilience to crises, consistently maintaining profitability even during recessions and periods of global uncertainty. This resilience is underpinned by several key factors, including robust regulatory frameworks, diversified revenue streams, and prudent risk management practices. The Australian Prudential Regulation Authority (APRA) enforces stringent capital adequacy requirements, ensuring banks hold sufficient reserves to absorb shocks. For instance, during the Global Financial Crisis (GFC) of 2008, Australian banks emerged relatively unscathed due to their strong capitalization and conservative lending practices, contrasting sharply with the failures seen in other global banking systems.

One of the critical reasons for the banks' resilience is their ability to diversify income sources. Australian banks generate revenue not only from traditional lending activities but also from wealth management, insurance, and financial advisory services. This diversification helps buffer against downturns in any single sector. For example, during the COVID-19 pandemic, while lending activities slowed, banks' wealth management divisions benefited from increased market activity, helping to offset potential losses. Additionally, the oligopolistic nature of Australia's banking sector, dominated by the "Big Four" (Commonwealth Bank, Westpac, ANZ, and NAB), provides a stable market share and pricing power, further insulating them from extreme volatility.

Another factor contributing to their resilience is the banks' focus on domestic markets, which are characterized by a stable economy and a strong housing sector. Australia's consistent population growth and robust housing demand have fueled mortgage lending, a core profit driver for banks. Even during global crises, the domestic focus has shielded Australian banks from overexposure to international risks. Moreover, the government's implicit guarantee of the banking system, reinforced during the GFC, has maintained depositor confidence and ensured liquidity during turbulent times.

Prudent risk management and conservative lending practices are also central to the banks' ability to weather crises. Australian banks maintain strict underwriting standards, particularly in mortgage lending, which constitutes a significant portion of their loan books. This approach minimizes defaults and reduces the need for large provisions during economic downturns. For instance, during the pandemic, banks proactively increased their provisions for bad debts, but the actual defaults remained lower than expected, allowing them to release these provisions and boost profits in subsequent periods.

Finally, the banks' ability to adapt quickly to changing conditions has been crucial. During crises, Australian banks have implemented cost-cutting measures, accelerated digital transformation, and restructured operations to maintain efficiency. For example, the shift to online banking during COVID-19 not only ensured continuity of services but also reduced operational costs. This agility, combined with strong balance sheets and strategic foresight, positions Australian banks to navigate future uncertainties while sustaining profitability. In essence, their resilience is a testament to a well-regulated, diversified, and adaptive banking system.

Has Trump Gone Bankrupt? Unraveling His Financial Battles with Banks

You may want to see also

Frequently asked questions

Australia's "Big Four" banks (Commonwealth Bank, Westpac, ANZ, and NAB) are among the most profitable in the world, consistently delivering high returns on equity (ROE) compared to global peers. Their dominance in a concentrated market, coupled with stable economic conditions, has fueled their financial success.

The banking sector accounts for a significant portion of Australia's economy, with the Big Four banks holding assets equivalent to roughly 200% of the country’s GDP. Their market capitalization also represents a substantial share of the Australian Securities Exchange (ASX).

Australian banks have not required direct taxpayer bailouts, even during the 2008 global financial crisis. However, they benefit from an implicit government guarantee, which lowers their borrowing costs and enhances their stability, effectively providing indirect taxpayer support.

![Greed [ NON-USA FORMAT, PAL, Reg.0 Import - Spain ]](https://m.media-amazon.com/images/I/511DV99T4aL._AC_UY218_.jpg)