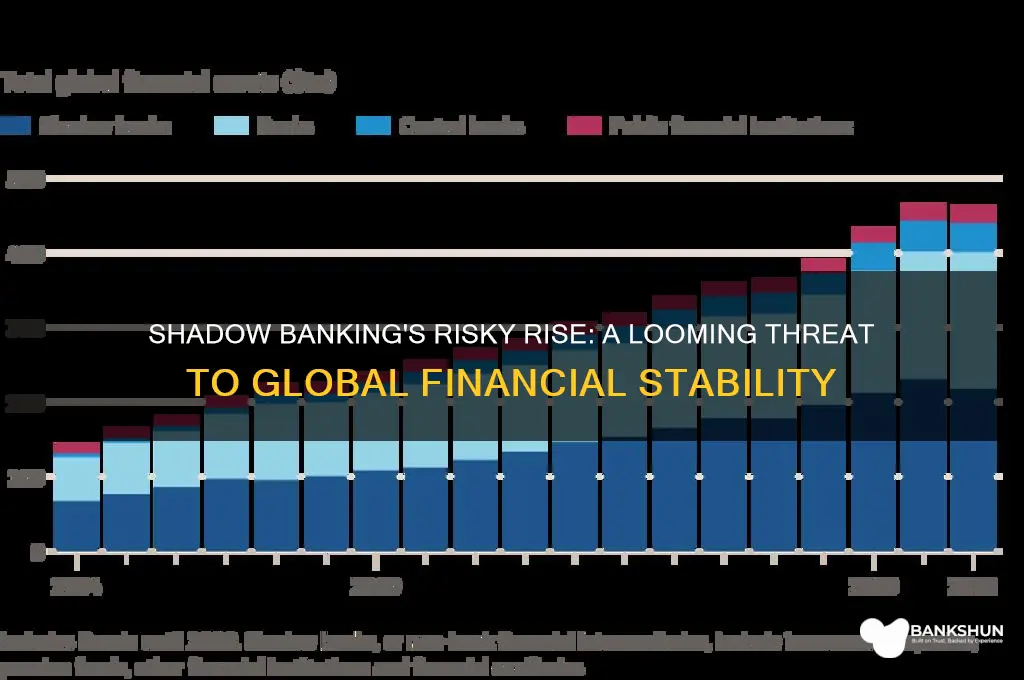

Shadow banks, non-traditional financial institutions operating outside the regulatory framework of conventional banks, pose a significant threat to the global economy due to their lack of oversight and high-risk practices. These entities, which include investment banks, hedge funds, and money market funds, engage in complex financial activities such as securitization, leverage, and short-term funding, often amplifying systemic risks. Unlike traditional banks, shadow banks are not subject to stringent capital requirements or deposit insurance, making them more vulnerable to liquidity crises and defaults. Their interconnectedness with the broader financial system means that a failure within this sector can quickly cascade into a global financial meltdown, as evidenced during the 2008 financial crisis. As shadow banking continues to grow in scale and complexity, regulators face mounting challenges in monitoring and mitigating the risks they pose, underscoring the urgent need for comprehensive reforms to safeguard the global economy.

Explore related products

What You'll Learn

- Unregulated lending practices increase systemic risk and financial instability globally

- Shadow banks evade oversight, creating hidden vulnerabilities in markets

- High leverage in shadow banking amplifies economic shocks and crises

- Lack of transparency in shadow banking obscures true risk exposure

- Shadow banks’ reliance on short-term funding triggers liquidity crunches

![]()

Unregulated lending practices increase systemic risk and financial instability globally

Unregulated lending practices within the shadow banking sector significantly amplify systemic risk and financial instability on a global scale. Shadow banks, which operate outside the traditional banking system and are often less regulated, engage in lending activities that can lead to excessive risk-taking. Unlike traditional banks, shadow banks are not subject to the same stringent capital requirements, liquidity standards, or oversight. This lack of regulation allows them to extend loans with higher leverage and riskier terms, often to borrowers who may not meet the creditworthiness standards of regulated institutions. As a result, the accumulation of risky assets within the shadow banking system creates a fragile foundation that can quickly unravel during economic downturns, triggering widespread financial distress.

One of the primary ways unregulated lending practices increase systemic risk is through the proliferation of opaque and interconnected financial instruments. Shadow banks frequently rely on complex structures such as asset-backed securities, collateralized debt obligations, and repurchase agreements to fund their lending activities. These instruments are often difficult to value and lack transparency, making it challenging for regulators and market participants to assess the true extent of risk. The interconnectedness of these instruments means that a default or distress in one part of the shadow banking system can rapidly spread to other institutions and markets, creating a domino effect that destabilizes the entire financial ecosystem.

Moreover, the absence of robust regulatory frameworks for shadow banks exacerbates moral hazard and encourages reckless behavior. Without strict oversight, shadow banks may prioritize short-term profits over long-term stability, leading to over-lending and the mispricing of risk. This behavior can result in asset bubbles, particularly in real estate or other sectors heavily reliant on credit. When these bubbles burst, the consequences are severe, as seen in the 2008 global financial crisis, where the collapse of shadow banking entities like Lehman Brothers and the implosion of the subprime mortgage market sent shockwaves through the global economy. The lack of a lender of last resort for shadow banks further compounds the problem, as there is no safety net to prevent a liquidity crisis from escalating into a full-blown insolvency crisis.

Globally, the rise of shadow banking in emerging markets adds another layer of systemic risk. In countries with underdeveloped formal banking sectors, shadow banks often fill the credit gap, but their unregulated nature makes them particularly vulnerable to economic shocks. Currency mismatches, reliance on volatile funding sources, and inadequate risk management practices in these markets can lead to sudden capital outflows and financial contagion. The globalized nature of financial markets means that distress in one region’s shadow banking sector can quickly spill over to other economies, undermining international financial stability.

Addressing the risks posed by unregulated lending practices in shadow banking requires coordinated global regulatory efforts. Policymakers must implement frameworks that enhance transparency, impose prudent risk management standards, and ensure that shadow banks are subject to adequate oversight. Stress testing, capital buffers, and liquidity requirements should be extended to shadow banking entities to mitigate their contribution to systemic risk. Additionally, international cooperation is essential to close regulatory loopholes and prevent shadow banks from exploiting jurisdictional arbitrage. Without such measures, the unchecked growth of shadow banking will continue to threaten the resilience of the global financial system, leaving economies vulnerable to recurring crises.

Exploring the Extensive Network of Central Bank Branches Nationwide

You may want to see also

Explore related products

![]()

Shadow banks evade oversight, creating hidden vulnerabilities in markets

Shadow banks, which include entities like investment funds, money market funds, and non-bank financial institutions, operate outside the traditional banking sector and often evade the stringent regulatory oversight applied to conventional banks. This lack of oversight allows shadow banks to engage in high-risk activities, such as leveraging complex financial instruments and relying heavily on short-term funding, without the same transparency or capital requirements. As a result, their operations remain largely hidden from regulators, creating systemic vulnerabilities that can destabilize financial markets. Unlike traditional banks, shadow banks are not subject to regular stress tests or liquidity coverage ratios, making it difficult for authorities to assess their resilience during economic downturns.

One of the primary ways shadow banks evade oversight is by operating in jurisdictions with lax regulations or by structuring their activities to fall outside the scope of existing financial laws. For instance, many shadow banking entities use special purpose vehicles (SPVs) or offshore entities to conduct their operations, which complicates efforts to monitor their activities. This regulatory arbitrage enables them to take on excessive risks, such as over-leveraging or investing in opaque assets, without the same scrutiny applied to traditional banks. The opacity of these activities makes it challenging for regulators to identify emerging risks or intervene before they escalate into broader market disruptions.

The interconnectedness of shadow banks with the traditional financial system further exacerbates hidden vulnerabilities. Shadow banks often rely on funding from traditional banks or engage in transactions with them, creating a web of dependencies that can amplify shocks. For example, during the 2008 financial crisis, the collapse of shadow banking entities like Lehman Brothers and the Reserve Primary Fund exposed the fragility of this interconnected system. When shadow banks face liquidity shortages or defaults, the ripple effects can quickly spread to traditional banks and other market participants, triggering a chain reaction of losses and destabilizing global markets.

Another critical issue is the reliance of shadow banks on wholesale funding, such as repos and commercial paper, which is inherently unstable compared to retail deposits. This short-term funding model makes shadow banks vulnerable to sudden withdrawals or "runs," as seen during periods of market stress. Unlike traditional banks, which have access to central bank liquidity facilities, shadow banks lack a reliable lender of last resort. This funding fragility can lead to abrupt deleveraging, asset fire sales, and a freeze in credit markets, as investors lose confidence and withdraw their funds en masse.

The hidden vulnerabilities created by shadow banks are further compounded by their role in amplifying asset price bubbles and increasing systemic leverage. By providing credit outside the regulated banking system, shadow banks contribute to excessive risk-taking and speculative activity, particularly in real estate and securities markets. When these bubbles burst, the resulting losses are often concentrated in shadow banking entities, but the fallout extends to the broader economy. Regulators, unable to monitor these activities effectively, are left to address the consequences after the damage is done, highlighting the urgent need for enhanced oversight and transparency in the shadow banking sector.

Does Signature Bank Still Provide Shredding Services? An Updated Guide

You may want to see also

Explore related products

![]()

High leverage in shadow banking amplifies economic shocks and crises

High leverage in shadow banking significantly amplifies economic shocks and crises by creating a fragile financial system prone to rapid contagion. Shadow banks, which include entities like investment funds, hedge funds, and non-bank lenders, often operate with much higher leverage ratios compared to traditional banks. This means they borrow extensively to fund their operations, magnifying both potential gains and losses. When asset prices decline or interest rates rise, highly leveraged shadow banks face immediate liquidity pressures, as the value of their collateral shrinks relative to their debt obligations. This vulnerability can trigger a cascade of forced asset sales, further depressing prices and spreading distress across interconnected markets.

The lack of regulatory oversight and access to central bank support exacerbates the risks associated with high leverage in shadow banking. Unlike traditional banks, shadow banks are not subject to stringent capital requirements or deposit insurance schemes, allowing them to take on greater risks without adequate buffers. During economic downturns, this lack of regulatory safeguards leaves shadow banks more exposed to funding runs and liquidity crises. For instance, during the 2008 financial crisis, highly leveraged shadow banks like structured investment vehicles (SIVs) collapsed, freezing credit markets and accelerating the global recession. The absence of a lender of last resort for these entities means that shocks to shadow banking can quickly spiral into systemic crises.

High leverage in shadow banking also amplifies economic shocks by intensifying procyclical behavior. During boom periods, shadow banks aggressively expand lending and investment, fueling asset bubbles and excessive risk-taking. However, when economic conditions deteriorate, these institutions abruptly contract their activities, withdrawing liquidity from markets and deepening downturns. This boom-and-bust cycle is particularly destabilizing because shadow banks operate in less transparent markets, making it difficult for regulators and investors to assess risks accurately. The sudden deleveraging process can lead to fire sales, credit crunches, and a self-reinforcing spiral of economic contraction.

Moreover, the interconnectedness of shadow banks with the broader financial system ensures that their high leverage poses systemic risks. Shadow banks often rely on short-term funding from traditional banks and money market funds, creating a web of interdependencies. When a highly leveraged shadow bank fails, it can trigger a chain reaction, as counterparties face losses and funding markets seize up. This contagion effect was evident during the collapse of Lehman Brothers, where the failure of a single institution exposed the fragility of the entire shadow banking ecosystem. The resulting loss of confidence and liquidity across markets underscored how high leverage in shadow banking can transform localized shocks into global crises.

In conclusion, high leverage in shadow banking acts as a dangerous amplifier of economic shocks and crises. By operating with excessive debt, shadow banks create a system vulnerable to rapid destabilization, particularly during periods of stress. The absence of robust regulatory frameworks and safety nets further heightens these risks, while the procyclical nature of shadow banking exacerbates economic volatility. Addressing these vulnerabilities requires stricter oversight, enhanced transparency, and measures to curb excessive leverage in the shadow banking sector. Without such reforms, the global economy remains exposed to the threat of shadow banking-driven crises.

Lloyds Bank Dividend Schedule: Frequency and Payment Insights

You may want to see also

Explore related products

![]()

Lack of transparency in shadow banking obscures true risk exposure

The lack of transparency in shadow banking is a critical issue that significantly obscures true risk exposure, posing a substantial threat to the global economy. Unlike traditional banks, shadow banks—which include entities like investment funds, money market funds, and structured investment vehicles—operate outside the stringent regulatory frameworks that govern conventional financial institutions. This opacity makes it difficult for regulators, investors, and even the institutions themselves to accurately assess the risks embedded in their operations. Without clear visibility into the assets, liabilities, and interconnectedness of these entities, the potential for systemic risk escalates, as vulnerabilities can remain hidden until they trigger a financial crisis.

One of the primary ways shadow banking obscures risk exposure is through the complexity of its financial instruments and transactions. Shadow banks often engage in securitization, repurchase agreements (repos), and derivative contracts, which are inherently difficult to value and track. For instance, securitization involves pooling loans and selling them as asset-backed securities, but the underlying assets’ quality and performance may not be fully disclosed. This lack of transparency makes it challenging to determine the true credit risk associated with these securities. Similarly, repos, which are short-term collateralized loans, can create a web of interconnected liabilities that are not always visible, amplifying counterparty risk during times of stress.

Another dimension of the transparency problem lies in the shadow banking sector’s reliance on wholesale funding, such as short-term loans and commercial paper, rather than stable customer deposits. This funding model is inherently fragile because it is prone to sudden withdrawals or "runs" if investors lose confidence. During such episodes, the true liquidity risk of shadow banks becomes apparent, but only after the damage is done. The 2008 financial crisis highlighted this vulnerability when the collapse of Lehman Brothers and the near-failure of money market funds exposed the systemic risks tied to opaque funding practices in shadow banking.

The global nature of shadow banking further exacerbates the transparency challenge. Many shadow banking activities transcend national borders, making it difficult for any single regulator to monitor or control them effectively. Regulatory arbitrage, where entities exploit differences in regulatory standards across jurisdictions, adds another layer of opacity. This fragmentation prevents a comprehensive understanding of the global shadow banking system’s risk exposure, leaving the international financial system vulnerable to shocks that can quickly spread across borders.

Finally, the absence of standardized reporting requirements for shadow banks compounds the problem. Traditional banks are subject to rigorous disclosure rules, stress tests, and capital adequacy requirements, but shadow banks often operate in a regulatory gray area. This lack of uniformity in reporting makes it nearly impossible to aggregate data on a systemic level, hindering efforts to identify emerging risks. As a result, policymakers and central banks are often left reacting to crises rather than proactively mitigating them, underscoring how the lack of transparency in shadow banking obscures true risk exposure and threatens global financial stability.

The Collapse of US Banks: Causes and Consequences of the Crisis

You may want to see also

Explore related products

![]()

Shadow banks’ reliance on short-term funding triggers liquidity crunches

Shadow banks, which operate outside the traditional banking system, often rely heavily on short-term funding to finance their operations. This includes repurchase agreements (repos), commercial paper, and other forms of short-term debt. While this funding model allows shadow banks to leverage their assets and generate higher returns, it also exposes them to significant liquidity risks. Short-term funding is inherently unstable because it needs to be continually rolled over, leaving shadow banks vulnerable to sudden shifts in market sentiment or funding conditions. When investors or lenders become risk-averse, they may refuse to renew these short-term loans, leading to a liquidity crunch.

The reliance on short-term funding creates a fragile foundation for shadow banks, particularly during times of economic stress or market volatility. For instance, during the 2008 financial crisis, shadow banks faced severe liquidity shortages as investors withdrew funds en masse, causing a domino effect of defaults and insolvencies. This phenomenon, known as a "run" on shadow banks, can spread rapidly across the financial system, as these institutions are deeply interconnected with traditional banks and other market participants. The sudden inability to access short-term funding forces shadow banks to sell assets at fire-sale prices, further depressing asset values and exacerbating the crisis.

Liquidity crunches triggered by short-term funding reliance can have systemic implications for the global economy. Shadow banks play a critical role in credit intermediation, providing loans to businesses, households, and other entities that may not have access to traditional banking services. When these institutions face liquidity shortages, credit flows dry up, stifling economic activity. Small and medium-sized enterprises (SMEs), which often depend on shadow banking for financing, are particularly vulnerable, as they may struggle to secure alternative funding sources. This credit freeze can lead to a broader economic slowdown, job losses, and reduced consumer spending.

Moreover, the interconnectedness of shadow banks with the broader financial system amplifies the risks of liquidity crunches. Shadow banks often engage in complex transactions with traditional banks, investment funds, and other financial institutions, creating a web of interdependencies. When a shadow bank faces a liquidity crisis, the contagion can quickly spread to its counterparties, triggering a chain reaction of defaults and losses. This systemic risk was evident during the 2008 crisis, where the collapse of shadow banking entities like Lehman Brothers had far-reaching consequences for global financial stability. Regulators and policymakers have since sought to address these risks, but the shadow banking sector's opacity and complexity continue to pose challenges.

To mitigate the risks associated with shadow banks' reliance on short-term funding, regulatory reforms have focused on enhancing transparency, imposing capital and liquidity requirements, and monitoring systemic risks. However, the shadow banking sector's ability to innovate and adapt to regulatory constraints means that new risks may emerge. For example, the rise of digital lending platforms and decentralized finance (DeFi) introduces additional layers of complexity and potential vulnerabilities. Ultimately, addressing the liquidity risks posed by shadow banks requires a comprehensive, globally coordinated approach that balances innovation with financial stability. Without such measures, the reliance on short-term funding will continue to threaten the resilience of the global economy.

Donate Personal Care Items to Your Local Food Bank

You may want to see also

Frequently asked questions

Shadow banks are non-bank financial institutions that perform bank-like activities, such as lending and credit intermediation, but operate outside traditional banking regulations. Unlike traditional banks, they are not subject to the same oversight, capital requirements, or deposit insurance, making them less transparent and riskier.

Shadow banks threaten the global economy by increasing systemic risk through opaque lending practices, high leverage, and interconnectedness with regulated banks. Their lack of oversight can lead to unchecked risk-taking, which, if it fails, can trigger financial contagion and destabilize markets.

Shadow banks played a significant role in the 2008 crisis by fueling the subprime mortgage bubble through securitization and complex financial instruments like collateralized debt obligations (CDOs). When the housing market collapsed, these institutions faced massive losses, contributing to the broader financial meltdown.

Shadow banks are difficult to regulate because they operate across borders and in diverse forms, such as hedge funds, private equity firms, and money market funds. Their lack of a unified regulatory framework and ability to exploit regulatory arbitrage make oversight challenging.

To mitigate risks, regulators can impose stricter transparency requirements, limit leverage, and extend oversight to shadow banking activities. International coordination is also crucial to close regulatory loopholes and ensure consistent monitoring of these institutions globally.

![Principles of Political Economy and Taxation [1911 Edition]](https://m.media-amazon.com/images/I/81Xx2WBrKnL._AC_UL320_.jpg)