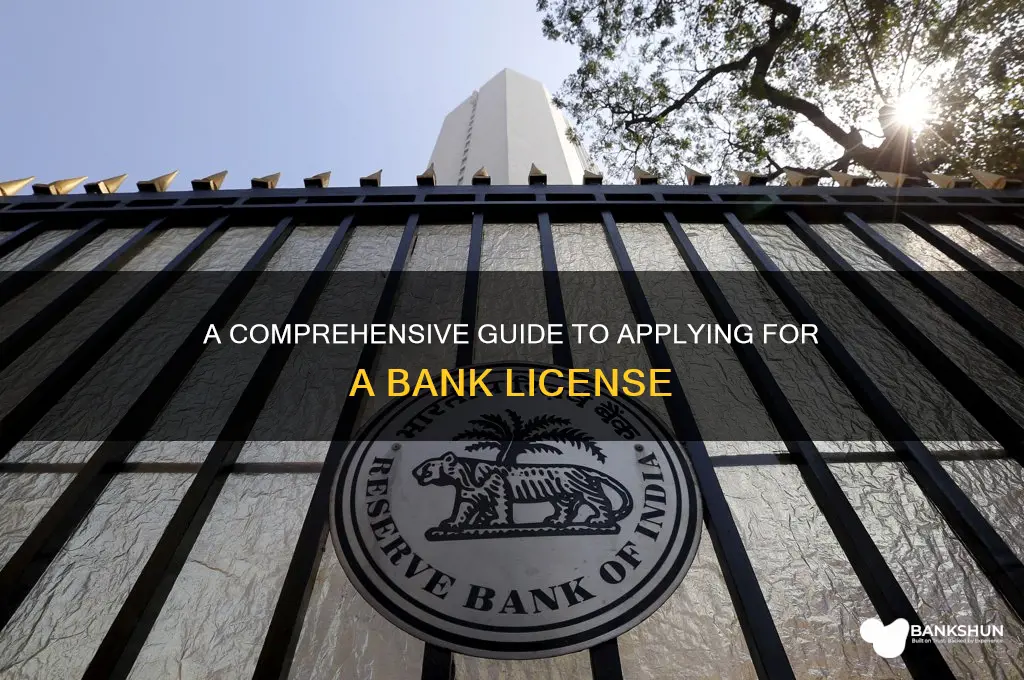

Applying for a bank license is a complex and highly regulated process that requires thorough preparation, a deep understanding of financial regulations, and a commitment to compliance. Prospective applicants must first research the specific requirements of the jurisdiction in which they intend to operate, as licensing criteria vary significantly by country and region. Key steps typically include developing a comprehensive business plan, securing sufficient capital, assembling a qualified management team, and demonstrating a robust risk management framework. Additionally, applicants must undergo rigorous scrutiny by regulatory authorities, who assess factors such as financial stability, operational integrity, and adherence to anti-money laundering (AML) and know-your-customer (KYC) standards. Engaging legal and financial advisors early in the process is often essential to navigate the intricate legal and procedural requirements, ensuring a smooth and successful application.

Explore related products

What You'll Learn

- Regulatory Requirements: Understand federal/state laws, capital needs, compliance mandates, and licensing authority expectations

- Business Plan: Develop a detailed strategy, financial projections, and operational structure for approval

- Application Process: Gather documents, complete forms, pay fees, and submit to regulatory bodies

- Background Checks: Ensure all key personnel pass thorough background and integrity assessments

- Post-Approval Steps: Fulfill ongoing reporting, audits, and compliance to maintain the license

![]()

Regulatory Requirements: Understand federal/state laws, capital needs, compliance mandates, and licensing authority expectations

Applying for a bank license is a complex process that requires a deep understanding of regulatory requirements, which encompass federal and state laws, capital needs, compliance mandates, and licensing authority expectations. The first step is to familiarize yourself with the legal framework governing banking operations in your jurisdiction. In the United States, for example, the primary federal regulators include the Office of the Comptroller of the Currency (OCC), the Federal Deposit Insurance Corporation (FDIC), and the Federal Reserve. Each state also has its own banking regulator, and requirements can vary significantly. Prospective applicants must thoroughly research both federal and state laws to ensure full compliance, as failure to meet these standards can result in application rejection or future regulatory penalties.

Capital requirements are a cornerstone of the bank licensing process, as they ensure the institution has sufficient financial resources to operate safely and manage risks. Federal regulations, such as those outlined in the Basel III framework, dictate minimum capital ratios that banks must maintain. For instance, Tier 1 capital, which includes common equity and retained earnings, must meet specific thresholds relative to risk-weighted assets. Additionally, state regulators may impose their own capital requirements, which could be more stringent than federal standards. Applicants must prepare detailed financial projections and business plans to demonstrate their ability to meet these capital needs, both at the outset and on an ongoing basis.

Compliance mandates are another critical aspect of regulatory requirements, encompassing a wide range of areas such as anti-money laundering (AML), know your customer (KYC) procedures, consumer protection laws, and cybersecurity standards. Banks are expected to implement robust compliance programs that include internal controls, regular audits, and employee training. Licensing authorities will scrutinize the applicant’s compliance framework to ensure it aligns with federal laws like the Bank Secrecy Act (BSA) and state-specific regulations. Failure to address these mandates adequately can lead to delays in the licensing process or outright denial.

Licensing authorities also have specific expectations that applicants must meet, including demonstrating a clear understanding of the banking business, a viable market need for the proposed institution, and a competent management team. Authorities will evaluate the applicant’s business model, risk management strategies, and corporate governance structure to ensure they align with regulatory standards. Additionally, applicants may be required to undergo interviews or provide detailed responses to inquiries from regulators. Transparency and thorough preparation are essential to meeting these expectations and gaining approval.

Finally, it is crucial to stay informed about evolving regulatory requirements, as banking laws and mandates frequently change in response to economic conditions, technological advancements, and emerging risks. Engaging legal and financial advisors with expertise in banking regulation can provide valuable guidance throughout the application process. By proactively addressing federal and state laws, capital needs, compliance mandates, and licensing authority expectations, applicants can significantly enhance their chances of successfully obtaining a bank license.

Has Simms Successfully Acquired Landmark Bank? Latest Updates and Insights

You may want to see also

Explore related products

![]()

Business Plan: Develop a detailed strategy, financial projections, and operational structure for approval

To successfully apply for a bank license, a robust Business Plan is essential. This plan must articulate a clear and detailed strategy that outlines the bank’s mission, vision, and objectives. Start by defining the target market and the specific financial services the bank will offer, such as retail banking, commercial lending, or investment services. Identify the unique value proposition that sets the bank apart from competitors, whether it’s innovative technology, specialized services, or a focus on underserved communities. The strategy should also include a roadmap for market entry, customer acquisition, and long-term growth, demonstrating a deep understanding of the banking industry and regulatory environment.

Financial projections are a critical component of the business plan and must be meticulously prepared to gain regulatory approval. Provide a five-year forecast of income statements, balance sheets, and cash flow statements, supported by realistic assumptions about revenue growth, expense management, and capital requirements. Highlight key financial ratios such as return on assets (ROA), return on equity (ROE), and net interest margin (NIM) to showcase the bank’s profitability and sustainability. Additionally, include a detailed capital adequacy plan that aligns with regulatory standards, outlining how the bank will maintain sufficient capital to absorb losses and support operations. Stress testing scenarios should also be incorporated to demonstrate resilience under adverse economic conditions.

The operational structure of the bank must be clearly defined to ensure efficient and compliant operations. Detail the organizational hierarchy, including roles and responsibilities of key personnel, such as the CEO, CFO, and compliance officer. Describe the technology infrastructure, including core banking systems, cybersecurity measures, and customer-facing platforms, ensuring they meet industry standards and regulatory requirements. Outline the internal controls and risk management frameworks that will be implemented to monitor and mitigate operational, credit, market, and liquidity risks. Include a plan for staffing, training, and compliance with labor laws to build a competent and ethical workforce.

Regulatory compliance is a cornerstone of the business plan, as banks operate in a highly regulated environment. Provide a comprehensive overview of how the bank will adhere to local and international banking regulations, including anti-money laundering (AML), know your customer (KYC), and data privacy laws. Detail the processes for reporting to regulatory bodies, conducting audits, and maintaining transparency in financial operations. Additionally, address how the bank will stay updated with evolving regulatory requirements and adapt its policies and procedures accordingly. A strong compliance framework not only ensures legal adherence but also builds trust with stakeholders.

Finally, the business plan should include a contingency and exit strategy to address potential challenges and uncertainties. Outline steps to be taken in case of unforeseen events such as economic downturns, technological failures, or changes in regulatory policies. Provide a clear exit strategy for investors, including potential scenarios for mergers, acquisitions, or liquidation, ensuring that all parties are protected. By presenting a well-thought-out contingency plan, the bank demonstrates its ability to navigate risks and maintain stability in adverse situations. This comprehensive approach to the business plan will significantly enhance the likelihood of obtaining a bank license.

Understanding Bank Analysis Fees: Calculation Methods and Cost Factors

You may want to see also

Explore related products

![Compliance [Blu-ray]](https://m.media-amazon.com/images/I/712fZO6aOlL._AC_UY218_.jpg)

![]()

Application Process: Gather documents, complete forms, pay fees, and submit to regulatory bodies

The application process for obtaining a bank license is a rigorous and detailed procedure that requires careful planning and execution. It begins with gathering the necessary documents, which serve as the foundation of your application. These documents typically include a comprehensive business plan outlining the bank’s vision, mission, target market, and financial projections. Additionally, you will need to provide detailed information about the bank’s ownership structure, including the identities and backgrounds of key stakeholders, directors, and executives. Regulatory bodies often require proof of professional qualifications and experience of the management team to ensure they are capable of running a financial institution. Other essential documents may include audited financial statements, proof of initial capital, and a detailed risk management framework. It is crucial to ensure all documents are accurate, up-to-date, and compliant with the regulatory requirements of the jurisdiction in which you are applying.

Once all required documents are compiled, the next step is to complete the application forms provided by the regulatory authority. These forms are typically extensive and require precise information about the proposed bank’s operations, governance, and compliance mechanisms. Common sections include details about the bank’s legal structure, proposed services (e.g., retail banking, commercial lending), anti-money laundering (AML) policies, and cybersecurity measures. It is imperative to carefully review each form to avoid errors or omissions, as these can lead to delays or rejections. Some jurisdictions may also require notarized or certified copies of certain documents, so it is advisable to consult with legal or financial advisors to ensure compliance.

After completing the forms, applicants must pay the required fees associated with the bank license application. These fees vary widely depending on the country or regulatory body but typically cover the cost of processing the application, conducting due diligence, and inspecting the proposed institution. Fees may be non-refundable, so it is essential to confirm the exact amount and payment methods accepted by the regulatory authority. Failure to pay the fees on time can result in the application being deemed incomplete or rejected outright. Keep a record of the payment confirmation, as it may need to be submitted along with the application.

The final step in the application process is to submit the completed application package to the regulatory bodies. This submission often requires a formal letter or cover page summarizing the contents of the application and affirming the accuracy of the information provided. Depending on the jurisdiction, submissions may be accepted electronically, physically, or both. It is critical to adhere to the submission guidelines, including deadlines and formatting requirements. After submission, the regulatory body will typically acknowledge receipt of the application and may request additional information or clarification during their review process. Applicants should be prepared for this stage, as it may involve further documentation or interviews with regulators.

Throughout the application process, maintaining transparency and cooperation with regulatory bodies is key to a successful outcome. Each step—gathering documents, completing forms, paying fees, and submitting the application—requires meticulous attention to detail and adherence to regulatory standards. Engaging legal or financial experts familiar with banking regulations can significantly streamline the process and increase the likelihood of approval. Once the application is submitted, patience is essential, as the review process can take several months, depending on the complexity of the application and the workload of the regulatory authority.

Does US Bank Drug Test for Employment? What You Need to Know

You may want to see also

Explore related products

![Law of Governance, Risk Management and Compliance: [Connected Ebook] (Aspen Casebook)](https://m.media-amazon.com/images/I/616gNHR5shL._AC_UY218_.jpg)

![]()

Background Checks: Ensure all key personnel pass thorough background and integrity assessments

When applying for a bank license, one of the most critical steps is ensuring that all key personnel pass thorough background and integrity assessments. Regulatory authorities require these checks to verify the trustworthiness, competence, and ethical standing of individuals who will hold positions of responsibility within the bank. This process is designed to mitigate risks associated with fraud, mismanagement, and other financial crimes. Background checks typically encompass criminal records, credit history, employment verification, and educational qualifications. For key roles such as the CEO, CFO, and board members, the scrutiny is even more rigorous, often extending to personal and professional references, as well as any past regulatory actions or legal disputes.

The first step in conducting background checks is to identify the key personnel who require assessment. This includes executives, directors, and any individuals with significant influence over the bank’s operations or decision-making processes. Once identified, the bank must engage a reputable third-party screening firm or use approved regulatory tools to conduct the checks. It is essential to comply with local and international regulations, such as those outlined by the Financial Action Task Force (FATF) or the Basel Committee on Banking Supervision, to ensure the process meets legal standards. Transparency and consent are also crucial; all individuals must be informed of the checks and provide written authorization.

Criminal background checks are a cornerstone of this process, as they reveal any history of financial crimes, fraud, or other offenses that could disqualify an individual from holding a banking position. These checks often extend beyond local records to include international databases, especially if the individual has lived or worked abroad. Credit history assessments are equally important, as they provide insights into an individual’s financial responsibility and stability. Poor credit management or significant debts could raise concerns about potential conflicts of interest or susceptibility to bribery.

Employment and educational verifications are another vital component of background checks. These assessments confirm the accuracy of an individual’s resume, ensuring they possess the qualifications and experience claimed. Discrepancies or falsifications in these areas can lead to disqualification. Additionally, integrity assessments may include behavioral interviews or psychometric tests to evaluate an individual’s ethical values, decision-making abilities, and alignment with the bank’s culture and regulatory expectations.

Finally, ongoing monitoring is often required even after key personnel pass initial background checks. Regulatory bodies may mandate periodic re-screening to ensure continued compliance and integrity. Banks must establish robust internal policies and procedures to manage this process effectively, documenting all findings and maintaining records for regulatory audits. By prioritizing thorough background and integrity assessments, banks not only meet licensing requirements but also build a foundation of trust and reliability essential for long-term success in the financial industry.

Banknotes in Northern Ireland: Legal Tender Status

You may want to see also

Explore related products

![]()

Post-Approval Steps: Fulfill ongoing reporting, audits, and compliance to maintain the license

Once a bank license is granted, the real work begins to ensure the institution remains compliant and operational. Post-approval steps are critical to maintaining the license and avoiding penalties or revocation. One of the primary requirements is ongoing reporting, which involves submitting regular financial statements, operational reports, and other mandated disclosures to the regulatory authority. These reports typically include balance sheets, income statements, cash flow statements, and detailed accounts of assets and liabilities. Timely and accurate reporting is essential, as it allows regulators to monitor the bank’s financial health and ensure it adheres to prudential norms. Failure to submit these reports on time or providing inaccurate information can result in severe consequences, including fines or regulatory intervention.

In addition to reporting, banks must undergo regular audits to verify compliance with regulatory standards and internal controls. These audits are conducted both internally and by external auditors approved by the regulatory body. Internal audits focus on assessing the bank’s risk management, governance, and operational efficiency, while external audits provide an independent evaluation of the bank’s financial statements and compliance with laws and regulations. Audit findings must be documented and shared with regulators, and any identified deficiencies must be addressed promptly. Banks should also establish an audit committee to oversee the audit process and ensure transparency.

Compliance with regulatory requirements is another cornerstone of maintaining a bank license. This includes adhering to anti-money laundering (AML) laws, know-your-customer (KYC) procedures, and other financial crime prevention measures. Banks must implement robust compliance programs, including training staff, monitoring transactions, and reporting suspicious activities to the relevant authorities. Additionally, compliance extends to consumer protection laws, such as fair lending practices and transparent fee structures. Regular reviews of policies and procedures are necessary to adapt to evolving regulatory frameworks and industry standards.

Banks must also maintain adequate capital and liquidity levels as part of their ongoing obligations. Regulatory authorities often prescribe minimum capital adequacy ratios (CAR) and liquidity coverage ratios (LCR) to ensure banks can absorb losses and meet short-term obligations. Institutions must monitor these ratios continuously and take corrective actions if thresholds are breached. Stress testing and scenario analysis are common tools used to assess the bank’s resilience to adverse financial conditions. Failure to meet capital or liquidity requirements can lead to restrictions on operations or even license revocation.

Lastly, banks must engage proactively with regulators to foster a cooperative relationship and demonstrate commitment to compliance. This includes attending regulatory meetings, responding promptly to inquiries, and seeking clarification on ambiguous regulations. Banks should also stay informed about changes in banking laws and guidelines, as non-compliance due to ignorance is not considered a valid excuse. By prioritizing ongoing reporting, audits, and compliance, banks can ensure long-term sustainability and maintain the trust of both regulators and customers.

FIA Test Bank: Unveiling the Total Number of Exam Questions

You may want to see also

Frequently asked questions

The initial steps include conducting thorough market research, developing a detailed business plan, and ensuring compliance with regulatory requirements. You must also identify the type of banking license you need (e.g., commercial, investment, or digital bank) and prepare the necessary documentation.

The key regulatory bodies vary by country but typically include the central bank, financial regulatory authority, or a similar government agency. For example, in the U.S., it’s the Federal Reserve or the Office of the Comptroller of the Currency (OCC), while in the EU, it’s the European Central Bank (ECB) and national competent authorities.

Required documentation often includes a detailed business plan, financial projections, information on key personnel, proof of capital adequacy, anti-money laundering (AML) and compliance policies, and a risk management framework. Specific requirements may vary by jurisdiction.

The timeline varies widely depending on the jurisdiction and complexity of the application. It can range from 6 months to 2 years or more. Regulatory scrutiny, completeness of the application, and the type of banking license sought are key factors influencing the duration.