Balancing a bank balance sheet is a critical process that ensures the financial health and accuracy of a bank’s operations. It involves reconciling assets, liabilities, and equity to confirm that the fundamental accounting equation (Assets = Liabilities + Equity) holds true. This task requires meticulous attention to detail, as it encompasses verifying cash reserves, loans, deposits, and other financial instruments, while also accounting for accrued interest, provisions, and off-balance-sheet items. Proper balance sheet management not only ensures compliance with regulatory standards but also provides stakeholders with a clear picture of the bank’s financial stability and risk exposure. Mastering this process is essential for maintaining trust, making informed decisions, and safeguarding the institution’s long-term viability.

Explore related products

What You'll Learn

- Assets vs. Liabilities: Understanding the relationship between what the bank owns and owes

- Capital Adequacy: Ensuring sufficient capital to cover risks and meet regulatory requirements

- Liquidity Management: Maintaining enough cash or liquid assets to meet short-term obligations

- Reconciliation Process: Verifying transactions to ensure accuracy and consistency in the balance sheet

- Off-Balance-Sheet Items: Accounting for contingent liabilities and other non-recorded financial exposures

![]()

Assets vs. Liabilities: Understanding the relationship between what the bank owns and owes

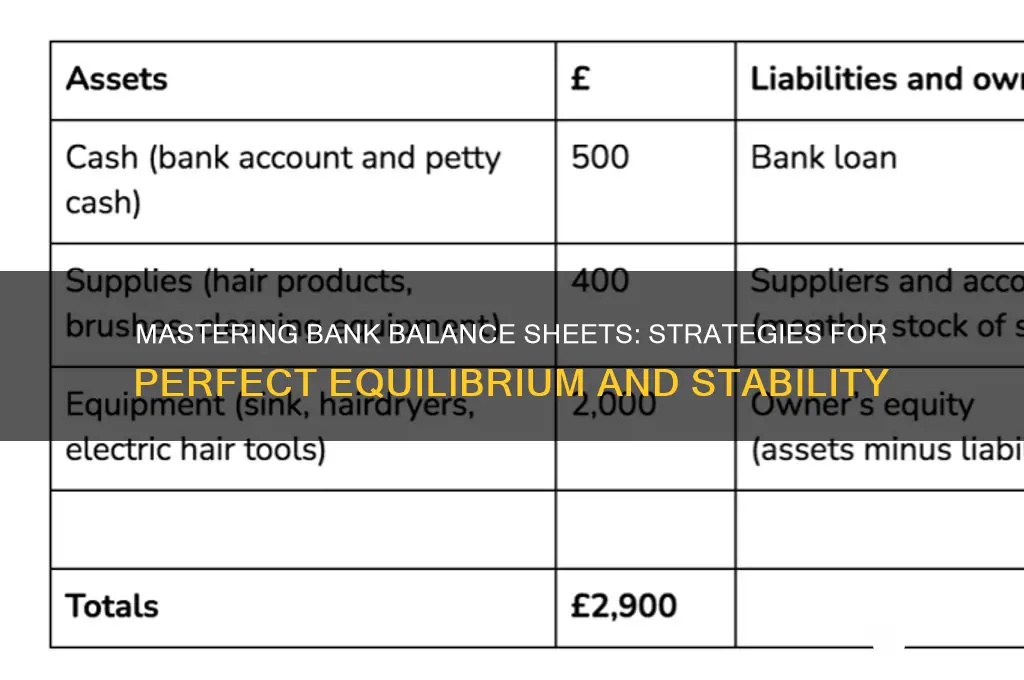

A bank's balance sheet is a critical financial statement that provides a snapshot of its financial health at a given point in time. At its core, the balance sheet is divided into two main sections: assets and liabilities, with a third component, equity, acting as the balancing factor. Understanding the relationship between what the bank owns (assets) and what it owes (liabilities) is essential for balancing the sheet and ensuring financial stability. Assets represent the economic resources controlled by the bank, such as cash, loans, securities, and physical properties. Liabilities, on the other hand, are the bank's obligations, including customer deposits, borrowed funds, and other debts. The fundamental equation governing the balance sheet is Assets = Liabilities + Equity, ensuring that what the bank owns is always equal to what it owes plus the owners' stake.

Assets are categorized into current and non-current based on their liquidity or how quickly they can be converted into cash. Current assets, like cash reserves, short-term investments, and loans due within a year, are vital for meeting immediate obligations. Non-current assets, such as long-term loans, buildings, and equipment, contribute to the bank's long-term value. For instance, when a bank issues a loan, it becomes an asset because it generates interest income over time. Similarly, cash held in vaults or reserves is a highly liquid asset. The total value of these assets reflects the bank's ability to generate revenue and maintain operations. However, assets alone do not tell the full story; they must be balanced against liabilities to assess the bank's financial position accurately.

Liabilities represent the bank's obligations to external parties and are also classified as current and non-current. Current liabilities, such as customer deposits, short-term borrowings, and accrued expenses, are debts due within a year. Non-current liabilities, like long-term bonds payable or deferred tax liabilities, are obligations due beyond a year. For example, when customers deposit money into their accounts, it becomes a liability for the bank because it must be available for withdrawal on demand. Similarly, when a bank borrows funds from other institutions, it creates a liability that must be repaid with interest. The relationship between assets and liabilities is symbiotic: deposits (liabilities) provide the funds for loans (assets), and the interest earned on loans helps cover the interest paid on deposits.

Balancing the bank's balance sheet requires ensuring that the total value of assets equals the sum of liabilities and equity. If assets exceed liabilities, the difference is reflected in equity, representing the owners' residual claim. Conversely, if liabilities exceed assets, it indicates a financial imbalance that must be addressed. For example, if a bank has $100 million in assets (loans, cash, etc.) and $90 million in liabilities (deposits, borrowings), the remaining $10 million is equity. This balance is crucial for maintaining trust with stakeholders, complying with regulatory requirements, and ensuring the bank can meet its obligations.

To effectively manage this relationship, banks must engage in prudent asset-liability management (ALM). ALM involves matching the maturity and cash flows of assets and liabilities to minimize risk and optimize profitability. For instance, a bank should avoid funding long-term loans with short-term deposits, as this creates a liquidity mismatch. Instead, it should align the duration of its assets and liabilities to ensure stability. Additionally, banks must maintain sufficient capital (equity) to absorb losses and support growth. By carefully monitoring and adjusting the mix of assets and liabilities, banks can maintain a balanced sheet and operate sustainably in the long term.

In summary, the relationship between assets and liabilities is the cornerstone of a bank's balance sheet. Assets represent what the bank owns and uses to generate income, while liabilities reflect what it owes to others. Balancing these two components is essential for financial stability, regulatory compliance, and stakeholder confidence. Through effective asset-liability management and a clear understanding of this relationship, banks can ensure they remain solvent, profitable, and capable of fulfilling their obligations to customers and investors.

Understanding Section 19: Impact on Bank Subsidiaries

You may want to see also

Explore related products

![]()

Capital Adequacy: Ensuring sufficient capital to cover risks and meet regulatory requirements

Capital adequacy is a cornerstone of a balanced bank balance sheet, ensuring that a bank maintains sufficient capital to absorb losses, support operations, and meet regulatory requirements. At its core, capital adequacy is about aligning a bank’s capital reserves with the risks it undertakes in its lending, investment, and operational activities. Banks must hold a minimum amount of capital, typically a mix of equity and debt, to act as a buffer against unexpected losses. This requirement is formalized through regulations like Basel III, which mandates specific capital ratios to safeguard financial stability. Ensuring capital adequacy involves regularly assessing risk-weighted assets (RWAs), which assign higher capital requirements to riskier assets, and maintaining a capital adequacy ratio (CAR) above the regulatory threshold, usually 8% of RWAs.

To achieve capital adequacy, banks must first conduct a thorough risk assessment of their assets and operations. This includes evaluating credit risk (the risk of loan defaults), market risk (the risk of losses from market fluctuations), and operational risk (the risk of losses from internal failures or external events). By quantifying these risks, banks can determine the appropriate level of capital needed to cover potential losses. For instance, a bank with a high proportion of risky loans will require more capital compared to one with a safer asset portfolio. Stress testing is another critical tool, simulating extreme scenarios to ensure the bank’s capital can withstand severe economic downturns or shocks.

Once risks are assessed, banks must ensure their capital structure meets regulatory demands while supporting growth and profitability. Tier 1 capital, primarily composed of common equity and retained earnings, is the most critical component as it absorbs losses without requiring the bank to cease operations. Tier 2 capital, including subordinated debt and loan-loss reserves, provides additional support but is less reliable in severe stress scenarios. Banks must strike a balance between retaining earnings to bolster capital and distributing profits to shareholders, as excessive dividends can weaken the capital base. Issuing new equity or debt can also enhance capital levels, but this must be weighed against the cost of capital and dilution of existing shareholders.

Monitoring and reporting are essential to maintaining capital adequacy. Banks must regularly calculate their CAR and compare it against regulatory minimums and internal targets. If the ratio falls below the threshold, immediate corrective actions are necessary, such as reducing risk exposure, raising additional capital, or retaining more earnings. Transparency in reporting ensures stakeholders, including regulators and investors, have confidence in the bank’s financial health. Additionally, banks should maintain a capital conservation buffer, typically 2.5% of RWAs, to absorb losses during periods of stress without restricting dividends or bonuses.

Finally, capital adequacy is not just a compliance exercise but a strategic imperative for long-term sustainability. Banks must adopt a forward-looking approach, anticipating changes in the economic environment and adjusting their capital plans accordingly. This includes diversifying revenue streams to reduce reliance on risky assets, investing in technology to mitigate operational risks, and fostering a strong risk culture throughout the organization. By prioritizing capital adequacy, banks can ensure they remain resilient, capable of supporting their customers and the broader economy, even in challenging times.

Exploring the Number of Publicly Traded Banks in the US

You may want to see also

Explore related products

![]()

Liquidity Management: Maintaining enough cash or liquid assets to meet short-term obligations

Liquidity management is a critical aspect of balancing a bank’s balance sheet, as it ensures the institution can meet its short-term obligations without disrupting operations or incurring excessive costs. At its core, liquidity management involves maintaining sufficient cash or easily convertible assets to cover withdrawals, loan demands, and other immediate liabilities. Banks must strike a balance between holding too much liquidity, which can reduce profitability, and holding too little, which can lead to solvency risks. Effective liquidity management requires a clear understanding of cash inflows and outflows, as well as the ability to forecast future needs accurately.

One key strategy in liquidity management is diversifying funding sources to reduce reliance on any single channel. Banks should maintain a mix of stable deposits, interbank borrowings, and long-term debt to ensure a steady stream of funds. Additionally, holding a portfolio of liquid assets, such as government securities or highly rated corporate bonds, allows banks to quickly convert these assets into cash if needed. Regular stress testing is essential to evaluate the bank’s ability to withstand liquidity shocks, such as sudden deposit withdrawals or market disruptions. These tests help identify potential gaps and inform adjustments to liquidity reserves.

Another important practice is maintaining a robust liquidity buffer, which acts as a safety net during unforeseen events. Central banks often set minimum liquidity coverage ratios (LCRs) to ensure banks hold enough high-quality liquid assets to survive a 30-day stress scenario. Banks should monitor their LCRs closely and adjust their asset portfolios to remain compliant. Furthermore, effective cash flow forecasting enables banks to anticipate liquidity needs and plan accordingly. This involves analyzing historical data, market trends, and seasonal variations to predict future inflows and outflows accurately.

Active management of the bank’s asset and liability mix is also crucial for liquidity management. Banks should align the maturities of their assets and liabilities to minimize funding risks. For example, short-term deposits should fund short-term loans, while long-term borrowings should support long-term investments. This practice, known as maturity matching, reduces the likelihood of liquidity shortfalls. Additionally, banks can use liquidity management tools like repurchase agreements (repos) and securities lending to access short-term funds when needed.

Finally, strong governance and risk management frameworks are essential for effective liquidity management. Banks should establish clear policies, procedures, and accountability structures to oversee liquidity risk. Regular reporting to senior management and the board ensures transparency and enables timely decision-making. Collaboration between treasury, risk management, and other departments fosters a holistic approach to liquidity management. By integrating these practices, banks can maintain sufficient liquidity to meet short-term obligations while supporting long-term growth and stability.

Foreclosing Homes: Banks' Win or Lose?

You may want to see also

Explore related products

$17.96 $22.95

![]()

Reconciliation Process: Verifying transactions to ensure accuracy and consistency in the balance sheet

The reconciliation process is a critical step in balancing a bank balance sheet, as it ensures that all transactions are accurately recorded and that the balance sheet reflects the true financial position of the bank. This process involves comparing the bank's internal records with external sources, such as statements from other financial institutions or customers, to verify the accuracy and consistency of transactions. To begin the reconciliation process, gather all relevant documents, including bank statements, general ledger accounts, and any supporting documentation for transactions. Organize these documents in a systematic manner to facilitate easy comparison and identification of discrepancies.

The first step in the reconciliation process is to compare the bank's internal records with the external bank statement. This involves matching each transaction recorded in the bank's general ledger with the corresponding entry on the bank statement. Transactions should be matched based on date, amount, and description to ensure accuracy. Any discrepancies, such as missing or duplicate transactions, should be flagged for further investigation. It is essential to maintain a detailed record of all matched and unmatched transactions, as this will help identify patterns and potential errors. Additionally, consider using reconciliation software or spreadsheets to streamline the process and minimize the risk of human error.

Once the initial comparison is complete, investigate any discrepancies to determine their cause. Common reasons for discrepancies include timing differences, errors in recording transactions, or fraudulent activities. For example, a deposit recorded in the bank's ledger may not appear on the bank statement due to a delay in processing. In such cases, it is necessary to verify the transaction with the customer or financial institution involved. If a discrepancy is found to be a result of an error, make the necessary adjustments to the bank's records to ensure accuracy. This may involve correcting the general ledger, updating account balances, or generating reversing entries to rectify the mistake.

An essential aspect of the reconciliation process is to verify the accuracy of account balances. This involves calculating the total debits and credits for each account and ensuring that they match the corresponding balances on the bank statement. If discrepancies are found, review the transactions associated with the account to identify the source of the error. It may be necessary to trace transactions back to their origin, such as deposit slips or withdrawal forms, to verify their accuracy. Furthermore, consider reconciling subsidiary ledgers, such as accounts receivable or payable, to ensure that they agree with the general ledger and bank statement. This comprehensive approach helps to identify and rectify errors that may impact the overall balance sheet.

To ensure the effectiveness of the reconciliation process, establish a regular schedule for reconciling accounts. Monthly reconciliations are common, but the frequency may vary depending on the volume and complexity of transactions. Regular reconciliations help to identify and address errors promptly, reducing the risk of material misstatements in the balance sheet. Additionally, implement internal controls to minimize the risk of errors and fraud. This may include segregating duties, such as separating the responsibilities for recording transactions and reconciling accounts, and requiring supervisory review of reconciliations. By following a structured reconciliation process and maintaining robust internal controls, banks can ensure the accuracy and consistency of their balance sheets, thereby providing reliable financial information to stakeholders.

Insured Properties: Banks and the Foreclosure Process

You may want to see also

Explore related products

![]()

Off-Balance-Sheet Items: Accounting for contingent liabilities and other non-recorded financial exposures

Balancing a bank's balance sheet involves not only accurately recording assets, liabilities, and equity but also addressing off-balance-sheet items, which are financial exposures not directly reflected on the balance sheet. These items, such as contingent liabilities and other non-recorded financial exposures, can significantly impact a bank's financial health and risk profile. Proper accounting for these items is critical to ensure transparency, compliance, and a true representation of the bank's financial position.

Contingent liabilities are potential obligations that arise from past events but are dependent on future uncertainties. Examples include loan guarantees, letters of credit, and legal claims. While these liabilities are not recorded on the balance sheet unless they are both probable and estimable, they must be disclosed in the financial statements' footnotes. Banks must assess the likelihood of these liabilities materializing and estimate their potential impact. If the liability is deemed probable and can be reasonably estimated, it should be recorded as a provision on the balance sheet. For instance, if a bank has issued a loan guarantee and it is likely that the borrower will default, the bank should record a liability for the expected loss. Proper disclosure and assessment of contingent liabilities are essential to avoid misleading stakeholders and to comply with accounting standards like IFRS or GAAP.

In addition to contingent liabilities, banks must account for other non-recorded financial exposures, such as derivative contracts, off-balance-sheet financing arrangements (e.g., asset securitizations), and commitments to lend. These items are often managed through risk management frameworks but are not directly reflected on the balance sheet. For example, derivative contracts can expose a bank to market risk, but their value is typically recorded in the income statement or through fair value adjustments rather than as assets or liabilities. Banks must ensure that these exposures are adequately disclosed and that their potential impact on the bank's financial position is assessed and communicated to regulators and investors.

To effectively manage off-balance-sheet items, banks should implement robust risk assessment and monitoring processes. This includes regularly reviewing contingent liabilities and other exposures to determine if they need to be recognized or disclosed. Stress testing and scenario analysis can help banks understand how these items might impact their balance sheet under adverse conditions. Additionally, banks should maintain clear policies and procedures for identifying, measuring, and disclosing off-balance-sheet items to ensure consistency and compliance with regulatory requirements.

Finally, transparency and communication are key when dealing with off-balance-sheet items. Banks must provide detailed disclosures in their financial statements to inform stakeholders about the nature, extent, and potential impact of these exposures. This includes explaining the methodologies used to assess contingent liabilities and other non-recorded financial exposures. By doing so, banks can build trust with investors, regulators, and other stakeholders while ensuring that their balance sheet provides a comprehensive and accurate view of their financial position. Proper accounting for off-balance-sheet items is not just a technical requirement but a critical component of sound financial management and risk governance in banking.

A Global Overview: How Many Banks Exist?

You may want to see also

Frequently asked questions

A bank balance sheet is a financial statement that shows a bank's assets, liabilities, and equity at a specific point in time. Balancing it ensures that the total assets equal the sum of liabilities and equity, reflecting the bank's financial health and compliance with regulatory standards.

To balance a bank balance sheet, verify that the total assets (e.g., loans, cash, investments) match the sum of total liabilities (e.g., deposits, borrowings) and shareholders' equity (e.g., retained earnings, capital). Use double-entry accounting to record transactions accurately.

Common challenges include mismatched entries, unrecorded transactions, valuation errors (e.g., loan impairments), and incorrect classification of assets or liabilities. Regular reconciliations and audits can help address these issues.

A bank balance sheet should be balanced at least monthly, but many banks do it daily or weekly to ensure accuracy and timely detection of discrepancies. Annual audits are also required for regulatory compliance.

Core banking systems, accounting software (e.g., SAP, Oracle), and spreadsheet tools (e.g., Excel) can assist in balancing a bank balance sheet. Automated reconciliation tools and ERP systems also streamline the process and reduce errors.