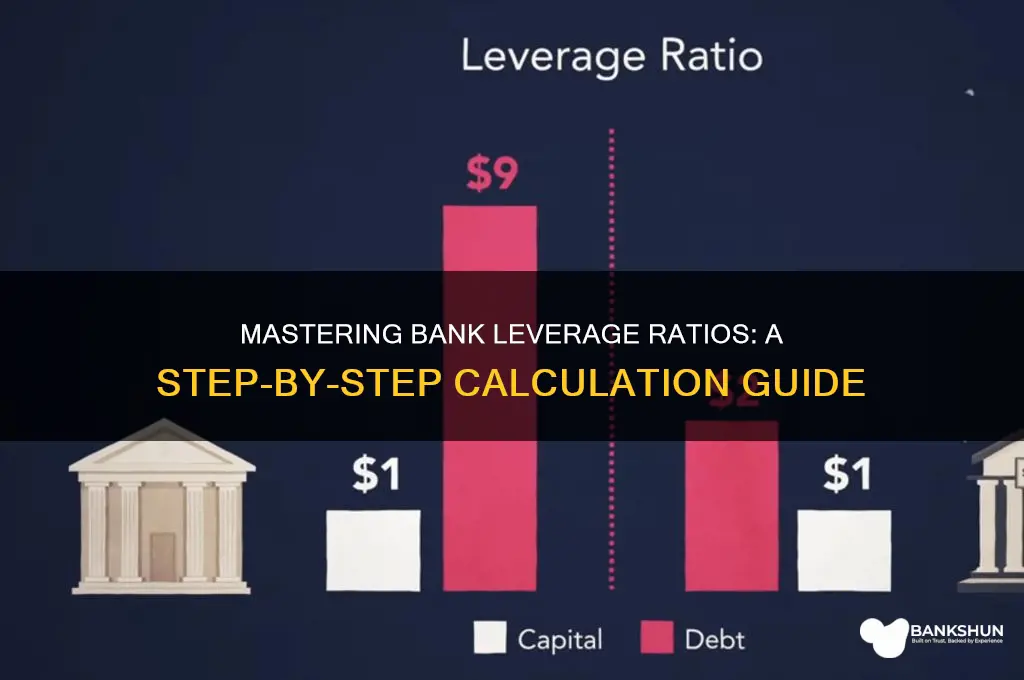

Calculating a bank's leverage ratio is a critical metric for assessing its financial stability and risk exposure. The leverage ratio measures the proportion of a bank's total assets to its equity capital, providing insight into how much debt the bank is using to finance its operations. Typically expressed as a percentage, a higher leverage ratio indicates greater reliance on borrowed funds, which can amplify both potential returns and risks. To calculate this ratio, divide the bank's total exposure, including on- and off-balance-sheet items, by its Tier 1 capital, as defined by regulatory frameworks such as Basel III. This simple yet powerful tool helps regulators, investors, and stakeholders evaluate a bank's ability to withstand financial shocks and maintain solvency.

| Characteristics | Values |

|---|---|

| Definition | Bank Leverage Ratio = Tier 1 Capital / Total Exposure |

| Tier 1 Capital | Includes common equity, retained earnings, and disclosed reserves. |

| Total Exposure | Sum of all on-balance-sheet assets and off-balance-sheet exposures. |

| Regulatory Minimum (Basel III) | 3% for Tier 1 Leverage Ratio (as of latest global standards). |

| Purpose | Measures financial stability and ability to absorb losses. |

| Frequency of Calculation | Quarterly or annually, as per regulatory requirements. |

| Latest Global Average (2023) | ~5-6% (varies by region and bank size). |

| Key Components | Tier 1 Capital, Total Assets, Derivatives, and Off-balance-sheet items. |

| Reporting Standard | IFRS 9 or GAAP, depending on jurisdiction. |

| Stress Testing | Often included in regulatory stress tests (e.g., CCAR in the U.S.). |

| Example Calculation | If Tier 1 Capital = $100 billion and Total Exposure = $2,000 billion, Leverage Ratio = 5%. |

Explore related products

What You'll Learn

![]()

Tier 1 Capital Definition

Tier 1 capital is a core measure of a bank's financial strength and a critical component in calculating the bank leverage ratio. It represents the most liquid and stable portion of a bank's capital, serving as the primary buffer to absorb losses without ceising operations. Tier 1 capital is defined as the sum of a bank's equity capital and disclosed reserves, minus any goodwill or intangible assets. This definition is crucial because it focuses on capital elements that can reliably absorb losses during stressful financial conditions. Equity capital includes common stock, retained earnings, and other comprehensive income, while disclosed reserves encompass items like general reserves and revaluation reserves that are openly reported in financial statements.

The importance of Tier 1 capital lies in its ability to provide a robust foundation for a bank's operations. It is the first line of defense against losses, ensuring that depositors and creditors are protected. Regulatory bodies, such as the Basel Committee on Banking Supervision, mandate minimum Tier 1 capital requirements to maintain the stability of the financial system. For instance, under Basel III, banks are required to maintain a Tier 1 capital ratio of at least 6% of their risk-weighted assets. This ratio is calculated by dividing Tier 1 capital by the total risk-weighted assets, which are adjusted for credit, market, and operational risks.

When calculating the bank leverage ratio, Tier 1 capital is used in its simplest form, without risk-weighting. The leverage ratio is defined as Tier 1 capital divided by the bank's total exposure, which includes both on- and off-balance-sheet items. This approach ensures that banks maintain a sufficient capital buffer relative to their overall size and risk exposure. Unlike the Tier 1 capital ratio, the leverage ratio does not differentiate between the risk levels of different assets, providing a more conservative measure of financial stability. This simplicity makes the leverage ratio a complementary tool to the risk-weighted capital ratios, offering a clearer picture of a bank's ability to withstand shocks.

To accurately define Tier 1 capital, it is essential to exclude certain elements that do not provide long-term stability. Goodwill, intangible assets, and certain deferred tax assets are subtracted from the total because they lack the liquidity and reliability needed to absorb losses effectively. Additionally, Tier 1 capital must be of a permanent nature, meaning it does not have a maturity date or mandatory redemption features. This ensures that the capital remains available to the bank during times of financial stress. By adhering to these criteria, Tier 1 capital provides a clear and consistent measure of a bank's core financial strength.

In summary, Tier 1 capital is a fundamental concept in banking regulation, representing the highest quality capital available to absorb losses. Its definition focuses on equity, disclosed reserves, and other permanent capital elements while excluding volatile or illiquid components. Understanding Tier 1 capital is essential for calculating both the Tier 1 capital ratio and the bank leverage ratio, which are critical metrics for assessing a bank's financial health and stability. By maintaining adequate Tier 1 capital, banks can ensure they have the necessary resources to withstand adverse economic conditions and protect their stakeholders.

Effective Ways to File a Complaint with Wema Bank

You may want to see also

Explore related products

![]()

Risk-Weighted Assets Calculation

The calculation of Risk-Weighted Assets (RWAs) is a critical component in determining a bank's leverage ratio, as it provides a more nuanced view of a bank's exposure to risk compared to simply using total assets. RWAs are calculated by assigning risk weights to different types of assets based on their inherent risk levels. These risk weights are typically determined by regulatory frameworks such as Basel III, which categorizes assets into various classes with corresponding risk percentages. For instance, cash and central government bonds are often assigned a 0% risk weight due to their low risk, while corporate loans or equities might carry higher risk weights, such as 100% or more, reflecting their greater risk exposure.

To calculate RWAs, banks must first categorize their assets according to the regulatory guidelines. Each category of assets, such as loans, investments, and off-balance-sheet items like letters of credit, is assigned a specific risk weight. For example, residential mortgages might have a risk weight of 35%, while commercial loans could be weighted at 100%. Off-balance-sheet exposures are first converted into credit equivalent amounts using conversion factors, and then risk weights are applied. This process ensures that all potential risks, both on and off the balance sheet, are accounted for in the RWA calculation.

Once the assets are categorized and risk weights are assigned, the next step is to multiply the value of each asset category by its respective risk weight. For example, if a bank has $100 million in residential mortgages with a 35% risk weight, the risk-weighted value of these mortgages would be $35 million. This calculation is repeated for all asset categories, and the results are summed to obtain the total RWAs. The formula for this step can be generalized as: RWAs = Σ(Asset Value × Risk Weight).

It is important to note that certain adjustments may be required during the RWA calculation to ensure accuracy and compliance with regulatory standards. For instance, banks may need to account for credit risk mitigation techniques, such as collateral or guarantees, which can reduce the risk weights applied to specific assets. Additionally, regulatory frameworks often include floors or caps on risk weights to prevent excessive risk-taking or underestimation of risk. These adjustments are crucial for maintaining the integrity of the RWA calculation and, by extension, the bank leverage ratio.

Finally, the calculated RWAs are used in conjunction with the bank's Tier 1 capital to determine the leverage ratio. The leverage ratio is computed as Tier 1 Capital divided by RWAs, expressed as a percentage. This ratio provides a measure of a bank's ability to absorb losses relative to its risk-weighted assets. By focusing on RWAs, regulators and banks can better assess the underlying risk profile of the institution, ensuring that capital adequacy requirements are met and financial stability is maintained. Understanding and accurately calculating RWAs is therefore essential for both regulatory compliance and effective risk management in the banking sector.

Does PNC Bank Charge Foreign Transaction Fees? A Comprehensive Guide

You may want to see also

Explore related products

![]()

On-Balance Sheet Exposures

The calculation of a bank's leverage ratio is a critical aspect of assessing its financial health and stability, and it primarily revolves around understanding the bank's on-balance sheet exposures. These exposures represent the assets and liabilities that are directly recorded on the bank's balance sheet, providing a snapshot of its financial position at a given moment. When calculating the leverage ratio, the focus is on measuring the bank's total assets relative to its equity, offering insight into how much risk the bank is taking on with its capital structure.

Another crucial aspect of on-balance sheet exposures is the bank's holdings of securities, such as government bonds, corporate bonds, and equities. These investments can be more liquid than loans but still carry market and credit risks. The value of these securities can fluctuate, affecting the bank's overall asset value. Banks must carefully manage these exposures to ensure they have sufficient capital to absorb potential losses. The leverage ratio calculation includes these securities, typically at their market value, to provide a realistic view of the bank's financial leverage.

In addition to assets, on-balance sheet exposures also include various liabilities. Deposits from customers, for example, are a primary source of funding for banks and are recorded as liabilities. These deposits can be demand deposits (withdrawals allowed at any time) or time deposits (fixed-term deposits). The stability and management of these liabilities are vital, as they directly impact the bank's liquidity and overall risk profile. Other liabilities may include short-term and long-term borrowings, which also need to be considered when assessing the bank's leverage.

Calculating the leverage ratio involves summing up all on-balance sheet assets and then dividing this total by the bank's equity or capital. The resulting ratio indicates the extent to which a bank is leveraging its assets with equity. A higher ratio suggests higher leverage and potentially greater risk, as the bank is funding a larger portion of its assets with debt. Regulators often set minimum leverage ratio requirements to ensure banks maintain a healthy capital structure and can absorb losses without jeopardizing their stability. Understanding and accurately measuring on-balance sheet exposures are fundamental steps in this calculation process.

Mobile Banking: Weekend Refunds?

You may want to see also

Explore related products

![]()

Off-Balance Sheet Adjustments

One key aspect of Off-Balance Sheet Adjustments involves converting off-balance sheet items into credit equivalent amounts. This is typically done using credit conversion factors (CCFs) prescribed by regulatory frameworks such as Basel III. For example, guarantees, letters of credit, and certain derivatives are assigned specific CCFs (e.g., 100% for guarantees, 100% for confirmed letters of credit, and 0-50% for derivatives depending on their risk). These factors are multiplied by the notional amounts of the off-balance sheet items to derive their credit equivalent values, which are then added to the balance sheet exposures.

Another important adjustment relates to contingent liabilities and commitments, such as loan commitments, standby letters of credit, and unused credit lines. These items represent potential future obligations that are not yet reflected on the balance sheet but could materialize under certain conditions. Banks must estimate the likelihood of these commitments being drawn and apply appropriate CCFs to convert them into credit equivalents. This ensures that the leverage ratio captures the full extent of a bank's potential exposure, even if the obligations are not currently realized.

Lastly, banks must consider the effects of derivatives and other complex financial instruments on their leverage ratio. While derivatives are often used for hedging purposes, they can also introduce significant leverage and risk. Off-Balance Sheet Adjustments for derivatives involve calculating their exposure based on replacement cost or potential future exposure, depending on the type of derivative. This ensures that the leverage ratio reflects the economic substance of these instruments, rather than just their notional amounts.

In summary, Off-Balance Sheet Adjustments are essential for accurately calculating a bank's leverage ratio by capturing risks and exposures not directly recorded on the balance sheet. By applying credit conversion factors, accounting for contingent liabilities, addressing securitization risks, and incorporating derivatives, banks can ensure a more holistic assessment of their financial leverage. These adjustments are vital for regulatory compliance and for providing stakeholders with a true picture of a bank's risk and capital adequacy.

Reconciling Bank Statements: Ensuring Financial Data Accuracy

You may want to see also

Explore related products

![]()

Final Ratio Formula & Interpretation

The final step in calculating a bank's leverage ratio involves synthesizing the key components into a single, meaningful metric. The leverage ratio formula is straightforward: Total Exposure ÷ Tier 1 Capital. Total Exposure typically includes all on-balance-sheet assets, derivatives, and off-balance-sheet exposures (such as loan commitments), adjusted for risk factors as per regulatory guidelines. Tier 1 Capital represents the bank's core equity capital, comprising common equity, retained earnings, and certain reserves, minus intangible assets and deductions mandated by regulators. This formula yields a ratio that reflects the extent to which a bank is funded by equity versus debt.

Interpreting the leverage ratio is critical for assessing a bank's financial stability. A lower leverage ratio indicates a stronger capital position, as the bank relies less on borrowed funds and has a larger equity cushion to absorb losses. For example, a leverage ratio of 5% means that for every $100 of assets, the bank holds $5 in Tier 1 Capital. Conversely, a higher leverage ratio suggests greater financial risk, as the bank is more dependent on debt, making it vulnerable to economic downturns or asset devaluations. Regulators often set minimum leverage ratio requirements (e.g., 3% under Basel III) to ensure banks maintain sufficient capital buffers.

The leverage ratio also serves as a complementary measure to risk-weighted capital ratios like the Common Equity Tier 1 (CET1) ratio. Unlike risk-weighted ratios, the leverage ratio does not adjust assets for risk, providing a simpler, more conservative view of capital adequacy. This makes it particularly useful for identifying excessive leverage that might be masked by risk-weighting methodologies. For instance, a bank with a high CET1 ratio but a low leverage ratio may still be at risk if its assets are heavily funded by debt.

In practical terms, banks and stakeholders use the leverage ratio to make informed decisions. Investors and creditors view it as an indicator of a bank's ability to withstand financial shocks. Regulators monitor it to enforce capital requirements and prevent systemic risks. Bank management employs it to optimize capital structure, balancing growth with stability. For example, a bank with a leverage ratio above regulatory thresholds may need to raise additional capital or reduce assets to comply with standards.

Finally, while the leverage ratio is a powerful tool, it should not be interpreted in isolation. It is most effective when analyzed alongside other financial metrics, such as profitability, liquidity, and asset quality. For instance, a bank with a low leverage ratio but declining profitability may still face long-term challenges. Similarly, a high leverage ratio in a stable economic environment might be manageable, but it could become problematic during a crisis. Thus, the leverage ratio is a critical but contextual measure of a bank's financial health.

Secure Banking: How Your Phone Safeguards Your Financial Future

You may want to see also

Frequently asked questions

A bank leverage ratio measures the proportion of a bank's total assets to its equity capital. It is important because it indicates the bank's ability to withstand financial stress and protects against excessive debt, ensuring stability in the financial system.

The bank leverage ratio is calculated by dividing the bank's total exposure (assets plus off-balance-sheet exposures) by its Tier 1 capital (core equity capital). The formula is: Leverage Ratio = Total Exposure / Tier 1 Capital.

A good bank leverage ratio typically ranges between 4% and 6%, depending on regulatory requirements and the bank's risk profile. Higher ratios indicate higher risk, while lower ratios suggest stronger financial stability.

Unlike risk-weighted capital ratios (e.g., CET1 or Total Capital Ratio), the leverage ratio does not adjust assets for risk. It provides a simpler, non-risk-based measure of capital adequacy, focusing solely on total exposure relative to capital.

Yes, banks are required to maintain a minimum leverage ratio as mandated by regulatory bodies such as the Basel Committee on Banking Supervision. For example, Basel III requires a minimum leverage ratio of 3% for global systemically important banks (G-SIBs).