Calculating a bank's liquidity position is essential for assessing its ability to meet short-term financial obligations and manage cash flow effectively. This involves analyzing key metrics such as the liquidity coverage ratio (LCR), which measures a bank's high-quality liquid assets against its total net cash outflows over a 30-day stress period, and the net stable funding ratio (NSFR), which evaluates the stability of a bank's funding sources relative to its assets and off-balance-sheet activities. Additionally, cash flow projections, asset-liability management, and stress testing are critical tools to ensure the bank can withstand liquidity shocks. Accurate liquidity calculations not only comply with regulatory requirements but also safeguard the bank's financial health and maintain stakeholder confidence.

Explore related products

What You'll Learn

![]()

Cash Reserves Calculation

Calculating a bank's cash reserves is a critical component of assessing its liquidity position. Cash reserves refer to the most liquid assets a bank holds, typically in the form of physical currency, deposits with central banks, and highly liquid securities that can be quickly converted to cash without significant loss of value. These reserves are essential for meeting short-term obligations, managing daily operational needs, and ensuring stability during financial stress. To calculate cash reserves, banks must identify and quantify these highly liquid assets accurately.

The first step in cash reserves calculation is to identify the eligible assets. These typically include vault cash, which is physical currency held in the bank’s vaults, and deposits held at the central bank, such as reserves maintained to meet regulatory requirements. Additionally, highly liquid securities like Treasury bills, certificates of deposit, and other money market instruments that mature within a short period (often 30 days or less) are also considered part of cash reserves. It is crucial to exclude illiquid assets or those that cannot be readily converted to cash without significant price discounts.

Once the eligible assets are identified, the next step is to determine their market value. This involves marking these assets to market, meaning their value is adjusted to reflect current market prices. For example, Treasury bills are valued based on their current market price, while deposits at the central bank are typically valued at their face amount. Accurate valuation ensures that the cash reserves reflect the true liquidity position of the bank. If market prices are not readily available, banks may use conservative estimates to avoid overstating liquidity.

After valuing the eligible assets, the bank aggregates these amounts to arrive at the total cash reserves. This figure is then compared against the bank’s total liabilities or other regulatory benchmarks to assess liquidity adequacy. For instance, regulatory frameworks like the Liquidity Coverage Ratio (LCR) require banks to hold sufficient high-quality liquid assets, including cash reserves, to cover net cash outflows over a 30-day stress period. Thus, cash reserves calculation is not just about identifying liquid assets but also ensuring they meet regulatory and operational liquidity needs.

Finally, banks must regularly monitor and update their cash reserves calculation to reflect changes in asset values, market conditions, and operational requirements. This involves maintaining robust systems for tracking liquid assets, conducting stress tests to evaluate resilience under adverse scenarios, and ensuring compliance with regulatory standards. Effective cash reserves management is vital for maintaining confidence among depositors, creditors, and regulators, as it demonstrates the bank’s ability to meet its short-term obligations and withstand liquidity shocks.

Firearm-Friendly Banking: Where Are the Options?

You may want to see also

Explore related products

![]()

Liquid Assets Valuation

The first step in liquid assets valuation is to classify assets based on their liquidity profile. Assets are often categorized into tiers, such as Level 1 (most liquid, like cash and central bank reserves), Level 2 (highly liquid but with slightly less certainty, such as government bonds), and Level 3 (less liquid assets with limited market observability). Each tier is assigned a valuation method that aligns with its liquidity characteristics. For instance, Level 1 assets are valued at their market price, while Level 2 assets may require models or observable market data for valuation. Level 3 assets, being the least liquid, often necessitate more complex valuation techniques, including discounted cash flow models or appraisals.

Once assets are categorized, the next step is to apply appropriate valuation techniques. Market prices are the preferred method for liquid assets due to their reliability and transparency. However, when market prices are unavailable or unreliable, banks may use valuation models that incorporate factors such as interest rates, credit spreads, and maturity profiles. It is essential to ensure that these models are regularly calibrated and validated to maintain accuracy. Additionally, banks must account for haircuts or discounts when valuing liquid assets to reflect potential losses in a forced liquidation scenario, especially during stressed market conditions.

Another critical aspect of liquid assets valuation is the consideration of currency and market risks. Banks operating in multiple jurisdictions must value assets in their respective currencies and account for exchange rate fluctuations. Similarly, market risks, such as interest rate changes or credit spreads, must be factored into the valuation process to ensure the bank’s liquidity position remains robust under various scenarios. Stress testing and scenario analysis are often employed to assess how liquid assets would perform under adverse conditions, providing a more comprehensive view of the bank’s liquidity resilience.

Finally, regulatory requirements play a significant role in liquid assets valuation. Banks must adhere to guidelines set by regulatory bodies such as the Basel Committee on Banking Supervision, which mandates specific liquidity ratios like the Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR). These ratios require banks to hold a sufficient amount of high-quality liquid assets (HQLA) to cover short-term cash outflows. Compliance with these regulations necessitates rigorous valuation practices, regular reporting, and transparency in how liquid assets are assessed and reported. Accurate liquid assets valuation not only ensures regulatory compliance but also enhances stakeholder confidence in the bank’s ability to manage liquidity risks effectively.

Best US-Based Seed Banks: Where to Source Your Seeds

You may want to see also

Explore related products

![]()

Liabilities Assessment

Assessing a bank's liabilities is a critical component in calculating its liquidity position, as it provides insight into the bank's funding sources and potential cash outflows. Liabilities represent the bank's obligations, including customer deposits, borrowings, and other debts, which must be carefully managed to ensure sufficient liquidity. The first step in liabilities assessment is to categorize and quantify all liability accounts. This involves identifying demand deposits, savings accounts, time deposits, and other customer liabilities, each with different withdrawal patterns and stability. For instance, demand deposits are typically more volatile and can be withdrawn at any time, while time deposits have fixed terms, providing a more stable funding source.

A key aspect of this assessment is analyzing the maturity structure of the bank's liabilities. This entails creating a liability maturity ladder or schedule, which outlines the timing of expected cash outflows. By matching this schedule with the bank's asset maturity profile, liquidity managers can identify potential funding gaps or surpluses. For example, a bank with a significant portion of short-term liabilities maturing in the next quarter should ensure it has enough liquid assets or alternative funding sources to meet these obligations. This maturity analysis is crucial for understanding the bank's ability to cover short-term and long-term liabilities.

Another important consideration is the cost and stability of funding sources. Different types of liabilities carry varying interest expenses and levels of reliability. Wholesale funding, such as large certificates of deposit or interbank borrowings, might be more costly and less stable compared to retail deposits. Assessing the concentration and diversity of funding sources is essential. A bank heavily reliant on a few large depositors or a specific type of funding may face higher liquidity risks. Therefore, a comprehensive liabilities assessment should include an analysis of funding costs, stability, and diversification.

Furthermore, off-balance-sheet items and contingent liabilities should not be overlooked. These include items like letters of credit, loan commitments, and derivatives, which can potentially impact a bank's liquidity. While they may not be immediate cash outflows, these obligations can materialize under certain conditions, affecting the bank's overall liquidity position. A thorough assessment should consider the likelihood and potential magnitude of these contingent liabilities becoming actual cash outflows.

In summary, liabilities assessment is a multifaceted process that involves categorizing and analyzing various types of bank obligations. It requires a detailed examination of maturity structures, funding costs, and the stability and diversity of liability sources. By understanding its liabilities, a bank can better manage its liquidity, ensuring it has the necessary funds to meet obligations as they come due, thereby maintaining financial stability and confidence among depositors and investors. This assessment is a fundamental step in the broader process of calculating and managing a bank's liquidity position.

Banking Tel Var Stones: A Step-by-Step Guide for Efficient Storage

You may want to see also

Explore related products

![]()

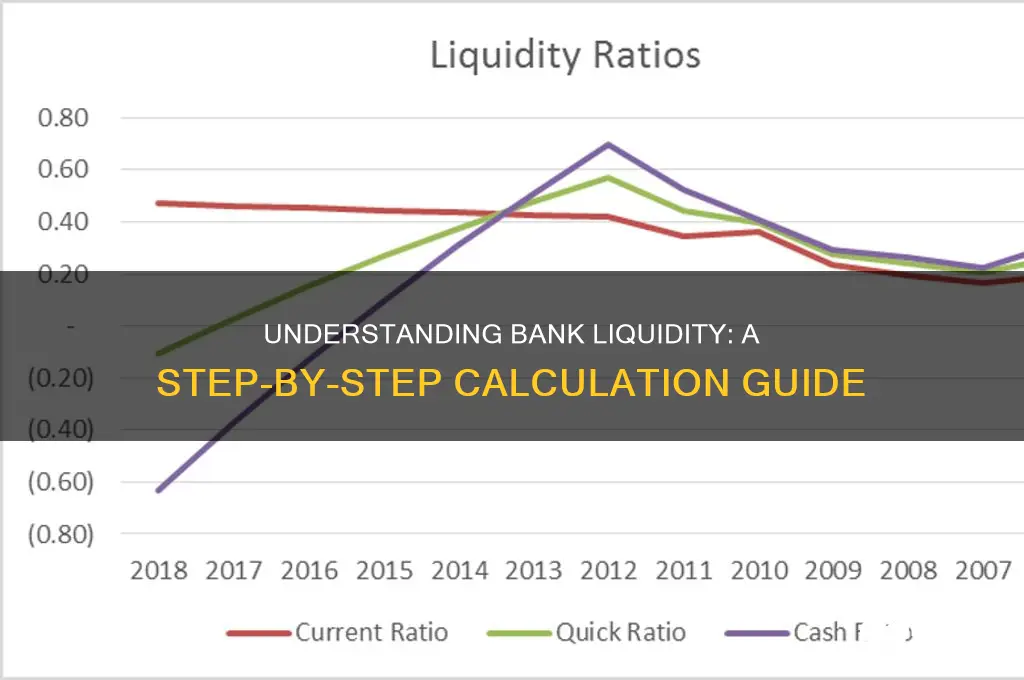

Liquidity Ratios Analysis

Liquidity ratios are essential tools for assessing a bank's ability to meet its short-term obligations and manage its liquidity position effectively. These ratios provide insights into the bank's capacity to convert assets into cash quickly without significant loss, ensuring it can honor deposit withdrawals, settle liabilities, and maintain operational stability. The primary liquidity ratios used in banking include the Current Ratio, Quick Ratio, Cash Ratio, and Net Stable Funding Ratio (NSFR). Each ratio offers a unique perspective on different aspects of a bank's liquidity profile, and analyzing them collectively provides a comprehensive view of its financial health.

The Current Ratio is calculated by dividing a bank's current assets by its current liabilities. For banks, current assets typically include cash, marketable securities, and short-term loans, while current liabilities encompass customer deposits and short-term borrowings. A current ratio above 1 indicates that the bank has sufficient liquid assets to cover its short-term liabilities. However, since banks operate with a high proportion of liabilities, a ratio significantly above 1 may not always be practical or necessary. Instead, regulators and analysts often focus on the composition and quality of assets to ensure they can be readily converted to cash.

The Quick Ratio (or Acid-Test Ratio) is a more stringent measure of liquidity, as it excludes inventory and other less liquid assets from current assets. For banks, this ratio focuses on cash, marketable securities, and accounts receivable. The quick ratio provides a clearer picture of a bank's immediate liquidity position, as it only considers assets that can be quickly converted to cash. A quick ratio above 1 is generally considered healthy, but banks often maintain lower ratios due to the nature of their operations, relying instead on stable funding sources and access to liquidity markets.

The Cash Ratio is the most conservative liquidity metric, calculated by dividing only cash and cash equivalents by current liabilities. This ratio reflects a bank's ability to meet its obligations using its most liquid assets. While a higher cash ratio is desirable, banks typically maintain lower levels to optimize returns on assets. However, during times of financial stress, a higher cash ratio becomes critical to ensure the bank can withstand liquidity shocks.

Lastly, the Net Stable Funding Ratio (NSFR) is a regulatory liquidity ratio introduced under Basel III to ensure banks maintain a stable funding profile relative to the composition of their assets and off-balance-sheet activities. The NSFR is calculated by dividing available stable funding by required stable funding. A ratio of 100% or higher indicates that a bank has sufficient stable funding to support its assets and risk exposures over a one-year horizon. This ratio is particularly important for assessing a bank's resilience to medium-term liquidity risks.

In conclusion, liquidity ratios analysis is a critical component of evaluating a bank's liquidity position. By examining the current ratio, quick ratio, cash ratio, and NSFR, stakeholders can gain a detailed understanding of a bank's ability to manage short-term and medium-term liquidity risks. These ratios, when analyzed in conjunction with other financial metrics and qualitative factors, provide a robust framework for assessing a bank's overall liquidity health and its capacity to navigate adverse market conditions.

Does MoneyKey Automatically Withdraw Payments From Your Bank Account?

You may want to see also

Explore related products

![]()

Stress Testing Methods

Stress testing is a critical component in assessing a bank's liquidity position, as it evaluates the institution's ability to withstand adverse financial scenarios. One widely used method is the Scenario Analysis, where banks simulate extreme but plausible events such as economic recessions, market crashes, or funding shocks. In this approach, banks project their liquidity position under these scenarios by estimating cash inflows and outflows, considering factors like deposit withdrawals, loan drawdowns, and asset sales. The goal is to determine if the bank can meet its obligations without breaching regulatory liquidity thresholds. For instance, a bank might model a scenario where interbank lending freezes, forcing it to rely solely on retail deposits and liquid assets.

Another method is Sensitivity Analysis, which examines how changes in key variables affect liquidity. This involves adjusting parameters such as deposit runoff rates, funding costs, or market liquidity conditions to assess their impact on the bank's liquidity position. For example, a bank might test the effect of a 20% increase in deposit withdrawals over a short period. By quantifying these sensitivities, banks can identify vulnerabilities and implement mitigating strategies, such as maintaining higher levels of high-quality liquid assets (HQLA) or diversifying funding sources.

Historical Stress Testing is a third method that relies on past financial crises to evaluate a bank's resilience. Banks analyze their liquidity performance during previous downturns, such as the 2008 global financial crisis, and apply those lessons to current conditions. This approach helps identify patterns and potential weaknesses that may re-emerge in similar future scenarios. For instance, a bank might assess how its liquidity position would fare if funding markets tighten as they did during the 2008 crisis.

A more advanced technique is Reverse Stress Testing, which identifies the extreme conditions under which a bank would fail to meet its liquidity needs. Unlike traditional stress testing, which starts with predefined scenarios, reverse stress testing works backward to determine the worst-case scenario that would exhaust the bank's liquidity resources. This method helps banks understand their breaking points and develop contingency plans to avoid such outcomes. For example, a bank might calculate the combination of deposit outflows, asset devaluations, and funding disruptions that would deplete its liquidity buffer.

Lastly, Dynamic Stress Testing incorporates time-varying factors and behavioral responses into the analysis. This method recognizes that liquidity conditions evolve over time and that market participants' behaviors can amplify stress. For instance, a bank might model how a gradual loss of confidence in the financial system could lead to a self-reinforcing cycle of funding withdrawals and asset fire sales. By accounting for these dynamics, banks can gain a more realistic understanding of their liquidity risks and take proactive measures to enhance their resilience.

Incorporating these stress testing methods into liquidity assessments allows banks to comprehensively evaluate their ability to navigate adverse conditions. By combining scenario analysis, sensitivity analysis, historical and reverse stress testing, and dynamic modeling, banks can identify potential liquidity shortfalls, strengthen their risk management frameworks, and ensure compliance with regulatory requirements. Regular and rigorous stress testing is essential for maintaining financial stability and safeguarding the bank's long-term viability.

Citizens Bank Business Debit Card: Does It Offer Rewards Points?

You may want to see also

Frequently asked questions

A bank's liquidity position refers to its ability to meet short-term financial obligations by converting assets into cash without significant loss. It is crucial for maintaining stability, ensuring depositors' confidence, and complying with regulatory requirements.

A bank's liquidity position is calculated using ratios such as the liquidity coverage ratio (LCR) and net stable funding ratio (NSFR), which compare high-quality liquid assets (HQLA) to short-term liabilities and stable funding sources, respectively.

The LCR measures a bank's ability to survive a 30-day stress period. It is computed as:

LCR = (High-Quality Liquid Assets) / (Total Net Cash Outflows over 30 days). Regulators typically require an LCR of 100% or higher.

HQLA are assets that can be easily and immediately converted into cash with minimal loss of value, such as cash, central bank reserves, and government securities. They are critical for maintaining liquidity during stress periods.

A bank can improve its liquidity position by increasing HQLA, diversifying funding sources, reducing reliance on short-term wholesale funding, and implementing robust liquidity risk management practices. Regular stress testing and monitoring also help.