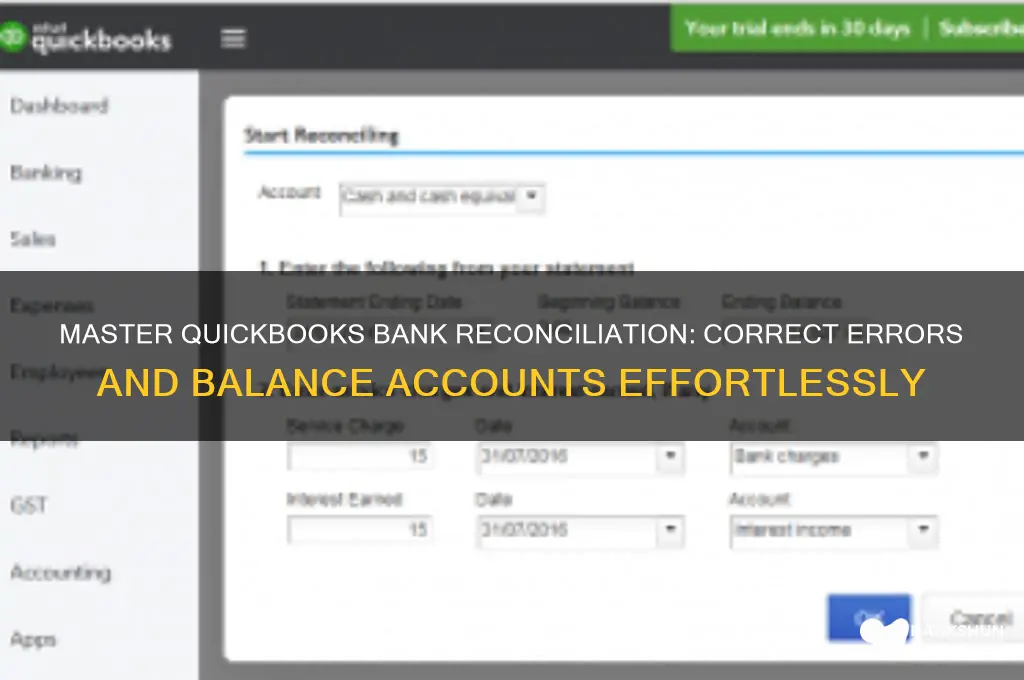

Correcting bank reconciliation in QuickBooks is a critical task for maintaining accurate financial records and ensuring that your business’s books align with your bank statements. Errors in reconciliation can arise from mismatched transactions, duplicate entries, or overlooked adjustments, leading to discrepancies between QuickBooks and your bank account. To correct these issues, start by reviewing the reconciliation report to identify discrepancies, then manually compare each transaction in QuickBooks with your bank statement. If you find unmatched transactions, verify their accuracy and re-enter or delete them as needed. Additionally, ensure that uncleared transactions are properly recorded and adjust opening balances if necessary. QuickBooks provides tools like the Reconcile feature and transaction detail reports to assist in this process. By systematically addressing errors and maintaining meticulous attention to detail, you can restore the integrity of your financial data and ensure smooth future reconciliations.

Explore related products

What You'll Learn

- Identify discrepancies: Compare bank statements with QuickBooks records to find unmatched transactions

- Adjust opening balance: Correct errors in the starting balance of the reconciliation

- Clear uncleared transactions: Mark cleared items and remove duplicates in the register

- Fix missing entries: Add omitted transactions to QuickBooks to match bank records

- Re-reconcile steps: Redo reconciliation, ensuring all corrections are accurately applied

![]()

Identify discrepancies: Compare bank statements with QuickBooks records to find unmatched transactions

To identify discrepancies in your bank reconciliation within QuickBooks, the first step is to gather both your bank statement and your QuickBooks records for the same period. Ensure that the date range you are reviewing is identical in both documents to maintain accuracy. Open your QuickBooks account and navigate to the Banking menu, then select the account you wish to reconcile. Here, you will find the transactions recorded in QuickBooks. Simultaneously, have your bank statement ready, either in physical or digital format, to facilitate a side-by-side comparison.

Begin by meticulously comparing each transaction listed on your bank statement with those recorded in QuickBooks. Start with the deposits or credits on the bank statement and match them against the income or deposit entries in QuickBooks. Pay close attention to the dates and amounts to ensure they align. If a transaction appears on the bank statement but is missing in QuickBooks, note it as an unmatched transaction. Similarly, if there are entries in QuickBooks that do not appear on the bank statement, flag these as well. This process requires patience and attention to detail to ensure no discrepancies are overlooked.

Next, review the withdrawals or debits on the bank statement and cross-reference them with the expenses or payments recorded in QuickBooks. Again, focus on matching dates and amounts to identify any inconsistencies. Common discrepancies include uncleared checks, automatic bank fees not recorded in QuickBooks, or transactions that were entered incorrectly in either the bank statement or QuickBooks. Make a list of all unmatched transactions, noting whether they are missing from QuickBooks or the bank statement, and the specific details of each transaction, such as date, amount, and description.

Once you have identified all discrepancies, categorize them to understand their nature. For example, some unmatched transactions may be due to timing differences, where a transaction has been recorded in one system but not yet in the other. Others may be errors, such as duplicate entries, incorrect amounts, or omitted transactions. By categorizing these discrepancies, you can prioritize which issues to address first. For instance, timing differences may resolve themselves as transactions clear, while errors will require immediate correction to ensure accurate financial records.

Finally, document all identified discrepancies in a clear and organized manner. Use a spreadsheet or QuickBooks’ reconciliation tools to track each unmatched transaction, its status (e.g., missing, incorrect, timing difference), and any actions taken to resolve it. This documentation will not only help you correct the current reconciliation but also serve as a reference for future reconciliations. By systematically comparing bank statements with QuickBooks records and carefully identifying discrepancies, you lay the foundation for an accurate and efficient bank reconciliation process.

Central Bank's Role: Regulating and Supervising Commercial Banking Operations

You may want to see also

Explore related products

![]()

Adjust opening balance: Correct errors in the starting balance of the reconciliation

When addressing errors in the opening balance of a bank reconciliation in QuickBooks, it’s crucial to first identify the source of the discrepancy. Start by reviewing the previous reconciliation report to confirm the ending balance, as this becomes the opening balance for the current reconciliation. If the opening balance is incorrect, it often stems from an error in the prior reconciliation, such as an unmatched transaction or an incorrect adjustment. To correct this, navigate to the "Banking" menu in QuickBooks and select the account you’re reconciling. Review the "Beginning Balance" field and compare it to your bank statement to pinpoint the discrepancy.

Once you’ve identified the error, adjust the opening balance directly in the reconciliation window. In QuickBooks Desktop, go to the "Reconcile" screen and locate the "Beginning Balance" field. Enter the correct amount based on your bank statement or previous reconciliation. If the error was caused by a missing or incorrect transaction, you may need to add or edit the transaction in the register before adjusting the balance. Ensure that all transactions up to the statement date are accurately recorded to avoid further discrepancies.

In QuickBooks Online, the process is slightly different. Access the reconciliation screen by going to "Accounting" and then "Chart of Accounts." Select the bank account and click "Reconcile." If the opening balance is incorrect, you’ll need to undo the previous reconciliation first. To do this, locate the last reconciliation in the "History" tab, click "Undo," and confirm the action. Once undone, re-enter the correct opening balance and proceed with the reconciliation, ensuring all transactions are matched correctly.

After adjusting the opening balance, carefully review the reconciliation to ensure all transactions are accounted for and matched. If the discrepancy was due to an omitted transaction, add it to the register and ensure it appears in the reconciliation. For example, if a deposit was missed, create a new transaction in the register and categorize it appropriately. Once all corrections are made, complete the reconciliation and compare the ending balance to your bank statement to confirm accuracy.

Finally, document the adjustments made to the opening balance for future reference. This can be done by adding a memo or note in the reconciliation window or by creating a separate document detailing the corrections. Regularly reviewing and correcting opening balances ensures the integrity of your financial records and prevents compounding errors in future reconciliations. By following these steps, you can effectively correct errors in the starting balance and maintain accurate bank reconciliations in QuickBooks.

Understanding the Steepness of a 20-Degree Banked Surface

You may want to see also

Explore related products

![]()

Clear uncleared transactions: Mark cleared items and remove duplicates in the register

To effectively clear uncleared transactions in QuickBooks, start by accessing your bank register. Navigate to the "Banking" menu, select "Banking" again, and then choose the appropriate account. Once in the register, locate the transactions that have been cleared by your bank but are still marked as uncleared in QuickBooks. To mark these items as cleared, click on the first transaction you want to update. In the "Cleared" column, you’ll see a checkbox or an icon (often a checkmark or a circle). Click on it to mark the transaction as cleared. Repeat this process for all cleared transactions that are still uncleared in the register. This step ensures that your QuickBooks register accurately reflects the actual cleared status of your bank transactions.

Next, identify and remove any duplicate transactions in the register. Duplicates can occur due to errors in data entry or syncing issues. Scan the register for transactions with identical dates, amounts, and payees. Once identified, select the duplicate transaction by clicking on it. Right-click and choose "Delete" or use the keyboard shortcut (usually "Ctrl + D") to remove it. Be cautious to delete only true duplicates and not legitimate transactions. Removing duplicates ensures that your register is clean and accurate, which is crucial for a successful bank reconciliation.

After marking cleared items and removing duplicates, verify the changes by reviewing the register. Ensure that all cleared transactions are correctly marked and that no duplicates remain. You can also run a reconciliation report to double-check your work. To do this, go to the "Banking" menu, select "Reconcile," and choose the account you’re working on. Compare the beginning balance, ending balance, and cleared transactions to your bank statement. If everything matches, your register is now accurately updated.

If you encounter discrepancies during the verification process, revisit the register to identify any missed uncleared transactions or lingering duplicates. Sometimes, transactions may be partially cleared or incorrectly categorized. Use the search function in the register to locate specific transactions by date, amount, or payee. Correct any errors by marking the appropriate transactions as cleared or deleting additional duplicates. Consistency and attention to detail are key to ensuring your QuickBooks register aligns with your bank statement.

Finally, save your changes and close the register. QuickBooks automatically updates the account information based on the modifications you’ve made. To ensure the changes are reflected in future reconciliations, perform a test reconciliation. Go to the "Banking" menu, select "Reconcile," and follow the prompts to complete the process. If the reconciliation matches your bank statement without discrepancies, you’ve successfully cleared uncleared transactions and removed duplicates. Regularly maintaining your register in this manner will streamline future reconciliations and keep your financial records accurate.

Challenging Yet Rewarding: Exploring the Banks Peninsula Track's Difficulty

You may want to see also

Explore related products

![]()

Fix missing entries: Add omitted transactions to QuickBooks to match bank records

When addressing missing entries in QuickBooks to correct bank reconciliation, the first step is to identify the omitted transactions by comparing your bank statement with the transactions recorded in QuickBooks. Look for any discrepancies where transactions appear on the bank statement but are missing in QuickBooks. Common examples include deposits, checks, fees, or electronic transfers that were overlooked. Once identified, gather all necessary details such as the date, amount, payee, and transaction type to ensure accuracy when adding them to QuickBooks.

To add the missing transactions, navigate to the appropriate transaction entry screen in QuickBooks. For deposits, go to the "Banking" menu and select "Make Deposits" or "Bank Deposit." For checks or expenses, use the "Write Checks" or "Expense" transaction forms. Enter the missing transaction details carefully, ensuring the date, amount, and account match the bank statement. If the transaction involves a specific category or account, assign it correctly to maintain proper categorization in your financial records. Save each transaction as you complete it to ensure it is recorded in QuickBooks.

After adding the missing entries, verify that they are correctly reflected in the bank register within QuickBooks. Go to the "Banking" menu, select "Use Register," and choose the appropriate bank account. Scroll through the register to confirm that the newly added transactions appear and match the bank statement. If any errors are found, such as incorrect amounts or dates, edit the transaction by double-clicking on it and making the necessary corrections. Accuracy at this stage is crucial to ensure the reconciliation process aligns with the bank records.

Once all missing transactions are added and verified, proceed to reconcile the bank account in QuickBooks. Go to the "Banking" menu, select "Reconcile," and choose the account you are working on. Enter the ending balance and statement date from your bank statement. QuickBooks will now compare the recorded transactions with the statement. If the missing entries were added correctly, the reconciliation should balance, indicating that QuickBooks now matches the bank records. If discrepancies remain, revisit the added transactions to ensure no errors were made.

Finally, maintain a record of the adjustments made during this process for future reference. Document the missing transactions that were added and any corrections performed. This documentation will be helpful if similar issues arise in the future or during audits. Regularly reviewing and updating your transactions in QuickBooks can prevent missing entries and make the reconciliation process smoother. By diligently adding omitted transactions and ensuring accuracy, you can maintain reliable financial records and streamline bank reconciliation in QuickBooks.

Exploring the Vast Number of Banks Operating in the USA

You may want to see also

Explore related products

![Quick Books Desktop Pro Plus 2024 | LIFETIME Version | USB | Only for Mac [software_key_card]](https://m.media-amazon.com/images/I/41xG2aOWLLL._AC_UL320_.jpg)

![]()

Re-reconcile steps: Redo reconciliation, ensuring all corrections are accurately applied

To re-reconcile your bank account in QuickBooks, you must first undo the previous reconciliation and then redo it, ensuring all corrections are accurately applied. Start by navigating to the Banking menu and selecting the account you need to correct. From the Account History section, locate the statement ending date of the reconciliation you want to fix. Click the small arrow next to the reconciliation entry and select "Undo Reconciliation." This step is crucial as it clears the previous reconciliation, allowing you to start fresh with the correct data. Confirm the action when prompted, understanding that this will remove all previously reconciled transactions for that period.

Once the reconciliation is undone, review the transactions within the statement period to identify and correct any discrepancies. Ensure that all uncleared transactions are accurately recorded and that any missing or incorrect entries are added or amended. This may involve matching uncleared transactions to the bank statement, adding missing deposits or withdrawals, and correcting any misclassified transactions. Take this opportunity to double-check that all transactions are categorized correctly to maintain accurate financial records. QuickBooks allows you to filter transactions by date, making it easier to focus on the specific period you are reconciling.

After making the necessary corrections, proceed to redo the reconciliation. Go back to the Banking menu, select the account, and click "Reconcile Now." Enter the correct statement ending date and balance from your bank statement. QuickBooks will display the updated list of transactions for the period. Carefully review each transaction, ensuring that all corrections are reflected and that the cleared status is accurate. Mark each transaction that has cleared the bank by checking the box in the "C" column. The difference between the cleared balance and the statement balance should now match, indicating that your corrections have been applied correctly.

As you reconcile, pay close attention to the running balance and the ending balance displayed by QuickBooks. If discrepancies persist, re-examine the transactions for any overlooked errors or omissions. Common issues include duplicate entries, incorrect amounts, or transactions assigned to the wrong account. Once all transactions are correctly marked and the difference is zero, complete the reconciliation by clicking "Reconcile Now." QuickBooks will prompt you to confirm the reconciliation and provide an option to print or save a reconciliation report for your records.

Finally, after re-reconciling, it’s essential to verify the accuracy of the process. Run a reconciliation report to ensure that all transactions are properly accounted for and that the ending balance matches your bank statement. If everything aligns, your bank reconciliation in QuickBooks is now corrected. Regularly reviewing and reconciling your accounts will help maintain the integrity of your financial data and prevent future discrepancies. By following these re-reconcile steps meticulously, you can ensure that all corrections are accurately applied and that your financial records remain reliable.

Citing the World Bank in Harvard Style: A Comprehensive Guide

You may want to see also

Frequently asked questions

To identify discrepancies, compare your bank statement transactions with those recorded in QuickBooks. Look for missing, duplicate, or incorrectly entered transactions. Use the "Reconcile" tool to highlight unmatched items and review uncleared transactions.

First, locate the incorrect transaction by reviewing the reconciliation report. Then, void or delete the erroneous entry, re-enter it correctly, and adjust the beginning balance if necessary. Finally, rerun the reconciliation to ensure accuracy.

Yes, you can undo a reconciliation by locating the reconciled transaction in the register, clicking "Edit Transaction," and unchecking the "Reconciled" box. For previous periods, you may need to contact QuickBooks support or manually adjust entries.

To adjust the beginning balance, go to the "Reconcile" screen, enter the correct opening balance in the "Beginning Balance" field, and proceed with the reconciliation. Ensure all transactions are accurately recorded before finalizing.

![QuickBooks Online for Beginners Bible Edition [2 Books in 1]: The Ultimate Fast Learning Guide for QBO, filled with Step-by-Step Illustrated Explanations, Practical Examples and Common Problem Solving](https://m.media-amazon.com/images/I/61WWhskpzAL._AC_UL320_.jpg)