Bank reconciliation is a critical process for ensuring the accuracy of financial records by comparing a company’s internal accounting records with the bank statement provided by the financial institution. A bank reconciliation template serves as a structured tool to streamline this process, helping identify discrepancies such as outstanding checks, deposits in transit, bank fees, or errors. Typically, the template includes sections for recording the bank statement balance, adding deposits not yet credited, subtracting outstanding payments, and adjusting for bank charges or interest. By systematically reconciling these items, businesses can maintain financial integrity, detect fraud, and ensure compliance with accounting standards. Utilizing a well-designed template not only saves time but also minimizes errors, making it an essential practice for effective financial management.

| Characteristics | Values |

|---|---|

| Purpose | To compare and match the bank statement with the company's accounting records. |

| Frequency | Monthly, quarterly, or as needed. |

| Key Components | Bank statement balance, company's cash account balance, outstanding checks, deposits in transit, bank errors, company errors. |

| Steps | 1. Gather bank statement and company records. 2. Compare ending balances. 3. Identify discrepancies. 4. Adjust for outstanding items. 5. Reconcile and document. |

| Tools | Excel, Google Sheets, accounting software (e.g., QuickBooks, Xero). |

| Template Format | Table format with columns for date, description, bank statement amount, company records amount, and adjustments. |

| Adjustments | Deposits in transit, outstanding checks, bank fees, interest, errors. |

| Documentation | Reconciliation report, notes on discrepancies, and corrective actions. |

| Best Practices | Double-check entries, maintain consistency, and review regularly. |

| Common Errors | Missed transactions, incorrect amounts, duplicate entries, timing differences. |

| Outcome | Ensures accuracy of financial records and identifies discrepancies or fraud. |

Explore related products

What You'll Learn

- Gather Statements: Collect bank and accounting records for the same period

- Match Transactions: Compare and align entries from both statements

- Identify Discrepancies: Note unmatched or missing transactions for investigation

- Adjust Entries: Correct accounting records to reflect accurate balances

- Finalize Report: Document reconciled balances and unresolved discrepancies

![]()

Gather Statements: Collect bank and accounting records for the same period

The foundation of any bank reconciliation lies in accurate, complete data. Before you begin matching transactions or identifying discrepancies, you need to gather the right statements. This means collecting both your bank statement and your internal accounting records for the exact same period. Think of it as aligning two puzzle pieces – they must cover the identical timeframe to fit together seamlessly.

Mismatched dates will lead to confusion, errors, and ultimately, a failed reconciliation.

Let's break down the process. First, obtain your bank statement for the period in question. Most banks provide digital statements accessible through online banking platforms. Download the PDF or Excel version for easy manipulation. If you prefer physical copies, request a printed statement from your bank. Ensure the statement includes all transactions, from the opening balance to the closing balance, along with any fees, interest, or adjustments. Simultaneously, extract your accounting records for the corresponding period. This could be from your accounting software, spreadsheets, or even a manual ledger. The key is to have a detailed list of all income, expenses, and transfers recorded during the same timeframe as your bank statement.

Pro Tip: If your accounting software allows, export the data in a format compatible with your bank statement (e.g., CSV or Excel) for easier comparison later.

Now, a word of caution: be meticulous about date ranges. Even a one-day discrepancy can throw off your entire reconciliation. Double-check that both your bank statement and accounting records start and end on the exact same dates. If there's a mismatch, adjust your accounting records to align perfectly. Remember, you're aiming for a snapshot of financial activity during a specific window, not a general overview.

Example: If your bank statement covers January 1st to January 31st, your accounting records must also reflect transactions from January 1st to January 31st, no more, no less.

Finally, consider the frequency of your reconciliations. Monthly reconciliations are standard, but quarterly or annual reconciliations might be suitable for less active accounts. The key is consistency. Regular reconciliations not only help catch errors early but also provide a clearer picture of your financial health. By diligently gathering statements for the same period, you lay the groundwork for a smooth and accurate bank reconciliation process.

Traveling Soon? How to Notify Your Bank About Your Trip

You may want to see also

Explore related products

![]()

Match Transactions: Compare and align entries from both statements

Matching transactions is the linchpin of bank reconciliation, where the goal is to ensure every entry in your records mirrors its counterpart in the bank statement. Begin by organizing both sets of documents chronologically, aligning dates as closely as possible. Start with the oldest transaction and work your way forward, marking matches with a checkmark or highlight to avoid duplication. For example, if your ledger shows a $300 deposit on October 5th, locate the same amount and date on the bank statement. This methodical approach minimizes errors and provides a clear audit trail.

When discrepancies arise, investigate systematically. Unmatched entries often stem from timing differences, such as deposits in transit or outstanding checks. For instance, a $500 check issued on October 1st may not appear on the bank statement until October 7th if it was delayed in processing. Cross-reference these with supporting documents like receipts or invoices to confirm their legitimacy. If an entry remains unmatched after scrutiny, flag it for further review—it could indicate an error, fraud, or unrecorded transaction.

Technology can streamline this process significantly. Utilize spreadsheet software like Excel or Google Sheets to create a reconciliation template with columns for dates, descriptions, amounts, and status (matched/unmatched). Formulas such as VLOOKUP or conditional formatting can automatically identify discrepancies, saving time and reducing manual effort. For businesses, accounting software like QuickBooks or Xero often includes built-in reconciliation tools that sync directly with bank feeds, making matching transactions nearly effortless.

Despite automation, human oversight remains critical. For example, a $1,200 vendor payment might be recorded as $120 in your ledger due to a typo—a mistake software might miss. Always review matched transactions for reasonableness, ensuring amounts and descriptions align logically. Additionally, maintain a reconciliation log detailing unresolved items and their resolution status. This not only aids in tracking progress but also serves as a reference for future reconciliations, helping identify recurring issues or patterns.

In conclusion, matching transactions demands precision, patience, and a blend of manual and digital techniques. By organizing documents, investigating discrepancies, leveraging technology, and maintaining vigilance, you can ensure your financial records accurately reflect your bank’s statements. This process not only safeguards against errors but also provides a foundation for sound financial management and decision-making.

Why I Want to Be a Banker

You may want to see also

Explore related products

![]()

Identify Discrepancies: Note unmatched or missing transactions for investigation

Unmatched or missing transactions are the red flags of bank reconciliation, signaling potential errors, oversights, or even fraud. These discrepancies arise when your internal records don’t align with the bank’s statement, creating a gap that demands investigation. Identifying them is critical, as unresolved discrepancies can distort financial reporting, lead to cash flow issues, or indicate deeper operational problems.

Begin by systematically comparing each transaction in your ledger to the bank statement, marking off matches and flagging those that don’t align. Use a color-coded system or a dedicated column in your reconciliation template to highlight unmatched entries. For example, transactions recorded in your books but absent from the bank statement (uncleared items) should be noted separately from those appearing on the statement but not in your records (unrecorded deposits or fees).

Investigate flagged discrepancies promptly. Common causes include timing differences (e.g., checks issued but not yet cashed), bank errors (e.g., incorrect posting of amounts), or oversight in recording transactions. For instance, a $500 deposit recorded in your ledger but missing from the bank statement could be due to a delay in processing, while a $200 bank fee not in your records might require updating your expense tracking.

Leverage tools like accounting software or spreadsheet formulas to streamline the process. For example, Excel’s VLOOKUP function can help identify unmatched transactions between your ledger and the bank statement. Additionally, maintain a running log of discrepancies and their resolutions to track patterns and improve future reconciliations.

Finally, treat discrepancies as opportunities for process improvement. Recurring issues, such as frequent timing differences, may indicate a need to adjust your reconciliation frequency or communication with the bank. By systematically identifying and addressing these gaps, you not only ensure accuracy but also strengthen your financial controls.

Impala Sensor Issues: Bank 2 Sensors in 2000 Models

You may want to see also

Explore related products

![]()

Adjust Entries: Correct accounting records to reflect accurate balances

Discrepancies between your bank statement and accounting records aren't uncommon. They arise from timing differences, errors, or overlooked transactions. Adjusting entries is the process of identifying and correcting these discrepancies to ensure your books accurately reflect your financial reality. Think of it as fine-tuning your financial data to achieve harmony between your internal records and external bank statements.

Unrecorded transactions are a prime culprit for discrepancies. Perhaps a check you issued hasn't cleared yet, or a deposit hasn't been processed by the bank. In these cases, adjusting entries are necessary to recognize these transactions in your accounting system, even if they haven't yet appeared on your bank statement. For instance, if you wrote a check for office supplies on the 28th, but it hasn't cleared by month-end, you'd need to debit your office supplies expense account and credit your checking account for the amount of the check.

Bank fees, interest earned, and automatic deductions can also create discrepancies. These items often appear on your bank statement but might not be reflected in your accounting software. Adjusting entries are required to record these transactions. For example, if your bank statement shows a monthly service charge of $25, you'd debit your bank service charges expense account and credit your checking account for $25.

Similarly, errors in recording transactions can lead to imbalances. A simple typo in an amount or an incorrect account selection can throw off your reconciliation. Careful review of both your accounting records and bank statement is crucial to identify these errors. Once identified, correcting entries are made to rectify the mistake. This might involve reversing the original incorrect entry and recording the correct one.

Remember, adjusting entries are not about manipulating numbers but about ensuring the accuracy and integrity of your financial data. They are a vital step in the bank reconciliation process, providing a clear picture of your financial position and allowing for informed decision-making. By diligently identifying and correcting discrepancies through adjusting entries, you maintain the reliability of your accounting records and gain a true understanding of your financial health.

Trump's Bankruptcies: Unraveling the Frequency of His Financial Declares

You may want to see also

Explore related products

![Microsoft Office Home 2024 | Classic Apps: Word, Excel, PowerPoint | One-Time Purchase for 1 PC/MAC | Instant Download | Formerly Home & Student 2021 [PC/Mac Online Code]](https://m.media-amazon.com/images/I/61phY52G-OL._AC_UL320_.jpg)

![]()

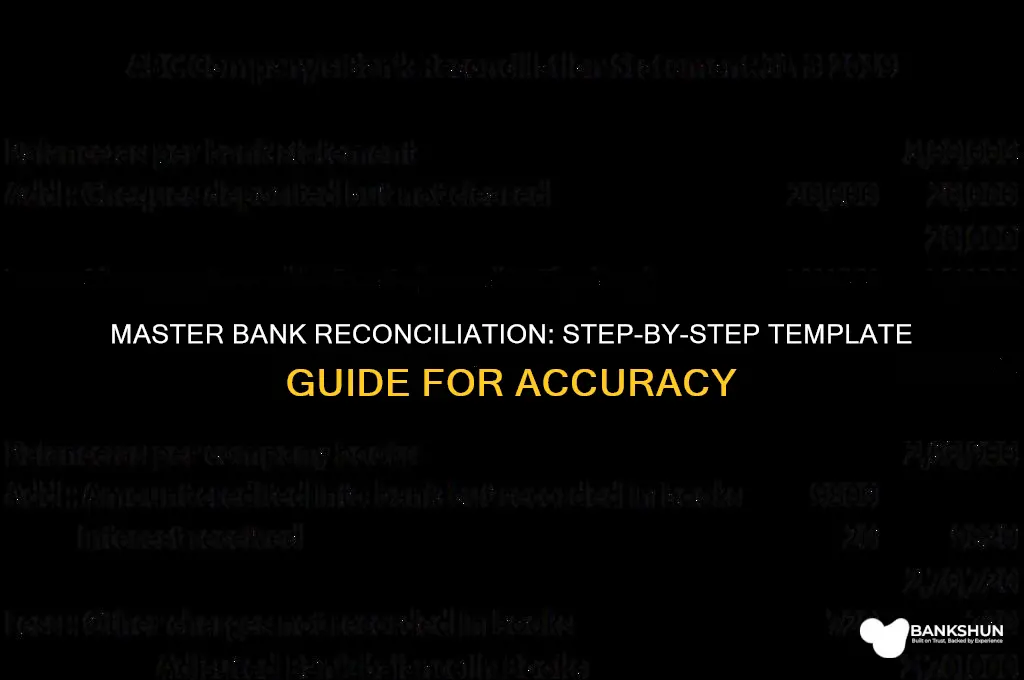

Finalize Report: Document reconciled balances and unresolved discrepancies

The final step in bank reconciliation is where precision meets accountability. After meticulously matching transactions, the focus shifts to documenting reconciled balances and unresolved discrepancies. This phase is critical because it transforms raw data into actionable insights, ensuring financial accuracy and transparency. Without a clear, structured report, even the most thorough reconciliation can lose its value.

Begin by clearly stating the reconciled balances for both the bank statement and the internal records. Use a table format for clarity, listing the starting balance, total deposits, total withdrawals, and the final reconciled balance. For example:

| Account | Starting Balance | Total Deposits | Total Withdrawals | Reconciled Balance |

|-----------------------|----------------------|--------------------|-----------------------|------------------------|

| Bank Statement | $10,000 | $5,000 | $3,000 | $12,000 |

| Internal Records | $10,000 | $5,000 | $3,000 | $12,000 |

This format ensures that anyone reviewing the report can quickly verify the accuracy of the reconciliation.

Next, address unresolved discrepancies with specificity. For each discrepancy, document the date, amount, description, and potential cause. For instance, an unresolved item might look like this:

| Date | Amount | Description | Potential Cause |

|----------------|------------|-------------------------------|------------------------------|

| 2023-10-15 | $200 | Missing deposit | Possible processing delay |

Include a brief analysis of each discrepancy, suggesting next steps such as contacting the bank, reviewing internal records, or awaiting additional information. This proactive approach demonstrates diligence and helps prevent future errors.

Finally, conclude the report with a summary statement affirming the reconciliation’s completeness and highlighting any actions required. For example: *"Reconciliation completed as of October 31, 2023. Two discrepancies totaling $350 remain unresolved and will be investigated by November 15, 2023."* This closing ensures accountability and sets clear expectations for follow-up.

By structuring the final report with precision and clarity, you not only document the reconciliation process but also provide a roadmap for maintaining financial integrity. This step is not merely administrative—it’s the cornerstone of reliable financial management.

Mastering Battery Bank Capacity Calculation for Optimal Energy Storage

You may want to see also

Frequently asked questions

A bank reconciliation template is a structured document used to compare and match a company’s internal financial records with its bank statement. It helps identify discrepancies, such as missing transactions, errors, or fraud, ensuring accuracy in financial reporting and cash management.

A bank reconciliation template should include the following elements: the statement date, ending balance per bank statement, outstanding deposits, outstanding checks, adjustments for bank fees or interest, and the reconciled balance. It should also have columns for both the company’s records and the bank statement for easy comparison.

A bank reconciliation template should be used monthly, ideally immediately after receiving the bank statement. Regular reconciliation ensures timely detection of discrepancies, maintains accurate financial records, and supports better cash flow management.