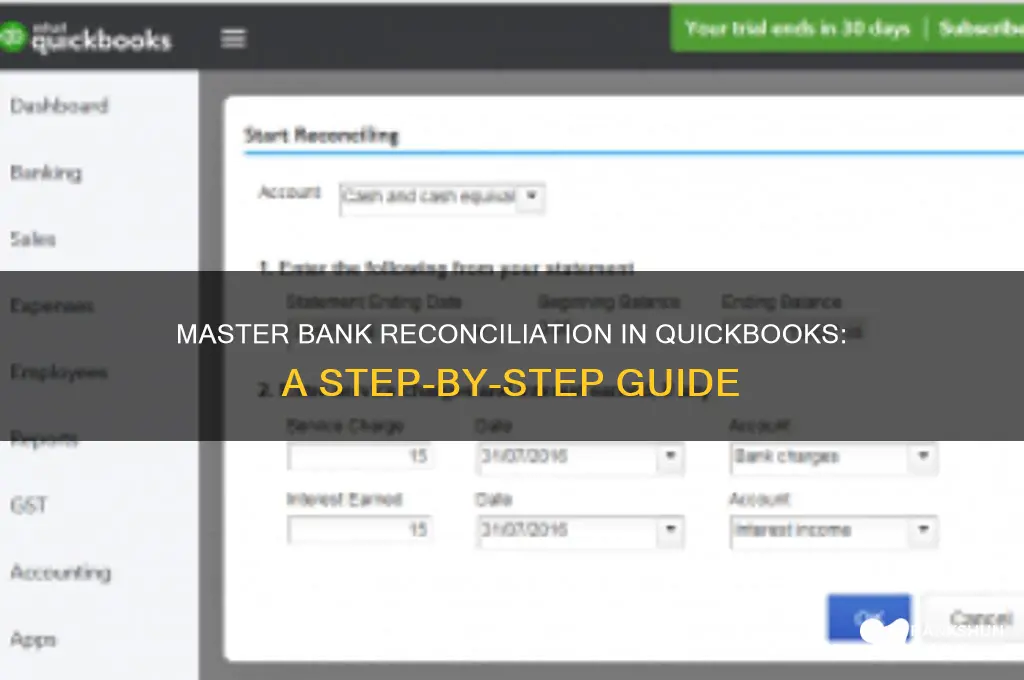

Bank reconciliation in QuickBooks is a critical process for ensuring the accuracy of your financial records by comparing your QuickBooks transactions with your bank statements. It helps identify discrepancies, such as missing or uncleared transactions, and ensures that your books reflect the true financial position of your business. To perform a bank reconciliation in QuickBooks, start by accessing the Banking menu and selecting Reconcile. Enter the ending balance and date from your bank statement, then match each transaction in QuickBooks to its corresponding entry on the statement. Unmatched or uncleared items should be reviewed and adjusted as needed. Completing this process regularly not only maintains financial integrity but also aids in detecting errors or fraudulent activities early on.

Explore related products

What You'll Learn

- Prepare Bank Statement: Gather and organize the latest bank statement for the reconciliation period

- Match Transactions: Compare QuickBooks transactions with bank statement entries to identify matches

- Identify Discrepancies: Locate and resolve unmatched transactions, such as missing or incorrect entries

- Adjust QuickBooks: Enter missing transactions or correct errors in QuickBooks to match the bank

- Finalize Reconciliation: Confirm all transactions match and complete the reconciliation process in QuickBooks

![]()

Prepare Bank Statement: Gather and organize the latest bank statement for the reconciliation period

The foundation of any successful bank reconciliation in QuickBooks lies in the accuracy and organization of your bank statement. Think of it as the blueprint for the entire process. Without a clear, up-to-date statement, you're essentially navigating in the dark, prone to errors and inconsistencies.

Begin by obtaining the most recent bank statement covering the reconciliation period. This could be a monthly statement or a custom date range, depending on your accounting cycle. Ensure it includes all transactions, from the smallest deposits to the largest withdrawals. Digital statements, often available through online banking portals, are ideal for their searchability and ease of import into QuickBooks. If you’re working with a paper statement, scan or photograph it for clarity and backup.

Once you have the statement, organize it for efficiency. Highlight or annotate key transactions that require special attention, such as recurring payments, transfers, or discrepancies. Group similar transactions (e.g., payroll, vendor payments) to streamline matching in QuickBooks. If your bank offers categorized statements, leverage this feature to save time. For businesses with multiple accounts, label each statement clearly to avoid confusion during reconciliation.

A practical tip: cross-reference the statement’s ending balance with your QuickBooks register before starting. This quick check can flag major discrepancies early, saving you from troubleshooting later. Remember, the goal here is to create a clean, structured document that serves as a reliable reference point throughout the reconciliation process.

Activate ASBA in Kotak Bank: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Match Transactions: Compare QuickBooks transactions with bank statement entries to identify matches

Matching transactions is the linchpin of bank reconciliation in QuickBooks, ensuring your financial records mirror reality. Begin by importing your bank statement into QuickBooks, either manually or through a secure bank feed. This step populates the reconciliation screen with both QuickBooks transactions and bank statement entries side by side. QuickBooks automatically suggests matches based on dates and amounts, but don’t rely solely on automation. Scrutinize each entry, as discrepancies like rounding differences or split transactions can slip through. For instance, a $120 QuickBooks entry might match a $120.50 bank statement entry if the bank rounded up a fee—flag such anomalies for further investigation.

The art of matching lies in recognizing patterns and exceptions. Look for recurring transactions like payroll deposits or subscription payments, which should align effortlessly. However, one-off entries like refunds or vendor payments require closer inspection. Use QuickBooks’ search function to cross-reference unclear transactions with invoices, bills, or receipts. For example, a $450 bank withdrawal might correspond to a vendor payment recorded as $450 in QuickBooks but labeled differently (e.g., "Office Supplies" vs. "Supply Co."). Context matters—ensure the transaction’s purpose aligns, not just its value.

Unmatched transactions are red flags demanding action. If a bank statement entry lacks a QuickBooks counterpart, investigate whether it’s an oversight, an error, or an unrecognized fee. Conversely, a QuickBooks transaction without a bank match might indicate a pending transaction or a recording mistake. For instance, a $750 invoice marked "paid" in QuickBooks but absent from the bank statement could mean the payment is still processing or was never sent. Use QuickBooks’ "Add Missing Transactions" feature to rectify such gaps, ensuring no financial activity is overlooked.

Efficiency in matching hinges on organization and consistency. Maintain uniform naming conventions for payees and categories in QuickBooks to simplify comparisons. For example, always record "Amazon Web Services" instead of alternating between "AWS" or "Amazon." Leverage QuickBooks’ memo field to add context to transactions, making future reconciliations smoother. For businesses with high transaction volumes, consider reconciling weekly rather than monthly to reduce complexity. Tools like QuickBooks’ reconciliation reports can highlight trends in unmatched transactions, helping you refine your process over time.

Mastering transaction matching transforms reconciliation from a chore into a diagnostic tool. It not only verifies accuracy but also uncovers insights into cash flow, spending patterns, and potential fraud. For instance, repeated unmatched withdrawals could signal unauthorized activity, while consistent timing discrepancies might indicate bank processing delays. By treating matching as a meticulous yet strategic task, you fortify QuickBooks as a reliable financial ally, ensuring every dollar is accounted for and every entry tells the right story.

Efficiently Remove Bank Transactions: A Step-by-Step App Guide

You may want to see also

Explore related products

![]()

Identify Discrepancies: Locate and resolve unmatched transactions, such as missing or incorrect entries

Unmatched transactions are the red flags of bank reconciliation in QuickBooks, signaling potential errors, oversights, or even fraud. These discrepancies—missing deposits, unrecorded withdrawals, or incorrect amounts—can distort your financial picture, leading to inaccurate reporting and decision-making. Identifying them requires a meticulous eye and a systematic approach, but resolving them ensures the integrity of your financial data.

Begin by comparing your bank statement line by line with QuickBooks transactions. Look for entries in the bank statement that don’t appear in QuickBooks, such as automatic fees, interest postings, or uncleared checks. Conversely, flag transactions in QuickBooks that haven’t cleared the bank, like recent deposits or outstanding payments. QuickBooks’ reconciliation tool highlights these mismatches, but manual scrutiny is essential for accuracy. For instance, a $500 deposit marked “pending” on the bank statement but missing in QuickBooks could be a timing issue, while a $1,200 withdrawal without a corresponding entry might indicate an unrecorded expense.

Once discrepancies are identified, investigate their root cause. Missing entries often stem from overlooked data entry, such as a forgotten invoice payment or an unrecorded cash deposit. Incorrect entries, on the other hand, may result from transposed numbers, wrong account selections, or duplicate postings. For example, a $3,500 payment recorded as $5,300 in QuickBooks would throw off your balance. Use QuickBooks’ search function to trace the transaction’s origin, checking details like dates, payees, and memos. If the error lies in the bank statement, contact your financial institution to clarify or correct it.

Resolving discrepancies requires precise action. For missing transactions, manually add them to QuickBooks, ensuring they’re categorized correctly. For incorrect entries, void or edit the transaction, depending on its type and age. Be cautious with edits to avoid altering historical data; instead, create a correcting journal entry if necessary. Document each resolution with a memo or audit trail for future reference. For recurring issues, such as frequent uncleared checks, consider adjusting your reconciliation frequency or payment processes to minimize future discrepancies.

The takeaway is clear: identifying and resolving unmatched transactions isn’t just about balancing numbers—it’s about maintaining trust in your financial data. By systematically comparing, investigating, and correcting discrepancies, you ensure QuickBooks reflects your true financial position. This diligence not only prevents errors but also strengthens your ability to make informed, data-driven decisions for your business.

Bank Apps and Social Security: What's the Connection?

You may want to see also

Explore related products

![]()

Adjust QuickBooks: Enter missing transactions or correct errors in QuickBooks to match the bank

Ensuring your QuickBooks records align perfectly with your bank statements is crucial for accurate financial reporting. One of the most critical steps in this process is adjusting QuickBooks by entering missing transactions or correcting errors. This task requires attention to detail and a systematic approach to maintain the integrity of your financial data.

Begin by comparing your bank statement with the transactions recorded in QuickBooks. Identify any discrepancies, such as missing deposits, unrecorded withdrawals, or incorrect amounts. For instance, if a client’s payment of $500 is reflected in your bank statement but not in QuickBooks, you’ll need to manually enter this transaction. Navigate to the Banking menu, select "Make Deposits" or "Write Checks" depending on the transaction type, and input the missing details. Ensure the date, amount, and account match the bank statement exactly to avoid future discrepancies.

Correcting errors in QuickBooks is equally important. Suppose a vendor payment was recorded as $300 instead of $30. To fix this, locate the incorrect transaction in the register or through the transaction history. Void or delete the erroneous entry, then re-enter the correct amount. Be cautious when deleting transactions, as this can affect your audit trail. Instead, consider voiding the entry and adding a memo explaining the correction for transparency. For recurring errors, such as misclassified expenses, review your chart of accounts and ensure transactions are being posted to the correct categories moving forward.

A practical tip is to use the "Reconcile" feature in QuickBooks to flag discrepancies during the reconciliation process. If a transaction appears in your bank statement but not in QuickBooks, the software will prompt you to add it. Similarly, if an amount doesn’t match, QuickBooks will highlight the discrepancy, allowing you to investigate and correct it immediately. This feature streamlines the adjustment process and reduces the likelihood of overlooking errors.

Finally, maintain a consistent reconciliation schedule—monthly or quarterly—to minimize the accumulation of discrepancies. Regularly updating QuickBooks with missing transactions and correcting errors not only ensures accuracy but also saves time in the long run. By staying proactive, you’ll maintain a reliable financial record that supports informed decision-making and compliance with accounting standards.

Equalizing Battery Banks: Optimal Timing for Extended Lifespan and Performance

You may want to see also

Explore related products

![]()

Finalize Reconciliation: Confirm all transactions match and complete the reconciliation process in QuickBooks

The final step in bank reconciliation within QuickBooks is a critical checkpoint: ensuring every transaction aligns perfectly between your records and the bank statement. This phase demands meticulous attention, as even minor discrepancies can snowball into significant financial inaccuracies. Begin by cross-verifying each entry, line by line, confirming dates, amounts, and descriptions match precisely. QuickBooks simplifies this process by highlighting unmatched transactions, but manual scrutiny remains essential to catch potential errors or omissions.

Once all transactions are confirmed, QuickBooks prompts you to finalize the reconciliation. This involves adjusting the ending balance to reflect any outstanding items, such as uncleared checks or deposits in transit. The software will display a reconciliation summary, detailing the beginning and ending balances, as well as the total of cleared transactions. Review this summary carefully; it serves as a final safeguard against errors before you commit the reconciliation.

A common pitfall at this stage is overlooking small discrepancies, assuming they’ll resolve themselves. However, even a $0.01 difference can indicate a deeper issue, such as a missed transaction or a data entry error. If discrepancies arise, QuickBooks allows you to undo the reconciliation and revisit earlier steps. Resist the urge to force numbers to match; instead, investigate the root cause to maintain data integrity.

Completing the reconciliation process in QuickBooks not only ensures accuracy but also provides a snapshot of your financial health at a specific point in time. Once finalized, the software locks the reconciled period, preventing accidental edits that could distort historical data. This feature is particularly valuable during audits or when generating financial reports. By treating this step with the rigor it deserves, you solidify the reliability of your financial records and streamline future reconciliations.

Practical tip: After finalizing reconciliation, export the summary report and archive it with your bank statement. This practice creates a tangible audit trail and simplifies reference in case of future discrepancies. Additionally, set a recurring reminder to reconcile accounts monthly, as consistency reduces the complexity of identifying and resolving mismatches. With these measures, QuickBooks becomes not just a tool for reconciliation but a cornerstone of your financial management strategy.

Contact Natwest Bank via Email: A Quick and Easy Guide

You may want to see also

Frequently asked questions

Bank reconciliation in QuickBooks is the process of comparing your QuickBooks transactions with your bank statement to ensure they match. It helps identify discrepancies, detect errors, and maintain accurate financial records, ensuring your books reflect your true financial position.

To start, go to the Accounting menu, select Reconcile, and choose the bank account you want to reconcile. Enter the ending balance and ending date from your bank statement, then click Start Reconciling to begin matching transactions.

If the beginning balance doesn’t match, it indicates an issue with a previous reconciliation. Review the last reconciliation report for errors or missed transactions. If necessary, undo the previous reconciliation and correct the discrepancies before starting anew.

Uncleared transactions are those that appear in QuickBooks but not on your bank statement. Leave these transactions unchecked during reconciliation. They will be reconciled in future periods once they clear your bank account.

If your reconciliation doesn’t balance, double-check for missed or duplicate transactions, ensure all transactions are correctly entered, and verify the ending balance and dates. Use the Locate Discrepancies tool in QuickBooks to identify and resolve issues.