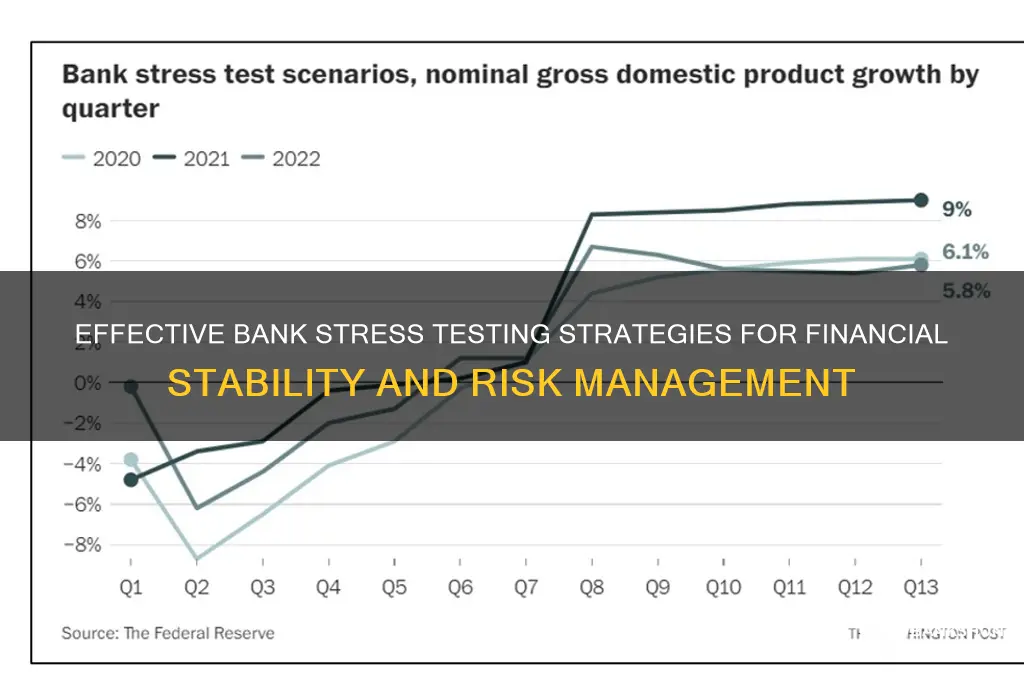

Stress testing for banks is a critical risk management tool designed to assess a financial institution's resilience to adverse economic scenarios. By simulating extreme but plausible events, such as severe recessions, market crashes, or geopolitical crises, stress tests evaluate a bank's ability to maintain sufficient capital and liquidity to absorb losses and continue operations. Regulatory bodies, like the Federal Reserve in the U.S. or the European Central Bank, often mandate these tests to ensure banks can withstand shocks without destabilizing the broader financial system. The process involves analyzing key metrics like capital adequacy ratios, asset quality, and funding stability under stress scenarios, providing insights into potential vulnerabilities and guiding strategic decision-making to enhance financial stability. Effective stress testing requires robust data, sophisticated modeling, and a forward-looking approach to identify and mitigate risks proactively.

| Characteristics | Values |

|---|---|

| Objective | Assess a bank's resilience to adverse economic and financial scenarios. |

| Regulatory Framework | Basel III, Dodd-Frank Act Stress Test (DFAST), Comprehensive Capital Analysis and Review (CCAR). |

| Scenarios | Baseline, adverse, and severely adverse scenarios (e.g., recession, market shocks). |

| Time Horizon | Typically 9 quarters (2.25 years) for stress testing. |

| Key Risk Factors | Credit risk, market risk, liquidity risk, operational risk, and interest rate risk. |

| Data Requirements | Historical and current financial data, macroeconomic indicators, and risk models. |

| Models Used | Economic models, credit risk models, liquidity models, and balance sheet models. |

| Capital Adequacy | Evaluate Tier 1 and Tier 2 capital ratios under stress scenarios. |

| Liquidity Metrics | Liquidity Coverage Ratio (LCR), Net Stable Funding Ratio (NSFR). |

| Reporting | Detailed reports to regulators, including capital plans and risk assessments. |

| Frequency | Annually for regulatory stress tests; more frequent for internal testing. |

| Stakeholders | Regulators, bank management, risk committees, and external auditors. |

| Validation | Regular validation of models and assumptions by independent teams. |

| Technology | Advanced analytics, AI/ML, and stress testing software (e.g., Moody’s, SAS). |

| Outcome | Identify capital shortfalls, adjust risk management strategies, and ensure compliance. |

| Latest Trends | Incorporation of climate risk, cybersecurity risks, and ESG factors. |

Explore related products

What You'll Learn

- Define stress scenarios: Identify severe but plausible events impacting bank's portfolio, economy, or operations

- Data collection: Gather historical and current data on assets, liabilities, and risk factors

- Model selection: Choose appropriate models to simulate stress impacts on bank's financial health

- Run stress tests: Execute scenarios to assess capital adequacy, liquidity, and earnings under stress

- Analyze results: Evaluate outcomes, identify vulnerabilities, and develop mitigation strategies for risks

![]()

Define stress scenarios: Identify severe but plausible events impacting bank's portfolio, economy, or operations

Stress testing for banks hinges on the ability to envision catastrophic yet realistic events that could destabilize financial systems. Defining stress scenarios is not about indulging in doomsday fantasies but about grounding extreme possibilities in historical precedent, economic theory, and current vulnerabilities. For instance, the 2008 financial crisis wasn’t unforeseeable—it was a severe but plausible scenario rooted in housing market bubbles and systemic leverage. Banks must identify such events, whether macroeconomic shocks like a global recession, geopolitical conflicts, or sector-specific crises like a collapse in commercial real estate. The key is to avoid both underestimating risks and overloading models with improbable hypotheticals.

To craft effective stress scenarios, banks should adopt a structured approach. Start by analyzing historical crises and their triggers—for example, the 1997 Asian Financial Crisis or the 2020 COVID-19 pandemic. Next, overlay current economic indicators, such as inflation rates, unemployment levels, and debt-to-GDP ratios, to identify emerging vulnerabilities. For instance, a scenario could simulate a 30% drop in asset prices coupled with a 5% rise in interest rates over 12 months. Tools like scenario trees or Monte Carlo simulations can help model the interplay of variables. However, caution is necessary: scenarios must remain plausible, avoiding extremes like a 90% stock market crash without a credible catalyst.

A persuasive argument for robust stress scenarios lies in their ability to expose hidden weaknesses. Consider a bank heavily exposed to sovereign debt in emerging markets. A scenario involving a sudden currency devaluation and default in a key market could reveal liquidity shortfalls or contagion risks. By contrast, a generic recession scenario might overlook such specifics. Tailoring scenarios to a bank’s unique portfolio and geographic footprint ensures relevance. For example, a European bank might stress-test for a eurozone breakup, while an Asian bank might focus on supply chain disruptions.

Comparatively, stress scenarios differ from baseline projections or sensitivity analyses. While the latter test incremental changes (e.g., a 1% interest rate hike), stress scenarios explore extreme outcomes (e.g., a 5% hike combined with a corporate bond market freeze). This distinction is critical: banks must prepare for not just likely events but also low-probability, high-impact “black swan” events. For instance, a cyberattack crippling payment systems or a pandemic-induced economic shutdown. Such scenarios require creativity, drawing on cross-disciplinary insights from economics, geopolitics, and technology.

In practice, defining stress scenarios is an iterative process requiring collaboration between risk managers, economists, and business leaders. Start with broad themes (e.g., economic shocks, operational failures) and refine them into quantifiable scenarios. For example, an operational stress test might simulate a prolonged IT outage affecting 70% of transactions for two weeks. Validate scenarios against historical data and peer benchmarks to ensure credibility. Finally, update scenarios annually to reflect evolving risks—a scenario relevant in 2019 might look very different in 2023. By grounding extreme events in reality, banks can transform stress testing from a compliance exercise into a strategic tool for resilience.

Food Banks: Charity Status Needed?

You may want to see also

Explore related products

![]()

Data collection: Gather historical and current data on assets, liabilities, and risk factors

Effective stress testing for banks hinges on the quality and comprehensiveness of the data collected. Historical and current data on assets, liabilities, and risk factors form the backbone of any stress testing framework. Without robust data, even the most sophisticated models will yield unreliable results, undermining the very purpose of stress testing—to assess a bank’s resilience under adverse conditions.

Step 1: Identify Data Sources

Begin by pinpointing reliable sources for historical and current data. Internal records, such as balance sheets, income statements, and loan portfolios, provide granular insights into assets and liabilities. External sources, including regulatory filings, market data providers (e.g., Bloomberg, Reuters), and macroeconomic databases (e.g., IMF, World Bank), offer context on risk factors like interest rates, unemployment, and GDP growth. For instance, historical data on loan defaults during the 2008 financial crisis can serve as a benchmark for stress scenarios.

Cautions in Data Collection

While gathering data, be wary of gaps or inconsistencies. Missing historical records or outdated risk factor data can skew results. For example, relying solely on pre-2008 data might overlook the impact of regulatory changes like Basel III. Additionally, ensure data is standardized across sources to avoid discrepancies. A practical tip: use data validation tools like Python’s Pandas library to clean and reconcile datasets before analysis.

Analyzing Risk Factors

Risk factors are the variables that drive stress scenarios. These include macroeconomic indicators (e.g., inflation, exchange rates), market risks (e.g., equity price shocks), and bank-specific risks (e.g., liquidity mismatches). For instance, a stress test might simulate a 200-basis-point rise in interest rates to assess its impact on a bank’s bond portfolio. By linking historical data to current trends, banks can identify vulnerabilities and tailor scenarios to their unique risk profile.

Takeaway: Data as the Foundation

Data collection is not a one-time task but an ongoing process. Regular updates ensure stress tests remain relevant in a dynamic financial landscape. For example, incorporating real-time data on COVID-19’s economic impact allowed banks to assess pandemic-related risks promptly. By treating data collection as a strategic priority, banks can build stress testing frameworks that are both accurate and actionable, ultimately safeguarding their stability in uncertain times.

The Uncanny Resemblance Between Rachel McAdams and Elizabeth Banks

You may want to see also

Explore related products

![]()

Model selection: Choose appropriate models to simulate stress impacts on bank's financial health

Selecting the right models for stress testing is akin to choosing the right tools for surgery—precision matters. Banks must simulate a range of economic shocks, from mild recessions to severe crises, and the models they use must capture the complexity of their balance sheets and risk exposures. For instance, a bank heavily reliant on mortgage lending might prioritize models that account for housing market volatility, while a globally diversified bank would need models that incorporate cross-border contagion risks. The goal is to avoid over-simplification, which could lead to underestimating risks, or over-complication, which could obscure actionable insights.

One practical approach is to categorize models based on their scope and granularity. Top-down models are useful for assessing macroeconomic shocks, such as a 2% drop in GDP or a 30% decline in asset prices. These models provide a broad view of how systemic risks affect the bank’s capital adequacy ratios. Conversely, bottom-up models focus on granular data, like loan-level defaults or deposit outflows, to simulate stress at the portfolio level. For example, a bottom-up model might analyze how a 50-basis-point rise in interest rates impacts fixed-rate mortgage holders versus adjustable-rate borrowers. Combining both approaches ensures a comprehensive assessment of risks across different scales.

However, model selection isn’t just about scope—it’s also about adaptability. Banks should choose models that can incorporate dynamic factors, such as behavioral changes during a crisis. For instance, during a pandemic, depositors might withdraw funds at a higher rate than historical norms suggest. Models that allow for such behavioral adjustments provide a more realistic simulation. Similarly, models should account for regulatory responses, like capital buffers or liquidity requirements, which can mitigate or exacerbate stress impacts. A model that ignores these factors risks producing misleading results.

A critical caution is to avoid over-reliance on historical data. While past crises provide valuable insights, they may not fully capture the risks of future shocks, such as cyberattacks or climate-related disasters. Banks should complement historical data with scenario analysis, such as a 20% decline in commercial real estate values due to remote work trends or a 15% increase in loan defaults due to extreme weather events. This forward-looking approach ensures that models remain relevant in an evolving risk landscape.

In conclusion, model selection for stress testing requires a balance of breadth, depth, and flexibility. Banks must choose models that align with their risk profile, incorporate dynamic factors, and look beyond historical precedents. By doing so, they can simulate stress impacts with greater accuracy and prepare more effectively for an uncertain future. The right models aren’t just tools—they’re strategic assets in safeguarding financial health.

Penny Roll Fees: Banks Charging for Change?

You may want to see also

Explore related products

![]()

Run stress tests: Execute scenarios to assess capital adequacy, liquidity, and earnings under stress

Stress testing is a critical tool for banks to evaluate their resilience against adverse economic conditions. By executing scenarios that simulate extreme but plausible events, such as a severe recession or a sudden market crash, banks can assess their capital adequacy, liquidity, and earnings under stress. These tests are not just regulatory requirements but essential practices for risk management and strategic planning. For instance, a bank might model a scenario where unemployment rises to 10%, interest rates spike by 2%, and asset prices drop by 30%. The goal is to determine if the bank can maintain sufficient capital to absorb losses, meet withdrawal demands, and sustain operations without compromising its financial health.

To execute stress tests effectively, banks must follow a structured approach. First, identify key risk factors relevant to the institution, such as credit risk, market risk, and operational risk. Next, develop scenarios that reflect these risks, ensuring they are both severe and realistic. For example, a liquidity stress test might simulate a run on the bank, where depositors withdraw 20% of funds within a week. Use historical data, macroeconomic forecasts, and expert judgment to calibrate these scenarios. Once the scenarios are defined, apply them to the bank’s financial models to measure the impact on capital ratios, liquidity positions, and earnings. Tools like Monte Carlo simulations or balance sheet models can enhance the accuracy of these assessments.

A common pitfall in stress testing is underestimating the interconnectedness of risks. For instance, a decline in asset values can erode capital, which in turn reduces lending capacity, further depressing earnings. Banks must adopt a holistic view, considering how stress in one area cascades into others. Another caution is over-reliance on historical data, which may not capture emerging risks like cybersecurity threats or climate-related shocks. To mitigate this, incorporate forward-looking indicators and stress test for tail-risk events, even if they have low probabilities. Regularly updating scenarios to reflect changing economic landscapes is equally vital.

The takeaway from stress testing is not just identifying vulnerabilities but also informing strategic decisions. For example, if a stress test reveals a liquidity gap under a severe scenario, the bank might increase its holdings of high-quality liquid assets or establish contingency funding sources. Similarly, if capital adequacy is at risk, the bank could consider retaining more earnings, issuing new capital, or reducing dividend payouts. Stress testing also fosters transparency and accountability, as results are often shared with regulators and stakeholders. By treating stress tests as a dynamic, ongoing process rather than a one-time exercise, banks can build resilience and maintain trust in their financial stability.

Banks' Role in Disaster Relief: Financial Support During Natural Calamities

You may want to see also

Explore related products

![]()

Analyze results: Evaluate outcomes, identify vulnerabilities, and develop mitigation strategies for risks

Stress testing for banks is not merely about running scenarios; it’s about extracting actionable insights from the chaos. Once the simulations are complete, the real work begins: dissecting the results to uncover weaknesses before they become crises. Start by comparing the outcomes against predefined thresholds and regulatory benchmarks. For instance, if a bank’s Tier 1 capital ratio drops below 6% under a severe recession scenario, it signals a critical vulnerability that demands immediate attention. This initial evaluation sets the stage for deeper analysis, ensuring no red flag goes unnoticed.

Next, identify vulnerabilities by isolating the specific areas where the bank falters under stress. Is it excessive exposure to a single sector, liquidity mismatches, or over-reliance on volatile funding sources? For example, a bank heavily invested in commercial real estate might see its loan portfolio deteriorate rapidly during a property market crash. Use tools like sensitivity analysis to pinpoint which variables—interest rates, unemployment levels, or asset prices—have the most significant impact on the bank’s health. This granular approach transforms raw data into a clear map of risk concentration.

Developing mitigation strategies requires a blend of creativity and pragmatism. If liquidity risk emerges as a key vulnerability, consider diversifying funding sources or establishing contingency credit lines. For capital adequacy issues, options might include retaining earnings, issuing new equity, or reducing dividend payouts. Stress test results should also inform strategic decisions, such as adjusting lending criteria or exiting high-risk markets. For instance, a bank exposed to climate risk might prioritize green financing to align its portfolio with long-term sustainability goals.

However, mitigation strategies must be realistic and scalable. Stress testing often reveals interconnected risks, meaning solutions in one area may inadvertently exacerbate problems elsewhere. For example, tightening lending standards to reduce credit risk could stifle revenue growth. Banks should conduct cost-benefit analyses and stress-test their mitigation plans to ensure they don’t introduce new vulnerabilities. Collaboration between risk management, finance, and business units is essential to craft holistic solutions that balance resilience with profitability.

Finally, treat stress testing as an iterative process, not a one-off exercise. Regularly update scenarios to reflect evolving risks—such as cyber threats, geopolitical instability, or pandemics—and reassess mitigation strategies accordingly. Establish a feedback loop where lessons from past tests inform future simulations, creating a dynamic risk management framework. By embedding this discipline into the bank’s culture, institutions can turn stress testing from a regulatory chore into a strategic advantage, ensuring they not only survive but thrive in uncertain times.

Does the World Bank Influence Global Oil Price Dynamics?

You may want to see also