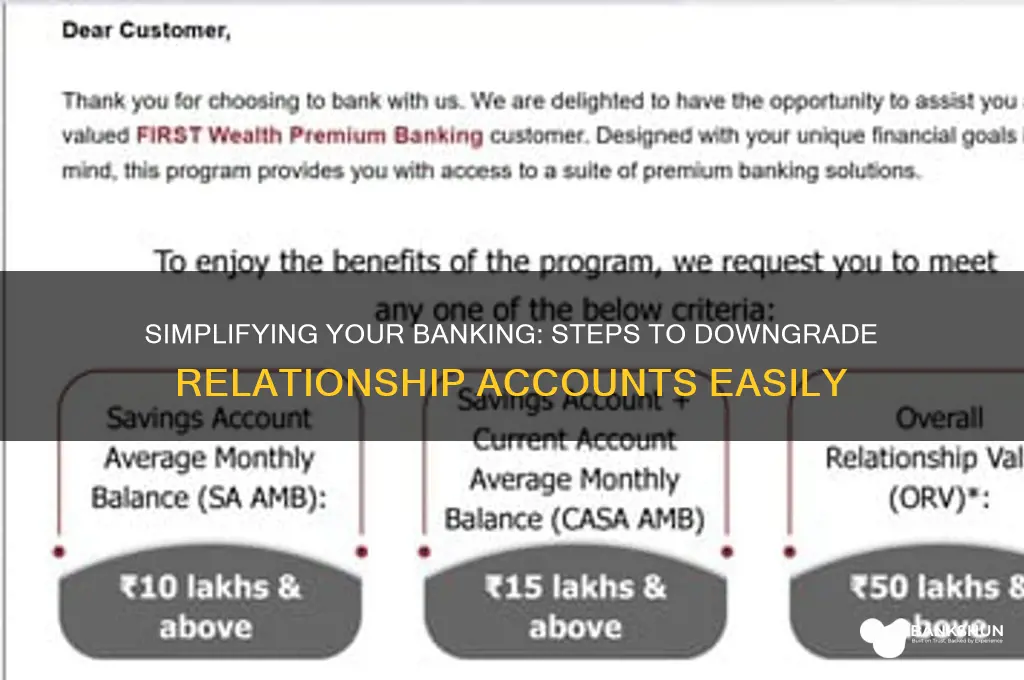

Downgrading from advanced relationship banking can be a strategic decision for individuals or businesses seeking to simplify their financial management or reduce associated costs. Advanced relationship banking often comes with premium services, personalized support, and higher fees, which may not align with current financial goals or needs. Whether due to changing financial circumstances, a desire for more straightforward banking solutions, or dissatisfaction with the value received, understanding the process of downgrading is essential. This involves reviewing your current banking package, assessing alternative options, and communicating effectively with your bank to ensure a smooth transition without compromising your financial stability. By carefully evaluating your priorities and following the necessary steps, you can successfully downgrade to a more suitable banking arrangement.

Explore related products

What You'll Learn

- Reassessing Relationship Needs: Evaluate current banking requirements to determine if advanced services are still necessary

- Simplifying Account Features: Identify and remove unnecessary premium features to reduce costs and complexity

- Switching to Basic Plans: Explore and transition to lower-tier banking packages with fewer benefits

- Negotiating Fees: Discuss with the bank to waive or reduce fees associated with advanced services

- Closing Unused Services: Terminate add-ons like wealth management or priority support to streamline the account

![]()

Reassessing Relationship Needs: Evaluate current banking requirements to determine if advanced services are still necessary

As financial circumstances evolve, the banking services that once seemed indispensable may no longer align with current needs. Advanced relationship banking, often characterized by personalized services, priority support, and premium features, comes at a cost—both literal and in terms of complexity. Before committing to a downgrade, it’s essential to systematically evaluate whether these high-tier services still serve a purpose in your financial life. Start by listing all the features you currently use and those that remain untouched. This inventory will reveal whether you’re paying for convenience you no longer require or if simpler alternatives could suffice.

Consider this scenario: a self-employed individual who initially opted for advanced banking to manage fluctuating cash flows and access business advisory services. Years later, their income stabilizes, and they rarely utilize the specialized support. In such cases, downgrading to a standard account could save hundreds annually in fees while still meeting basic banking needs. The key is to match your current financial behavior with the services offered, rather than clinging to a status quo that no longer benefits you.

To conduct this evaluation, follow a structured approach. First, review your monthly statements for the past year to identify usage patterns. Are you consistently leveraging perks like waived fees, higher transaction limits, or exclusive investment opportunities? If not, quantify the value of these unused features against their cost. Second, assess life changes that may have altered your banking needs—retirement, a shift to salaried employment, or reduced investment activity. These shifts often signal that advanced services are no longer justified.

A cautionary note: downgrading isn’t always about cost-cutting. Some advanced accounts offer protections or benefits that, while infrequently used, could prove invaluable in specific scenarios. For instance, overdraft buffers or fraud resolution services might be worth retaining if your financial situation lacks a safety net. Weigh the intangible value of peace of mind against tangible savings before making a decision.

Ultimately, reassessing relationship needs is about aligning your banking strategy with your present reality. It’s not a step backward but a strategic recalibration. By critically examining usage patterns, life changes, and the true value of premium features, you can make an informed choice that optimizes both financial efficiency and long-term stability. This process isn’t just about downgrading—it’s about upgrading your financial mindfulness.

Israeli Settlements: Legality in the West Bank

You may want to see also

Explore related products

![]()

Simplifying Account Features: Identify and remove unnecessary premium features to reduce costs and complexity

Advanced relationship banking often comes with a suite of premium features that, while appealing initially, may not align with your current financial needs or goals. Simplifying account features by identifying and removing these unnecessary add-ons can significantly reduce costs and streamline your banking experience. Start by reviewing your account statements to pinpoint services you rarely or never use, such as priority customer support, waived fees on foreign transactions, or access to exclusive investment products. These features often come with hidden costs embedded in your monthly maintenance fees or annual charges.

Once you’ve identified underutilized features, contact your bank to request their removal. Most institutions allow customers to downgrade to a basic account tier, though some may require you to close the existing account and open a new one. Be prepared to negotiate; banks often prefer to retain customers and may offer waivers or discounts on certain features rather than lose your business entirely. For instance, if you no longer travel internationally, removing foreign transaction fee waivers could save you $50–$100 annually without impacting your day-to-today banking.

A comparative analysis of your current account versus a simplified alternative can highlight the potential savings. For example, a premium account with a $30 monthly fee and unused features like concierge services or travel insurance could cost $360 annually. Downgrading to a basic account with a $5 monthly fee saves $300 per year, which could be redirected toward savings or debt repayment. Tools like budgeting apps or bank comparison websites can help you visualize these differences and make an informed decision.

Finally, consider the long-term benefits of simplicity. Complex accounts with multiple features often lead to confusion and overspending. By removing unnecessary premium services, you not only reduce costs but also gain clarity and control over your finances. This approach aligns with the principle of minimalism in personal finance, where less is often more. Start small—remove one feature at a time—and reassess your needs periodically to ensure your account remains tailored to your lifestyle.

Mastering Battery Bank Capacity Calculation for Optimal Energy Storage

You may want to see also

Explore related products

![]()

Switching to Basic Plans: Explore and transition to lower-tier banking packages with fewer benefits

Downgrading from advanced relationship banking to a basic plan isn’t just about cutting costs—it’s a strategic realignment of your financial priorities. Advanced packages often bundle services like priority customer support, waived fees, or investment perks that may no longer align with your needs. For instance, if you’re no longer maintaining a high account balance or using premium features like wealth management tools, you’re essentially paying for unused benefits. Start by auditing your current usage: How often do you utilize concierge services? Do you actually need unlimited free wire transfers? Identifying underused perks is the first step to determining if a basic plan is a better fit.

Transitioning to a lower-tier package requires a clear understanding of what you’re giving up—and what you’re gaining. Basic plans typically offer core banking services like checking, savings, and debit cards but strip away extras like cashback rewards, travel insurance, or preferential loan rates. However, the trade-off is significant cost savings. For example, downgrading from a premium account with a $50 monthly fee to a basic account with a $5 fee could save you $540 annually. To make this switch, contact your bank’s customer service or visit a branch to discuss available options. Some banks may require closing the existing account and opening a new one, so prepare to transfer funds and update direct deposits or automatic payments.

One common hesitation in downgrading is the fear of losing convenience or status. However, basic plans often suffice for individuals with straightforward financial needs. For instance, a retiree with stable income and minimal transaction volume may find advanced features unnecessary. Similarly, a freelancer who previously needed premium services for business expenses might now operate on a smaller scale. The key is to assess your current lifestyle and financial goals. If you’re prioritizing debt repayment or saving for a specific goal, redirecting funds from premium banking fees can accelerate your progress.

Before finalizing the switch, scrutinize the fine print of the basic plan. Some banks impose transaction limits, charge for paper statements, or require minimum balances to avoid fees. For example, a basic account might limit you to 10 free ATM withdrawals per month, with a $2 fee thereafter. Additionally, ensure the new plan aligns with your long-term needs. If you anticipate returning to advanced banking in the future, inquire about upgrade processes. Most banks allow seamless transitions, but some may require a waiting period or reapplication.

Ultimately, downgrading to a basic banking plan is about maximizing value without overspending on unnecessary features. It’s a practical move for those whose financial habits have evolved or simplified. By carefully evaluating your needs, understanding the trade-offs, and navigating the transition process, you can secure a banking package that aligns with your current priorities while freeing up resources for other financial goals. Think of it as decluttering your financial life—less complexity, more clarity.

Mastering the Side Part: A Step-by-Step Guide to Cutting Banks

You may want to see also

Explore related products

![]()

Negotiating Fees: Discuss with the bank to waive or reduce fees associated with advanced services

Banks often bundle advanced relationship banking with premium fees, assuming clients value the services enough to pay a premium. However, these fees can accumulate, especially for services you rarely use. Before initiating negotiations, audit your account to identify which advanced services you actually utilize. For instance, if you’re paying for priority customer support but rarely need it, this is a prime candidate for fee reduction. Understanding your usage patterns gives you concrete data to support your negotiation, shifting the conversation from a vague request to a data-driven discussion.

Negotiating fees requires a strategic approach, not a confrontational one. Start by researching what competitors offer for similar services—banks are often more flexible when they know you’re aware of alternatives. Frame your request as a retention opportunity for the bank. For example, say, *“I’ve been a loyal customer for X years, and while I value our relationship, the fees for advanced services are becoming a concern. Can we explore options to reduce or waive these fees to ensure this account remains a good fit for me?”* This positions you as a customer worth retaining, not just a complainer.

Banks are more likely to waive or reduce fees if they see you as a high-value customer. Highlight your account’s positives: consistent balances, frequent transactions, or long-term loyalty. If you’re considering downgrading, mention this as a last resort. For instance, *“I’m evaluating my options, including downgrading to a basic account, but I’d prefer to stay with your bank if we can find a solution.”* This creates urgency without being aggressive. Additionally, timing matters—banks are often more flexible during quarterly reviews or when they’re pushing retention targets.

Not all fees are negotiable, but many are. Monthly maintenance fees, annual service charges, and even overdraft fees can sometimes be reduced or waived. For example, if you’re paying a $30 monthly fee for advanced services, ask if they can waive it in exchange for maintaining a higher minimum balance or opting into paperless statements. Be specific in your ask: *“Could you waive the $30 fee if I maintain a $5,000 balance instead of $2,500?”* Banks often have internal policies allowing for such adjustments, but they won’t offer them unless prompted.

If initial negotiations stall, escalate the conversation to a relationship manager or branch manager. These individuals have more authority to make exceptions. Bring documentation of your account history and competitor offers to strengthen your case. Remember, banks prioritize profitability, but they also value long-term relationships. By presenting yourself as a customer worth keeping and backing your request with data, you increase your chances of success. Even if they can’t waive fees entirely, they may offer partial reductions or alternative solutions, such as bundling services at a lower cost.

Financing Cars with Rebuilt Titles: What Banks Offer?

You may want to see also

Explore related products

![[50 Pack] BESTTEN Single Pole Decorator Wall Light Switch with Wallplate, 15A 120/277V, On/Off Rocker Paddle Interrupter, UL Listed, White](https://m.media-amazon.com/images/I/71pklf7G38L._AC_UY218_.jpg)

![]()

Closing Unused Services: Terminate add-ons like wealth management or priority support to streamline the account

Advanced relationship banking often bundles services like wealth management, priority support, or exclusive perks that may lose relevance over time. Review your account statement to identify add-ons you haven’t used in the past six months. Wealth management services, for instance, typically charge annual fees ranging from 0.5% to 2% of assets under management, which can add up even if you’re not actively utilizing their advice. Similarly, priority support often comes with monthly fees of $20–$50, yet many customers find standard support sufficient for their needs. By pinpointing these unused services, you can calculate potential savings and make informed decisions about what to terminate.

Termination isn’t always straightforward, so approach it strategically. Start by contacting your relationship manager to discuss your intent to downgrade. Banks often require written requests or specific forms to process cancellations, so ask for clear instructions. For wealth management services, ensure there are no penalties for early termination, as some contracts include clauses that charge fees if you exit before a certain period. Priority support may be easier to cancel, but confirm whether it’s tied to other account benefits. Pro tip: Schedule a follow-up call or email to verify the changes have been implemented, as administrative errors can occur.

Comparing the value of these add-ons to their cost reveals why termination makes sense. For example, if you’re managing investments independently through robo-advisors or self-directed platforms, wealth management fees become redundant. Similarly, priority support’s faster response times may not justify the cost if your banking needs are minimal. A comparative analysis of your usage versus the fees paid can highlight where you’re overspending. For instance, a customer paying $30 monthly for priority support but only calling twice a year could save $360 annually by switching to standard support.

The psychological barrier to downgrading often stems from the perception of losing "elite" status. However, reframing this as a practical optimization can make the decision easier. Think of it as decluttering your financial portfolio—just as you’d remove unused subscriptions, streamline your banking to reflect your current needs. Banks may offer alternatives, such as retaining certain perks at a lower cost or bundling services differently. For example, some institutions allow customers to keep priority support by maintaining a lower minimum balance or reducing the fee to $10/month. Exploring these options ensures you’re not sacrificing convenience unnecessarily.

After terminating unused services, monitor your account for at least two billing cycles to ensure the changes are reflected accurately. Unexpected fees or lingering charges can occur, so stay vigilant. Additionally, reassess your banking needs annually or after significant life changes, such as retirement or a career shift, to ensure your account structure remains aligned with your goals. By closing unused services, you not only reduce costs but also simplify your financial management, making it easier to focus on what truly matters.

Exploring NBT Bank's Reach: Total Number of Branches Revealed

You may want to see also

Frequently asked questions

Downgrading from Advanced Relationship Banking means transitioning from a higher-tier banking service to a standard or lower-tier account, often resulting in reduced benefits, features, and personalized services.

Contact your bank’s customer service or relationship manager to request a downgrade. They will guide you through the process, which may involve submitting a formal request and meeting specific account requirements.

Downgrading may result in the loss of certain perks, such as fee waivers, priority services, or higher interest rates. Ensure you review the changes with your bank to understand how it impacts your accounts.

Typically, there are no fees for downgrading, but it’s best to confirm with your bank. Some institutions may have specific terms or conditions tied to the transition process.