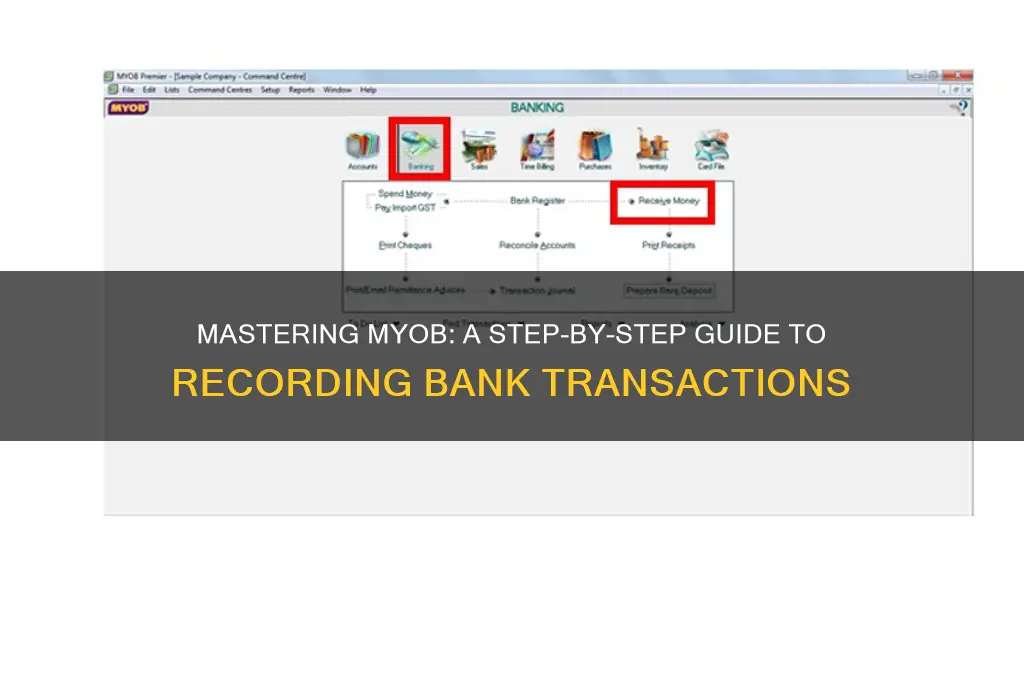

Entering bank transactions in MYOB is a crucial task for maintaining accurate financial records and ensuring smooth business operations. This process involves recording all incoming and outgoing transactions, such as deposits, withdrawals, and transfers, into the software's banking module. To begin, users must first navigate to the banking section within MYOB, where they can select the appropriate bank account and choose the option to record a new transaction. Each entry requires specific details, including the date, transaction type, amount, and a brief description, which helps in categorizing and tracking the transaction. By following a systematic approach and double-checking entries for accuracy, users can effectively manage their bank transactions, enabling better financial management and reporting.

Explore related products

What You'll Learn

![]()

Setting up bank accounts in MYOB

Before entering bank transactions in MYOB, you must first set up your bank accounts correctly. This foundational step ensures accuracy and streamlines your financial management. MYOB allows you to create multiple bank accounts, each tailored to your business needs, whether it’s a checking account, savings account, or credit card. Start by navigating to the Banking menu and selecting Bank Accounts. Click New to begin the setup process. Here, you’ll input essential details such as the account name, type, and opening balance. Accuracy in this stage is critical, as errors can lead to discrepancies in your financial records.

Once you’ve created a bank account, MYOB offers customization options to align it with your business operations. For instance, you can assign a unique code to each account for easy identification in reports. Additionally, you can specify the account’s currency if you deal with international transactions. A practical tip is to reconcile your opening balance with your bank statement to ensure consistency from the outset. This step not only prevents future discrepancies but also builds a reliable foundation for transaction entry.

A common oversight during setup is neglecting to configure bank feeds, a feature that automatically imports transactions from your bank into MYOB. Enabling this not only saves time but also minimizes manual data entry errors. To activate bank feeds, link your bank account to MYOB by providing your online banking credentials. While this process may vary depending on your bank, MYOB provides step-by-step guidance. Once enabled, transactions will sync regularly, ensuring your records are always up-to-date. However, periodically review these imports for accuracy, as automated systems can occasionally misinterpret transaction details.

In conclusion, setting up bank accounts in MYOB is a strategic step that goes beyond mere data entry. It involves customization, optimization, and integration to create a robust financial framework. By taking the time to configure accounts thoughtfully and leverage features like bank feeds, you’ll position yourself for efficient transaction management. This groundwork not only simplifies your workflow but also enhances the reliability of your financial data, ultimately supporting better decision-making for your business.

UBS: Understanding the Renowned Swiss Banking Giant's Name

You may want to see also

Explore related products

![]()

Importing bank statements into MYOB

To begin the import process, navigate to the Banking tab in MYOB and select Import Bank Statement. Here, you’ll be prompted to choose the file from your computer. MYOB’s intelligent matching system will attempt to reconcile imported transactions with existing entries in your ledger. However, this feature works best when your chart of accounts is well-organized and up-to-date. For instance, if a transaction description includes "Office Supplies," MYOB will match it to the corresponding expense account, provided it’s correctly labeled.

While importing is efficient, it’s not without potential pitfalls. One common issue is duplicate entries, which can occur if you accidentally import the same statement twice. To avoid this, always verify the date range of the statement before importing. Additionally, MYOB may not always categorize transactions accurately, especially for ambiguous descriptions like "Transfer" or "Payment." In such cases, manual review and reclassification are necessary to maintain accurate financial records.

A practical tip for maximizing the benefits of importing bank statements is to establish a routine. For example, importing statements weekly or monthly ensures your records remain current and reduces the volume of transactions to review at once. Pair this with regular reconciliation of your bank accounts within MYOB to catch discrepancies early. By combining automation with periodic manual checks, you can maintain a robust and error-free accounting system.

In conclusion, importing bank statements into MYOB is a powerful tool for modernizing your financial management. While it offers efficiency and accuracy, success hinges on understanding its limitations and adopting best practices. By staying vigilant during the import process and maintaining a consistent routine, you can leverage this feature to its fullest potential, freeing up time to focus on strategic financial decisions.

Donating at a Sperm Bank: A Step-by-Step Guide to Giving Back

You may want to see also

Explore related products

![]()

Reconciling transactions in MYOB

To begin reconciling, navigate to the *Banking* menu in MYOB and select *Reconcile Accounts*. Choose the bank account you wish to reconcile and enter the statement date and ending balance from your bank statement. MYOB will display a list of uncleared transactions, allowing you to tick off those that appear on your statement. For unmatched transactions, investigate potential issues such as data entry errors, timing differences, or missing entries. For instance, a deposit recorded in MYOB might not yet appear on the bank statement due to processing delays.

A key feature of MYOB’s reconciliation tool is its ability to flag discrepancies automatically. If the difference between your MYOB balance and bank statement balance cannot be resolved, MYOB prompts you to record a *suspense account* entry. This temporary adjustment ensures your books balance while you investigate further. For example, if a $500 discrepancy exists, create a suspense account entry for that amount and revisit it once you identify the root cause, such as an overlooked fee or duplicate transaction.

Practical tips can streamline the reconciliation process. First, reconcile frequently—ideally monthly—to minimize the volume of transactions and simplify discrepancy resolution. Second, leverage MYOB’s search and filter functions to quickly locate specific transactions. Third, maintain consistent naming conventions for payees and categories to avoid confusion. For instance, ensure "Office Supplies Inc." is always entered the same way, rather than variations like "Office Supplies" or "OSI."

In conclusion, reconciling transactions in MYOB is not just a compliance task but a proactive measure to safeguard your financial health. By systematically matching entries, addressing discrepancies, and utilizing MYOB’s tools, you ensure accuracy and reliability in your financial records. Regular reconciliation also highlights potential issues early, such as unauthorized transactions or accounting errors, enabling timely corrective action. Master this process, and you’ll transform a routine task into a powerful tool for financial management.

Mastering Banking Success: Essential Strategies to Excel in Your Career

You may want to see also

![]()

Manually entering bank transactions in MYOB

One critical aspect of manual entry is transaction categorization. MYOB allows you to assign each transaction to a specific account, such as "Office Expenses" or "Sales Income," which directly impacts your profit and loss statement. For example, if you’re entering a $500 payment to a supplier, ensure it’s coded to the correct expense account rather than a general account like "Bank." Misclassification can distort financial reports, making it harder to track cash flow or identify trends. Use MYOB’s Account Right List feature to create custom categories tailored to your business needs, ensuring every transaction is accurately reflected in your books.

While manual entry offers control, it’s not without risks. Common pitfalls include duplicate entries, omitted transactions, and transposition errors (e.g., typing $125 as $152). To mitigate these, maintain a systematic approach: reconcile your MYOB records with bank statements monthly, and use the Memorise Transaction feature for recurring entries like rent or payroll. Additionally, leverage MYOB’s Audit Trail to track changes and identify mistakes. For businesses with high transaction volumes, consider batching entries—grouping similar transactions (e.g., multiple office supply purchases) into a single session to improve efficiency without sacrificing accuracy.

Finally, manual entry in MYOB is an opportunity to strengthen financial discipline. By actively engaging with each transaction, you gain deeper insights into your business’s financial health. For instance, regularly entering and reviewing transactions can highlight unnecessary expenses or untapped revenue streams. Pair this process with MYOB’s Reporting Tools to generate cash flow statements or profit and loss reports, turning raw data into actionable intelligence. While automated feeds save time, manual entry ensures you remain intimately connected to your financial operations, fostering a proactive approach to money management.

Exploring Morgan Stanley Private Bank's Size and Global Reach

You may want to see also

![]()

Correcting errors in bank transactions in MYOB

Errors in bank transactions can disrupt financial records and lead to discrepancies in your MYOB account. Identifying and correcting these mistakes promptly is crucial for maintaining accurate financial data. When you notice an incorrect transaction, such as a wrong amount, date, or account allocation, MYOB provides tools to rectify these errors without compromising the integrity of your records. The key is to act swiftly and methodically to ensure the correction aligns with accounting principles and MYOB’s functionality.

To correct an error, start by locating the incorrect transaction in the bank register or reconciliation window. MYOB allows you to edit transactions directly, but this approach is not always advisable, especially if the transaction has already been reconciled. Instead, use the "Delete" or "Void" function for unreconciled transactions, ensuring the error is removed without affecting the balance. For reconciled transactions, the process is more intricate. You must first unreconcile the account, which involves reversing the reconciliation process to access and modify the transaction. This step requires careful attention to avoid further discrepancies.

Once the transaction is accessible, create a reversing entry to offset the error. For instance, if a deposit was recorded as $500 instead of $50, enter a withdrawal of $450 to correct the balance. Follow this with a new, accurate transaction reflecting the correct amount. This two-step process ensures a clear audit trail, allowing you to track the correction and maintain transparency in your financial records. Always double-check the account balance and reconciliation report after making corrections to confirm accuracy.

A common pitfall is attempting to correct errors by directly modifying reconciled transactions without unreconciliating the account first. This can lead to unbalanced books and complicate future reconciliations. Another mistake is failing to document the correction process, which is essential for accountability and compliance. To avoid these issues, familiarize yourself with MYOB’s reconciliation tools and practice in a test environment before correcting errors in live data. Additionally, consider consulting MYOB’s support resources or an accounting professional for complex scenarios.

In conclusion, correcting errors in bank transactions in MYOB requires precision and adherence to specific procedures. By following a structured approach—unreconciling the account, creating reversing entries, and documenting changes—you can maintain accurate financial records while minimizing the risk of further errors. Regularly reviewing transactions and staying informed about MYOB’s features will enhance your ability to manage corrections efficiently.

Mastering Bank Revenue Audits: A Comprehensive Step-by-Step Guide

You may want to see also

Frequently asked questions

To enter a bank deposit in MYOB, go to Banking > Spend/Receive Money, select the bank account, choose Receive Money, enter the details (date, amount, customer, etc.), and click Record.

To record a bank transfer, go to Banking > Transfer Money, select the "Transfer from" and "Transfer to" accounts, enter the amount and date, and click Record.

To reconcile bank transactions, go to Banking > Bank Reconciliation, select the account, enter the statement date and ending balance, match transactions, and click Reconcile when complete.

To enter a bank withdrawal, go to Banking > Spend/Receive Money, select the bank account, choose Spend Money, enter the details (date, amount, payee, etc.), and click Record.