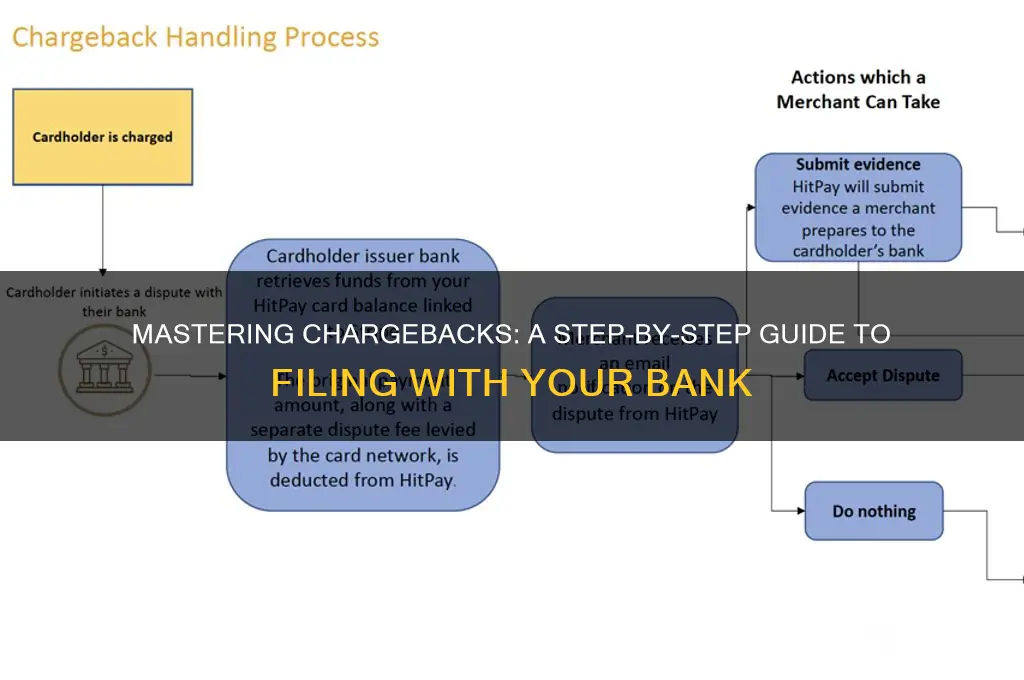

Filing a chargeback with your bank is a crucial process for resolving disputes over unauthorized or fraudulent transactions, as well as for addressing issues with goods or services that were not delivered as promised. It involves formally requesting your bank to reverse a transaction, typically after attempts to resolve the issue directly with the merchant have failed. Understanding the steps to file a chargeback, including gathering necessary documentation, contacting your bank within the specified timeframe, and providing detailed evidence to support your claim, is essential to ensure a successful outcome. This process not only helps protect your finances but also holds merchants accountable for their transactions.

| Characteristics | Values |

|---|---|

| Definition | A chargeback is a reversal of a credit or debit card transaction initiated by the cardholder through their bank. |

| Reasons for Filing | Fraudulent charges, unauthorized transactions, goods/services not received, billing errors, or disputes with merchants. |

| Time Limit | Typically 60–120 days from the transaction date, depending on the bank and card network. |

| Required Documentation | Proof of transaction (receipt, invoice), communication with the merchant, and any relevant evidence (e.g., emails, photos). |

| Process Steps | 1. Contact the merchant to resolve the issue. 2. If unresolved, contact your bank. 3. Submit a chargeback request with required documentation. 4. Bank investigates and decides. |

| Card Network Policies | Visa, Mastercard, American Express, and Discover have specific chargeback reason codes and procedures. |

| Fees | Some banks may charge a fee for filing a chargeback, refunded if successful. |

| Impact on Credit Score | Generally does not affect credit score, but frequent chargebacks may raise red flags. |

| Merchant Response | Merchants can dispute the chargeback, leading to further investigation by the bank or card network. |

| Outcome | If successful, the transaction is reversed, and funds are returned to the cardholder. If denied, the cardholder may need to repay the amount. |

| Prevention Tips | Monitor transactions regularly, use secure payment methods, and keep records of purchases and communications. |

Explore related products

What You'll Learn

- Understanding Chargeback Reasons: Identify valid reasons for filing, such as fraud, non-receipt, or defective goods

- Gathering Required Evidence: Collect receipts, emails, and transaction details to support your chargeback claim

- Contacting Your Bank: Reach out to your bank via phone, online portal, or in-person to initiate the process

- Submitting a Dispute Form: Complete and submit the bank’s chargeback dispute form with accurate information

- Following Up on Status: Track the progress of your chargeback and respond promptly to any bank requests

![]()

Understanding Chargeback Reasons: Identify valid reasons for filing, such as fraud, non-receipt, or defective goods

Chargebacks are a consumer's last resort when a purchase goes awry, but not all disputes qualify. Banks and card networks have strict criteria for what constitutes a valid claim, and understanding these reasons is crucial to navigating the process successfully. The most common grounds for a chargeback fall into three categories: fraud, non-receipt of goods or services, and defective or misrepresented products. Each reason has its nuances, and recognizing which applies to your situation is the first step in building a compelling case.

Fraudulent charges are perhaps the most straightforward reason for a chargeback. If you spot an unauthorized transaction on your statement—whether due to identity theft, a stolen card, or unrecognized merchant—you have a strong case. However, timing is critical. Most banks require you to report fraud within 60 days of the statement date, though some may extend this to 120 days. Keep detailed records of any communication with the bank and, if possible, file a police report to bolster your claim. This not only strengthens your case but also helps authorities track fraudulent activity.

Non-receipt of goods or services is another valid reason, but it’s often more complex. For instance, if you ordered a product that never arrived, or paid for a service that was never rendered, you can file a chargeback. However, banks typically require proof that you attempted to resolve the issue with the merchant first. This could include emails, delivery tracking information, or receipts showing the purchase. Be cautious with digital goods or services, as some banks may classify these as "received" if you’ve accessed them even once. Always document your efforts to contact the seller before escalating to a chargeback.

Defective or misrepresented goods present a trickier scenario, as the burden of proof lies heavily on the consumer. If an item arrives damaged, doesn’t match its description, or fails to function as advertised, you may have grounds for a chargeback. However, banks often require evidence such as photos, return policies, or correspondence with the merchant. For high-value items, consider retaining an independent expert to assess the defect. Additionally, be wary of "buyer’s remorse" claims—simply disliking a product doesn’t qualify as a valid reason. Focus on tangible issues that deviate from the merchant’s promises.

In all cases, the key to a successful chargeback is preparation and documentation. Before filing, review your bank’s specific policies and gather all relevant evidence. While chargebacks are a powerful tool for protecting consumers, they should be used judiciously. Misuse can lead to fees, account restrictions, or even closure. By understanding the valid reasons for filing and approaching the process methodically, you can safeguard your finances while maintaining a positive relationship with your bank.

Ernie Banks' Wife Liz: Unveiling Her Age and Life Story

You may want to see also

Explore related products

$33.45

![]()

Gathering Required Evidence: Collect receipts, emails, and transaction details to support your chargeback claim

Filing a chargeback requires more than a verbal assertion—it demands concrete proof. Receipts, emails, and transaction details form the backbone of your claim, serving as irrefutable evidence that can sway the bank’s decision in your favor. Without these, your case risks being dismissed as unsubstantiated. Think of them as the bricks and mortar of your argument, each piece reinforcing the legitimacy of your dispute.

Begin by scouring your records for any document tied to the transaction. Receipts, whether digital or physical, should be your first target. Ensure they clearly display the date, amount, and merchant name. If the purchase was made online, download or screenshot the confirmation page—this often contains critical details like order numbers and descriptions. Emails exchanged with the merchant, especially those addressing issues like non-delivery or defective products, are equally vital. Organize these chronologically to illustrate a clear timeline of events.

Transaction details from your bank or credit card statement are another cornerstone. Highlight the disputed charge, noting the exact date, amount, and merchant identifier. If the transaction was recurring, gather statements showing the pattern. For international purchases, include currency conversion details to avoid discrepancies. Pro tip: If the merchant used a different name on your statement than their public-facing brand, cross-reference this information to avoid confusion during the chargeback process.

While collecting evidence, be meticulous but selective. Banks don’t need your entire financial history—just the relevant pieces. For instance, if disputing a subscription charge, include only the statements showing the unauthorized renewals, not every monthly bill. Similarly, if the issue involves a product’s condition, attach photos or inspection reports alongside your emails. Overloading the bank with irrelevant data can dilute the impact of your strongest evidence.

Finally, anticipate counterarguments. Merchants often dispute chargebacks, so ensure your evidence is comprehensive enough to address potential rebuttals. For example, if claiming non-delivery, include tracking information showing the package never arrived. If the dispute involves a service, provide screenshots of failed attempts to use it. The goal is to leave no room for doubt, making your chargeback claim as airtight as possible.

Sperm Bank Workers: China's Unique Job

You may want to see also

Explore related products

![]()

Contacting Your Bank: Reach out to your bank via phone, online portal, or in-person to initiate the process

The first step in filing a chargeback is to contact your bank, and the method you choose can significantly impact the process's efficiency. Each bank offers multiple channels for communication, but not all are created equal. Phone calls, for instance, provide immediate interaction, allowing you to explain your situation in detail and receive real-time feedback. This method is particularly useful for complex cases where written communication might lead to misunderstandings. When calling, have your account information and transaction details ready to streamline the conversation. Most banks have dedicated fraud or dispute departments, so ask to be directed to the appropriate team to ensure your case is handled by specialists.

In contrast, online portals offer a convenient and often faster alternative, especially for tech-savvy individuals. Many banks provide secure messaging systems or dispute forms within their online banking platforms. This method allows you to submit your request at any time, avoiding potential hold times associated with phone calls. When using an online portal, be concise and clear in your explanation, providing all necessary transaction details, including dates, amounts, and merchant information. Screenshots or digital copies of receipts can be invaluable here, as they provide visual evidence to support your claim. Remember, the goal is to make it as easy as possible for the bank to understand and process your request.

For those who prefer a more personal touch or have complex cases that require detailed discussion, an in-person visit to a local branch can be the most effective approach. This method allows for a face-to-face conversation, which can be crucial in conveying the urgency or intricacies of your situation. When visiting a branch, bring all relevant documentation, including receipts, correspondence with the merchant, and any previous communication with the bank regarding the issue. A well-prepared in-person meeting can expedite the process, as it provides a comprehensive overview of your case in one interaction.

Each contact method has its advantages, and the choice depends on your personal preference and the nature of your dispute. Phone calls offer immediacy, online portals provide convenience, and in-person visits allow for detailed, personal interaction. Regardless of the method, the key is to provide clear, concise, and complete information. Banks typically have specific time frames for filing chargebacks, so prompt action is essential. By choosing the most suitable contact method and presenting your case effectively, you can significantly increase the chances of a successful chargeback resolution.

It's worth noting that some banks may have specific requirements or preferences for how they handle chargeback requests. For instance, certain banks might prioritize online submissions to streamline their internal processes, while others may encourage phone calls for a more personalized approach. Checking your bank's website or contacting their customer service for guidance on their preferred method can save time and ensure your request is handled efficiently. Ultimately, the goal is to initiate the chargeback process promptly and provide the bank with all the necessary information to support your claim.

Deactivating Standard Bank Cellphone Banking: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Submitting a Dispute Form: Complete and submit the bank’s chargeback dispute form with accurate information

Filing a chargeback begins with a critical step: submitting a dispute form to your bank. This form is your formal request for the bank to investigate and potentially reverse a transaction you believe is unauthorized, fraudulent, or incorrect. Accuracy is paramount here—incorrect or incomplete information can delay the process or even lead to a denial. Start by gathering all relevant details: the transaction date, amount, merchant name, and a clear explanation of why you’re disputing the charge. Most banks provide dispute forms online through their banking portals or mobile apps, though some may require a written request. Treat this form as a legal document; double-check every field before submission.

The structure of a dispute form varies by bank but typically includes sections for personal information, transaction details, and a narrative explaining the dispute. Be concise yet detailed in your explanation. For instance, if the charge is unauthorized, state explicitly, “I did not authorize this transaction, and I do not recognize the merchant.” If the issue is related to a product or service, describe the problem clearly, such as, “The item was never delivered, and the merchant has not responded to my inquiries.” Avoid emotional language; stick to facts. Attach supporting documents like receipts, emails, or screenshots to strengthen your case. Remember, the bank will use this information to decide whether to proceed with the chargeback.

One common mistake is assuming the bank will automatically side with you. Banks are required to investigate disputes fairly, which means they’ll scrutinize your claim. If your dispute lacks evidence or appears frivolous, it may be denied. For example, claiming a charge is fraudulent without proof can backfire if the bank finds evidence of your authorization. Similarly, disputing a subscription charge because you forgot to cancel it is unlikely to succeed. Understand the chargeback reason codes—such as “fraud,” “product not received,” or “service not as described”—and select the one that best fits your situation. This ensures your dispute is categorized correctly and increases the chances of a favorable outcome.

Submitting the form is just the beginning. After submission, the bank typically has 30 days to investigate, though timelines vary. During this period, monitor your account and keep records of all communication with the bank. If the dispute is complex, the bank may request additional information or documentation. Respond promptly to avoid delays. Once the investigation is complete, the bank will notify you of the decision. If the chargeback is approved, the disputed amount will be credited to your account. If denied, you may have the option to appeal or pursue other remedies, such as contacting the merchant directly or seeking legal advice.

In summary, submitting a dispute form is a structured process that demands precision and preparation. Approach it methodically: gather evidence, complete the form accurately, and understand the criteria for a successful dispute. While the process can be time-consuming, it’s a powerful tool for resolving transaction issues. Treat it as your formal case to the bank, and you’ll maximize your chances of a positive resolution.

Can Banks Mortgage Foreclosed Homes?

You may want to see also

Explore related products

![]()

Following Up on Status: Track the progress of your chargeback and respond promptly to any bank requests

After initiating a chargeback, the waiting game begins, but it’s not a passive process. Banks typically provide a reference number or case ID once your claim is filed, which serves as your key to tracking progress. Log into your online banking portal or mobile app regularly to check for updates. Most institutions have a dedicated section for disputes or claims where you can view the status, estimated resolution time, and any pending actions required from you. If digital tracking isn’t available, call your bank’s customer service line and use your reference number to inquire about the status. Proactive monitoring ensures you’re aware of any delays or additional steps needed to keep the process moving.

Banks often require supplementary documentation or clarification during the chargeback process, and delays in responding can stall or even jeopardize your case. If your bank requests additional information, such as receipts, correspondence with the merchant, or proof of attempted resolution, respond within 48 hours. Provide clear, concise, and organized documentation to support your claim. For example, if disputing a fraudulent charge, include screenshots of unauthorized transactions and a statement confirming you didn’t authorize them. Ignoring or delaying these requests can result in the bank ruling against you, so treat these communications as time-sensitive priorities.

Comparing the chargeback process to a legal case highlights the importance of persistence and organization. Just as a lawyer follows up on court filings, you must stay engaged with your bank’s progress. Set calendar reminders to check the status weekly, especially if the estimated resolution time exceeds 30 days. If the process seems stagnant, escalate your inquiry by contacting the bank’s dispute resolution team directly or requesting a supervisor. Keep a detailed record of all communications, including dates, names of representatives, and summaries of conversations. This documentation can be invaluable if discrepancies arise or if you need to appeal a decision later.

Finally, understanding the timeline and potential outcomes of a chargeback helps manage expectations. Banks typically have 30 to 90 days to investigate, though complex cases may take longer. During this period, the merchant has the opportunity to challenge your claim, which could extend the process. If the bank rules in your favor, the disputed amount is credited to your account, often temporarily, until the investigation concludes. If the decision goes against you, you can appeal, but this requires additional evidence or a stronger case. Knowing these stages allows you to anticipate next steps and remain proactive in securing a fair resolution.

Shaving for Bankers: A Necessary Evil?

You may want to see also

Frequently asked questions

A chargeback is a request made to your bank to reverse a transaction when you believe it was unauthorized, fraudulent, or if the merchant failed to deliver the goods or services as agreed. File a chargeback if you’ve exhausted all other options, such as contacting the merchant directly, and the issue remains unresolved.

To file a chargeback, contact your bank’s customer service or visit your online banking portal. Provide details about the transaction, including the date, amount, and reason for the dispute. Your bank will guide you through the process, which may involve submitting a formal dispute form or written statement.

The chargeback process typically takes 30 to 90 days, depending on your bank and the complexity of the case. Once filed, your bank will investigate the claim, temporarily reverse the charge, and notify the merchant. The merchant can dispute the chargeback, which may extend the timeline. If the bank rules in your favor, the charge is permanently reversed.