Filing TDS (Tax Deducted at Source) returns is a critical compliance requirement for banks in India, as they are responsible for deducting tax at the source on various payments such as interest on deposits, dividends, and other specified transactions. To file TDS returns, banks must first register on the TRACES (TDS Reconciliation Analysis and Correction Enabling System) portal and obtain a TAN (Tax Deduction and Collection Account Number). The process involves preparing Form 24Q or Form 26Q, depending on the nature of the payments, and submitting it electronically through the NSDL (National Securities Depository Limited) website. Banks need to ensure accurate reporting of deductee details, tax deductions, and challan information to avoid penalties. Regular reconciliation of TDS payments with Form 26AS and timely filing within the due dates, typically quarterly, are essential to maintain compliance with the Income Tax Act, 1961.

| Characteristics | Values |

|---|---|

| Applicable Forms | Form 26Q (For TDS on payments other than salary) |

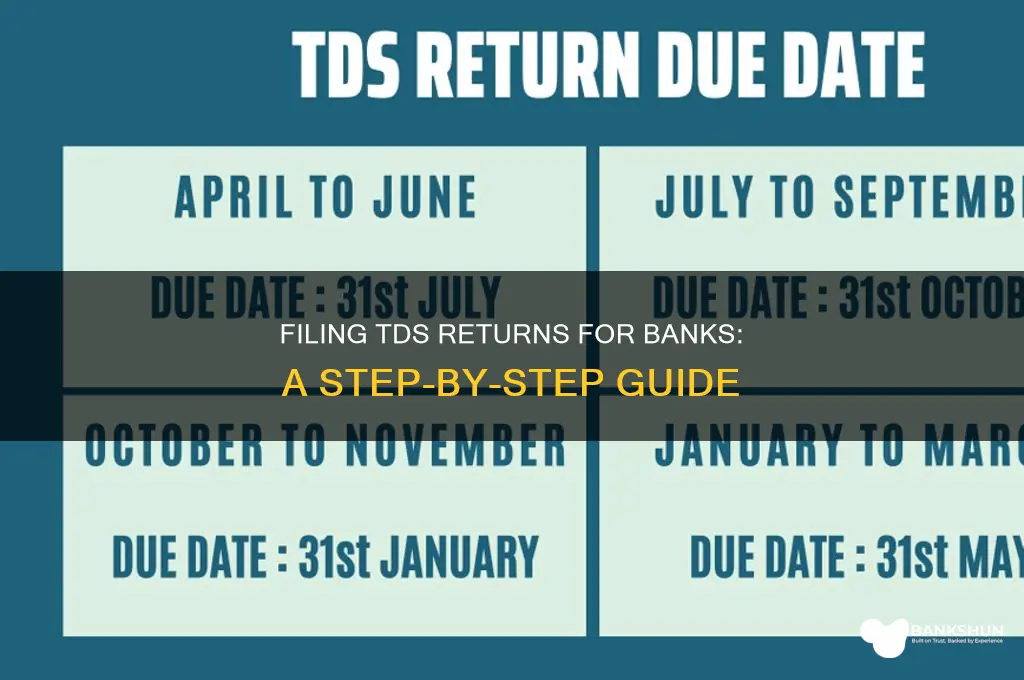

| Due Dates | Quarterly: 31st July, 31st October, 31st January, 31st May (for the respective quarters) |

| Filing Mode | Online through the NSDL website (https://www.tin-nsdl.com/) |

| Prerequisites | 1. TAN (Tax Deduction Account Number) 2. Digital Signature Certificate (DSC) or E-signing 3. FVU (File Validation Utility) Software |

| Challan Details | Challan 281 is used for depositing TDS |

| Penalty for Late Filing | Rs. 200 per day until the default continues (Section 234E) |

| Interest on Late Deposit | 1% per month or part of the month (Section 201(1A)) |

| Correction of Return | File a corrective return using the same form (26Q) |

| Verification | Returns must be verified by the authorized signatory using DSC or E-signing |

| Records Maintenance | Banks must maintain TDS records for 6 years from the end of the relevant assessment year |

| Annual Return | Form 24Q (for salary payments) and Form 26Q (for non-salary payments) must be filed annually |

| PAN Verification | Banks must verify the PAN of deductees before filing returns |

| Refund Process | Excess TDS can be claimed as a refund by the deductee while filing ITR |

| Updates | Regularly check NSDL website for updates in FVU software and filing procedures |

Explore related products

What You'll Learn

![]()

TDS Return Due Dates

Filing TDS (Tax Deducted at Source) returns is a critical compliance requirement for banks, and understanding the due dates is paramount to avoid penalties and ensure smooth operations. The due dates for TDS returns are not arbitrary; they are structured to align with the financial calendar and provide a systematic approach to tax collection. For banks, the TDS return due dates are typically quarterly, with specific deadlines for each quarter. The first quarter (April to June) has a due date of July 31, the second quarter (July to September) is due by October 31, the third quarter (October to December) by January 31, and the fourth quarter (January to March) by May 31. These dates are non-negotiable and apply uniformly across all entities responsible for TDS deductions, including banks.

Analyzing the implications of these due dates reveals a strategic design by tax authorities. By staggering the deadlines quarterly, the system ensures a continuous flow of tax revenue throughout the financial year. For banks, this means maintaining meticulous records of TDS deductions on a monthly basis to avoid last-minute rushes and errors. Missing a due date can result in penalties under Section 234E of the Income Tax Act, which imposes a fine of ₹200 per day until the return is filed. This underscores the importance of integrating TDS return filing into the bank’s routine compliance calendar.

From an instructive perspective, banks should adopt a proactive approach to manage TDS return due dates effectively. First, designate a compliance team or individual responsible for tracking and filing TDS returns. Second, leverage technology by using TDS return filing software that automates data compilation and validation, reducing manual errors. Third, maintain a checklist of required documents, such as Form 26Q (for TDS on payments other than salaries) and Form 27Q (for TDS on payments to non-residents), to ensure all necessary details are included. Fourth, conduct periodic internal audits to verify the accuracy of TDS deductions and filings. Finally, set internal deadlines a week before the actual due date to account for unforeseen delays.

Comparatively, banks can draw lessons from other industries that handle TDS returns. For instance, corporate entities often use ERP systems integrated with tax compliance modules to streamline the process. Banks, with their robust IT infrastructure, can adopt similar tools to enhance efficiency. Additionally, benchmarking against peers can provide insights into best practices, such as real-time TDS tracking and automated reminders for due dates. While banks deal with larger transaction volumes, the principles of timely compliance remain consistent across sectors.

In conclusion, mastering TDS return due dates is not just about adhering to deadlines but also about embedding a culture of compliance within the bank’s operations. By understanding the structure, analyzing the implications, and adopting proactive measures, banks can navigate this regulatory requirement with ease. The key takeaway is that timely and accurate TDS return filing is not just a legal obligation but a reflection of the bank’s commitment to financial integrity and operational excellence.

Does BMO Bank Accept Coins in Illinois? A Quick Guide

You may want to see also

Explore related products

![]()

Form 26Q Filing Process

Banks and financial institutions in India are mandated to deduct Tax Deducted at Source (TDS) on various payments, such as interest on fixed deposits exceeding ₹40,000 (for senior citizens, ₹50,000) in a financial year. Filing TDS returns is a critical compliance requirement, and Form 26Q is specifically designed for reporting TDS deductions on payments other than salaries. This form is filed quarterly, ensuring transparency and accountability in tax collections.

The filing process begins with preparation of data, where banks compile details of TDS deductions, including PANs of deductees, payment amounts, and TDS rates. Accuracy is paramount, as errors can lead to penalties or notices from the Income Tax Department. For instance, a missing PAN or incorrect TDS rate can result in a 200% penalty under Section 272A. Banks often use accounting software or ERP systems to automate data compilation, reducing manual errors.

Once data is ready, Form 26Q is filed online via the NSDL (National Securities Depository Limited) website. The process involves logging into the e-filing portal, selecting the relevant quarter, and uploading the prepared file in the specified format. Banks must ensure the file adheres to the TRACES (TDS Reconciliation Analysis and Correction Enabling System) format, which includes fields like challan details, deductee information, and TDS amounts. A digital signature certificate (DSC) is mandatory for authentication, ensuring the filer’s identity and data integrity.

After submission, the FVU (File Validation Utility) validates the file for errors. If discrepancies are found, the file is rejected, and banks must rectify and resubmit. Upon successful validation, a provisional receipt is generated, followed by a Form 26Q acknowledgment after processing. This acknowledgment must be preserved as proof of filing. Notably, late filing attracts a fee of ₹200 per day under Section 234E, capped at the TDS amount.

A comparative analysis reveals that Form 26Q is more complex than Form 24Q (for salary TDS) due to the diversity of payments it covers. For instance, TDS on rent, professional fees, or interest payments requires meticulous categorization. Banks often conduct internal audits before filing to ensure compliance, leveraging tools like TRACES for reconciliation. This proactive approach minimizes risks and streamlines the process, making Form 26Q filing a seamless part of tax compliance.

In conclusion, mastering the Form 26Q filing process is essential for banks to avoid penalties and maintain regulatory compliance. By combining accurate data preparation, adherence to TRACES formats, and timely submission, banks can efficiently fulfill their TDS obligations. Practical tips include maintaining a PAN verification system, training staff on TRACES usage, and setting reminders for quarterly deadlines. This structured approach ensures not just compliance but also operational efficiency in tax management.

Step-by-Step Guide to RTGS Transactions in IDBI Bank

You may want to see also

Explore related products

$6.99

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UY218_.jpg)

![(Old Version) H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UY218_.jpg)

![]()

TDS Payment Procedures

Banks and financial institutions play a pivotal role in the Tax Deducted at Source (TDS) ecosystem, acting as both deductors and facilitators of tax payments. The TDS payment procedure is a critical component of this process, ensuring that taxes are remitted to the government in a timely and accurate manner. This procedure involves several steps, each requiring meticulous attention to detail to avoid penalties and ensure compliance with the Income Tax Act, 1961.

Step-by-Step Payment Process

The first step in the TDS payment procedure is the generation of a unique challan, specifically Form 281 (now replaced by Form 26QB, 26Q, etc., depending on the nature of payment). Banks must correctly identify the applicable form based on the type of payment, such as interest, rent, or professional fees. For instance, TDS on interest paid to residents is filed under Section 194A, while TDS on rent is covered under Section 194-I. Once the challan is generated, the bank must deposit the tax amount through the online tax payment portal of the NSDL (National Securities Depository Limited) or authorized bank branches. The payment should be made within 7 days from the end of the month in which the deduction is made. For example, if TDS is deducted in April, the payment must be made by May 7.

Critical Cautions and Common Pitfalls

One of the most common pitfalls in TDS payment is the incorrect selection of the assessment year or the tax deduction account number (TAN). Banks must ensure that the TAN is accurately entered to avoid discrepancies in the government’s records. Another critical aspect is the timely payment of TDS. Delayed payments attract interest at 1.5% per month under Section 201(1A) and a penalty of up to Rs. 1 lakh under Section 271H. Additionally, banks must be cautious while handling TDS on payments to non-residents, as these require separate forms (e.g., Form 27Q) and may involve withholding tax certificates (Form 16A) for foreign entities.

Leveraging Technology for Efficiency

Modern banking systems have integrated TDS payment procedures into their core operations, often through automated software solutions. These tools ensure that TDS calculations, challan generation, and payments are executed seamlessly, reducing the risk of human error. For instance, banks can use ERP systems or dedicated tax compliance software to track TDS deductions in real-time and generate reports for audit purposes. Such technological interventions not only streamline the process but also enhance transparency and accountability.

Post-Payment Responsibilities

After completing the TDS payment, banks must file the TDS return within the stipulated deadlines. For quarterly returns, the due dates are July 31, October 31, January 31, and May 31 for the respective quarters. Filing the return involves submitting Form 24Q (for salary payments) or Form 26Q (for non-salary payments) through the TRACES (TDS Reconciliation Analysis and Correction Enabling System) portal. Banks must also issue Form 16A to deductees as proof of tax deduction, which is crucial for individuals and entities to claim tax credits in their annual returns. Failure to issue these certificates can lead to dissatisfaction among customers and potential legal repercussions.

Strategic Takeaway

Mastering the TDS payment procedure is not just a compliance requirement but a strategic imperative for banks. Efficient management of TDS payments enhances operational credibility, fosters customer trust, and mitigates financial risks. By adopting a structured approach, leveraging technology, and staying updated with regulatory changes, banks can navigate the complexities of TDS payments with confidence. For instance, regular training sessions for staff on updated TDS regulations and the use of automated tools can significantly reduce errors and improve compliance rates. Ultimately, a robust TDS payment framework positions banks as reliable partners in the nation’s tax administration system.

Bank Transaction Records: Are They Mandatory?

You may want to see also

Explore related products

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UY218_.jpg)

![]()

TDS Certificate Generation

Banks play a crucial role in deducting Tax Deducted at Source (TDS) on various transactions, such as interest on fixed deposits exceeding ₹40,000 per annum. After deduction, the onus lies on the bank to generate and issue TDS certificates to the deductees, ensuring compliance with Income Tax Act provisions. This process, known as TDS Certificate Generation, is a critical step in the TDS return filing cycle for banks.

Understanding Form 16A: The TDS Certificate

The TDS certificate issued by banks is Form 16A, a document that serves as proof of tax deduction for the deductee. It contains essential details like the deductee's PAN, TAN of the bank, amount of income paid, TDS deducted, and the period of deduction. This form is crucial for individuals and entities to claim credit for TDS while filing their income tax returns.

Banks utilize specialized software or online platforms to generate Form 16A in bulk, ensuring accuracy and efficiency.

Generation Process: A Step-by-Step Breakdown

- Data Compilation: Banks collate transaction data for the relevant period, identifying transactions subject to TDS deduction. This includes details like interest payments, commission payouts, etc.

- TDS Calculation: The bank's system calculates the applicable TDS based on the transaction amount and prevailing tax rates.

- Form 16A Generation: Utilizing dedicated software or online portals, the bank generates Form 16A for each deductee, populating it with the compiled data and calculated TDS.

- Validation and Verification: Generated forms undergo rigorous validation checks to ensure accuracy of details like PAN, TAN, and TDS amounts.

- Issuance: Banks issue Form 16A to deductees either physically or electronically, adhering to the prescribed timelines.

Challenges and Best Practices

Despite its importance, TDS certificate generation can pose challenges for banks. Data accuracy, timely issuance, and managing large volumes of transactions are common hurdles. To overcome these, banks should:

- Invest in robust TDS software: Automated solutions streamline the process, minimize errors, and ensure timely generation.

- Implement stringent data validation checks: Double-checking PAN details, transaction amounts, and TDS calculations is crucial to avoid discrepancies.

- Establish clear timelines: Define internal deadlines for data compilation, generation, and issuance to ensure compliance with statutory timelines.

- Offer electronic issuance options: Providing deductees with the option to download Form 16A online enhances convenience and reduces administrative burden.

By adopting these best practices, banks can ensure efficient and accurate TDS certificate generation, fulfilling their obligations and facilitating smooth tax compliance for their customers.

Business Hours: Are Banks Open on Saturdays?

You may want to see also

Explore related products

![H&R Block Tax Software Deluxe 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51Mlng5FWYL._AC_UY218_.jpg)

![]()

TDS Return Correction Steps

Filing TDS returns is a critical compliance requirement for banks, but errors can occur despite meticulous preparation. The Income Tax Department allows for corrections through a structured process, ensuring accuracy and adherence to regulations. Understanding the TDS return correction steps is essential for banks to rectify mistakes efficiently and avoid penalties.

Identifying the Need for Correction

The first step in the TDS return correction process is identifying the error. Common mistakes include incorrect PAN details, wrong challan information, or mismatched deductee particulars. Banks should cross-verify the filed return with source documents and Form 26AS to pinpoint discrepancies. Once identified, the type of error determines the correction procedure—whether it’s a minor typo or a major data mismatch affecting tax computations.

Filing a Correction Statement

Banks must file a correction statement using the relevant TDS return form (e.g., Form 24Q, 26Q, or 27Q) based on the payment type. The correction statement should be submitted online through the NSDL or TIN portal. While filing, select the appropriate correction type: ‘C1’ for correcting challan details, ‘C2’ for deductee-related changes, or ‘C3’ for both. Ensure all mandatory fields are accurately filled, and the corrected data aligns with supporting documents.

Handling Late Fees and Interest

If the correction is filed after the due date, banks may incur late fees under Section 234E (Rs. 200 per day until the return is filed) and interest under Section 201 (1% per month or part thereof until the tax is deducted). To minimize financial impact, rectify errors promptly and ensure the corrected return is filed within the earliest possible timeframe.

Post-Correction Follow-Up

After filing the correction statement, banks should verify its acceptance by checking the TDS CPC portal. If rejected, the portal will provide reasons for rejection, allowing for further corrections. Additionally, banks must update their internal records and communicate the changes to the deductees to ensure their Form 26AS reflects the corrected details. This ensures transparency and avoids future discrepancies.

Best Practices for Error Prevention

While corrections are permissible, prevention is always better. Banks should implement robust internal controls, such as automated data validation tools and regular audits, to minimize errors. Training staff on TDS compliance and maintaining a checklist for return filing can significantly reduce the need for corrections. Proactive measures not only save time but also enhance the bank’s reputation for compliance.

Bank of Dave: Fact or Fiction? Uncovering the Truth Behind the Legend

You may want to see also

Frequently asked questions

The due date for filing TDS returns (Form 24Q, 26Q, 27Q, or 27EQ) for banks is typically the 31st of July for the first quarter, 31st of October for the second quarter, 31st of January for the third quarter, and 31st of May for the fourth quarter of the financial year.

Banks primarily use Form 26Q for TDS on payments other than salaries (e.g., interest, rent, etc.) and Form 27Q for TDS on payments to non-residents. Form 24Q is used for TDS on salaries, though this is less common for banks unless they are deducting TDS on salary payments.

Banks need the following documents for filing TDS returns: PAN details of deductees, TDS challan details (Form 281), and a consolidated file containing details of TDS deductions (as per the respective form format). Additionally, a digital signature certificate (DSC) is required for online filing.