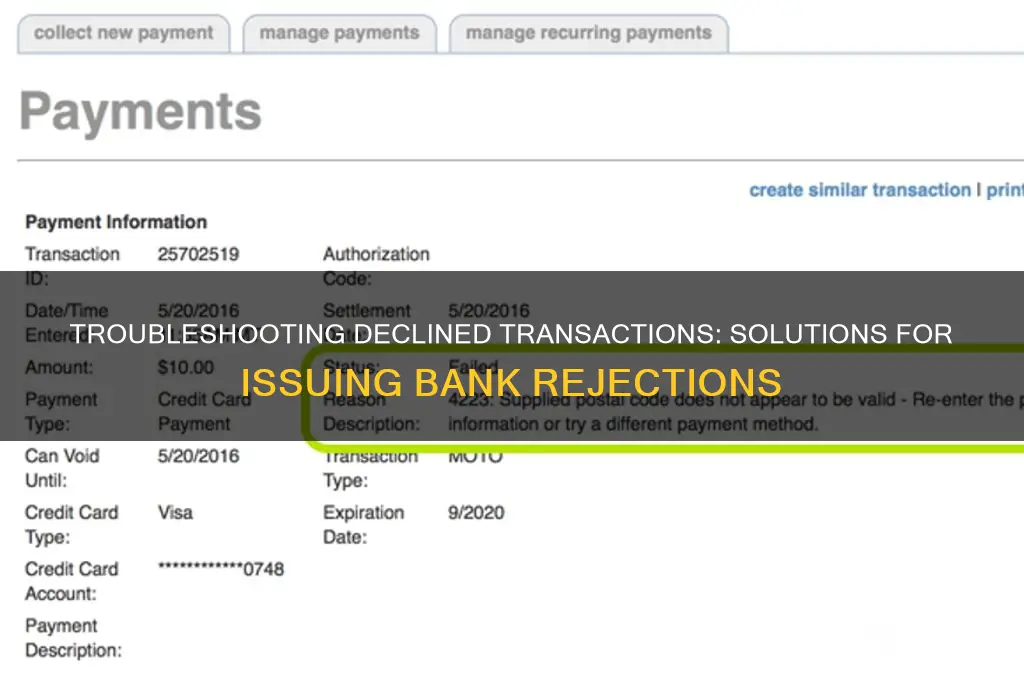

When a payment is declined by the issuing bank, it can be frustrating for both the customer and the merchant, often stemming from issues like insufficient funds, expired cards, or security concerns. Resolving this requires a systematic approach: first, the customer should verify their account balance and card details to ensure accuracy, while the merchant can provide clear error messages and suggest alternative payment methods. If the issue persists, contacting the bank directly can help identify specific reasons for the decline, such as fraud prevention measures or transaction limits. Additionally, merchants can implement tools like address verification systems (AVS) or 3D Secure to enhance transaction security and reduce the likelihood of future declines. By addressing the root cause and improving communication, both parties can work together to ensure a smoother payment process.

| Characteristics | Values |

|---|---|

| Common Reasons for Decline | Insufficient funds, expired card, incorrect card details, suspicious activity, daily/monthly limits exceeded, card not activated. |

| Immediate Actions | Double-check card details, ensure sufficient funds, confirm card activation, verify if the card is expired. |

| Contact Issuing Bank | Call the bank’s customer service number (usually on the back of the card) to inquire about the decline reason. |

| Fraud Prevention | Notify the bank if the transaction was legitimate to avoid fraud blocks. |

| Alternative Payment Methods | Use a different card, PayPal, or other payment options if available. |

| Retry Transaction | Wait a few minutes and retry the transaction after resolving the issue. |

| Check for Holds/Blocks | Ensure no temporary holds or blocks are placed on the account by the bank. |

| Update Billing Information | Verify and update billing address, phone number, or other details if outdated. |

| International Transactions | Notify the bank if making an international purchase to avoid blocks. |

| Merchant Issues | Contact the merchant to ensure there are no issues on their end (e.g., system errors). |

| Monitor Account Activity | Regularly check account statements for unauthorized or suspicious activity. |

| Prevent Future Declines | Keep card details updated, monitor spending limits, and maintain sufficient funds. |

Explore related products

What You'll Learn

- Verify card details accuracy: Double-check card number, expiration date, CVV, and name for errors

- Check for insufficient funds: Ensure the cardholder has enough balance to cover the transaction

- Confirm card activation status: Verify if the card is active and not expired or blocked

- Address fraud prevention flags: Resolve potential security holds or suspicious activity alerts with the bank

- Contact issuing bank directly: Reach out to the bank for specific decline reasons and solutions

![]()

Verify card details accuracy: Double-check card number, expiration date, CVV, and name for errors

A single typo can derail a transaction. Transposing digits in the card number, mistyping the CVV, or entering an outdated expiration date are common culprits behind "declined by issuing bank" errors. These mistakes trigger automatic rejections as banks flag discrepancies between the entered data and their records. Even a minor error, like a misplaced space or a missing digit, can disrupt the payment process. This simple yet critical step of verifying card details is often overlooked, yet it’s the easiest fix for many declined transactions.

Begin by methodically re-entering the card number, ensuring each digit is correct and in the right sequence. Pay attention to the expiration date, as using an expired card or mistyping the month or year will immediately trigger a decline. The CVV, a three- or four-digit code on the back or front of the card, must match exactly—banks use this as a security measure to confirm physical possession of the card. Lastly, confirm the name on the card matches the billing information provided. Discrepancies, such as abbreviations or missing middle names, can cause rejections.

Consider using a magnifying glass or bright lighting if the card details are hard to read. For online transactions, type slowly and deliberately, avoiding rushed inputs. If you’re assisting someone else with their card, ask them to read the details aloud while you enter them, reducing the chance of errors. For recurring payments, periodically verify stored card details, as expiration dates or CVVs may change over time. These small precautions can prevent unnecessary declines and streamline the payment process.

While verifying card details seems straightforward, it’s a step often rushed or skipped, leading to avoidable frustration. Banks and payment processors rely on precise data to authenticate transactions, and even minor discrepancies can halt the process. By taking a few extra seconds to double-check each field, you not only increase the likelihood of approval but also demonstrate diligence in handling sensitive financial information. This simple practice is a cornerstone of successful transactions, bridging the gap between a declined payment and a seamless experience.

Disputing Ally Bank Charges: A Step-by-Step Guide to Resolve Disputes

You may want to see also

Explore related products

![]()

Check for insufficient funds: Ensure the cardholder has enough balance to cover the transaction

Insufficient funds are a common reason for transaction declines, often leaving both merchants and cardholders perplexed. When a payment is flagged as "declined by issuing bank," the first step should always be to verify the cardholder’s available balance. Banks and financial institutions have strict protocols to prevent overdrafts, and even a minor shortfall can trigger a rejection. For instance, if a transaction of $150 is attempted but the account holds only $145, the bank will automatically decline it to protect both parties from fees and complications.

To address this issue, cardholders should log into their banking portal or mobile app to check their real-time balance. It’s crucial to account for pending transactions, as these can reduce available funds temporarily. For example, a recent gas station authorization hold might tie up $75, leaving less than expected for other purchases. Merchants can assist by suggesting customers review their account details immediately, ensuring transparency and avoiding repeated failed attempts.

A practical tip for cardholders is to maintain a buffer in their account, especially when making large or recurring payments. Financial advisors often recommend keeping at least 10% of the account balance free to accommodate unexpected holds or fluctuations. For businesses, integrating a balance-check reminder in the checkout process can reduce declines. For instance, a prompt like, "Please ensure your account has sufficient funds before proceeding," can serve as a helpful nudge.

Comparatively, while insufficient funds are a straightforward issue, they often mask deeper financial habits. Frequent declines due to low balances may indicate a need for better budgeting or a shift to prepaid cards with set limits. On the merchant side, offering alternative payment methods like digital wallets or buy-now-pay-later options can mitigate the impact of such declines. Ultimately, addressing insufficient funds is not just about resolving a single transaction but fostering financial awareness and flexibility for both parties.

How Technology is Transforming Community Banks: Opportunities and Challenges

You may want to see also

Explore related products

![]()

Confirm card activation status: Verify if the card is active and not expired or blocked

A declined transaction can often be traced back to an inactive, expired, or blocked card. Before assuming the issue lies with the issuing bank, it’s crucial to confirm the card’s activation status. Many cards require activation upon receipt, a step that’s easy to overlook. Log in to your online banking portal or mobile app to check if the card is listed as active. If you’re unsure, call the number on the back of the card or the issuer’s customer service line to verify. This simple step can save time and frustration, ensuring the problem isn’t as complex as it initially seems.

Activation isn’t the only factor—expiration dates and blocked cards are equally important. Credit and debit cards typically expire every 3–5 years, and using an expired card will result in a decline. Check the embossed or printed date on the card to confirm its validity. Additionally, banks may block a card due to suspected fraud, unusual activity, or failure to meet payment terms. If your card is blocked, the issuer usually sends a notification via email, text, or mail. Ignoring these alerts can lead to unnecessary declines, so staying informed is key.

To proactively avoid this issue, set reminders for card expiration dates and monitor your account regularly. Most banks allow you to request a replacement card 30–60 days before expiration. If your card is blocked, contact the issuer immediately to resolve the issue. Provide any requested documentation promptly, such as proof of identity or transaction details, to expedite the unblocking process. Being proactive not only prevents declines but also strengthens your relationship with the bank.

Comparatively, while technical issues or insufficient funds are common reasons for declines, card activation status is often overlooked. Unlike those problems, which require external solutions, this issue is entirely within your control. By verifying activation, expiration, and block status, you can eliminate a major potential cause of declines. This approach is both efficient and empowering, putting you in the driver’s seat when it comes to managing your financial transactions.

Does Wells Fargo Finance Mobile Homes? A Comprehensive Guide

You may want to see also

Explore related products

![]()

Address fraud prevention flags: Resolve potential security holds or suspicious activity alerts with the bank

Fraud prevention flags are a critical line of defense for banks, but they can also be a source of frustration for legitimate customers. When a transaction is flagged as suspicious, it triggers a security hold, often resulting in a declined payment. Understanding why these flags occur is the first step to resolving them. Banks use complex algorithms to detect unusual patterns, such as transactions in unfamiliar locations, large purchases outside your typical spending habits, or multiple attempts to use a card in a short period. Recognizing these triggers can help you anticipate and address potential issues before they escalate.

To resolve a fraud prevention flag, start by contacting your bank immediately. Most banks have dedicated fraud departments or customer service lines available 24/7. Provide them with details about the transaction, including the date, time, location, and amount. Be prepared to verify your identity with personal information, such as your Social Security number or account details. If the transaction was legitimate, the bank may lift the hold after confirming the details with you. In some cases, they may require additional documentation, such as a receipt or proof of travel, to validate the purchase.

Prevention is just as important as resolution. To minimize future flags, keep your bank informed about upcoming travel plans or large purchases. Many banks offer online or mobile app features where you can submit travel notices or flag upcoming transactions. Additionally, monitor your account regularly for unauthorized activity. Setting up transaction alerts can help you catch suspicious activity early, allowing you to report it to your bank before a hold is placed. Proactive communication with your bank not only reduces the likelihood of declined transactions but also strengthens your relationship with the institution.

In some cases, fraud prevention flags may indicate a more serious issue, such as identity theft or card compromise. If you notice multiple flags or unauthorized transactions, take immediate action. Change your online banking passwords, request a new card, and consider placing a fraud alert on your credit report. While these steps may seem drastic, they are essential for protecting your financial security. Remember, banks are your partners in fraud prevention, and working together can help ensure your accounts remain safe and accessible.

Finally, stay informed about evolving fraud tactics and how banks are responding. Phishing scams, skimming devices, and data breaches are increasingly sophisticated, and banks continually update their security measures to counter these threats. Educating yourself about these risks and adopting best practices, such as using secure payment methods and avoiding suspicious links, can reduce the likelihood of triggering fraud prevention flags. By staying vigilant and maintaining open communication with your bank, you can navigate security holds with confidence and minimize disruptions to your financial life.

Counting Nickels: Understanding the Quantity in a Standard Bank Roll

You may want to see also

Explore related products

![]()

Contact issuing bank directly: Reach out to the bank for specific decline reasons and solutions

A declined transaction can be frustrating, especially when the reason isn't immediately clear. One of the most direct and effective ways to resolve this issue is to contact the issuing bank. This approach allows you to bypass generic error messages and get to the root of the problem. By speaking directly with a representative, you can gain specific insights into why the transaction was declined and what steps you can take to resolve it. This method is particularly useful because it provides personalized solutions tailored to your situation, rather than relying on one-size-fits-all advice.

When reaching out to the bank, it’s essential to prepare beforehand to make the conversation as productive as possible. Start by gathering relevant information, such as the transaction details, the error message received, and any recent changes to your account or financial situation. This preparation ensures that the bank representative can quickly identify the issue. For instance, if the decline was due to insufficient funds, the bank might suggest transferring money from another account or waiting until your next deposit clears. If the issue is related to security concerns, they may guide you through verifying your identity or updating your account settings.

The tone and approach of your conversation can significantly impact the outcome. Be polite and cooperative, as bank representatives are more likely to assist customers who are respectful and patient. Clearly explain the situation and ask specific questions, such as, “Can you tell me the exact reason for the decline?” or “What steps can I take to ensure future transactions go through?” If the decline was due to a suspected fraudulent activity, the bank might require additional documentation or place a temporary hold on your account for security purposes. Understanding these requirements upfront can save time and reduce stress.

One practical tip is to ask the bank representative to note the conversation in your account records. This documentation can be helpful if the issue persists or if you need to escalate the matter later. Additionally, inquire about preventive measures to avoid future declines. For example, if the bank flagged the transaction due to unusual activity, they might recommend setting up transaction alerts or updating your contact information. Some banks also offer pre-authorization services for specific merchants or travel-related expenses, which can prevent declines when you’re abroad or making large purchases.

In conclusion, contacting the issuing bank directly is a proactive and efficient way to address a declined transaction. It provides clarity, personalized solutions, and the opportunity to take preventive measures. By approaching the conversation with preparation, respect, and specific questions, you can resolve the issue swiftly and gain valuable insights into managing your account effectively. This method not only fixes the immediate problem but also empowers you to handle similar situations in the future with confidence.

Bank Payments: Weekend Clearance Explained

You may want to see also

Frequently asked questions

This message indicates that your bank has rejected the transaction. Common reasons include insufficient funds, expired card, incorrect card details, or the bank’s fraud prevention system flagging the transaction as suspicious.

Contact your bank to verify the reason for the decline. Ensure your account has sufficient funds, update expired or incorrect card details, or confirm if the transaction was flagged as fraudulent. Alternatively, try using a different payment method.

Yes, you can retry after addressing the issue (e.g., adding funds or correcting details). However, avoid multiple immediate retries, as this may trigger further security blocks. Wait a few minutes or contact your bank first.

Your card may have been declined due to security measures, such as unusual spending patterns or transactions in unfamiliar locations. Contact your bank to verify if the transaction was blocked for security reasons and request approval if legitimate.