Forming a co-operative bank involves a structured process that emphasizes community-driven financial services and democratic member control. It begins with identifying a group of individuals or organizations with a shared economic or social goal, who then draft a detailed business plan outlining the bank’s mission, services, and operational framework. The next step is to register the co-operative under relevant legal and regulatory frameworks, ensuring compliance with banking laws and obtaining necessary licenses. Members must collectively pool capital through share subscriptions, establishing a solid financial foundation. Governance is critical, requiring the election of a board of directors from among the members to oversee operations and ensure transparency. Additionally, partnerships with regulatory bodies, financial institutions, and technology providers are essential to streamline operations and maintain compliance. By fostering inclusivity, accountability, and member participation, a co-operative bank can effectively serve its community while promoting sustainable economic development.

Explore related products

What You'll Learn

- Legal Requirements: Understand laws, regulations, and compliance needed to establish a co-operative bank

- Membership Structure: Define eligibility, roles, and responsibilities of members in the co-operative

- Capital Formation: Plan share capital, deposits, and funding sources for bank operations

- Governance Framework: Establish board structure, decision-making processes, and member democracy

- Operational Setup: Develop banking services, technology, and infrastructure for smooth functioning

![]()

Legal Requirements: Understand laws, regulations, and compliance needed to establish a co-operative bank

Establishing a co-operative bank is not a task for the faint-hearted. It demands a meticulous understanding of the legal landscape, which varies significantly across jurisdictions. In the United States, for instance, the process is governed by both federal and state laws, with the National Credit Union Administration (NCUA) playing a pivotal role in regulating credit unions, a common form of co-operative bank. In contrast, the European Union’s framework emphasizes member-driven governance under the Cooperative Societies Act, ensuring alignment with regional directives. Before embarking on this venture, it’s crucial to identify the specific legal requirements of your locality, as these will dictate the feasibility and structure of your co-operative bank.

One of the first steps in navigating legal requirements is to determine the type of co-operative bank you intend to form. Will it be a credit union, a rural co-operative bank, or a multi-state co-operative society? Each category comes with its own set of regulations. For example, in India, the Reserve Bank of India (RBI) mandates that co-operative banks adhere to the Banking Regulation Act, 1949, and the RBI Master Directions. These regulations cover aspects such as minimum capital requirements, which typically range from ₹2 crore to ₹20 crore, depending on the bank’s scope and scale. Understanding these classifications and their associated rules is essential to avoid legal pitfalls and ensure compliance from the outset.

Compliance with anti-money laundering (AML) and know your customer (KYC) regulations is another critical aspect of forming a co-operative bank. These measures are designed to prevent financial crimes and protect the integrity of the banking system. In the European Union, for instance, co-operative banks must comply with the Fourth and Fifth Anti-Money Laundering Directives, which require robust customer due diligence and transaction monitoring. Similarly, in the United States, the Bank Secrecy Act (BSA) imposes stringent reporting requirements on financial institutions, including co-operative banks. Implementing these measures not only ensures legal compliance but also builds trust with regulators and customers alike.

Governance and operational transparency are equally important legal considerations. Co-operative banks are unique in that they are owned and operated by their members, which necessitates a clear and democratic governance structure. This includes holding regular general meetings, maintaining accurate records of member contributions, and ensuring that decision-making processes are transparent and inclusive. For example, in Canada, the Canada Cooperatives Act requires co-operatives to maintain a register of members, file annual reports, and adhere to specific voting procedures. Failure to meet these governance standards can result in legal penalties, loss of license, or even dissolution of the co-operative bank.

Finally, it’s imperative to stay abreast of evolving legal and regulatory changes. Financial regulations are dynamic, often influenced by global economic trends, technological advancements, and policy shifts. For instance, the rise of digital banking has prompted regulators worldwide to introduce new rules on cybersecurity and data protection. Co-operative banks must invest in legal counsel or compliance officers who can monitor these changes and ensure ongoing adherence. Proactive compliance not only mitigates legal risks but also positions the co-operative bank as a reliable and forward-thinking institution in the eyes of its members and regulators.

Does Christopher Banks Offer Free Return Shipping? Find Out Here

You may want to see also

Explore related products

![]()

Membership Structure: Define eligibility, roles, and responsibilities of members in the co-operative

A co-operative bank thrives on the collective strength of its members, making a well-defined membership structure its cornerstone. Eligibility criteria should be clear and inclusive, balancing accessibility with the bank's financial stability. Consider factors like residency within a specific geographic area, shared economic interests, or affiliation with a particular community or industry. For instance, a rural co-operative bank might prioritize local farmers and small business owners, while a tech-focused co-op could target professionals in the digital sector. Age restrictions, if any, should be justified by the bank's mission and regulatory requirements, typically setting a minimum age of 18 for full membership rights.

Once eligibility is established, roles within the co-operative must be clearly outlined to ensure active participation and democratic governance. Members typically serve as both customers and owners, holding equal voting rights regardless of their financial contribution. Beyond this fundamental role, members can take on additional responsibilities such as serving on the board of directors, participating in committees, or acting as volunteers for community outreach programs. For example, a member with financial expertise might chair the audit committee, while another with marketing skills could lead promotional efforts. These roles should be rotational to encourage broad engagement and prevent concentration of power.

Responsibilities of members extend beyond financial transactions to include upholding the co-operative’s principles and values. This includes attending annual general meetings, participating in decision-making processes, and contributing to the bank’s capital through share purchases or deposits. Members must also commit to transparency, accountability, and mutual support, fostering a culture of trust and collaboration. Practical tips include providing training sessions on co-operative governance and offering incentives for active participation, such as dividend preferences or reduced service fees for engaged members.

A comparative analysis of successful co-operative banks reveals that those with a tiered membership structure often achieve greater sustainability. For instance, some banks categorize members as regular, premium, or institutional, with each tier having distinct benefits and obligations. Regular members might enjoy basic banking services, while premium members could access higher loan limits or exclusive investment opportunities. Institutional members, such as local businesses or NGOs, might contribute larger capital but also gain voting privileges proportional to their stake. This model ensures diverse participation while aligning incentives with the bank’s growth objectives.

In conclusion, a robust membership structure is the backbone of a co-operative bank, requiring careful consideration of eligibility, roles, and responsibilities. By fostering inclusivity, defining clear roles, and encouraging active participation, the bank can harness the collective power of its members to achieve shared financial and social goals. Practical steps, such as setting transparent criteria, offering diverse engagement opportunities, and implementing tiered structures, can help create a dynamic and resilient co-operative ecosystem.

How Remit2India Transactions Appear in Your Bank Statements Explained

You may want to see also

Explore related products

![]()

Capital Formation: Plan share capital, deposits, and funding sources for bank operations

Capital formation is the cornerstone of any co-operative bank’s sustainability. Without a robust financial foundation, even the most well-intentioned co-operative will struggle to meet its operational needs and fulfill its members’ expectations. Share capital, deposits, and funding sources are the three pillars that must be meticulously planned to ensure liquidity, stability, and growth. Share capital, for instance, represents the initial equity raised from members, who become part-owners of the bank. This equity not only provides a buffer against losses but also signals credibility to regulators and potential depositors. For example, India’s IFFCO-Tokio General Insurance began with a modest share capital of ₹150 crore, which grew exponentially as members and investors recognized its potential. This underscores the importance of setting a realistic yet ambitious share capital target, typically ranging from ₹5 crore to ₹50 crore, depending on the scale and scope of operations.

Deposits are the lifeblood of a co-operative bank’s operations. They provide the liquidity needed to extend loans, invest in securities, and manage day-to-day expenses. Unlike commercial banks, co-operative banks often rely on local communities for deposits, making trust and accessibility critical. A successful strategy involves offering competitive interest rates, flexible deposit schemes, and personalized services tailored to members’ needs. For instance, Germany’s Raiffeisen Banks, pioneers in the co-operative banking model, attracted deposits by offering tiered interest rates based on deposit tenure, with rates up to 1.5% for long-term deposits. However, caution must be exercised to avoid over-reliance on volatile short-term deposits, which can lead to liquidity crises during economic downturns. A balanced deposit portfolio, with at least 40% in long-term deposits, is recommended to ensure stability.

Funding sources beyond share capital and deposits are essential for scaling operations. Co-operative banks can explore partnerships with larger financial institutions, government grants, and international development funds to augment their capital base. For example, the World Bank’s International Development Association (IDA) provides low-interest loans and grants to co-operative banks in developing countries, often with repayment periods of 25–40 years. Additionally, issuing bonds or securing lines of credit from central banks can provide a cushion during cash flow shortages. However, such external funding comes with strings attached, including compliance with stringent regulatory requirements and repayment obligations. A prudent approach is to limit external debt to 30% of total assets, ensuring the bank retains control over its decision-making processes.

A comparative analysis of successful co-operative banks reveals a common thread: diversification of funding sources. Spain’s Mondragon Corporation, the world’s largest worker co-operative, thrives by combining member contributions, retained earnings, and strategic partnerships. Similarly, Canada’s Desjardins Group, a co-operative financial institution, leverages a mix of deposits, government-backed securities, and interbank lending to maintain liquidity. These examples highlight the importance of not putting all eggs in one basket. By diversifying funding sources, co-operative banks can mitigate risks, seize growth opportunities, and remain resilient in the face of economic uncertainties.

In conclusion, capital formation requires a strategic, multi-pronged approach. Start by setting a realistic share capital target, backed by a compelling business plan to attract members. Build a deposit base by offering competitive rates and tailored services, while ensuring a healthy mix of short-term and long-term deposits. Finally, explore external funding options judiciously, balancing growth ambitions with financial stability. By mastering these elements, a co-operative bank can establish a solid financial foundation, enabling it to serve its members effectively and contribute to the broader community’s economic development.

Easy Steps to Add a Beneficiary in Commercial Bank

You may want to see also

Explore related products

![[2 Pack]Small Portable Charger for iPhone 17/16/15 Series,5000mAh 3A PD USB C Power Bank, Mini Travel Essentials Battery Pack for iPhone 17/17 Pro/16/16 Plus/16 Pro/15 Pro Max,Samsung,Android/LG etc](https://m.media-amazon.com/images/I/51Fnx3IgDCL._AC_UL320_.jpg)

![]()

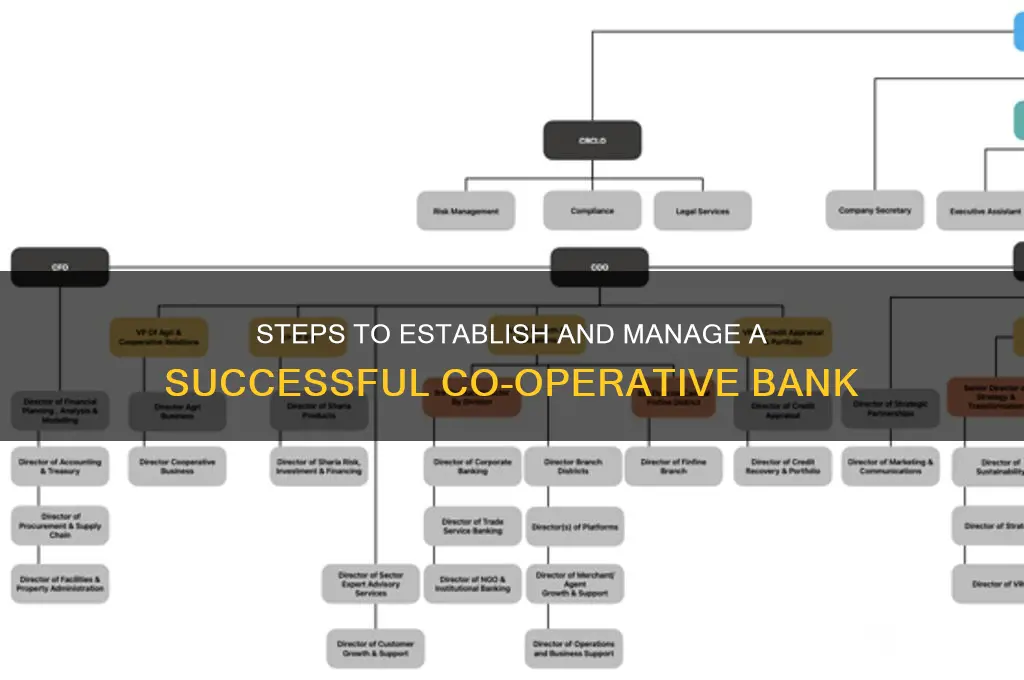

Governance Framework: Establish board structure, decision-making processes, and member democracy

A co-operative bank’s governance framework is its backbone, ensuring stability, transparency, and member-centric decision-making. At its core lies the board structure, which must balance expertise with democratic representation. Typically, a co-operative bank’s board consists of 7–15 members, elected by the membership base. These directors should reflect the diversity of the membership—geographically, professionally, and demographically—to ensure all voices are heard. For instance, a rural co-operative bank might include farmers, local business owners, and community leaders on its board. This structure fosters inclusivity and aligns the bank’s goals with its members’ needs.

Decision-making processes in a co-operative bank must prioritize consensus while maintaining efficiency. Key decisions, such as strategic direction or major investments, should require a two-thirds majority vote from the board, with dissenting opinions documented to encourage transparency. However, day-to-day operations can follow a simpler approval process, delegated to committees or management to avoid bottlenecks. For example, a credit committee might handle loan approvals up to a certain threshold, while larger loans require full board review. This tiered approach ensures accountability without sacrificing agility.

Member democracy is the lifeblood of a co-operative bank, distinguishing it from traditional financial institutions. Members must have a direct say in governance through annual general meetings (AGMs), where they elect board members, approve financial statements, and vote on policy changes. To encourage participation, banks can employ strategies like proxy voting, virtual AGMs, and educational workshops on co-operative principles. For instance, a co-operative bank in Spain increased AGM attendance by 40% by offering a financial literacy session before the meeting. Such initiatives empower members to take ownership of their bank’s future.

A critical caution in governance is avoiding concentration of power. While a strong board chair or CEO can provide leadership, unchecked authority undermines co-operative values. Implementing term limits—typically 2–3 years with a maximum of two consecutive terms—prevents entrenchment and encourages fresh perspectives. Additionally, an independent audit committee, separate from the board, should oversee financial practices to ensure integrity. For example, a co-operative bank in Canada faced a governance crisis when its long-serving chair approved loans to personal associates, highlighting the need for robust checks and balances.

In conclusion, a co-operative bank’s governance framework must be designed with intentionality, balancing structure with flexibility, and authority with democracy. By establishing a diverse board, tiered decision-making processes, and robust member engagement mechanisms, the bank can remain true to its co-operative identity while achieving financial sustainability. Practical steps, such as term limits and independent oversight, safeguard against common pitfalls, ensuring the bank serves its members effectively for generations to come.

Small Banks, Big Shocks: Strategies for Surviving Economic Turmoil

You may want to see also

Explore related products

![]()

Operational Setup: Develop banking services, technology, and infrastructure for smooth functioning

Co-operative banks must prioritize a robust operational setup to ensure seamless service delivery and member satisfaction. This involves a meticulous blend of banking services, cutting-edge technology, and resilient infrastructure. Begin by identifying core services tailored to your members' needs—savings accounts, loans, and payment solutions are foundational. For instance, a rural co-operative bank might focus on microloans for farmers, while an urban one could emphasize digital payment systems. Each service should align with regulatory requirements and member expectations, ensuring compliance and relevance.

Technology is the backbone of modern banking, and co-operative banks cannot afford to lag. Invest in a scalable core banking system that integrates seamlessly with digital platforms. Mobile banking apps, online portals, and automated teller machines (ATMs) are no longer optional—they are essential. For example, a cloud-based core banking solution can reduce upfront costs while offering flexibility for future growth. Additionally, prioritize cybersecurity measures such as encryption, two-factor authentication, and regular audits to protect member data. A single breach can erode trust, so proactive measures are critical.

Infrastructure development goes beyond technology to include physical and human resources. Establish a network of branches and service points strategically located to serve your members effectively. For instance, a co-operative bank in a sprawling rural area might rely on mobile banking units to reach remote members. Simultaneously, invest in training programs to upskill staff, ensuring they can handle both traditional and digital banking tasks. A well-trained workforce not only enhances operational efficiency but also improves member experience through personalized service.

Balancing innovation with sustainability is key. Adopt green banking practices by investing in energy-efficient infrastructure and promoting paperless transactions. For example, solar-powered ATMs or digital receipt systems can reduce environmental impact while cutting costs. Similarly, leverage data analytics to optimize operations—predicting member behavior can help tailor services and allocate resources more efficiently. By integrating sustainability and innovation, co-operative banks can differentiate themselves while contributing to broader societal goals.

Finally, establish a feedback loop to continuously refine your operational setup. Regularly survey members to gauge satisfaction levels and identify pain points. For instance, if members complain about slow transaction processing, consider upgrading your payment gateway or server capacity. Similarly, benchmark your performance against industry standards to identify areas for improvement. A dynamic, member-centric approach ensures that your co-operative bank remains agile and responsive, fostering long-term growth and trust.

Master Bank Fishing: Proven Tips to Catch Saugeye Easily

You may want to see also

Frequently asked questions

A co-operative bank is a financial institution owned and operated by its members, who are typically the customers. Unlike traditional banks, which are owned by shareholders and prioritize profit, co-operative banks focus on serving their members' needs and distributing profits as dividends or reinvesting in the community.

The legal requirements vary by country but generally include registering under the relevant co-operative societies act, obtaining a banking license from the financial regulatory authority, and meeting minimum capital requirements. A detailed business plan and compliance with banking regulations are also essential.

The minimum number of members required to form a co-operative bank varies by jurisdiction. Typically, it ranges from 10 to 50 members. These members must be committed to the co-operative's objectives and willing to invest in its capital.

Capital can be raised through member contributions, issuing shares, or securing loans from other financial institutions. Members typically invest in the bank by purchasing shares, and the bank may also attract deposits from the public once operational.

A co-operative bank must have a democratic governance structure, with members electing a board of directors to oversee operations. Decisions are made based on the principle of "one member, one vote," ensuring equal participation regardless of the size of their investment. Regular general meetings are also mandatory to maintain transparency and accountability.