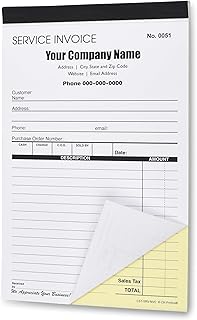

Invoicing international clients can be a complex process, especially when dealing with banks, as it involves navigating different currencies, tax regulations, and payment methods. To ensure smooth transactions, it is essential to understand the specific requirements of both the client's country and your own, including any applicable tax laws, such as VAT or GST, and currency exchange rates. When invoicing international clients at banks, consider using a clear and detailed invoice template that includes all necessary information, such as your business details, client information, invoice number, payment terms, and a breakdown of services or products provided. Additionally, familiarize yourself with the bank's preferred payment methods, such as wire transfers or online payment platforms, and ensure that your invoice complies with their formatting and submission requirements to avoid delays or complications in receiving payments.

| Characteristics | Values |

|---|---|

| Currency | Use the client's local currency to avoid exchange rate fluctuations and additional fees. |

| Payment Methods | Offer multiple options like wire transfers (SWIFT), ACH transfers, credit cards, or online payment platforms (PayPal, TransferWise). |

| Invoice Details | Include your business name, address, contact info, client details, invoice number, date, payment terms, itemized services/products, quantities, rates, taxes (if applicable), and total amount due. |

| Payment Terms | Clearly state due dates, late payment penalties, and accepted payment methods. |

| Tax Considerations | Research and comply with tax regulations in both your country and the client's country. Consider VAT, GST, or other applicable taxes. Consult a tax professional if needed. |

| Invoice Format | Use a professional template, preferably in PDF format, to ensure clarity and avoid formatting issues. |

| Payment Processing Fees | Be aware of bank fees for international transactions and consider who bears the cost (you or the client). |

| Exchange Rate Risk | Consider using forward contracts or other hedging strategies to mitigate currency fluctuations. |

| Communication | Clearly communicate payment instructions and expectations to the client. |

| Record Keeping | Maintain accurate records of invoices, payments, and correspondence for tax and accounting purposes. |

| Compliance | Ensure compliance with anti-money laundering (AML) and know-your-customer (KYC) regulations. |

Explore related products

$57 $60

What You'll Learn

- Currency Selection: Choose the right currency to avoid exchange rate fluctuations and fees

- Payment Methods: Offer options like wire transfers, SWIFT, or online platforms for convenience

- Invoice Details: Include client’s bank details, payment terms, and compliance with local regulations

- Tax Considerations: Understand VAT, GST, or withholding taxes to ensure accurate billing

- Compliance & Documentation: Adhere to international banking rules and provide necessary export/import documents

![]()

Currency Selection: Choose the right currency to avoid exchange rate fluctuations and fees

Selecting the right currency for invoicing international clients is a strategic decision that can significantly impact your bottom line. Exchange rate fluctuations and transaction fees can erode profits if not managed carefully. For instance, invoicing a European client in USD exposes you to euro-dollar volatility, while invoicing in their local currency (EUR) shifts the risk to them. This choice depends on your risk tolerance, the client’s preference, and the stability of the currencies involved.

To minimize risk, consider invoicing in a stable, widely accepted currency like the USD, EUR, or GBP, especially if your client operates in a region with volatile local currency. However, if your client prefers to pay in their local currency, negotiate a clause in the contract that allows for price adjustments based on exchange rate movements beyond a certain threshold. For example, if the rate fluctuates by more than 3%, either party can request a price review. This protects both sides from unexpected losses.

Another practical approach is to use a multi-currency account offered by many international banks. These accounts allow you to hold and invoice in multiple currencies, reducing conversion fees and providing better exchange rates. For instance, platforms like Wise or PayPal offer such accounts, enabling seamless transactions in over 40 currencies. However, be mindful of their fee structures, as some charge for withdrawals or currency conversions.

For long-term contracts, consider using a forward exchange contract to lock in a favorable exchange rate for future transactions. This financial instrument guarantees a specific rate for up to two years, shielding you from market volatility. While it requires a commitment, it provides predictability and reduces financial risk. For example, if you expect the USD to strengthen against the EUR, locking in the current rate can save you money over time.

Finally, always communicate transparently with your client about currency choices and associated costs. Provide clear breakdowns of fees, exchange rates, and payment terms in the invoice to avoid disputes. Tools like currency converters or invoicing software (e.g., Xero, QuickBooks) can help you present this information accurately. By aligning currency selection with both parties’ interests, you build trust and ensure smoother international transactions.

Exploring the GCC's Banking Landscape: A Comprehensive Bank Count

You may want to see also

Explore related products

![]()

Payment Methods: Offer options like wire transfers, SWIFT, or online platforms for convenience

Wire transfers remain a cornerstone for invoicing international clients, prized for their reliability and global acceptance. To execute one, ensure your invoice includes the client’s bank name, SWIFT code, account number, and any intermediary bank details if applicable. Specify the currency to avoid exchange rate discrepancies, and clearly state whether fees are shared or borne by the recipient. While wire transfers can take 1–5 business days, their traceability and security make them ideal for large transactions. Always confirm receipt with the client to prevent payment delays.

SWIFT payments, facilitated by the Society for Worldwide Interbank Financial Telecommunication network, offer a standardized method for cross-border transactions. This system ensures accuracy by using unique bank identifiers (BIC/SWIFT codes) and structured messaging. However, SWIFT payments often incur higher fees due to intermediary banks, and processing times vary. To optimize this method, provide clients with a detailed breakdown of costs and timelines in your invoice. Encourage them to use the SWIFT gpi (global payments innovation) service for faster tracking and transparency.

Online platforms like PayPal, TransferWise (now Wise), and Stripe have revolutionized international invoicing by offering speed, lower fees, and user-friendly interfaces. These platforms typically convert currencies at mid-market rates, saving clients from unfavorable exchange fees. When using such services, include a direct payment link in your invoice and specify the exact amount in the client’s preferred currency. Be mindful of platform limits—for instance, PayPal caps transactions at $10,000 per transfer for unverified accounts. For recurring clients, consider setting up automated invoicing through these platforms to streamline payments.

Choosing the right payment method depends on your client’s preferences, transaction size, and urgency. Wire transfers suit high-value payments, SWIFT ensures structured compliance, and online platforms cater to convenience and speed. Always offer at least two options in your invoice to accommodate diverse needs. Include a brief note explaining the pros and cons of each method, such as: “Wire transfers are secure but slower, while online platforms offer instant payments with lower fees.” This empowers clients to make informed decisions and fosters trust in your invoicing process.

To minimize errors, double-check all payment details before sending the invoice and provide a clear reference number (e.g., “Invoice #12345”) for easy tracking. If using multiple currencies, lock in exchange rates with a forward contract to protect against fluctuations. Finally, follow up with clients after sending the invoice to confirm receipt and answer any questions about payment methods. By offering flexibility and clarity, you’ll ensure timely payments and strengthen international business relationships.

Mergers: Boon or Bane for Banks' Short-Term Profits?

You may want to see also

Explore related products

![]()

Invoice Details: Include client’s bank details, payment terms, and compliance with local regulations

Invoicing international clients requires precision, especially when detailing bank information, payment terms, and regulatory compliance. Start by clearly listing the client’s bank details, including the SWIFT/BIC code, IBAN (if applicable), bank name, and branch address. Omitting any of these can delay payment or result in failed transactions. For instance, a U.S. client paying a UK vendor would need the vendor’s IBAN and SWIFT code to ensure seamless wire transfer. Always verify these details with the client to avoid errors, as international banking systems vary widely.

Payment terms are equally critical and should align with both parties’ expectations. Specify the currency (e.g., USD, EUR, GBP) to avoid exchange rate confusion. Include due dates, late payment penalties, and accepted payment methods (bank transfer, credit card, etc.). For example, offering a 2% discount for payment within 10 days can incentivize prompt settlement. However, be cautious with extended payment terms, as they may strain cash flow. Tailor terms to the client’s country; a 30-day payment window is standard in the U.S., while European clients may expect 60 days.

Compliance with local regulations is non-negotiable and varies by jurisdiction. Research the client’s country-specific invoicing requirements, such as mandatory tax identifiers (e.g., VAT number in the EU) or specific invoice formats. For instance, invoices in Germany must include a unique invoice number and the vendor’s tax number. Failure to comply can lead to legal penalties or payment rejection. Tools like accounting software with international invoicing templates can help ensure adherence to these rules.

Finally, consider the practicalities of cross-border payments. Factor in transaction fees, currency conversion charges, and potential delays when setting payment terms. For instance, wire transfers can take 2–5 business days, while platforms like Wise or PayPal offer faster alternatives but with varying fees. Communicate these details transparently to manage client expectations. By meticulously addressing bank details, payment terms, and regulatory compliance, you streamline the invoicing process and foster trust with international clients.

Activate UCO Bank Net Banking: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Tax Considerations: Understand VAT, GST, or withholding taxes to ensure accurate billing

Navigating the tax landscape is crucial when invoicing international clients, as VAT, GST, and withholding taxes vary significantly across jurisdictions. For instance, the European Union applies a standard VAT rate ranging from 17% to 27%, while Australia imposes a 10% GST on most goods and services. Ignoring these differences can lead to undercharging, overcharging, or non-compliance penalties. Always verify the tax obligations in both your country and the client’s country to ensure accurate billing.

To streamline this process, start by determining whether the service or product is subject to VAT, GST, or withholding tax. For example, digital services often fall under VAT in the EU, while physical goods may incur GST in countries like Canada or India. Use tax lookup tools or consult a tax professional to confirm rates and thresholds. If the client’s country requires you to register for VAT or GST, factor in the administrative burden and potential costs.

Withholding taxes present another layer of complexity, particularly for freelancers or businesses in countries with tax treaties. For instance, the U.S. may withhold up to 30% of payments to non-resident contractors unless a treaty reduces this rate. To mitigate this, provide clients with a completed W-8BEN-E form (for U.S. clients) or equivalent documentation in other countries. Clearly state the applicable tax rate on your invoice to avoid disputes and ensure timely payment.

A practical tip is to use invoicing software that supports international tax rules, such as QuickBooks or Xero, which automatically calculates VAT or GST based on the client’s location. However, always double-check these calculations manually, as software may not account for specific exemptions or thresholds. For instance, small businesses below a certain revenue threshold may be exempt from VAT registration in some countries.

In conclusion, understanding and correctly applying VAT, GST, or withholding taxes is non-negotiable when invoicing international clients. Proactive research, accurate documentation, and the use of appropriate tools can prevent costly errors and foster trust with your clients. Treat tax compliance as an investment in your business’s reputation and long-term success.

Step-by-Step Guide to Activating HDFC Net Banking Easily and Securely

You may want to see also

Explore related products

![]()

Compliance & Documentation: Adhere to international banking rules and provide necessary export/import documents

International transactions demand meticulous adherence to regulatory frameworks, as banks act as gatekeepers for cross-border financial flows. Each country has its own set of rules governing foreign exchange, anti-money laundering (AML), and trade compliance. For instance, the USA’s Office of Foreign Assets Control (OFAC) prohibits transactions with sanctioned entities, while the EU’s General Data Protection Regulation (GDPR) mandates data privacy in invoicing. Ignoring these rules risks transaction delays, penalties, or even account freezes. Banks scrutinize invoices for compliance, often rejecting those lacking critical details like HS codes (Harmonized System) for goods or missing certificates of origin.

To navigate this complexity, start by identifying the regulatory bodies governing your trade corridor. For exports from the UK to India, for example, you’ll need to comply with HM Revenue & Customs (HMRC) rules and India’s Directorate General of Foreign Trade (DGFT) requirements. Common documents include commercial invoices, packing lists, bills of lading, and certificates of origin. For services, a detailed invoice describing the work, currency, and payment terms suffices, but ensure it aligns with the destination country’s tax laws, such as India’s Goods and Services Tax (GST) or the EU’s VAT.

A persuasive argument for thorough documentation is risk mitigation. Incomplete or inaccurate paperwork can trigger audits or customs holds, delaying payments by weeks. For instance, a missing export license for controlled goods (e.g., electronics with encryption) can halt a shipment entirely. To avoid this, use standardized templates provided by banks or trade associations, such as the International Chamber of Commerce (ICC)’s Incoterms 2020, which clarify responsibilities between buyer and seller. Additionally, leverage digital tools like SWIFT’s Trade Finance platform to ensure documents are securely transmitted and compliant with global standards.

Comparatively, domestic invoicing is straightforward, but international invoicing requires a layered approach. While a local invoice might only need a description and amount, an international one must include terms like Incoterms (e.g., EXW, FOB), payment currency (e.g., USD, EUR), and compliance declarations. For instance, a US exporter must declare on the invoice whether the transaction complies with the Export Administration Regulations (EAR). Similarly, an EU exporter must include an EORI (Economic Operators Registration and Identification) number. These details are not optional—they are prerequisites for banks to process payments.

In conclusion, compliance and documentation are the backbone of successful international invoicing. Treat each invoice as a legal document, ensuring it meets the regulatory demands of both your country and the recipient’s. Invest time in understanding specific requirements, such as the need for a Form A (Generalized System of Preferences certificate) for duty-free exports to certain countries. By doing so, you not only ensure smooth transactions but also build trust with banks and clients, positioning your business as a reliable global partner.

Contacting US Bank via Email: A Step-by-Step Guide for Customers

You may want to see also

Frequently asked questions

Use the client’s local currency or a mutually agreed-upon currency (e.g., USD, EUR) to avoid confusion and simplify payment processing. Clearly state the currency on the invoice.

Provide your SWIFT/BIC code, IBAN (if applicable), account number, and bank name. Ensure details are accurate and formatted correctly for international transfers.

Research tax regulations in the client’s country. In many cases, you may not need to charge VAT/GST if the client is outside your tax jurisdiction, but always consult a tax professional.

Clearly specify payment terms (e.g., net 30 days) and preferred payment methods (e.g., wire transfer, PayPal). Consider including late payment penalties to ensure timely payments.