Managing your bank expenses is a crucial step toward achieving financial stability and making informed decisions about your money. By regularly reviewing your bank statements, categorizing transactions, and identifying recurring charges, you can gain a clear understanding of where your money is going. Start by logging into your online banking account or examining your monthly statements to track income, fixed expenses, variable spending, and subscriptions. Highlight areas of unnecessary spending or potential savings, and consider using budgeting tools or apps to streamline the process. This proactive approach not only helps you avoid unnecessary fees but also empowers you to align your spending with your financial goals.

| Characteristics | Values |

|---|---|

| Access Online Banking | Log in to your bank’s website or mobile app using your credentials. |

| Navigate to Transactions | Look for "Transaction History," "Account Activity," or similar sections. |

| Filter by Date Range | Select a specific period (e.g., monthly, quarterly) to analyze expenses. |

| Categorize Expenses | Use built-in categorization tools or manually tag transactions (e.g., groceries, bills). |

| Download Statements | Export transaction data as PDF, CSV, or Excel for detailed analysis. |

| Use Budgeting Tools | Utilize bank-provided budgeting features or third-party apps (e.g., Mint, YNAB). |

| Check for Fees | Review account statements for bank fees (e.g., overdraft, maintenance). |

| Monitor Subscriptions | Identify recurring charges for subscriptions or services. |

| Track Cash Withdrawals | Note ATM withdrawals and cash transactions. |

| Review Pending Transactions | Check for pending or unauthorized charges. |

| Set Alerts | Enable notifications for large transactions or low balances. |

| Compare with Budget | Match expenses against your planned budget to identify overspending. |

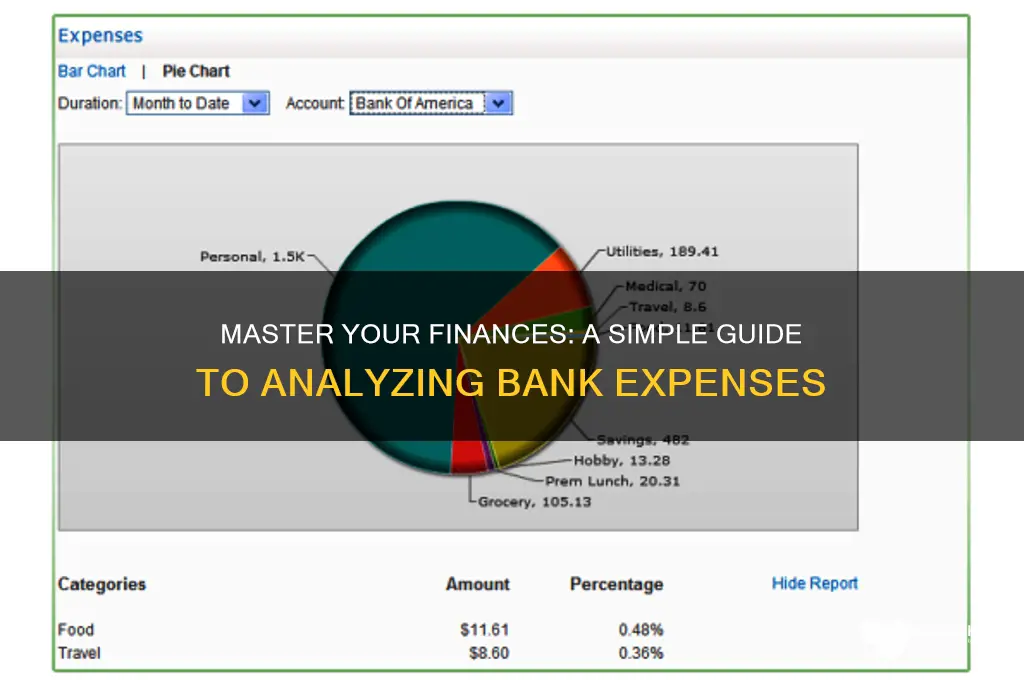

| Analyze Trends | Use charts or graphs (if available) to spot spending patterns. |

| Contact Customer Support | Reach out to your bank for clarification on unfamiliar charges. |

| Secure Your Account | Ensure two-factor authentication is enabled for secure access. |

Explore related products

What You'll Learn

- Track Spending Habits: Categorize transactions to identify patterns and areas for potential savings

- Review Monthly Statements: Scrutinize all charges, fees, and subscriptions for accuracy and relevance

- Analyze Bank Fees: Check for overdraft, ATM, and maintenance fees to minimize unnecessary costs

- Evaluate Subscriptions: Cancel unused or redundant services to reduce recurring expenses

- Compare Account Types: Ensure your bank account aligns with your needs to avoid extra fees

![]()

Track Spending Habits: Categorize transactions to identify patterns and areas for potential savings

Understanding your spending habits begins with categorizing your transactions. Most banks and financial apps allow you to tag expenses as "Groceries," "Dining Out," "Entertainment," or "Utilities." By assigning these labels, you transform a jumble of numbers into a clear picture of where your money goes. For instance, you might notice that 30% of your monthly spending falls under "Dining Out," while only 10% goes to "Groceries." This simple act of categorization reveals patterns that might otherwise remain hidden.

Once categorized, analyze your spending over time to identify trends. Are there months where "Entertainment" spikes? Do "Utilities" consistently rise during certain seasons? For example, if your "Travel" category doubles in the summer, it might reflect vacation expenses. Recognizing these patterns helps you anticipate future costs and adjust your budget accordingly. Tools like spreadsheets or budgeting apps can automate this analysis, making it easier to spot recurring behaviors.

To maximize savings, focus on categories with the highest discretionary spending. Discretionary expenses, like "Dining Out" or "Entertainment," are often areas where cuts can be made without significantly impacting your lifestyle. For instance, if you spend $200 monthly on coffee shops, reducing this to $100 could save $1,200 annually. Compare this to fixed expenses like rent or insurance, which are harder to reduce. Prioritize trimming the categories where your spending is most flexible.

Finally, use your categorized data to set realistic goals. If "Subscriptions" account for 15% of your monthly expenses, consider canceling unused services. Or, if "Groceries" are higher than expected, challenge yourself to meal plan and reduce food waste. The key is to turn insights into actionable steps. By regularly reviewing and adjusting your categories, you’ll not only track spending but also cultivate financial discipline that leads to long-term savings.

Who Sets Interest Rates: Banks or External Factors?

You may want to see also

Explore related products

![]()

Review Monthly Statements: Scrutinize all charges, fees, and subscriptions for accuracy and relevance

Every month, your bank sends a detailed statement summarizing your financial activity. This document is more than just a record; it’s a tool for uncovering hidden costs, unauthorized charges, or unnecessary subscriptions. Start by setting aside 15–20 minutes each month to review it thoroughly. Begin with the transaction list, comparing each entry against your own records or memory. Look for discrepancies, no matter how small—a $2.99 charge you don’t recognize could be a forgotten subscription or a fraudulent transaction.

Next, dissect the fees section. Banks often charge for overdrafts, ATM usage, or account maintenance, and these can add up quickly. For instance, a single overdraft fee can range from $25 to $35, depending on your bank. If you spot recurring fees, investigate whether they’re avoidable. Many banks waive maintenance fees if you maintain a minimum balance or set up direct deposits. Similarly, consider switching to a no-fee account if you’re paying for services you don’t use.

Subscriptions are another area where money often leaks unnoticed. Gym memberships, streaming services, or software subscriptions can cost as little as $5 or as much as $50 monthly. Multiply that by 12, and you’re looking at $60 to $600 annually. Cross-reference each subscription charge with your current usage. If you haven’t watched Netflix in months or haven’t stepped into the gym since January, cancel it immediately. Most services allow cancellation online or via a quick phone call.

Finally, adopt a proactive mindset. Treat your monthly statement review as a financial health check-up. Use it to identify patterns—are you frequently paying overdraft fees? Are there recurring charges for services you no longer need? Addressing these issues not only saves money but also improves your financial discipline. Tools like budgeting apps or spreadsheet templates can help track expenses between statements, making the review process even more effective.

By scrutinizing your monthly statements, you’re not just auditing your bank’s accuracy; you’re taking control of your financial narrative. It’s a small habit with a big payoff, ensuring every dollar is accounted for and every expense justified.

Who Owns Ally Bank? Understanding the Ownership of Ally Bank

You may want to see also

Explore related products

![]()

Analyze Bank Fees: Check for overdraft, ATM, and maintenance fees to minimize unnecessary costs

Bank fees can silently erode your savings, often going unnoticed until they accumulate into a significant financial burden. Overdraft, ATM, and maintenance fees are among the most common culprits, but they’re also the easiest to spot and control. Start by reviewing your monthly statements—most banks provide digital access to transaction histories, making it simple to identify recurring charges. Look for patterns: Are overdraft fees tied to specific spending habits? Do ATM fees spike when you’re traveling or using out-of-network machines? Maintenance fees, often billed monthly, can be particularly insidious because they’re predictable yet often overlooked. By pinpointing these charges, you’ll gain clarity on where your money is going and how to stop the leaks.

To tackle overdraft fees, first understand how they occur. Banks typically charge $35 or more each time your account balance dips below zero, even if the transaction is only a few dollars. A practical strategy is to set up account alerts for low balances or enable automatic transfers from a linked savings account. Some banks also offer overdraft protection plans, but these can come with their own fees, so weigh the costs carefully. If overdrafts are frequent, consider switching to a bank with a more forgiving policy or a no-overdraft-fee account, such as those offered by digital banks like Chime or Ally.

ATM fees are another avoidable expense, often costing $2 to $5 per transaction, depending on whether the machine is out-of-network or international. To minimize these, plan cash withdrawals strategically. Use your bank’s ATM locator app to find fee-free machines, and withdraw larger amounts less frequently to reduce the number of transactions. If you travel often, consider opening an account with a bank that reimburses ATM fees, such as Ally or Schwab. Alternatively, rely on cash-back options at retailers to avoid ATMs altogether.

Maintenance fees, typically ranging from $5 to $15 monthly, are often tied to account requirements like minimum balances or direct deposit thresholds. To eliminate these, review your account terms and adjust your banking habits accordingly. For example, if your account requires a $1,500 minimum balance to waive fees, ensure you maintain that balance or switch to a no-fee account. Many banks also waive maintenance fees for students, seniors, or customers who enroll in paperless statements. If your bank doesn’t offer flexibility, it may be time to explore fee-free alternatives like credit unions or online banks.

The key to minimizing bank fees is proactive management. Set aside time each month to review your statements, question unfamiliar charges, and negotiate with your bank if necessary. Many institutions will waive fees as a one-time courtesy or adjust terms for loyal customers. By staying vigilant and making informed choices, you can reclaim hundreds of dollars annually and redirect them toward savings or other financial goals. Remember, every fee avoided is a step toward greater financial health.

Ethiopia's Banking Oversight: How the Government Regulates Commercial Banks

You may want to see also

Explore related products

![]()

Evaluate Subscriptions: Cancel unused or redundant services to reduce recurring expenses

Subscriptions can silently drain your bank account, often going unnoticed until they accumulate into a significant monthly expense. Many people sign up for services with good intentions—a gym membership for fitness, a streaming platform for entertainment, or a software tool for productivity—only to forget about them as habits change. These recurring charges, though small individually, can add up to hundreds of dollars annually. The first step in reclaiming control is to identify which subscriptions are active on your account. Start by reviewing your bank statements or using budgeting apps that categorize transactions, flagging all recurring payments. Once you’ve compiled a list, ask yourself: *When was the last time I used this service? Does it still align with my current needs or goals?* If the answer is no, it’s time to act.

Canceling unused subscriptions isn’t just about saving money—it’s about aligning your spending with your values and priorities. For instance, if you’re paying $15 monthly for a meditation app you haven’t opened in six months, that’s $180 a year that could be redirected to savings, debt repayment, or a more meaningful expense. To streamline the process, set aside 30 minutes to audit your subscriptions. Visit each service’s website or app, locate the cancellation option (often buried in account settings), and follow the steps. Be cautious of retention offers—companies may tempt you with discounts or free trials, but resist unless the service genuinely adds value. If you’re unsure, consider setting a calendar reminder to reassess in 30 days.

A common pitfall is underestimating the psychological barriers to cancellation. Some services make it deliberately difficult to unsubscribe, requiring phone calls or multiple clicks to deter you. Others rely on inertia, banking on your reluctance to spend time canceling. To counter this, treat subscription cancellation as a task with tangible rewards. For example, calculate how much you’ll save annually by canceling a $10 monthly service and label that amount as “extra savings” in your budget. This reframing turns a chore into a financial win, making it easier to follow through. Additionally, use tools like virtual credit cards or privacy-focused email addresses when signing up for trials to avoid unwanted renewals.

Comparing the cost of subscriptions to their actual usage reveals a stark contrast in value. For example, a $20 monthly gym membership equates to $240 annually, but if you only visit twice a month, you’re paying $10 per session—a rate that could be matched or beaten by pay-per-visit options. Similarly, bundling services can sometimes save money, but only if you use all the included features. A streaming bundle might offer three platforms for $25, but if you only watch one, you’re overpaying. The takeaway? Be ruthless in evaluating whether each subscription earns its keep. If not, cancel it without guilt—your bank account will thank you.

Step-by-Step Guide to Activating Your SBI Internet Banking Account

You may want to see also

Explore related products

![]()

Compare Account Types: Ensure your bank account aligns with your needs to avoid extra fees

Bank accounts are not one-size-fits-all. A checking account designed for frequent transactions might charge fees for low balances, while a savings account optimized for growth could penalize you for withdrawals. Understanding these differences is the first step to avoiding unnecessary expenses. For instance, a student with minimal funds might benefit from a no-fee student account, whereas a small business owner could save by choosing a business account with waived fees for high transaction volumes.

To compare effectively, list your banking habits: monthly transactions, average balance, ATM usage, and direct deposit frequency. Then, scrutinize account features against your needs. Does the account require a minimum balance to waive fees? Are there limits on free transactions? For example, if you use out-of-network ATMs twice a month and your account charges $3 per use, switching to an account with a larger ATM network or fee reimbursements could save you $72 annually.

Consider the hidden costs of misalignment. A savings account with a monthly fee of $10 and a 0.01% APY might seem insignificant, but if you maintain a $5,000 balance, the annual fee ($120) dwarfs the $5 in interest earned. Conversely, a high-yield savings account with no fees and a 4% APY would earn you $200 annually on the same balance. The takeaway? Aligning your account type with your financial behavior maximizes savings and minimizes fees.

Finally, don’t overlook the power of negotiation. If your current account no longer suits your needs but you value your banking relationship, contact your institution. Many banks will waive fees or upgrade your account type to retain customers. For instance, a customer with a long history of on-time payments might secure a fee waiver on a premium account, effectively upgrading their benefits without changing banks. Proactive comparison and communication are your best tools for optimizing bank expenses.

Understanding Bank Charge Disputes: A Step-by-Step Guide for Consumers

You may want to see also

Frequently asked questions

Log in to your online banking account through your bank's website or mobile app. Navigate to the "Transactions" or "Account Activity" section to view a detailed list of your expenses.

Check for unauthorized transactions, recurring subscriptions, overdraft fees, ATM charges, and any other unusual or unexpected expenses. Ensure all charges are accurate and justified.

It’s best to review your bank expenses weekly or monthly to catch errors, fraudulent activity, or unnecessary spending early and maintain better financial control.

Yes, many banking apps and budgeting tools allow you to categorize expenses (e.g., groceries, utilities, entertainment). This helps you understand spending patterns and manage your budget effectively.