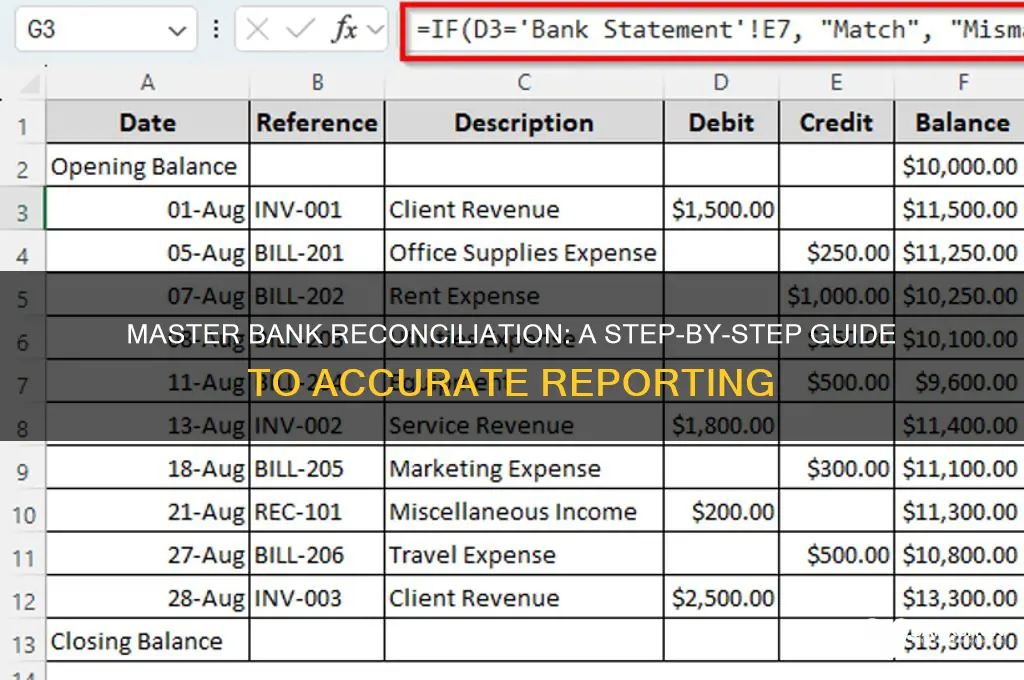

A bank reconciliation report is a critical financial tool used to ensure that a company’s internal records align with its bank statement, identifying discrepancies such as unrecorded transactions, errors, or fraud. To create this report, start by gathering the company’s general ledger and the latest bank statement for the same period. Compare the ending balance of the bank statement with the company’s cash account balance, noting any differences. Next, account for outstanding checks, deposits in transit, bank fees, and interest income that may affect the balance. Adjust both the bank statement and the company’s records to reflect these items, ensuring both balances match. Finally, document all adjustments and discrepancies in a formal reconciliation report, providing a clear audit trail and maintaining accurate financial records. This process not only ensures financial integrity but also helps in detecting and resolving issues promptly.

| Characteristics | Values |

|---|---|

| Purpose | To ensure accuracy between a company's financial records and bank statements. |

| Frequency | Monthly, quarterly, or annually, depending on business needs. |

| Key Components | Bank statement balance, company's book balance, reconciling items. |

| Steps | 1. Gather bank statement and company records. 2. Compare transactions. 3. Identify discrepancies. 4. Adjust for outstanding items. 5. Finalize and document. |

| Outstanding Items | Uncleared checks, unrecorded deposits, bank fees, interest income. |

| Tools | Accounting software (e.g., QuickBooks, Xero), Excel, or manual templates. |

| Documentation | Reconciliation report, adjusted journal entries, supporting documents. |

| Review and Approval | Reviewed by a supervisor or auditor for accuracy and completeness. |

| Common Discrepancies | Timing differences, errors in recording, bank errors, fraud. |

| Best Practices | Regularly reconcile, double-check entries, maintain detailed records. |

| Compliance | Adhere to accounting standards (e.g., GAAP, IFRS) and internal policies. |

| Automation | Use software to streamline the process and reduce errors. |

| Reporting Format | Structured table or spreadsheet with columns for date, description, and amounts. |

| Outcome | Accurate financial statements and identification of potential issues. |

Explore related products

$4.99 $19.99

What You'll Learn

- Gather Bank Statements: Collect all relevant bank statements for the period being reconciled

- Match Transactions: Compare bank statement entries with internal accounting records for accuracy

- Identify Discrepancies: Highlight unmatched or missing transactions for further investigation

- Adjust Entries: Record necessary corrections or missing items in the accounting system

- Finalize Report: Summarize reconciled balances and discrepancies in a formal report

![]()

Gather Bank Statements: Collect all relevant bank statements for the period being reconciled

The foundation of any bank reconciliation report lies in the accuracy and completeness of the source data. Gathering all relevant bank statements for the period being reconciled is the critical first step, as it ensures that every transaction is accounted for and discrepancies can be identified. Start by identifying the exact date range for the reconciliation period, typically a month or a quarter, and ensure that all statements—whether physical or digital—are collected without omission. Missing even a single statement can lead to errors that cascade through the entire reconciliation process, undermining the report's reliability.

In practice, this step requires meticulous organization. For businesses with multiple accounts—operating, savings, or specialized accounts—each statement must be retrieved and labeled clearly to avoid confusion. Digital statements should be downloaded in a consistent format (PDF or CSV) and stored in a dedicated folder for easy access. If physical statements are used, scan them for digital backup and file the originals systematically. A practical tip is to create a checklist of all accounts and tick them off as statements are collected, ensuring nothing is overlooked.

While gathering statements, be mindful of timing. Some banks may take several days to generate end-of-month statements, so plan ahead to avoid delays. Additionally, verify that the statements cover the entire period without gaps. For instance, if reconciling January, ensure the statement includes transactions from January 1 to January 31, inclusive. Partial statements or overlapping periods can introduce errors, such as double-counting or missing transactions, which complicate the reconciliation process.

A comparative approach highlights the importance of this step across different organizational sizes. For small businesses, the process might involve just a few accounts, making it relatively straightforward. However, for larger corporations with dozens of accounts across multiple banks and currencies, the complexity increases exponentially. In such cases, leveraging accounting software or ERP systems to automate statement collection can save time and reduce human error. Regardless of scale, the principle remains the same: completeness and accuracy in statement collection are non-negotiable.

Finally, consider the analytical value of this step beyond reconciliation. Collected statements provide a snapshot of cash flow, transaction patterns, and financial health. By reviewing them during the gathering phase, you may identify anomalies—such as unexpected fees or unauthorized transactions—that warrant further investigation. This proactive approach not only strengthens the reconciliation process but also enhances overall financial management. In essence, gathering bank statements is not just a procedural step but a strategic opportunity to ensure financial integrity.

Paying by Bank Draft: A Step-by-Step Guide for Easy Transactions

You may want to see also

Explore related products

![]()

Match Transactions: Compare bank statement entries with internal accounting records for accuracy

The foundation of any bank reconciliation report lies in meticulously matching transactions between your bank statement and internal accounting records. This process ensures accuracy, identifies discrepancies, and safeguards your financial health. Think of it as a financial detective work, where every entry is a clue to be verified and reconciled.

A systematic approach is crucial. Start by organizing both sets of records chronologically, ensuring dates align for easy comparison. Utilize accounting software that allows for side-by-side viewing and automated matching where possible. This streamlines the process and minimizes human error.

Begin by identifying obvious matches – identical amounts and descriptions. These are your low-hanging fruit, quickly reconciling large portions of your records. However, don't be lulled into complacency. Even seemingly straightforward matches deserve scrutiny. Double-check dates, payee names, and transaction types to ensure they truly correspond.

A more nuanced approach is required for partial matches. These occur when amounts are similar but not identical, or descriptions vary slightly. Investigate these discrepancies diligently. Could it be a rounding difference, a fee deduction, or a typo? Contact vendors or review supporting documentation to clarify the discrepancy and determine the correct entry.

Unmatched transactions demand the most attention. These could indicate errors in recording, missed entries, or even fraudulent activity. Scrutinize these entries carefully, cross-referencing with invoices, receipts, and other supporting documents. If the source of the discrepancy remains unclear, contact your bank for clarification. Remember, every unmatched transaction represents a potential hole in your financial picture, so thorough investigation is paramount.

How to Deposit a Postal Order: A Step-by-Step Banking Guide

You may want to see also

Explore related products

![]()

Identify Discrepancies: Highlight unmatched or missing transactions for further investigation

Unmatched or missing transactions are the red flags of bank reconciliation, signaling potential errors, oversights, or even fraud. These discrepancies arise when the bank statement and internal records don’t align, requiring meticulous scrutiny to ensure financial accuracy. Identifying them is not just a procedural step—it’s a critical safeguard for maintaining trust in your financial data.

Begin by cross-referencing every transaction on the bank statement with your internal ledger. Use accounting software to automate this process, but don’t rely solely on technology; manual spot-checks are essential for catching anomalies. For instance, a $5,000 deposit recorded in your books but absent on the bank statement could indicate a processing delay or a misposted entry. Highlight these inconsistencies in a separate column or spreadsheet, categorizing them as "unmatched" or "missing" for clarity.

Next, investigate the root cause of each discrepancy. Common culprits include timing differences (e.g., checks issued but not yet cashed), bank fees or interest not recorded internally, or data entry errors. For example, a $200 bank fee might be missing from your records if it wasn’t automatically imported into your accounting system. Cross-check dates, amounts, and descriptions to pinpoint the issue. If a transaction remains unexplained after initial review, flag it for deeper analysis, such as verifying source documents or contacting the bank.

To streamline this process, establish a systematic approach. Prioritize discrepancies by dollar amount, starting with the largest variances. Use color-coding or conditional formatting in spreadsheets to visually distinguish unresolved items. For recurring issues, such as frequent timing differences, consider adjusting your reconciliation frequency or improving communication with the bank. Documentation is key—maintain detailed notes on each investigation to track progress and inform future reconciliations.

Finally, treat discrepancies as opportunities to strengthen your financial controls. Persistent unmatched transactions may indicate systemic issues, such as inadequate training or flawed workflows. Implement corrective measures, such as double-entry verification for high-value transactions or regular audits of bank feeds. By addressing discrepancies proactively, you not only ensure accurate reporting but also build resilience against future errors or discrepancies.

Mastering Marg: Step-by-Step Guide to Creating a Bank Ledger

You may want to see also

Explore related products

![]()

Adjust Entries: Record necessary corrections or missing items in the accounting system

Recording necessary corrections or missing items in the accounting system is a critical step in ensuring the accuracy of your bank reconciliation report. Discrepancies between your internal records and bank statements often stem from timing differences, errors, or omitted transactions. Adjusting entries bridges this gap, aligning your books with the bank’s data. For instance, if a vendor payment was recorded internally but not yet cleared by the bank, an adjusting entry ensures the expense is recognized in the correct period. This process demands precision, as even minor oversights can distort financial statements and mislead decision-making.

To execute adjusting entries effectively, follow a structured approach. Begin by identifying the nature of the discrepancy—is it an outstanding deposit, uncleared check, or bank fee not recorded in your system? Once identified, classify the adjustment as a debit or credit to the appropriate account. For example, an unrecorded bank service charge requires a debit to "Bank Fees" and a credit to "Cash." Use supporting documentation, such as invoices or bank notices, to substantiate the entry. Consistency is key; ensure the adjustment adheres to your accounting framework (e.g., accrual or cash basis) and is documented in a clear, auditable manner.

While adjusting entries are essential, they are not without risks. Over-reliance on manual adjustments can mask systemic issues, such as recurring data entry errors or flawed processes. To mitigate this, investigate the root cause of discrepancies. For instance, if uncleared checks frequently appear, consider implementing a more robust check-tracking system. Additionally, avoid backdating entries to prior periods unless absolutely necessary, as this can complicate audits and distort period-specific performance metrics. Regularly review and reconcile accounts to minimize the volume of adjustments needed.

A comparative analysis of manual versus automated adjustments highlights efficiency gains. Manual entries, while flexible, are time-consuming and prone to human error. Automated systems, integrated with banking software, can flag discrepancies in real-time and suggest corrective entries. For small businesses, tools like QuickBooks or Xero streamline this process, reducing the likelihood of oversight. However, automation is not foolproof; periodic manual reviews remain essential to catch anomalies that algorithms might miss. The ideal approach blends automation with human oversight, balancing speed and accuracy.

In conclusion, adjusting entries are the linchpin of an accurate bank reconciliation report. They require meticulous attention to detail, a structured process, and a proactive mindset to address underlying issues. By mastering this step, you not only ensure financial statements reflect reality but also strengthen the integrity of your accounting system. Whether manual or automated, the goal remains the same: to reconcile discrepancies transparently and efficiently, fostering trust in your financial data.

Understanding Cash Bundles: Bank Procedures and Security Measures Explained

You may want to see also

Explore related products

![]()

Finalize Report: Summarize reconciled balances and discrepancies in a formal report

The final step in the bank reconciliation process is arguably the most critical: presenting your findings in a clear, concise, and professional report. This document serves as the ultimate proof of your work, highlighting the accuracy (or discrepancies) between your internal records and the bank's statement. Think of it as the polished narrative that translates raw data into actionable insights for stakeholders.

A well-structured report begins with a summary section, a concise snapshot of the reconciliation's outcome. Here, you'll present the reconciled bank balance, clearly stating the final figure after adjustments for outstanding deposits, uncleared checks, and any identified errors. This figure should match the adjusted bank statement balance, providing a clear indication of financial accuracy.

Next, delve into the discrepancies. Don't simply list them; categorize them for clarity. Were they timing differences, like deposits in transit or outstanding checks? Were there errors in recording transactions, such as incorrect amounts or duplicate entries? Perhaps there were bank fees or interest charges not reflected in your records. Each category should be accompanied by a brief explanation and the corresponding monetary impact.

Quantifying the discrepancies is crucial. Highlight the total variance between your initial records and the reconciled balance. This figure serves as a key performance indicator, revealing the effectiveness of your internal controls and the accuracy of your bookkeeping practices.

Remember, the goal is transparency and accountability. Your report should be easily understandable by individuals with varying levels of financial expertise. Use clear language, avoid jargon, and consider including visual aids like tables or charts to illustrate the reconciliation process and highlight key findings. By presenting a comprehensive and well-organized report, you not only demonstrate your diligence but also provide valuable insights for improving financial management practices.

Securely Access Your Metro Bank Account: A Step-by-Step Login Guide

You may want to see also

Frequently asked questions

A bank reconciliation report is a document that compares a company's internal financial records with the bank statement to identify discrepancies, ensure accuracy, and detect errors or fraud. It is important for maintaining financial integrity, tracking cash flow, and ensuring compliance with accounting standards.

The key steps include: 1) Gather the company’s internal records and the bank statement for the same period, 2) Compare the ending balances, 3) Identify and adjust for outstanding checks, deposits in transit, and bank fees, 4) Account for any errors or discrepancies, and 5) Ensure both records match after adjustments.

It is best practice to prepare a bank reconciliation report monthly, coinciding with the end of each bank statement period. This ensures timely detection of discrepancies and maintains up-to-date financial records.

Common discrepancies include outstanding checks or deposits, bank service charges, interest income, NSF (non-sufficient funds) checks, and errors in recording transactions (e.g., incorrect amounts or duplicate entries).

Many accounting software programs, such as QuickBooks, Xero, or SAP, offer built-in bank reconciliation features that automate the process. Spreadsheets (e.g., Excel) can also be used manually for smaller businesses or simpler reconciliations.