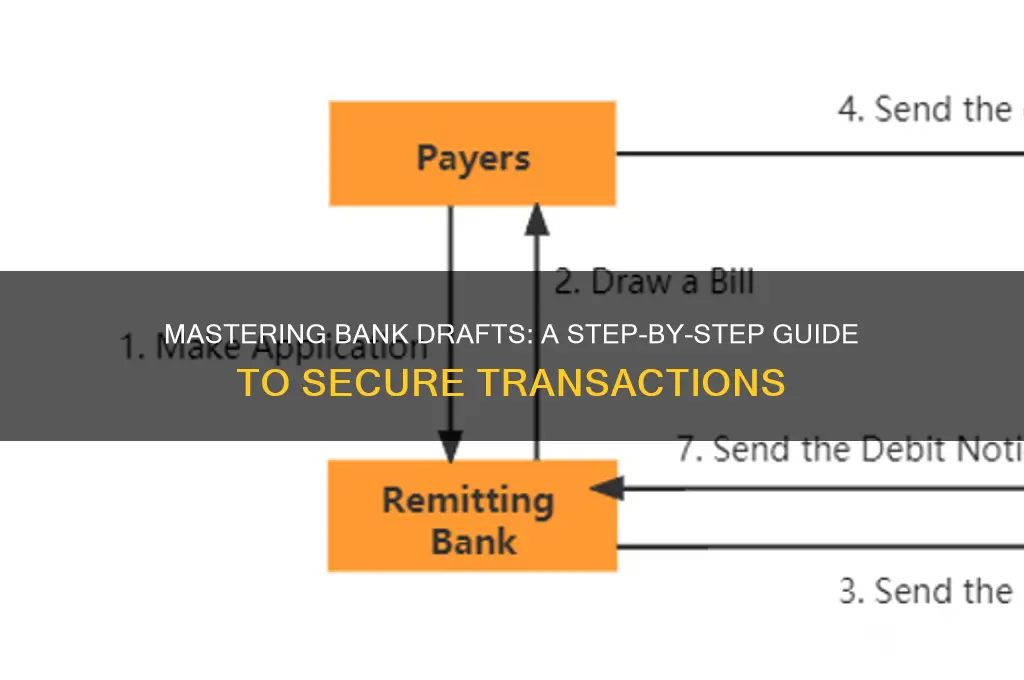

Making a draft in a bank, also known as a bank draft or demand draft, is a secure and reliable method of transferring funds, often used for transactions where a high level of trust and assurance is required. Essentially, a bank draft is a prepaid instrument issued by a bank, guaranteeing payment to the recipient, as the funds are withdrawn from the payer's account at the time of issuance. This process involves the payer instructing their bank to create the draft, which is then drawn on the bank's own account, ensuring the recipient receives cleared funds. Understanding how to make a bank draft is crucial for individuals and businesses engaging in significant financial transactions, such as purchasing property, paying fees, or conducting international trade, where the assurance of payment is paramount.

Explore related products

What You'll Learn

- Understanding Draft Types: Learn about demand, time, and sight drafts for different banking needs

- Draft Application Process: Steps to apply for a draft at your bank branch or online

- Required Documents: Essential documents needed for draft issuance, including ID and account details

- Fees and Charges: Understand bank fees, service charges, and currency conversion costs for drafts

- Draft Security Features: Key security elements like watermarks, signatures, and unique codes to prevent fraud

![]()

Understanding Draft Types: Learn about demand, time, and sight drafts for different banking needs

Bank drafts are essential financial instruments used to facilitate secure and efficient transactions, particularly in international trade and high-value payments. Understanding the different types of drafts—demand, time, and sight—is crucial for selecting the right tool for your banking needs. Each type serves a distinct purpose, offering varying levels of flexibility, security, and control over the payment process.

Demand drafts, as the name suggests, are payable immediately upon presentation. This type of draft is akin to a check but is drawn by a bank on another bank or branch. It guarantees payment because the amount is prepaid by the purchaser, ensuring funds are available. For instance, if you need to pay university fees abroad, a demand draft provides a secure and widely accepted method. The recipient can encash it instantly, making it ideal for time-sensitive transactions. However, its immediacy also means less control over when the payment is processed, so it’s best used when urgency outweighs the need for delayed payment.

In contrast, time drafts introduce a delay, as they are payable at a specific future date. This draft functions like a post-dated check, allowing the payer to manage cash flow more effectively. For example, a business importing goods might use a time draft to align payment with the arrival and sale of the inventory. The recipient, however, must wait until the maturity date to receive funds, which could be a drawback if immediate liquidity is required. Time drafts are particularly useful in trade finance, where both parties benefit from structured payment timelines.

Sight drafts occupy a middle ground, as they are payable on demand but typically used in international trade. Unlike demand drafts, sight drafts are not prepaid; instead, they rely on the creditworthiness of the parties involved. For instance, in a letter of credit transaction, the exporter presents the sight draft along with shipping documents to the importer’s bank, which then honors the payment. This draft type balances immediacy with the assurance of a bank’s involvement, reducing risk for both parties. However, it requires meticulous documentation and adherence to trade terms, such as those outlined in Incoterms.

Choosing the right draft type depends on your specific banking needs. If you prioritize speed and certainty, a demand draft is optimal. For transactions requiring delayed payment, a time draft offers flexibility. Sight drafts, meanwhile, are best suited for international trade, where bank involvement adds a layer of security. Understanding these distinctions ensures you leverage the appropriate instrument, whether for personal or business purposes. Always consult your bank to clarify fees, processing times, and any regulatory requirements associated with each draft type.

Cancel NEFT Transaction in Kotak Bank: Step-by-Step Guide

You may want to see also

Explore related products

![]()

Draft Application Process: Steps to apply for a draft at your bank branch or online

Applying for a bank draft is a straightforward process, whether you choose to visit your bank branch or utilize online banking services. Here's a step-by-step guide to ensure a seamless experience.

Initiating the Process: In-Branch vs. Online

Start by deciding your preferred method. Visiting a bank branch offers personalized assistance, ideal for those seeking guidance or having complex requirements. Simply approach the customer service desk and express your intent to apply for a draft. Alternatively, online banking provides convenience and speed. Log in to your account, navigate to the 'Payments' or 'Transfers' section, and look for the 'Demand Draft' or 'Bank Draft' option. This digital approach is efficient, often allowing you to complete the process within minutes.

Required Information and Documentation

Regardless of the application method, having the necessary details at hand is crucial. You'll need to provide the payee's name, the amount, and the purpose of the draft. Ensure the payee's name is accurate, as any discrepancies may lead to complications. Additionally, have your account number and sufficient funds to cover the draft amount, including any applicable fees. For in-branch applications, carry valid identification and, in some cases, proof of address. Online applications may require you to input these details digitally, so have scanned copies or clear photos ready.

Step-by-Step Application

- In-Branch: Fill out the draft application form provided by the bank representative. Double-check the details for accuracy. Submit the form along with your identification and any other required documents. The bank will process your request, and you'll receive the draft, typically within a few minutes to an hour, depending on the bank's procedures.

- Online: Select the draft option in your online banking portal. Input the payee's details, amount, and purpose. Review the information carefully, as errors may result in delays or additional charges. Confirm the transaction, and the bank will generate a unique draft number. You can then choose to collect the physical draft from your branch or have it mailed to your registered address.

Post-Application Considerations

After submitting your application, keep the receipt or transaction reference number for future reference. If you opt for a physical draft, ensure secure storage and handle it with care, as it is a negotiable instrument. For online applications, note the draft number and expected delivery time. In case of any discrepancies or issues, promptly contact your bank's customer support for assistance. Remember, each bank may have slight variations in their processes, so familiarizing yourself with your bank's specific guidelines is always beneficial.

By following these steps, you can efficiently navigate the draft application process, ensuring a smooth transaction for your financial needs. Whether you prefer the traditional in-branch approach or the convenience of online banking, understanding these procedures empowers you to make informed choices.

Contacting Zenith Bank Customer Care: A Quick and Easy Guide

You may want to see also

Explore related products

![]()

Required Documents: Essential documents needed for draft issuance, including ID and account details

To initiate the process of obtaining a bank draft, one must first understand the critical role that documentation plays. The required documents serve as the foundation for a secure and legitimate transaction, ensuring that both the bank and the customer are protected. Among the essential documents needed for draft issuance, a valid government-issued identification (ID) is paramount. This could include a passport, driver's license, or national ID card, depending on the country's regulations. The ID must be current and clearly display the customer's photograph and personal details, leaving no room for ambiguity.

In addition to identification, account details are a crucial component of the documentation process. Customers must provide accurate information about the account from which the funds will be withdrawn, including the account number, type (e.g., savings, checking), and the name of the account holder. For added security, some banks may require a recent bank statement or a voided check to verify the account's authenticity. It is essential to ensure that the account has sufficient funds to cover the draft amount, as well as any associated fees, to avoid delays or rejections.

A comparative analysis of document requirements across different banks reveals varying degrees of stringency. While some institutions may accept digital copies of IDs and account statements, others insist on physical, original documents. Furthermore, international transactions often necessitate additional documentation, such as proof of address or a notarized affidavit, to comply with cross-border regulations. Customers should familiarize themselves with their bank's specific requirements to streamline the draft issuance process and minimize the risk of errors or omissions.

From a practical standpoint, it is advisable to gather all necessary documents before visiting the bank to save time and prevent multiple trips. A helpful tip is to create a checklist of required items, including ID, account details, and any supplementary documents. For individuals aged 18 and above, the process is relatively straightforward, but minors or individuals with joint accounts may need to provide additional documentation, such as parental consent or co-account holder authorization. By being prepared and organized, customers can ensure a smooth and efficient draft issuance experience.

In conclusion, the essential documents needed for draft issuance are not merely bureaucratic formalities but vital components of a secure financial transaction. By understanding the specific requirements and being diligent in providing accurate information, customers can navigate the process with confidence. As a final takeaway, it is worth noting that some banks offer online draft issuance services, which may have different documentation requirements. Customers should verify these details with their bank to determine the most suitable method for their needs, taking into account factors such as convenience, security, and processing time.

Linking Your Bank Account to Blockchain: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Fees and Charges: Understand bank fees, service charges, and currency conversion costs for drafts

Bank drafts, while secure and widely accepted, aren’t free. Issuance fees are standard, typically ranging from $10 to $50 per draft, depending on the bank and draft type (domestic vs. international). Some banks waive this fee for premium account holders or those meeting minimum balance requirements. Always inquire about fee structures before initiating the process, as costs can vary significantly between institutions.

Beyond the issuance fee, service charges may apply for additional services like expedited delivery or draft cancellation. For instance, overnight courier delivery can add $20–$30, while canceling a draft after issuance might incur a penalty of up to 50% of the draft value. These charges are often non-negotiable, so factor them into your decision-making.

Currency conversion costs are a hidden pitfall for international drafts. Banks typically apply a markup of 2–5% on the exchange rate, which can erode the draft’s value. For example, a $1,000 draft converted from USD to EUR with a 3% markup would result in the recipient receiving €970 instead of €1,000. To minimize losses, compare exchange rates across banks or consider using a specialized currency exchange service for larger amounts.

A practical tip: If you frequently issue drafts, negotiate a flat fee or discounted rate with your bank. Some institutions offer tiered pricing for bulk transactions or loyalty programs that reduce costs over time. Additionally, ask for a detailed fee breakdown before finalizing the draft to avoid surprises. Understanding these fees upfront ensures you’re not overpaying for a service that should streamline, not complicate, your transactions.

How Cybercriminals Use Viruses to Steal Your Banking Information

You may want to see also

Explore related products

![]()

Draft Security Features: Key security elements like watermarks, signatures, and unique codes to prevent fraud

Bank drafts, while less common in the digital age, remain a trusted financial instrument for secure transactions. Their physical nature, however, makes them susceptible to fraud. To combat this, drafts incorporate sophisticated security features that act as a multi-layered defense against counterfeiting and tampering.

Let's dissect these key elements: watermarks, signatures, and unique codes.

Watermarks: The Invisible Shield

Imagine holding a draft up to the light. A genuine watermark, a subtle design embedded within the paper itself, should be visible. This isn't a simple printed image; it's a complex pattern created during the paper manufacturing process. Counterfeiters struggle to replicate this level of intricacy, making watermarks a powerful deterrent. Look for watermarks featuring the issuing bank's logo, denomination, or other security symbols.

Multi-tonal watermarks, visible from both sides of the draft, further enhance security.

Signatures: The Human Touch in a Digital World A legitimate bank draft bears the authorized signatures of bank officials. These signatures, often accompanied by titles and designations, are not mere formalities. They represent a personal guarantee of the draft's authenticity. Banks employ rigorous signature verification processes, ensuring that only authorized individuals can sign drafts. For added security, some drafts incorporate raised or embossed signatures, making them difficult to forge.

Unique Codes: The Digital Fingerprint Think of unique codes as a draft's DNA. These alphanumeric sequences, often printed in both visible and invisible ink, are virtually impossible to replicate. Invisible ink codes, revealed under ultraviolet light, add an extra layer of protection. These codes are linked to a central database, allowing banks to instantly verify a draft's legitimacy. Some drafts even incorporate microprinting, where tiny text is embedded within the code, further complicating counterfeiting attempts.

The Symphony of Security Watermarks, signatures, and unique codes don't operate in isolation. Their combined effect creates a symphony of security, making bank drafts incredibly difficult to forge. Each feature complements the others, forming a robust defense against fraud. When handling a draft, scrutinize these elements carefully. A missing watermark, a suspicious signature, or an inconsistent code should raise red flags. Remember, these security features are your allies in ensuring the integrity of your financial transactions.

Does Simple Bank Charge ATM Fees? A Comprehensive Guide

You may want to see also

Frequently asked questions

A bank draft is a secure payment method where a bank guarantees payment on behalf of the payer. It is used for large transactions, international payments, or when a more reliable alternative to personal checks is needed.

Visit your bank branch, provide the recipient’s details, the amount, and pay the draft value plus any fees. The bank will issue the draft, which you can then send to the recipient.

Yes, banks typically charge a fee for issuing a draft. The fee varies by bank and the draft amount, so check with your bank for specific charges.

Bank drafts are usually cleared within 1-2 business days, as the funds are guaranteed by the bank. However, international drafts may take longer depending on the recipient’s bank processing time.