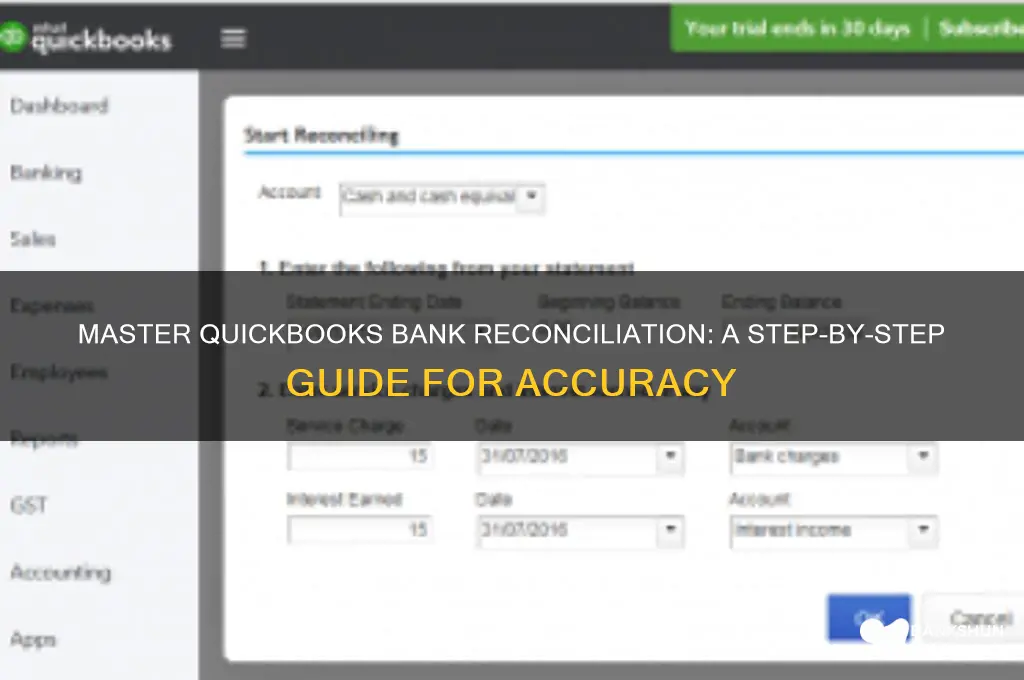

Bank reconciliation in QuickBooks is a critical process for ensuring the accuracy of your financial records by comparing your QuickBooks transactions with your bank statements. It helps identify discrepancies, such as missing or uncleared transactions, and ensures that your books reflect the true financial position of your business. To perform a bank reconciliation in QuickBooks, start by accessing the Banking menu and selecting Reconcile. Enter the ending balance and date from your bank statement, then match transactions in QuickBooks to those on the statement. Unmatched or uncleared items should be reviewed and adjusted as needed. Completing this process regularly not only maintains financial integrity but also aids in detecting errors or fraudulent activities early on.

| Characteristics | Values |

|---|---|

| Purpose | To match QuickBooks transactions with bank statements for accuracy. |

| Prerequisites | Updated bank statement, active QuickBooks account, and reconciled period. |

| Steps | 1. Go to Banking > Reconcile. 2. Select the account to reconcile. 3. Enter the Ending Date and Ending Balance from the bank statement. 4. Mark transactions in QuickBooks that match the bank statement. 5. Click Reconcile Now once balances match. |

| Matching Transactions | Compare dates, amounts, and descriptions between QuickBooks and the bank statement. |

| Adjustments | Make adjustments for uncleared transactions, fees, or interest not yet recorded. |

| Reconciliation Discrepancies | Resolve discrepancies by checking for missing or duplicate transactions. |

| Completion | Ensure the Difference field shows $0.00 before finalizing. |

| Reports | Generate a Reconciliation Report for audit purposes. |

| Frequency | Recommended monthly or as per bank statement availability. |

| Tools | QuickBooks Desktop or QuickBooks Online. |

| Best Practices | Regularly reconcile to maintain accurate financial records. |

Explore related products

What You'll Learn

- Prepare Bank Statement: Gather and organize your bank statement for the period you're reconciling

- Match Transactions: Compare QuickBooks transactions with bank statement entries to identify matches

- Adjust Opening Balance: Ensure QuickBooks opening balance matches the bank statement's beginning balance

- Clear Uncleared Items: Review and clear any uncleared transactions in QuickBooks

- Finalize Reconciliation: Confirm discrepancies, make adjustments, and complete the reconciliation process in QuickBooks

![]()

Prepare Bank Statement: Gather and organize your bank statement for the period you're reconciling

The foundation of any successful bank reconciliation in QuickBooks lies in the accuracy and organization of your bank statement. Before diving into the reconciliation process, ensure you have the correct statement for the period you're working with. This might seem obvious, but it's a critical step often overlooked, leading to discrepancies and unnecessary headaches.

Gathering the Statement: Obtain the bank statement directly from your financial institution. Most banks provide online access to statements, allowing you to download a PDF or CSV file. If you prefer physical copies, request a printed statement for the specific period. For instance, if you're reconciling the previous month's transactions, ensure the statement covers the entire month, from the first to the last day. This comprehensive approach ensures you don't miss any transactions.

Organizing the Data: Once you have the statement, it's time to organize the information. Start by reviewing the statement for any unusual or unexpected transactions. Highlight or make notes of these entries, as they might require further investigation during the reconciliation process. Then, categorize the transactions into logical groups. For example, separate income sources, expense types, and transfers. This categorization simplifies the matching process in QuickBooks, making it easier to identify any discrepancies.

A practical tip is to use a spreadsheet to organize the data. Create columns for date, description, amount, and category. This structured format allows for quick sorting and filtering, enabling you to identify patterns or anomalies. For instance, sorting by date can reveal any missing or duplicate transactions, while filtering by category can help you quickly total specific expense types.

Attention to Detail: Pay close attention to the statement's opening and closing balances. These figures are crucial for reconciliation. Ensure the opening balance matches the previous period's closing balance, as this continuity is essential for accurate financial reporting. Any discrepancy here could indicate an error in the previous reconciliation or a missing transaction.

In summary, preparing the bank statement is a meticulous process that requires attention to detail and organization. By gathering the correct statement, organizing transactions, and focusing on key balances, you set the stage for a smooth and accurate bank reconciliation in QuickBooks. This initial step is the cornerstone of the entire process, ensuring the integrity of your financial data.

Step-by-Step Guide to Registering for Capitec Internet Banking Easily

You may want to see also

Explore related products

![]()

Match Transactions: Compare QuickBooks transactions with bank statement entries to identify matches

Matching transactions is the cornerstone of bank reconciliation in QuickBooks, ensuring your financial records align with your actual bank activity. Begin by importing your bank statement into QuickBooks, either manually or through a secure bank feed. This step is crucial because it provides a clear, up-to-date snapshot of your bank transactions. Once imported, QuickBooks will automatically attempt to match these entries with existing transactions in your register. Pay close attention to the dates, amounts, and descriptions, as even small discrepancies can indicate errors or missing entries.

The matching process in QuickBooks is designed to be intuitive but requires careful oversight. For instance, a deposit recorded in QuickBooks as $1,200 might appear on your bank statement as $1,200.50 due to accrued interest. QuickBooks may flag this as a mismatch, but you’ll need to investigate further. Use the "Find Matches" feature to manually link these transactions, ensuring you account for every penny. If a transaction remains unmatched, consider whether it was entered incorrectly, omitted, or if it’s a bank fee or interest adjustment that needs to be recorded separately.

One practical tip is to start with larger, more distinct transactions first, as these are easier to identify and match. For example, a $5,000 invoice payment is less likely to be confused with other entries than a $50 office supply purchase. Once the larger transactions are reconciled, focus on the smaller ones, using filters to narrow down by date or amount. This systematic approach minimizes errors and ensures no transaction is overlooked. Additionally, regularly reconciling accounts—monthly or quarterly—prevents discrepancies from compounding over time.

Caution should be exercised when dealing with duplicate transactions or those that appear in both QuickBooks and your bank statement but don’t align perfectly. For example, a check payment might clear the bank days after it’s recorded in QuickBooks, leading to a timing mismatch. In such cases, verify the transaction details and adjust the date or amount in QuickBooks if necessary. Avoid the temptation to delete unmatched transactions without investigation, as this can lead to inaccurate financial reporting.

In conclusion, matching transactions in QuickBooks is a meticulous but essential task that bridges the gap between your accounting records and actual bank activity. By leveraging QuickBooks’ automated tools, adopting a systematic approach, and exercising caution with discrepancies, you can ensure your financial data remains accurate and reliable. Regular reconciliation not only maintains compliance but also provides a clear financial picture, enabling better decision-making for your business.

How Banks Calculate Your Pre-Approval Amount: Key Factors Explained

You may want to see also

Explore related products

![]()

Adjust Opening Balance: Ensure QuickBooks opening balance matches the bank statement's beginning balance

Before reconciling your bank account in QuickBooks, a critical step often overlooked is ensuring the opening balance in QuickBooks aligns with the beginning balance on your bank statement. This discrepancy can stem from various sources: initial setup errors, missed transactions, or adjustments not recorded in QuickBooks. Ignoring this mismatch will render your reconciliation inaccurate, leading to unreliable financial reports.

To adjust the opening balance, navigate to the Chart of Accounts in QuickBooks, locate your bank account, and select "Edit." Here, you’ll find the opening balance field. Compare this figure to the beginning balance on your bank statement. If they differ, update the QuickBooks balance to match the statement. This step is purely an adjustment to the starting point and does not affect historical transactions. It’s a corrective measure, not a transaction entry, ensuring your reconciliation begins on solid ground.

A common pitfall is confusing this adjustment with recording transactions. For instance, if your QuickBooks opening balance is $10,000 but your statement shows $10,500, simply update the QuickBooks balance to $10,500. Do not create a journal entry for the $500 difference, as this would double-count the adjustment. The goal is to synchronize the starting point, not to account for the discrepancy as a transaction.

For businesses with multiple bank accounts or those transitioning to QuickBooks mid-year, this step becomes even more crucial. Each account must be individually verified and adjusted if necessary. If you’re unsure about the source of the discrepancy, review your initial setup or consult the bank statements from the period when the account was added to QuickBooks. Accuracy here prevents compounding errors in future reconciliations.

Finally, after adjusting the opening balance, run a reconciliation report to verify the alignment. If the beginning and ending balances match your bank statement, you’ve successfully addressed the foundational issue. This process not only ensures data integrity but also builds confidence in your financial reporting, allowing you to focus on more strategic aspects of your business.

Monthly Fees: Are US Banks Charging Customers?

You may want to see also

Explore related products

![]()

Clear Uncleared Items: Review and clear any uncleared transactions in QuickBooks

Uncleared transactions in QuickBooks can distort your financial picture, leading to inaccurate reporting and decision-making. These items represent checks, deposits, or other transactions that haven’t yet posted to your bank account. Left unresolved, they create discrepancies between your QuickBooks records and actual bank statements, undermining the integrity of your reconciliation process. Addressing these uncleared items is a critical step in ensuring your books reflect reality.

Begin by accessing the "Reconcile" tool in QuickBooks and navigating to the "Uncleared Transactions" section. Here, you’ll find a list of transactions that haven’t cleared your bank. Compare this list against your bank statement, meticulously matching dates, amounts, and descriptions. For checks, verify payee names and memo details. For deposits, ensure the source (e.g., customer payments, sales revenue) aligns with your records. This cross-referencing minimizes errors and ensures accuracy.

Once identified, clear uncleared items by marking them as reconciled in QuickBooks. If a transaction appears in QuickBooks but not on your bank statement, investigate further. It could be a timing issue (the transaction hasn’t posted yet) or an error (e.g., incorrect entry, missing deposit). For timing discrepancies, note the transaction date and recheck in subsequent reconciliations. For errors, correct the entry in QuickBooks immediately to maintain data integrity.

A proactive approach to uncleared items saves time and reduces frustration. Regularly review outstanding transactions and follow up on discrepancies promptly. For example, if a check hasn’t cleared within 30 days, contact the payee to confirm receipt. Similarly, if a deposit is missing, verify with your bank or the payer. By staying vigilant, you ensure a smoother reconciliation process and more reliable financial reporting. Clearing uncleared items isn’t just a task—it’s a safeguard for your financial accuracy.

How Banks Investigate and Combat Fraudulent Activities Effectively

You may want to see also

Explore related products

![]()

Finalize Reconciliation: Confirm discrepancies, make adjustments, and complete the reconciliation process in QuickBooks

Discrepancies between your QuickBooks records and bank statement are inevitable, but they don’t have to derail your reconciliation. QuickBooks flags these differences during the reconciliation process, highlighting uncleared transactions, missing entries, or timing mismatches. Before finalizing, scrutinize each discrepancy. Cross-reference dates, amounts, and descriptions with both your bank statement and QuickBooks register. Look for common culprits like uncleared checks, pending deposits, or bank fees not yet recorded in QuickBooks.

Once discrepancies are confirmed, adjustments are necessary to align QuickBooks with your bank statement. For uncleared transactions, ensure they’re accurately entered in QuickBooks and marked as "outstanding." If a transaction is missing, manually add it to the appropriate account, ensuring it matches the bank statement details. For timing differences, like deposits in transit or outstanding checks, verify their status and adjust accordingly. QuickBooks allows you to create journal entries for corrections, but use this sparingly to avoid cluttering your books.

Completing the reconciliation in QuickBooks is straightforward but requires attention to detail. After addressing discrepancies, review the "Begin Reconciliation" window to ensure the ending balance matches your bank statement. If it does, click "Reconcile Now." QuickBooks will prompt you to confirm the reconciliation and generate a report summarizing the process. Save this report for your records—it’s a critical audit trail. Once finalized, QuickBooks locks the reconciled period, preventing accidental changes.

A practical tip: Before clicking "Reconcile Now," double-check that all adjustments are correct. Mistakes made after finalization require reversing the entire reconciliation, a tedious process. Additionally, if discrepancies persist despite thorough review, consider reaching out to your bank to verify statement accuracy or consult a QuickBooks expert for guidance. Finalizing reconciliation isn’t just about balancing numbers—it’s about ensuring your financial records are accurate, reliable, and ready for decision-making.

Locate Your PNC Bank Branch ID: A Quick and Easy Guide

You may want to see also

Frequently asked questions

Bank reconciliation in QuickBooks is the process of comparing your QuickBooks records with your bank statement to ensure accuracy and identify discrepancies. It’s important because it helps maintain financial integrity, detect errors, and prevent fraud.

To start, go to the Banking menu, select Reconcile, choose the account you want to reconcile, and enter the ending balance and ending date from your bank statement. Click Start Reconciling to begin matching transactions.

If the beginning balance doesn’t match, it indicates a discrepancy from a previous reconciliation. Review the previous reconciliation report, check for missed or incorrect entries, and correct them before proceeding.

Uncleared transactions are those that appear in QuickBooks but not on your bank statement. Leave them unchecked during reconciliation, as they will clear in future statements. Ensure they are accurately recorded in QuickBooks.

If the reconciliation doesn’t balance, review your transactions for errors, missed entries, or duplicate entries. Use the Locate Discrepancies tool in QuickBooks to identify issues. If the problem persists, consult with an accountant or QuickBooks support.