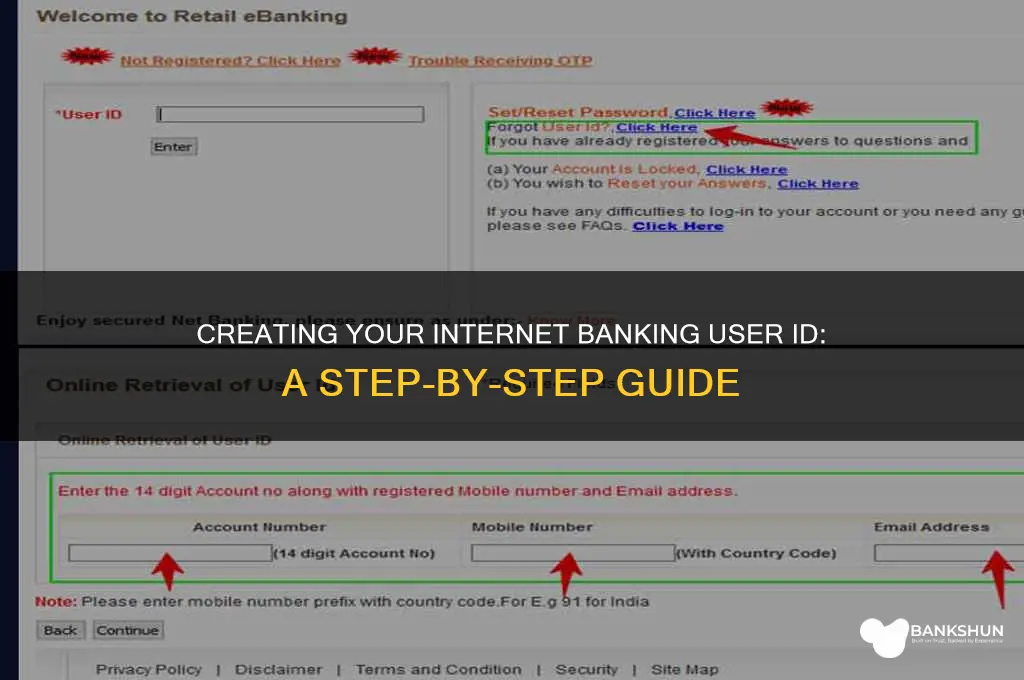

Creating an internet banking user ID is a straightforward process that allows you to access your bank account online securely and conveniently. Typically, you start by visiting your bank’s official website or mobile app and locating the registration or first-time user option. You’ll be required to provide personal details such as your account number, debit card number, or registered mobile number for verification. Following this, you’ll create a unique user ID, often adhering to specific criteria like length, alphanumeric characters, or special symbols. Once verified, your user ID is activated, enabling you to log in and manage your finances seamlessly. Always ensure you follow your bank’s guidelines and keep your credentials secure to protect your account.

| Characteristics | Values |

|---|---|

| Bank-Specific Process | Each bank has its own unique process for creating an internet banking user ID. |

| Registration Methods | Online via bank's website, mobile app, or offline at a bank branch. |

| Required Documents | Account number, CIF number, debit/credit card details, or registered mobile number. |

| Authentication Methods | OTP (One-Time Password) sent to registered mobile number or email. |

| User ID Format | Alphanumeric (combination of letters and numbers), often customizable. |

| Password Creation | Users typically set a password during the registration process. |

| Security Questions | Some banks require setting up security questions for additional security. |

| Instant Activation | User ID is often activated instantly upon successful registration. |

| Customer Support | Available via phone, email, or chat for assistance during registration. |

| Terms and Conditions | Users must agree to the bank's terms and conditions for internet banking. |

| Compatibility | Works across desktop, mobile, and tablet devices. |

| Multi-Factor Authentication (MFA) | Some banks implement MFA for enhanced security during login. |

| Temporary User ID | Some banks provide a temporary ID that requires conversion to a permanent one. |

| Notification System | Users receive notifications upon successful user ID creation. |

| Reset/Recovery Options | Option to reset or recover user ID via registered mobile number or email. |

| Language Support | Multiple languages supported based on the bank's regional presence. |

| Compliance | Adheres to local and international banking regulations and security standards. |

Explore related products

What You'll Learn

- Choose a Unique ID: Combine letters, numbers, and symbols for a secure, memorable, and unique user ID

- Follow Bank Guidelines: Adhere to the bank’s specific rules for creating a valid user ID

- Avoid Personal Info: Skip using names, birthdays, or easily guessable details in your ID

- Register Online: Complete the bank’s online registration process to create your user ID

- Verify Your ID: Confirm your user ID via OTP, email, or other bank-approved verification methods

![]()

Choose a Unique ID: Combine letters, numbers, and symbols for a secure, memorable, and unique user ID

Creating a user ID for internet banking isn’t just about picking a name—it’s about crafting a digital fortress. A unique ID combines letters, numbers, and symbols to form a barrier against unauthorized access. Think of it as a complex lock: the more varied the components, the harder it is to pick. For instance, "JohnDoe123" is predictable, but "J#7dN!9x" is a puzzle. This approach leverages entropy, a security principle where randomness increases strength. By mixing uppercase and lowercase letters, digits, and special characters, you exponentially reduce the likelihood of a brute-force attack.

Now, let’s break it down into actionable steps. Start with a base word or phrase that’s personally meaningful but not obvious—a childhood nickname, a favorite book, or a hobby. For example, if you love hiking, use "TrailBlazer." Next, dissect it: replace letters with numbers or symbols (e.g., "Tr@!lBl@z3r"). Add a random element to throw off patterns, like appending "!9m" to make it "Tr@!lBl@z3r!9m." Keep it between 8–16 characters to balance complexity and memorability. Avoid common substitutions like "4" for "A" or "1" for "L," as hackers account for these.

Memorability is just as critical as complexity. A secure ID is useless if you can’t recall it. One trick is to create a mnemonic. For instance, "My cat Whiskers was born in 2015" becomes "McWwb!2015#." Here, "Mc" stands for "My cat," "Wwb" for "Whiskers was born," and "!2015#" adds the year with symbols. Test your ID by trying to recall it after a day—if it sticks, it’s a keeper. If not, simplify the mnemonic or shorten the phrase.

Finally, consider the platform’s rules. Some banks restrict symbols or require specific formats, so check their guidelines before finalizing. For example, if only alphanumeric characters are allowed, focus on mixing letters and numbers creatively, like "K1ngF1sh86." Even without symbols, you can achieve uniqueness by combining unrelated words or using multiple languages. For instance, "Soleil365Luna" blends French and Spanish with numbers.

In conclusion, a unique user ID is a blend of art and science. It’s about thinking like both a hacker and a poet—crafting something unpredictable yet personally resonant. By combining letters, numbers, and symbols thoughtfully, you create a digital signature that’s both secure and yours. Remember, this isn’t just a password; it’s the first line of defense for your financial life. Make it count.

Complete Guide to Filling HDFC Bank DRF Form Easily

You may want to see also

Explore related products

![Simplified Guide to iMovie For Every User [Colored]: Master Video Editing on Mac and iPhone for YouTube, TikTok, and Everyday Content & Movie Creation](https://m.media-amazon.com/images/I/6138HraqWHL._AC_UY218_.jpg)

![]()

Follow Bank Guidelines: Adhere to the bank’s specific rules for creating a valid user ID

Creating a valid internet banking user ID isn’t a one-size-fits-all process. Each bank has its own set of rules designed to ensure security and compliance. Ignoring these guidelines can lead to rejected IDs, delayed access, or even account locks. For instance, while one bank may allow special characters like underscores or hyphens, another might strictly prohibit them. Similarly, character limits can vary—some banks permit up to 12 characters, while others restrict it to 8. Failing to adhere to these specifics can render your ID invalid, forcing you to start over.

Banks often provide detailed instructions in their online registration portals or user manuals. These guidelines typically cover allowed characters (alphanumeric, special symbols), case sensitivity (upper vs. lower case), and prohibited elements (sequential numbers, easily guessable patterns). For example, a bank might require a combination of letters and numbers but disallow spaces or consecutive identical characters. Some banks even mandate the inclusion of specific elements, such as your date of birth or initials, in a particular format. Always review these rules before attempting to create your ID.

A common pitfall is assuming that what worked for one bank will work for another. For instance, if your previous bank allowed your full name as a user ID, your current bank might restrict it to a nickname or a combination of your name and a unique identifier. Another example is password complexity rules—some banks may require at least one uppercase letter and one number, while others might demand a special character as well. Misinterpreting or overlooking these nuances can lead to frustration and unnecessary delays.

To ensure compliance, follow a systematic approach. Start by locating the bank’s official guidelines, often found in the "Help" or "FAQs" section of their website. If unclear, contact customer support for clarification. Once you understand the rules, brainstorm a user ID that meets all criteria. Test it during the registration process, as some banks provide real-time feedback on whether your ID is valid. If rejected, revise it immediately, ensuring each attempt aligns with the bank’s specifications.

Finally, treat your user ID as a critical security element. Avoid sharing it or using easily guessable information, even if the bank allows it. While adhering to guidelines is essential, combining compliance with security best practices ensures your internet banking experience remains safe and seamless. Remember, the goal isn’t just to create a valid ID but to create one that protects your account while meeting the bank’s standards.

How to Effectively Lodge a Complaint with Commonwealth Bank

You may want to see also

Explore related products

![]()

Avoid Personal Info: Skip using names, birthdays, or easily guessable details in your ID

Using personal information like names, birthdays, or easily guessable details in your internet banking user ID is a common pitfall that compromises security. Hackers and fraudsters often exploit publicly available data, such as social media profiles or public records, to guess login credentials. For instance, combining your first name with your birth year (e.g., "John1985") creates an ID that’s vulnerable to brute-force attacks. Even seemingly obscure details, like a pet’s name or favorite sports team, can be deduced through social engineering tactics. By avoiding these predictable patterns, you eliminate low-hanging fruit for cybercriminals.

Consider the anatomy of a secure user ID: it should be abstract, random, and unrelated to your personal life. Instead of "Sarah2000," opt for a combination of unrelated words or characters, like "BlueOak37." This approach leverages unpredictability, making it exponentially harder for attackers to crack. Tools like password managers often include random ID generators, which can create strings like "K29LmtG5" or "Zephyr9Vox." While these may seem less memorable, pairing them with a secure password manager ensures accessibility without sacrificing security.

A comparative analysis reveals the stark difference in vulnerability between personal and non-personal IDs. A study by cybersecurity firm Kaspersky found that 83% of breached accounts used IDs containing personal information. Conversely, accounts with randomized IDs experienced significantly fewer breaches. This data underscores the importance of depersonalizing your user ID. Even if a hacker gains access to your other credentials, a non-personalized ID acts as an additional layer of defense, complicating their efforts to infiltrate your account.

Practical implementation involves a two-step process. First, brainstorm a list of random words, numbers, or phrases that hold no personal significance. For example, "Crimson7Wren" or "Atlas42Quill." Second, test the ID’s strength using online tools like the zxcvbn password strength estimator. Aim for a score above 80%, indicating high resistance to guessing or cracking. Remember, the goal isn’t just to create an ID—it’s to build a fortress around your financial data. By divorcing your user ID from personal details, you’re not just following best practices; you’re actively thwarting potential threats.

Effortlessly Sync Your Bank Transactions to YNAB: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Register Online: Complete the bank’s online registration process to create your user ID

Creating an internet banking user ID begins with the bank’s online registration process, a straightforward yet crucial step that unlocks access to digital financial services. Most banks design their registration portals to be user-friendly, requiring minimal technical expertise. To start, visit the bank’s official website and locate the "Register for Internet Banking" or "New User Registration" option, typically found on the homepage. This initiates a sequence of steps where you’ll be prompted to enter personal details such as your account number, debit card details, and registered mobile number. Accuracy is key here—a single typo can delay the process or trigger security flags.

The registration process often includes a verification stage to confirm your identity. This may involve receiving a One-Time Password (OTP) on your registered mobile number or email address. Some banks also require additional details, like your date of birth or the IFSC code of your branch, to ensure the account belongs to you. Once verified, you’ll be guided to create a unique user ID. This is where personalization comes in—choose a combination of letters, numbers, or special characters that’s easy for you to remember but difficult for others to guess. Avoid common patterns like "12345" or your name, as these compromise security.

While the process is generally intuitive, there are pitfalls to avoid. For instance, never register on a public Wi-Fi network or an unsecured device, as this exposes your credentials to potential hackers. Additionally, be wary of phishing attempts—always type the bank’s URL directly into your browser instead of clicking on links from unsolicited emails or messages. If you encounter technical issues, such as a frozen screen or error messages, clear your browser cache or switch to a different browser. Most banks also offer customer support via chat or phone to assist with registration challenges.

Completing the online registration process not only creates your user ID but also sets the foundation for secure internet banking. Once registered, you’ll gain access to features like fund transfers, bill payments, and account statements, all from the convenience of your device. It’s a small investment of time that yields long-term benefits, streamlining your financial management and reducing reliance on physical bank visits. By following the bank’s instructions carefully and prioritizing security, you’ll ensure a smooth transition into the digital banking ecosystem.

How Bank Transfers Work Over the Weekend

You may want to see also

Explore related products

![]()

Verify Your ID: Confirm your user ID via OTP, email, or other bank-approved verification methods

Creating a secure internet banking user ID is only the first step; verifying it is where the real security begins. Banks employ multiple layers of verification to ensure that the person accessing the account is indeed the account holder. One of the most common methods is One-Time Password (OTP) verification, where a unique code is sent to your registered mobile number. This OTP must be entered within a specified time frame, typically 5 to 10 minutes, to confirm your identity. The ephemeral nature of the OTP ensures that even if intercepted, it cannot be reused, adding a robust layer of security.

Another widely used method is email verification, where a confirmation link or code is sent to your registered email address. This method is particularly useful for users who may not have immediate access to their mobile phones or prefer a secondary verification channel. However, it’s crucial to ensure your email account is also secure, as compromised emails can undermine this verification step. Banks often recommend enabling two-factor authentication (2FA) on your email account for added protection.

For those who prefer a more traditional approach, bank-approved physical verification is an option. This involves visiting a bank branch with valid identification documents, such as a passport or driver’s license, to confirm your identity in person. While this method is less convenient, it is highly secure and often required for high-risk transactions or when setting up internet banking for the first time. Some banks also offer biometric verification, such as fingerprint or facial recognition, for users with compatible devices, blending convenience with advanced security.

A lesser-known but equally effective method is security questions, where you answer pre-set questions during the verification process. While this method is simple, it relies heavily on the uniqueness and secrecy of your answers. Avoid using easily guessable information like birthdays or common names. Instead, opt for specific details only you would know, such as the name of your first pet or the street you grew up on.

In conclusion, verifying your internet banking user ID is a critical step that leverages multiple methods to ensure security. Whether through OTPs, emails, physical verification, or security questions, each method serves a unique purpose and caters to different user preferences. By understanding and utilizing these bank-approved verification methods, you not only protect your account but also contribute to a safer digital banking ecosystem. Always keep your contact details updated and follow best practices to maintain the integrity of your verification channels.

Banking Regulations: Are They Universal or Unique?

You may want to see also

Frequently asked questions

Contact your bank’s customer service or visit their official website/mobile app. Follow the registration process, which typically involves entering your account details, verifying your identity, and setting up a unique user ID.

Most banks allow you to choose your own user ID during the registration process, provided it meets their criteria (e.g., length, uniqueness). Some banks may assign a temporary ID that you can later change.

Typically, no additional documents are required if you’re an existing account holder. You’ll need your account number, debit/credit card details, registered mobile number, and sometimes your ATM PIN or OTP for verification.

Visit your bank’s website or app and look for the "Forgot User ID" option. You’ll need to verify your identity using your account details, registered mobile number, or debit/credit card information to retrieve your user ID.