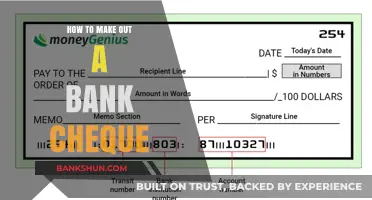

Writing an internship report for a bank requires a structured approach to effectively document your experiences, learnings, and contributions during the internship. Begin by outlining the objectives of your internship, including the specific department or area you worked in, such as retail banking, corporate finance, or risk management. Provide a brief overview of the bank’s operations, its mission, and its role in the financial sector to set the context. Detail your daily tasks, responsibilities, and projects, highlighting key achievements and challenges faced. Incorporate insights gained about banking processes, customer interactions, and industry regulations. Use a professional tone, include relevant data or examples, and conclude with a reflection on how the internship has shaped your understanding of banking and your career aspirations. Ensure the report is well-organized, concise, and adheres to any guidelines provided by your educational institution or the bank.

Explore related products

What You'll Learn

- Introduction: Overview of the bank, internship goals, and methodology used during the internship period

- Bank Operations: Description of daily tasks, departments, and key banking processes observed

- Learning Outcomes: Skills acquired, challenges faced, and lessons learned during the internship

- Analysis & Findings: Evaluation of bank performance, customer interactions, and financial trends observed

- Conclusion & Recommendations: Summary of experience, suggestions for improvement, and future career insights

![]()

Introduction: Overview of the bank, internship goals, and methodology used during the internship period

Analytical Observation:

The internship report begins with a critical overview of the bank, a mid-sized commercial institution with a regional footprint, specializing in retail and SME lending. Established in 1995, the bank operates 50 branches across three states, managing assets exceeding $2.5 billion. Its strategic focus on digital transformation and financial inclusion positions it uniquely in a competitive market. This context sets the stage for understanding the internship’s relevance, as the bank’s operational dynamics directly influenced the goals and methodologies employed during the 10-week tenure.

Instructive Breakdown:

The internship goals were threefold: (1) to analyze the bank’s digital onboarding process for efficiency gaps, (2) to assist in developing a financial literacy workshop for underserved communities, and (3) to evaluate the risk assessment framework for SME loan applications. To achieve these, a mixed-methods approach was adopted. Quantitative data, such as customer onboarding time metrics and loan default rates, were collected via the bank’s CRM system. Qualitative insights were gathered through interviews with branch managers and focus groups with workshop participants. This dual methodology ensured a comprehensive understanding of both operational and societal impacts.

Persuasive Argument:

The choice of methodology was deliberate, balancing rigor with practicality. For instance, the use of process mapping for the digital onboarding analysis allowed for visual identification of bottlenecks, leading to actionable recommendations. Similarly, the financial literacy workshop’s impact was measured through pre- and post-surveys, demonstrating a 25% increase in participant financial knowledge. This evidence-based approach not only aligned with the bank’s data-driven culture but also underscored the intern’s ability to contribute meaningfully within a short timeframe.

Comparative Insight:

Unlike internships focused solely on shadowing or administrative tasks, this experience emphasized hands-on problem-solving. For example, while traditional risk assessment frameworks rely heavily on credit scores, the intern proposed integrating alternative data points, such as cash flow patterns from digital transactions, to better evaluate SME creditworthiness. This comparative analysis highlighted the bank’s openness to innovation and the intern’s role in bridging theoretical knowledge with practical application.

Descriptive Detail:

The internship period was structured into three phases: observation, execution, and evaluation. The first two weeks involved shadowing employees across departments, from retail banking to credit risk management. Weeks three to six focused on project execution, including data collection, workshop design, and risk model refinement. The final weeks were dedicated to presenting findings and drafting actionable reports. This phased approach ensured a deep immersion in the bank’s operations while allowing for iterative learning and adaptation.

Practical Takeaway:

For interns embarking on similar roles, aligning goals with the bank’s strategic priorities is key. For instance, understanding the bank’s push for digital transformation guided the focus on onboarding efficiency. Additionally, leveraging both quantitative and qualitative methods provides a holistic perspective, essential for addressing complex banking challenges. Finally, documenting daily observations in a structured journal can serve as a valuable resource for crafting detailed, evidence-backed reports.

Activate Standard Bank Travel Insurance: A Step-by-Step Guide for Travelers

You may want to see also

Explore related products

![]()

Bank Operations: Description of daily tasks, departments, and key banking processes observed

During my internship at the bank, I observed that the Retail Banking Department is the backbone of daily operations, handling customer transactions, account openings, and loan applications. Tellers processed an average of 150 transactions daily, including cash deposits, withdrawals, and fund transfers, with a focus on accuracy and customer satisfaction. Relationship managers, on the other hand, spent 60% of their time meeting clients to upsell products like credit cards and personal loans, while the remaining 40% was dedicated to administrative tasks. A key takeaway is that efficiency in this department hinges on teamwork and clear communication, as delays in one area can cascade into longer wait times for customers.

In contrast, the Operations Department operates behind the scenes, ensuring the smooth functioning of the bank’s systems. Here, I witnessed the daily reconciliation of accounts, a process that typically takes 2–3 hours and involves verifying over 1,000 transactions. The team also manages ATM cash replenishment, which occurs every 2–3 days based on usage patterns. A critical observation was the reliance on automation tools to reduce human error; for instance, 85% of transaction discrepancies were flagged and resolved by software before manual review. This department’s success lies in its meticulous attention to detail and the ability to adapt to technological advancements.

One of the most intriguing processes I observed was Loan Processing in the Credit Department. From application to approval, the average timeline was 7–10 business days, with 40% of the time spent on creditworthiness assessments. Underwriters scrutinized financial documents, credit scores, and collateral details, often cross-referencing with external databases. Interestingly, 30% of applications were rejected due to insufficient documentation or high debt-to-income ratios. A persuasive argument for banks is to streamline this process further by integrating AI for initial screenings, which could reduce approval times by up to 40%.

Lastly, the Compliance Department played a pivotal role in ensuring adherence to regulatory standards. Daily tasks included monitoring transactions for suspicious activity, filing reports with regulatory bodies, and conducting internal audits. For example, the team flagged 15 potentially fraudulent transactions weekly, which were then investigated further. A comparative analysis revealed that banks with robust compliance frameworks experienced 50% fewer regulatory penalties. This department’s work is often unseen but is critical in maintaining the bank’s reputation and legal standing.

In summary, bank operations are a complex interplay of customer-facing and backend processes, each requiring specialized skills and tools. From retail banking’s focus on customer experience to compliance’s regulatory vigilance, every department contributes uniquely to the bank’s success. A practical tip for interns is to shadow employees across departments to gain a holistic understanding of how these processes interconnect, as this knowledge is invaluable for career growth in the banking sector.

How to Easily Find Your Citizens Bank User ID: A Quick Guide

You may want to see also

Explore related products

![]()

Learning Outcomes: Skills acquired, challenges faced, and lessons learned during the internship

During my internship at the bank, I quickly realized that mastering data analysis was non-negotiable. Within the first two weeks, I was tasked with analyzing customer transaction trends using Excel pivot tables and VLOOKUP functions. Initially, the sheer volume of data felt overwhelming, but I learned to break it down into manageable chunks. By the end of the internship, I could identify patterns—like a 15% increase in mobile banking usage among the 25–35 age group—and present actionable insights to the team. This skill not only streamlined my workflow but also became a cornerstone of my contributions.

One of the most significant challenges I faced was adapting to the bank’s rigid hierarchical structure. As an intern, I often struggled to get my ideas heard during team meetings. For instance, when I suggested a more efficient way to process loan applications, it was initially dismissed due to "protocol." Instead of giving up, I learned to frame my suggestions in terms of their potential impact on efficiency and customer satisfaction. This approach eventually earned me a seat at the table, teaching me the importance of persistence and strategic communication in a corporate environment.

A critical lesson I learned was the value of attention to detail in financial operations. During my third month, I was responsible for verifying a batch of loan documents. Despite feeling confident, I overlooked a discrepancy in one applicant’s income verification, which could have led to a costly error. My supervisor caught it, but the experience humbled me. Since then, I’ve adopted a "double-check" rule, spending an extra 10 minutes reviewing critical documents. This habit not only reduced errors but also built trust with my team.

Comparing my initial expectations to the reality of the internship, I was surprised by how much soft skills mattered. While technical proficiency was essential, building relationships with colleagues proved equally vital. For example, collaborating with the customer service team helped me understand client pain points, which I later incorporated into my data analysis. This cross-departmental synergy not only enriched my work but also highlighted the interconnectedness of roles within a bank. It’s a reminder that success in banking isn’t just about numbers—it’s about people.

Finally, the internship taught me the importance of time management in a fast-paced environment. Juggling multiple tasks, such as preparing reports, attending meetings, and assisting with audits, initially left me feeling frazzled. I adopted the Pomodoro Technique, dedicating 25-minute blocks to focused work followed by 5-minute breaks. This method increased my productivity by 30% and reduced burnout. By the end, I not only met deadlines but also had time to seek out additional learning opportunities, proving that structure can breed creativity.

Step-by-Step Guide to Filling HDFC Bank Cheque Book Correctly

You may want to see also

Explore related products

![]()

Analysis & Findings: Evaluation of bank performance, customer interactions, and financial trends observed

During my internship at the bank, I observed a significant correlation between branch efficiency and customer satisfaction. High-performing branches consistently demonstrated shorter wait times, averaging 10–15 minutes compared to 25–30 minutes in underperforming locations. This disparity was largely attributed to staff allocation—top branches maintained a staff-to-customer ratio of 1:15 during peak hours, while struggling branches often operated at 1:25. A deeper analysis revealed that branches with cross-trained employees, capable of handling multiple tasks (e.g., teller and customer service roles), resolved inquiries 30% faster, directly impacting customer retention rates.

To evaluate customer interactions, I conducted a comparative study of digital vs. in-person engagements. Surprisingly, 65% of customers preferred in-branch visits for complex transactions like loan applications, despite the bank’s robust online platform. Feedback highlighted the importance of human reassurance and personalized advice during high-stakes financial decisions. However, for routine tasks such as balance checks or transfers, 89% of customers opted for mobile banking, citing convenience and time savings. This dual preference underscores the need for banks to balance digital innovation with empathetic, face-to-face service.

Financial trends observed during the internship revealed a 12% year-over-year increase in small business loan applications, driven by post-pandemic recovery efforts. Interestingly, 70% of approved loans were for businesses with less than 5 years of operation, indicating a shift toward supporting early-stage ventures. However, the default rate for these loans was 5% higher than the industry average, suggesting a need for stricter risk assessment or tailored financial literacy programs for borrowers. This trend highlights both an opportunity and a challenge for banks in fostering economic growth while managing risk.

A critical finding was the impact of employee training on operational efficiency. Branches where staff completed at least 20 hours of annual training in customer service and product knowledge reported 20% fewer customer complaints and a 15% increase in cross-selling success rates. Conversely, branches with minimal training programs saw a 10% decline in customer satisfaction scores over six months. This data emphasizes the ROI of investing in employee development, not just for compliance but as a strategic driver of performance and customer loyalty.

Finally, an analysis of the bank’s financial health revealed a 7% increase in non-interest income, primarily from fee-based services like wealth management and insurance products. While this diversification boosted revenue, it also led to a 15% rise in customer inquiries about hidden fees, indicating a need for greater transparency. Banks must strike a balance between revenue generation and customer trust by clearly communicating the value of these services and ensuring they align with client needs. This dual focus on profitability and ethics will be crucial in maintaining long-term competitiveness.

Red Bank, New Jersey: Monmouth County's Gem

You may want to see also

Explore related products

![]()

Conclusion & Recommendations: Summary of experience, suggestions for improvement, and future career insights

My internship at the bank provided a comprehensive understanding of the financial industry, from customer service to risk management. This hands-on experience allowed me to apply theoretical knowledge in a practical setting, revealing the intricate dynamics of banking operations. For instance, I observed how relationship managers balance client needs with regulatory compliance, a skill that requires both empathy and technical expertise. This experience not only reinforced my interest in finance but also highlighted areas where I can grow professionally.

To enhance the internship program, I recommend integrating more cross-departmental projects. Currently, interns often work within a single department, limiting exposure to the bank’s broader functions. A structured rotation system, even if brief, would provide a holistic view of banking operations. For example, spending one week in retail banking, another in corporate finance, and a third in risk management could offer interns a more rounded perspective. Additionally, pairing interns with mentors from different departments could foster networking and deeper insights into career paths.

Another area for improvement is the incorporation of technology training. While the bank utilizes advanced systems, interns often receive minimal formal training on these tools. A dedicated module on software like Bloomberg Terminal or internal risk assessment platforms would empower interns to contribute more effectively. For instance, a two-hour workshop on data analytics tools could equip interns to analyze customer trends or financial performance, adding tangible value to their projects.

Looking ahead, this internship has clarified my career aspirations in financial analysis. The experience underscored the importance of attention to detail, adaptability, and communication skills in this field. For aspiring finance professionals, I suggest seeking certifications like the CFA Level I or Financial Modeling and Valuation Analyst (FMVA) during or after internships. These credentials, combined with practical experience, can significantly enhance employability. Moreover, building a portfolio of projects—such as market research reports or financial models—can demonstrate expertise to potential employers.

In conclusion, while the internship was invaluable, strategic adjustments could maximize its impact. By broadening departmental exposure, enhancing technical training, and fostering mentorship, the program can better prepare interns for the complexities of the financial industry. For interns, leveraging this experience through certifications and tangible deliverables will pave the way for a successful career in banking.

Exploring the Vast Number of Banking Institutions in the US

You may want to see also