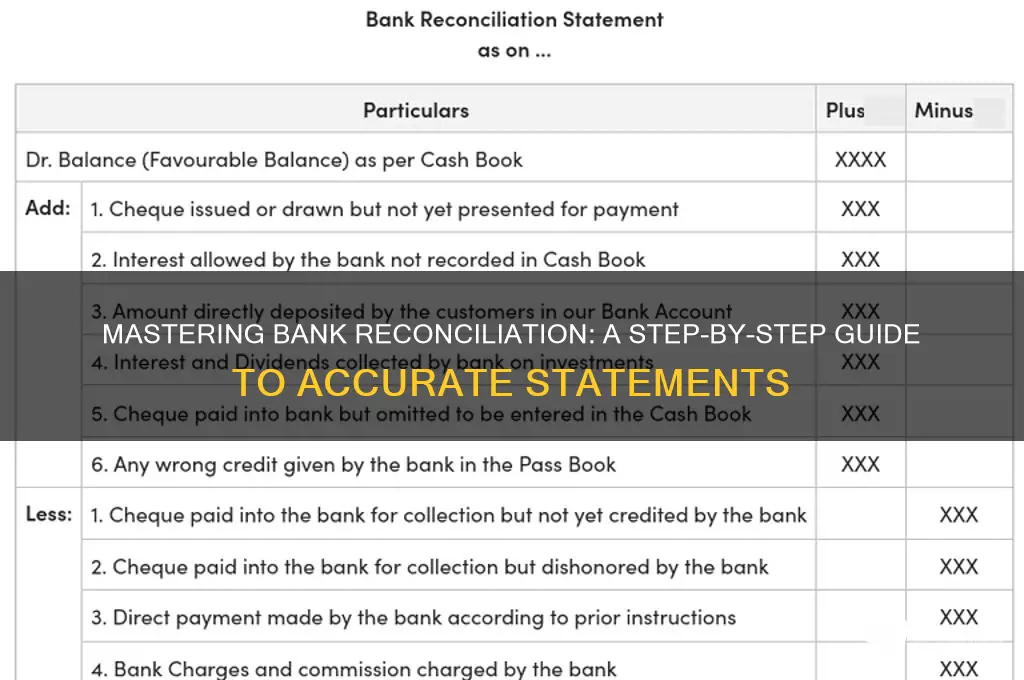

Reconciling a bank statement is a critical process for ensuring the accuracy of your financial records and identifying any discrepancies between your internal accounts and the bank's records. It involves comparing your business's or personal ledger entries with the transactions listed on the bank statement, verifying that all deposits, withdrawals, fees, and other activities are correctly recorded. Proper reconciliation helps detect errors, unauthorized transactions, or potential fraud, while also providing a clear snapshot of your financial health. To do it effectively, you’ll need to gather all relevant documents, match transactions meticulously, account for outstanding items, and adjust for timing differences. This process not only maintains financial integrity but also supports better decision-making and compliance with accounting standards.

| Characteristics | Values |

|---|---|

| Collect Documents | Gather your bank statement, checkbook register, deposit slips, and any other transaction records. |

| Choose a Reconciliation Period | Select a specific time frame (e.g., monthly) to reconcile your statement. |

| Compare Transactions | Match each transaction on your bank statement with your checkbook register or accounting records. |

| Identify Outstanding Items | Note any uncleared checks, pending deposits, or bank fees not yet recorded in your books. |

| Adjust for Timing Differences | Account for transactions that have not yet appeared on the bank statement (e.g., outstanding checks or deposits in transit). |

| Reconcile Opening Balance | Ensure your starting balance in the checkbook register matches the previous statement's ending balance. |

| Calculate Adjusted Balance | Add uncleared deposits and subtract outstanding checks/withdrawals to determine the reconciled balance. |

| Verify Bank Fees and Interest | Confirm that all bank charges and earned interest are accurately recorded. |

| Document Discrepancies | Investigate and resolve any discrepancies between your records and the bank statement. |

| Update Records | Make necessary adjustments to your checkbook register or accounting software to match the reconciled balance. |

| Finalize Reconciliation | Confirm that the adjusted balance matches the bank statement's ending balance. |

| Maintain Records | Keep all reconciliation documents for future reference and audits. |

| Frequency | Ideally, reconcile monthly or as frequently as needed for accurate financial tracking. |

| Tools | Use accounting software, spreadsheets, or manual ledgers for efficient reconciliation. |

| Review for Fraud | Look for unauthorized transactions or discrepancies that may indicate fraud. |

Explore related products

What You'll Learn

- Verify Opening Balance: Confirm the starting balance matches the previous statement's closing balance

- Record Deposits: Add all deposits not yet credited by the bank to your records

- Track Withdrawals: Subtract all withdrawals, including fees, checks, and debits, from your balance

- Identify Outstanding Items: Note uncleared checks, pending deposits, or transactions not yet processed

- Reconcile Discrepancies: Investigate and correct any differences between your records and the bank statement

![]()

Verify Opening Balance: Confirm the starting balance matches the previous statement's closing balance

The opening balance on your bank statement is the cornerstone of accurate reconciliation. It represents the financial position of your account at the beginning of the statement period, and its correctness is paramount. A discrepancy here can throw off your entire reconciliation process, leading to incorrect conclusions about your account's health. Therefore, the first step in reconciling your bank statement is to verify that the opening balance matches the closing balance from the previous statement.

To perform this verification, start by retrieving your most recent bank statement and the one preceding it. Locate the closing balance on the older statement, which should be clearly marked at the bottom of the document. This figure represents the total amount in your account at the end of the previous statement period. Next, open the current statement and find the opening balance, typically listed at the top. These two numbers must be identical for your reconciliation to proceed accurately. If they differ, investigate the cause immediately, as it could indicate an error in the bank's records or an oversight in your own tracking.

Consider a scenario where the previous statement's closing balance was $5,200, but the current statement's opening balance shows $5,350. This $150 discrepancy could stem from a variety of sources, such as a deposit or withdrawal that wasn't recorded, a bank fee, or an interest payment. To resolve this, review all transactions between the two statement periods, cross-referencing them with your personal records. If the discrepancy persists, contact your bank to request a detailed transaction history or to report a potential error. Timely resolution ensures that your financial records remain reliable.

A practical tip to streamline this process is to maintain a running record of your account balance, updated with each transaction. This can be done in a spreadsheet or a financial management app, where you log deposits, withdrawals, and fees as they occur. By doing so, you create a real-time snapshot of your account that can be easily compared to the bank's statements. For instance, if you note a $200 deposit on the 15th of the month, ensure it appears on the statement covering that period. This habit not only aids in verifying the opening balance but also helps identify discrepancies early, reducing the complexity of reconciliation.

In conclusion, verifying the opening balance against the previous statement's closing balance is a critical step in bank statement reconciliation. It ensures that your starting point is accurate, laying the foundation for a reliable review of your account activity. By systematically comparing these figures, investigating discrepancies, and maintaining detailed records, you can maintain a clear and accurate picture of your financial status. This diligence not only safeguards your finances but also fosters confidence in your ability to manage them effectively.

Northern Ireland's Food Banks: Counting Community Support and Locations

You may want to see also

Explore related products

![]()

Record Deposits: Add all deposits not yet credited by the bank to your records

Deposits made but not yet credited by the bank create a critical gap between your records and the bank’s statement. This discrepancy often stems from timing differences—checks or electronic transfers initiated but not processed by the bank’s cutoff date. Failing to account for these deposits leads to inaccurate reconciliation, potentially triggering overdrafts or misinformed financial decisions. Identifying and recording these pending deposits ensures your internal records reflect the true state of your finances, even if the bank hasn’t caught up.

To address this, begin by cross-referencing your deposit records with the bank statement. Highlight any deposits made after the statement’s closing date or those still in transit. For example, a $500 check deposited on the 28th of the month may not appear on a statement closing on the 25th. Add these unrecorded deposits to your bank statement balance before proceeding with reconciliation. This step bridges the temporal gap, aligning your records with actual account activity.

Practical tools like digital spreadsheets or accounting software streamline this process. Use color-coding or separate columns to distinguish pending deposits from credited ones. For businesses, ensure all departments (e.g., sales, accounting) sync deposit data to avoid omissions. Individuals should retain deposit slips or digital confirmations as proof. Regularly updating these records minimizes errors and provides a clear audit trail if discrepancies arise later.

A common pitfall is assuming electronic transfers post instantly. While ACH deposits typically clear within 1–3 business days, weekends, holidays, or bank-specific policies can delay processing. Similarly, mobile check deposits may take 2–5 days depending on the bank’s verification process. Understanding these timelines helps in accurately identifying which deposits require manual addition during reconciliation.

In conclusion, recording deposits not yet credited by the bank is a proactive step toward maintaining financial accuracy. By systematically identifying, documenting, and adding these transactions, you ensure your records remain reliable despite processing delays. This practice not only facilitates seamless reconciliation but also fosters confidence in your financial management, enabling informed decision-making based on a complete and current financial picture.

CRA in Banking: What It Stands For and Why It Matters

You may want to see also

Explore related products

![]()

Track Withdrawals: Subtract all withdrawals, including fees, checks, and debits, from your balance

Every withdrawal, no matter how small, chips away at your account balance. Tracking these deductions is a cornerstone of accurate bank reconciliation. This process involves meticulously subtracting all outgoing transactions from your recorded balance to ensure it aligns with the bank's statement.

Missed withdrawals, whether a forgotten ATM fee or an overlooked subscription debit, can lead to a distorted financial picture, potentially resulting in overdrafts and financial surprises.

Imagine your bank account as a reservoir. Every withdrawal, be it a check written for rent, a debit card purchase at the grocery store, or a monthly service fee, acts as a drain, reducing the water level. Just as you'd need to account for every outlet to know the true water level, you must account for every withdrawal to know your true account balance. This includes those easy-to-overlook automatic payments and recurring subscriptions that silently siphon funds.

Recognizing the cumulative effect of these seemingly minor deductions is crucial. A $5 daily coffee habit translates to $150 monthly, while a $10 monthly streaming service adds up to $120 annually.

The process is straightforward but demands diligence. Start by gathering all relevant documents: your bank statement, checkbook register, and any receipts or records of debit card transactions. Systematically go through each withdrawal, ensuring every check number, debit amount, and fee is accounted for. Double-check dates and amounts, as even a small discrepancy can throw off your reconciliation. Consider using a spreadsheet or financial software to streamline this process, allowing for easy sorting, filtering, and calculation.

Don't fall into the trap of assuming your memory or mental calculations are foolproof. A single overlooked withdrawal can lead to a snowball effect, making future reconciliations increasingly difficult. Treat each withdrawal with equal importance, regardless of its size. Remember, accuracy is paramount; a reconciled statement is only as reliable as the data it's based on. By meticulously tracking withdrawals, you gain a clear understanding of your spending habits and ensure your financial records reflect reality.

Understanding Bank Payoff Calculations: How Lenders Determine Your Final Amount

You may want to see also

Explore related products

![]()

Identify Outstanding Items: Note uncleared checks, pending deposits, or transactions not yet processed

Outstanding items are the discrepancies between your records and your bank statement, and they can significantly impact the accuracy of your reconciliation. These items fall into three main categories: uncleared checks, pending deposits, and unprocessed transactions. Each requires careful identification and handling to ensure your financial records remain precise.

Uncleared Checks: The Lingering Debits

Imagine writing a check for a large purchase, say $500, but it hasn't yet been cashed by the recipient. This creates a discrepancy: your checkbook balance reflects the deduction, but your bank statement doesn't. These uncleared checks represent future outflows that haven't materialized yet. To identify them, meticulously compare your check register with the cleared transactions on your bank statement. Note down any checks written but not yet appearing as debits.

Recognizing these outstanding checks is crucial for understanding your true available balance and avoiding potential overdrafts.

Pending Deposits: The Promised Inflows

Conversely, pending deposits represent money owed to you that hasn't yet hit your account. This could be a paycheck deposited on a Friday afternoon, which might not clear until the following Monday. Or perhaps a client's payment made electronically, awaiting processing by the bank. Scrutinize your deposit slips and online banking records for any transactions marked as "pending" or "in process." These represent future additions to your balance, and failing to account for them could lead to an inaccurate picture of your financial position.

Unprocessed Transactions: The Hidden Variables

Not all discrepancies are as straightforward as checks and deposits. Unprocessed transactions encompass a range of activities, from automatic bill payments scheduled for future dates to bank fees deducted at month-end. These can be trickier to identify, requiring a thorough review of your bank statement for any entries not reflected in your personal records. Look for recurring charges, subscription fees, or even ATM withdrawals that might have slipped your mind. By diligently tracking these unprocessed transactions, you gain a comprehensive understanding of your account activity and can anticipate future changes to your balance.

The Takeaway: A Proactive Approach

Identifying outstanding items isn't just about balancing numbers; it's about gaining control over your financial narrative. By meticulously noting uncleared checks, pending deposits, and unprocessed transactions, you transform your bank reconciliation from a reactive chore into a proactive tool for financial management. This awareness empowers you to make informed decisions, avoid surprises, and maintain a clear and accurate picture of your financial health.

Navigating Short Sales: A Step-by-Step Guide to Approaching Your Bank

You may want to see also

Explore related products

![]()

Reconcile Discrepancies: Investigate and correct any differences between your records and the bank statement

Discrepancies between your records and a bank statement aren’t uncommon, but they require prompt attention to maintain financial accuracy. Start by comparing every transaction listed on both documents, noting any differences in amounts, dates, or missing entries. Common culprits include uncleared checks, pending deposits, bank fees, or automatic deductions you might have overlooked. Highlight these variances clearly to avoid confusion during the investigation phase.

Once discrepancies are identified, investigate systematically. For uncleared checks or deposits, verify the dates and confirm if the transactions are still in process. Contact the bank to inquire about any fees or charges you don’t recognize, as these can sometimes be errors or unauthorized activities. Cross-reference your accounting software or ledger to ensure no data entry mistakes, such as transposed numbers or omitted transactions. If a discrepancy persists, gather supporting documents like receipts or invoices to substantiate your records.

Correcting discrepancies involves updating your records or disputing errors with the bank. If the mistake is on your end, adjust your ledger or accounting software to match the bank statement. For bank errors, submit a formal dispute with evidence, such as proof of a deposit or incorrect fee. Keep a detailed log of all communications and actions taken during this process. For recurring issues, consider implementing safeguards like double-checking entries or using automated reconciliation tools to minimize future errors.

A proactive approach to reconciling discrepancies not only ensures financial accuracy but also builds trust in your financial management. Regularly reviewing statements and addressing inconsistencies promptly can prevent small errors from escalating into larger problems. Treat each discrepancy as an opportunity to refine your processes, whether by improving record-keeping habits or enhancing communication with your financial institution. By doing so, you’ll maintain a clear and reliable financial picture.

Currency Exchange at Bank of Scotland: What You Need to Know

You may want to see also

Frequently asked questions

The first step is to gather all necessary documents, including your bank statement, check register, deposit slips, and any other records of transactions.

Compare your records with the bank statement, noting any transactions that appear on one but not the other, such as outstanding checks, deposits in transit, or bank fees.

Contact your bank immediately to report the error and provide documentation to support your claim. Follow up until the issue is resolved.

It’s best to reconcile your bank statement monthly to ensure accuracy, catch errors early, and maintain proper financial records.

Outstanding checks are those you’ve written but haven’t cleared the bank yet, while deposits in transit are deposits made but not yet reflected on the statement. Adjust your balance by subtracting outstanding checks and adding deposits in transit to reconcile accurately.