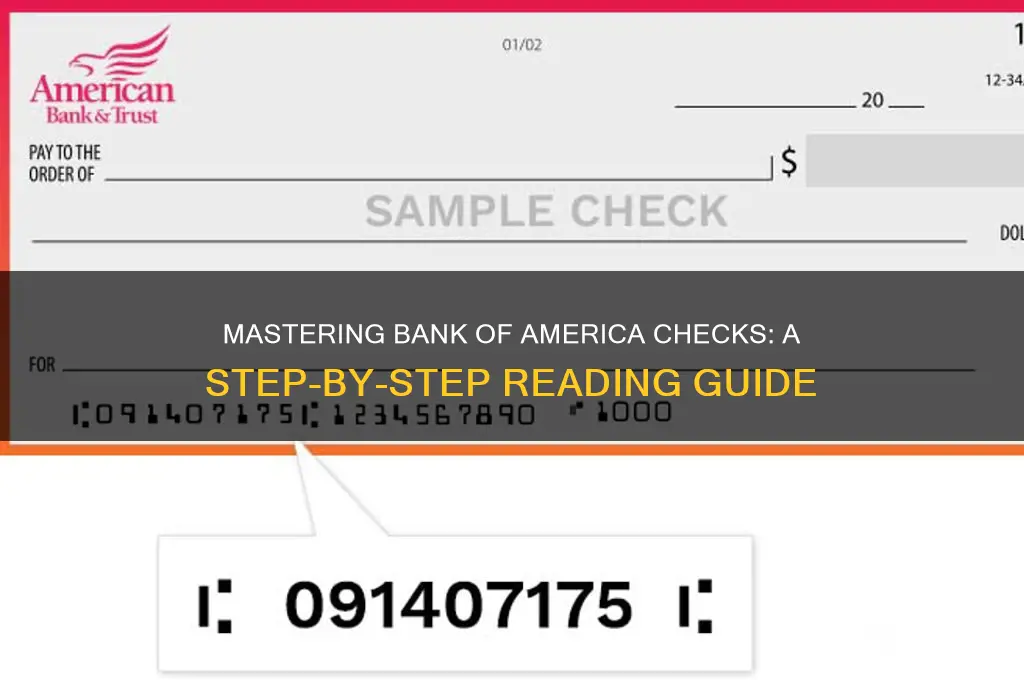

Reading a Bank of America check is a straightforward process once you understand the key components. The check typically includes the payer’s name and address in the top left corner, followed by the check number in the upper right. Below this, you’ll find the date line, where the check writer specifies the date of issuance. The payee’s name is written on the line labeled Pay to the Order of, while the numerical amount is indicated in the box to the right. Below this, the amount is spelled out in words, followed by a fraction line to prevent alterations. The bottom of the check contains the bank’s routing number, account number, and check number, printed in MICR (Magnetic Ink Character Recognition) font for easy processing. Familiarizing yourself with these elements ensures accurate handling and verification of the check.

Explore related products

What You'll Learn

- Understanding Check Components: Identify key elements like date, payee, amount, signature, and memo lines

- Verifying Check Authenticity: Check for security features, watermarks, and microprinting to prevent fraud

- Reading Numerical Amounts: Ensure written and numerical amounts match to avoid discrepancies

- Endorsing the Check: Sign the back correctly for deposit or cashing purposes

- Handling Check Errors: Learn how to address mistakes like incorrect dates or missing signatures

![]()

Understanding Check Components: Identify key elements like date, payee, amount, signature, and memo lines

A Bank of America check, like any standard check, is a compact document brimming with essential information. Each component serves a specific purpose, ensuring clarity, security, and legal validity. To decipher its contents accurately, start by locating the date in the upper right corner. This field indicates when the check was written and establishes the timeframe for its validity. Banks typically honor checks within six months of the date; beyond that, they may be refused. Always verify the date aligns with the intended transaction period to avoid complications.

Next, identify the payee line, usually found below the date. This is where the recipient’s name is written, determining who can legally deposit or cash the check. Precision is critical here—misspellings or incomplete names can render the check unusable. For example, if the payee is a business, ensure the full legal name is used, not a shortened version. Double-checking this field prevents delays or rejections during processing.

The amount section is arguably the most critical part of the check, appearing in two places: numerically in a designated box and written out in words on the adjacent line. Both must match exactly; discrepancies can lead to rejection or fraud. For instance, if the check is for $123.45, write “123.45” in the box and “One Hundred Twenty-Three and 45/100” on the line. This redundancy ensures accuracy and provides a safeguard against tampering.

The signature line, located at the bottom right, is the check writer’s authorization for the transaction. A missing or mismatched signature invalidates the check, as it confirms the account holder’s consent. Always sign in ink, using the same signature on file with the bank. For added security, consider using a unique signature style that’s difficult to replicate but consistent enough for verification.

Finally, the memo line is optional but highly useful. This field allows you to note the purpose of the check, such as “Rent for January” or “Invoice #12345.” While it doesn’t affect the check’s validity, it provides context for both the payer and payee, aiding in record-keeping and dispute resolution. Think of it as a mini-ledger entry that simplifies financial tracking.

By mastering these components—date, payee, amount, signature, and memo—you’ll navigate Bank of America checks with confidence, ensuring every transaction is accurate, secure, and hassle-free.

Are Dollar Coins Still Available at Banks? What You Need to Know

You may want to see also

Explore related products

![]()

Verifying Check Authenticity: Check for security features, watermarks, and microprinting to prevent fraud

Bank of America checks incorporate advanced security features to deter fraud, but these measures are only effective if you know how to verify them. Start by examining the check under a bright light to detect watermarks, which are subtle designs embedded in the paper. Authentic Bank of America checks often feature a faint watermark of the bank’s logo or name. Tilt the check at different angles to observe color-shifting ink, typically used in the dollar amount or signature line, which changes hue depending on the viewing angle. These features are difficult to replicate and serve as a primary indicator of authenticity.

Microprinting is another critical security element to inspect. Genuine checks often include tiny, precise text in areas like the border or signature line, which appears as a solid line to the naked eye but reveals clear, legible characters under magnification. Counterfeit checks may omit this detail or produce blurry, inconsistent microprint. To test this, use a magnifying glass or the zoom function on your smartphone camera to scrutinize these areas. If the microprint is missing or poorly executed, the check is likely fraudulent.

Watermarks and security threads are additional layers of protection. Hold the check up to light to look for a security thread, a thin ribbon embedded in the paper that spells out "Bank of America" or includes a repeating pattern. This thread is invisible when the check is flat on a surface but becomes visible when backlit. Similarly, authentic checks often have a watermark that can only be seen when held at an angle to light. Counterfeit checks may lack these features or include poorly executed imitations, such as uneven threads or smudged watermarks.

Practical tips for verification include comparing the check to a known authentic sample, if available, and checking for inconsistencies in font, spacing, or alignment. Fraudulent checks often exhibit slight discrepancies in these areas due to the limitations of counterfeit printing methods. Additionally, verify the check’s details against the issuer’s account information, such as the account number and bank routing number, using official Bank of America resources. If in doubt, contact the bank directly to confirm the check’s validity before accepting it.

In conclusion, verifying the authenticity of a Bank of America check requires a systematic approach to inspecting security features, watermarks, and microprinting. By familiarizing yourself with these elements and employing tools like magnification and light sources, you can significantly reduce the risk of falling victim to check fraud. Vigilance and attention to detail are key to protecting yourself and your finances in an increasingly sophisticated fraud landscape.

Vanguard Bank Verification Process: Understanding the Timeline for Account Approval

You may want to see also

Explore related products

![Ultimate Guide To Reality Checks: Your Roadmap To Using Reality Checks For Lucid Dreaming [Lucid Dream Book By The Creator Of How To Lucid]](https://m.media-amazon.com/images/I/719ZZxFmbcL._AC_UL320_.jpg)

![]()

Reading Numerical Amounts: Ensure written and numerical amounts match to avoid discrepancies

A single discrepancy between the written and numerical amounts on a Bank of America check can lead to payment delays, rejections, or even fraud. This critical detail often goes overlooked, yet it’s the linchpin of check validity. For instance, if the written amount says "One Hundred Fifty Dollars and 00/100" but the numerical box reads "$15.00," the check becomes ambiguous and may be flagged by the bank’s processing system. Always double-check both fields to ensure they align precisely, as even a minor typo can trigger complications.

The process of verifying these amounts isn’t just about accuracy—it’s about protecting your finances. Fraudsters often exploit mismatches to alter checks post-issuance. For example, a check with "Fifty Dollars" written out but "$5,000.00" in the numerical field could be manipulated if the payee notices the discrepancy and chooses to exploit it. To prevent this, use clear, legible handwriting and ensure the numerical amount is written firmly, with no extra spaces that could allow digits to be added.

Consider this practical tip: After writing the amount in words, draw a line from the last word to the edge of the line to prevent additional words from being inserted. For instance, if you write "Seventy-Five Dollars and 00/100," draw a straight line after "100" to fill the remaining space. Similarly, when filling the numerical box, start the amount at the far left to deter tampering. These small precautions take seconds but significantly reduce the risk of fraud or processing errors.

Banks, including Bank of America, prioritize the numerical amount when discrepancies arise, but this doesn’t absolve you of responsibility. If the written amount is higher, the bank will still honor the numerical value, potentially leaving you shortchanged. Conversely, if the written amount is lower, you could face overdraft fees or legal issues for issuing a bad check. The takeaway? Consistency between both formats isn’t just a formality—it’s a safeguard for your financial integrity.

Finally, educate anyone who handles checks on your behalf—employees, family members, or assistants—about this critical step. A shared understanding of the importance of matching amounts can prevent costly mistakes. Keep a checklist handy: write the amount in words, print the numerical amount clearly, and verify both before signing. This simple routine ensures your checks are processed smoothly and securely, every time.

SoFi's Banking Journey: Tracing Its Evolution as a Financial Institution

You may want to see also

Explore related products

![]()

Endorsing the Check: Sign the back correctly for deposit or cashing purposes

Endorsing a check is a critical step in ensuring it can be deposited or cashed, and Bank of America checks are no exception. The back of the check contains a designated area for your signature, but the way you sign it depends on your intentions. A simple signature suffices if you’re depositing the check into your own account, but additional wording is required for third-party deposits or cashing. For instance, writing "For Deposit Only" followed by your account number ensures the funds go directly into your account, reducing the risk of fraud.

Consider the scenario where you’re endorsing a check for someone else to deposit. In this case, you’ll need to sign the check and add the phrase "Pay to the Order of" followed by the recipient’s name. This type of endorsement, known as a special endorsement, transfers the check’s value to the specified individual. However, be cautious: once endorsed this way, the check can be further endorsed by the recipient, potentially leading to unintended consequences if it falls into the wrong hands.

For cashing purposes, a blank endorsement—your signature alone—is typically sufficient. Yet, this method carries significant risk. A blank endorsement makes the check payable to anyone who presents it, akin to carrying cash. If the check is lost or stolen, the funds could be claimed by someone else. To mitigate this, consider using a restrictive endorsement like "For Deposit Only" or "For Mobile Deposit Only," which limits the check’s use to a specific purpose.

Practical tips can streamline the endorsement process. Always sign the check in permanent ink and ensure your signature matches the one on file with your bank to avoid processing delays. If endorsing for a minor or someone with limited access to banking, include their account number to ensure seamless deposit. Lastly, double-check the endorsement area for any pre-printed instructions from the issuer, as these may dictate specific requirements for processing.

In conclusion, endorsing a Bank of America check correctly hinges on understanding your intent and the associated risks. Whether depositing, cashing, or transferring funds, the right endorsement safeguards your money and ensures compliance with banking procedures. By mastering these nuances, you’ll navigate check transactions with confidence and efficiency.

Claymont Delaware Food Bank: Availability and Community Support Explored

You may want to see also

Explore related products

![]()

Handling Check Errors: Learn how to address mistakes like incorrect dates or missing signatures

Checks, despite their declining use, remain a vital financial tool, and errors on them can cause significant headaches. A misplaced decimal, an incorrect date, or a forgotten signature can render a check invalid, delaying payments and creating unnecessary stress. Understanding how to identify and rectify these mistakes is crucial for anyone who still relies on this traditional payment method.

For instance, a check with an incorrect date, even if just a day off, may be rejected by the bank. Similarly, a missing signature is a glaring red flag, as it compromises the security and authenticity of the transaction.

Addressing these errors requires a methodical approach. Start by carefully reviewing the check for any discrepancies. Dates should be written clearly and match the current date or a future date if post-dated. Ensure the numerical and written amounts match exactly; a discrepancy, no matter how small, will invalidate the check. The signature line, often overlooked in haste, is non-negotiable. A missing signature renders the check worthless.

If you spot an error, don't panic. Most mistakes can be rectified. For minor errors like incorrect dates or amounts, you can carefully draw a single line through the mistake and write the correct information above it, initialing the change. However, this method should be used sparingly and only for minor corrections.

For more significant errors, such as a missing signature or a completely incorrect payee name, it's best to void the check entirely. Write "VOID" across the front in large, clear letters. This prevents the check from being cashed fraudulently. Then, simply issue a new check with the correct information. Remember, it's always better to be safe than sorry when dealing with financial transactions.

While check errors can be frustrating, they are usually avoidable with careful attention to detail. Double-checking all information before signing and dating the check is a simple yet effective preventative measure. Keeping a record of issued checks, including dates, amounts, and payees, can also help identify errors quickly and efficiently. By understanding how to handle check errors, you can ensure smooth and secure financial transactions, even in an increasingly digital world.

Unlocking Academic Success: Strategies to Locate Your School Test Banks

You may want to see also

Frequently asked questions

The date is written in the top right corner of the check. It indicates when the check was written and is an essential detail for processing.

The routing number is the first 9-digit number at the bottom left corner of the check. It identifies the bank and is crucial for electronic transactions.

The account number is the second set of numbers at the bottom of the check, located between the routing number and the check number. It is typically 10–12 digits long.