Understanding how to read a bank's Uniform Bank Performance Report (UBPR) is essential for assessing a financial institution's health, performance, and risk profile. The UBPR is a standardized report generated by the Federal Financial Institutions Examination Council (FFIEC), providing a comprehensive snapshot of a bank's financial condition, including key metrics such as asset quality, capital adequacy, earnings, liquidity, and sensitivity to market risk. By analyzing the UBPR, stakeholders, including investors, regulators, and bank management, can evaluate a bank's efficiency, profitability, and compliance with regulatory standards. Familiarizing oneself with the report's structure, ratios, and benchmarks is crucial for interpreting the data accurately and making informed decisions about the bank's stability and future prospects.

What You'll Learn

- Understanding UBPR Basics: Key sections, purpose, and how to access the report

- Analyzing Financial Condition: Assets, liabilities, equity, and capital adequacy ratios

- Evaluating Performance Ratios: ROA, ROE, net interest margin, and efficiency metrics

- Assessing Risk Metrics: Loan quality, liquidity, and sensitivity to market risks

- Comparing Peer Data: Benchmarking against similar banks for contextual insights

![]()

Understanding UBPR Basics: Key sections, purpose, and how to access the report

The Uniform Bank Performance Report (UBPR) is a critical tool for analyzing a bank's financial health, but its value lies in understanding its structure. This quarterly report, spanning four pages, is divided into key sections: Income Statement, Balance Sheet, Ratios, and Peer Group Comparisons. Each section serves a distinct purpose, from detailing revenue and expenses to benchmarking performance against similar institutions. Knowing where to look within these sections is the first step to unlocking the UBPR's insights.

Accessing the UBPR is straightforward but requires knowing where to look. The report is publicly available through the Federal Financial Institutions Examination Council (FFIEC) website, a centralized hub for bank regulatory data. To retrieve a specific bank’s UBPR, you’ll need its unique FDIC certificate number or institution name. Once located, the report can be downloaded in PDF or spreadsheet format, allowing for both readability and data manipulation. This accessibility ensures that investors, analysts, and regulators alike can scrutinize a bank’s performance with ease.

While the UBPR is comprehensive, its true power lies in the Ratios section, which distills complex financial data into actionable metrics. Key ratios like Return on Assets (ROA), Net Interest Margin (NIM), and Efficiency Ratio provide a snapshot of profitability, asset utilization, and operational efficiency. For instance, an ROA below the peer group average may signal underperformance, while a high Efficiency Ratio could indicate bloated expenses. These ratios are not just numbers—they are diagnostic tools that highlight areas of strength or weakness.

A common pitfall when reading a UBPR is overlooking the Peer Group Comparisons. These comparisons contextualize a bank’s performance by benchmarking it against institutions of similar size, location, and business model. For example, a small community bank’s NIM might appear low in isolation but could be competitive when compared to peers. Ignoring this context can lead to misinterpretations, so always cross-reference with peer data to gain a balanced perspective.

In conclusion, mastering the UBPR begins with familiarity of its key sections and purpose. By focusing on the Income Statement, Balance Sheet, Ratios, and Peer Group Comparisons, readers can extract meaningful insights into a bank’s financial condition. Coupled with easy access via the FFIEC website, the UBPR becomes an indispensable resource for anyone evaluating bank performance. Remember: the report’s value is not in its data alone but in the story those numbers tell when analyzed thoughtfully.

Mastering Piggy Bank Slot Machine: Tips, Tricks, and Winning Strategies

You may want to see also

![]()

Analyzing Financial Condition: Assets, liabilities, equity, and capital adequacy ratios

A bank's Uniform Bank Performance Report (UBPR) is a treasure trove of data, but deciphering its financial health requires a focused lens on assets, liabilities, equity, and capital adequacy ratios. These elements paint a picture of a bank's stability, risk exposure, and ability to weather economic storms.

Think of assets as the bank's toolbox. Loans, investments, and cash reserves are its primary tools for generating income. Analyzing the composition of assets reveals the bank's risk appetite. A high concentration in risky loans, for example, could signal potential vulnerabilities.

Liabilities, on the other hand, represent the bank's obligations. Deposits, borrowings, and other debts are the fuel that powers its operations. A healthy bank maintains a balanced mix of liabilities, avoiding over-reliance on volatile funding sources like short-term borrowings.

Equitable distribution of wealth is key, even for banks. Equity represents the owners' stake and acts as a buffer against losses. A strong equity base indicates resilience and the ability to absorb shocks.

Capital adequacy ratios tie these elements together. Ratios like Tier 1 Capital Ratio and Total Capital Ratio measure a bank's capital relative to its risk-weighted assets. Regulators set minimum thresholds for these ratios, ensuring banks hold sufficient capital to absorb losses and maintain stability.

Imagine a bank with a high proportion of risky loans, funded largely by short-term borrowings, and a thin equity cushion. This combination would raise red flags, suggesting potential liquidity and solvency risks. Conversely, a bank with a diversified asset portfolio, stable funding sources, and robust equity would be viewed as financially sound.

By scrutinizing assets, liabilities, equity, and capital adequacy ratios within the UBPR, investors, regulators, and even depositors can gain valuable insights into a bank's financial condition, its risk profile, and its ability to navigate the ever-changing financial landscape.

Building Societies vs Banks: Which is Safer?

You may want to see also

![]()

Evaluating Performance Ratios: ROA, ROE, net interest margin, and efficiency metrics

A bank's Uniform Bank Performance Report (UBPR) is a treasure trove of financial insights, but deciphering its performance ratios requires a keen eye. Among the most critical metrics are Return on Assets (ROA), Return on Equity (ROE), Net Interest Margin (NIM), and efficiency ratios. These figures paint a vivid picture of a bank's profitability, risk management, and operational effectiveness. For instance, a bank with an ROA above 1% is generally considered healthy, while an ROE exceeding 10% suggests robust returns for shareholders. However, these benchmarks are not one-size-fits-all; they must be contextualized within the bank's size, market, and economic environment.

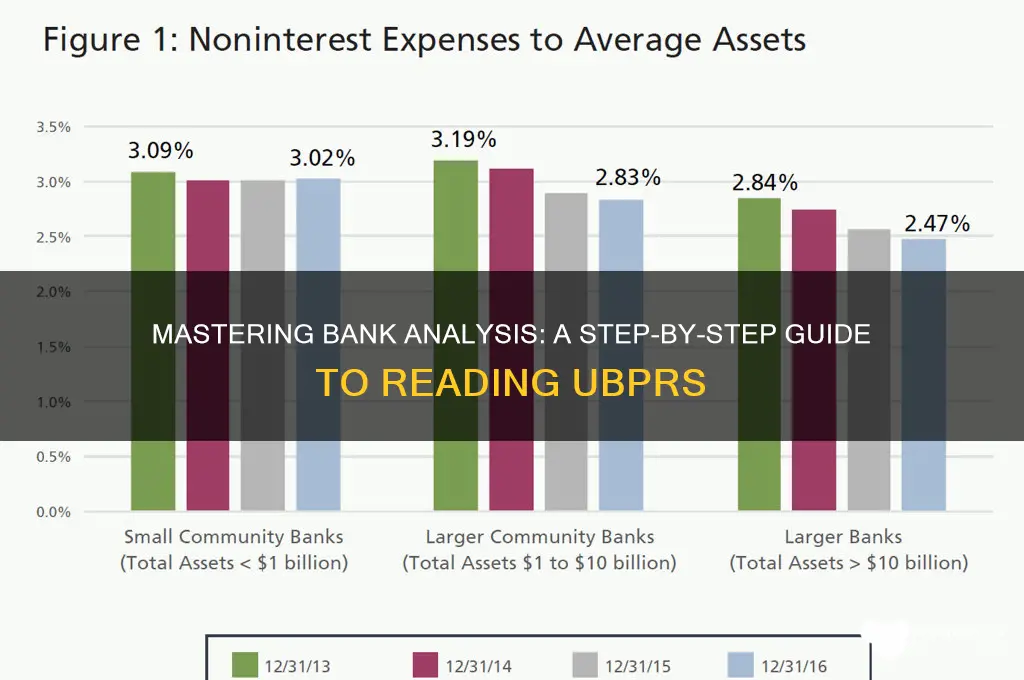

To evaluate these ratios effectively, start by comparing them to industry averages and the bank's historical performance. A declining NIM, for example, could signal increasing funding costs or shrinking loan spreads, warranting a closer look at the bank's interest-earning assets and liabilities. Efficiency ratios, calculated as non-interest expenses divided by revenue, should ideally fall below 60%. A higher ratio may indicate bloated operational costs or underperforming revenue streams. Practical tip: Use peer group comparisons to identify whether the bank’s inefficiencies are systemic or unique to its operations.

While ROA and ROE are often analyzed together, they reveal distinct aspects of performance. ROA measures how efficiently a bank uses its assets to generate profit, while ROE focuses on profitability relative to shareholders’ equity. A bank with high ROE but low ROA may be leveraging excessive debt, which could amplify risk. Conversely, a high ROA with moderate ROE suggests prudent asset utilization without over-reliance on leverage. Caution: Avoid interpreting these ratios in isolation; cross-reference them with capital adequacy and risk-weighted asset metrics for a balanced view.

Net Interest Margin (NIM) is the lifeblood of a bank’s profitability, representing the difference between interest income and interest expense. A widening NIM typically indicates favorable lending conditions or effective interest rate management. However, in a low-rate environment, banks may struggle to maintain NIM, prompting them to seek higher-yielding but riskier assets. Example: A regional bank with a NIM of 3.5% in a rising rate environment might outperform its peers by strategically adjusting its loan portfolio toward variable-rate products.

Finally, efficiency metrics, such as the efficiency ratio or operating leverage, provide a lens into a bank’s cost management. A bank with a low efficiency ratio is better at converting revenue into profit, often through streamlined operations or technology investments. Takeaway: Focus on trends rather than snapshots. A bank consistently improving its efficiency ratio over time is likely investing in sustainable growth, whereas sudden spikes could indicate temporary cost-cutting measures or revenue declines. By mastering these performance ratios, you can uncover the true financial health and strategic direction of any bank.

Shipping Cars: Hawaii Banks and Your Options

You may want to see also

![]()

Assessing Risk Metrics: Loan quality, liquidity, and sensitivity to market risks

A bank's Uniform Bank Performance Report (UBPR) is a treasure trove of data for assessing risk metrics, particularly in the areas of loan quality, liquidity, and sensitivity to market risks. To begin, examine the loan portfolio quality by looking at the ratio of non-performing loans to total loans. This ratio, found in the UBPR under the asset quality section, should ideally be below 2% for a healthy bank. For instance, a ratio of 1.5% indicates that only 1.5% of the bank's loans are non-performing, which is a positive sign. However, a ratio above 5% may signal potential issues with the bank's lending practices or economic stress in the bank's operating region.

When evaluating liquidity, focus on the bank's liquidity coverage ratio (LCR) and net stable funding ratio (NSFR), which are critical in ensuring the bank can meet its short-term obligations. The LCR, typically expressed as a percentage, measures the bank's high-quality liquid assets against its total net cash outflows over a 30-day stress period. A healthy bank should maintain an LCR above 100%, indicating sufficient liquidity to cover short-term needs. For example, an LCR of 120% suggests the bank has 20% more liquid assets than required, providing a buffer against unexpected liquidity demands.

Sensitivity to market risks, particularly interest rate risk, can be assessed by analyzing the bank's earnings and economic value sensitivity to changes in interest rates. The UBPR provides metrics such as the cumulative gap and the duration gap, which help in understanding how the bank’s earnings and economic value might be affected by interest rate fluctuations. For instance, a positive cumulative gap indicates that the bank’s assets will reprice faster than its liabilities in a rising interest rate environment, potentially boosting net interest income. Conversely, a negative gap suggests vulnerability to margin compression.

To practically apply these insights, consider a scenario where a bank has a high concentration of fixed-rate loans and a significant reliance on short-term deposits. In a rising interest rate environment, the bank’s funding costs could increase rapidly while its loan income remains static, squeezing profitability. To mitigate this risk, banks often use hedging strategies, such as interest rate swaps, or adjust their asset-liability mix. For investors or analysts, tracking these metrics over multiple reporting periods can reveal trends and potential red flags, such as a consistent decline in loan quality or increasing liquidity pressures.

In conclusion, assessing risk metrics through the UBPR requires a detailed examination of loan quality, liquidity, and sensitivity to market risks. By focusing on specific ratios and gaps, stakeholders can gain a nuanced understanding of a bank’s risk profile. For example, a bank with a low non-performing loan ratio, a robust LCR, and a well-managed cumulative gap is likely better positioned to weather economic uncertainties. Conversely, deviations from healthy benchmarks should prompt deeper investigation into the bank’s risk management practices and strategic decisions. This analytical approach transforms raw data into actionable insights, enabling informed decision-making in banking and investment contexts.

Positive Pay: A Secure Banking Solution

You may want to see also

![]()

Comparing Peer Data: Benchmarking against similar banks for contextual insights

Bank performance doesn’t exist in a vacuum. Understanding how a bank stacks up against its peers is crucial for meaningful analysis. This is where benchmarking using UBPR data shines. By comparing key ratios and metrics to similar institutions, you gain context, identify areas of strength and weakness, and make informed decisions.

Imagine analyzing a bank's return on assets (ROA) in isolation. A 1% ROA might seem decent, but without context, it's meaningless. Benchmarking reveals if this ROA is impressive within its peer group or lagging behind.

Identifying Peer Groups: Precision is Key

Not all banks are created equal. Effective benchmarking requires defining a relevant peer group. Consider factors like asset size, geographic location, business model (commercial, community, credit union), and loan portfolio composition. The FFIEC provides peer group classifications within the UBPR, but further refinement might be necessary. For instance, comparing a rural community bank heavily invested in agricultural loans to a large urban commercial bank focused on corporate lending would be misleading.

Aim for a peer group of 10-20 banks for statistical significance while maintaining homogeneity.

Key Metrics for Benchmarking: Beyond the Basics

While traditional ratios like ROA, ROE, and net interest margin are essential, delve deeper into UBPR data for a comprehensive comparison. Analyze:

- Asset Quality: Non-performing loan ratios, loan loss reserves, and charge-offs reveal risk management practices and potential vulnerabilities.

- Liquidity: Liquidity coverage ratio and loan-to-deposit ratio indicate a bank's ability to meet short-term obligations.

- Efficiency: Efficiency ratio (non-interest expense/revenue) highlights operational effectiveness.

- Capital Adequacy: Tier 1 leverage ratio and total risk-based capital ratio assess a bank's financial strength and resilience.

Cautions and Considerations: Avoiding Misleading Comparisons

Benchmarking is a powerful tool, but it requires careful interpretation. Be mindful of:

- Outliers: A single bank with extreme values can skew averages. Consider using median values for a more robust comparison.

- Temporal Fluctuations: Economic cycles and market conditions can significantly impact performance. Compare data over multiple periods to identify trends.

- Strategic Differences: Banks may have distinct business strategies. A bank focusing on high-risk, high-reward loans might exhibit different metrics than a conservative lender.

Comparing UBPR data against peers transforms raw numbers into actionable insights. It allows stakeholders to:

- Identify areas for improvement: Pinpoint weaknesses relative to competitors and develop targeted strategies.

- Validate strengths: Confirm areas of competitive advantage and build upon them.

- Make informed investment decisions: Assess a bank's relative performance and potential for growth.

- Monitor industry trends: Track changes in the banking landscape and adapt strategies accordingly.

By leveraging benchmarking effectively, UBPR data becomes a powerful tool for understanding a bank's position within its competitive environment and driving informed decision-making.

Step-by-Step Guide to Activating Axis Bank Internet Banking Easily

You may want to see also

Frequently asked questions

A UBPR (Uniform Bank Performance Report) is a standardized report generated by the Federal Financial Institutions Examination Council (FFIEC) that provides detailed financial and performance data for individual banks. It is important because it helps stakeholders, including regulators, investors, and bank management, assess a bank's financial health, risk profile, and operational efficiency.

You can find a bank's UBPR on the FFIEC's website under the "Uniform Bank Performance Report" section. It is typically updated quarterly, reflecting the bank's financial data as of the end of each quarter.

Key metrics to focus on include the Texas Ratio (non-performing assets to equity and reserves), net interest margin (NIM), return on assets (ROA), return on equity (ROE), and capital adequacy ratios (e.g., Tier 1 leverage ratio). These metrics provide insights into asset quality, profitability, and capital strength.