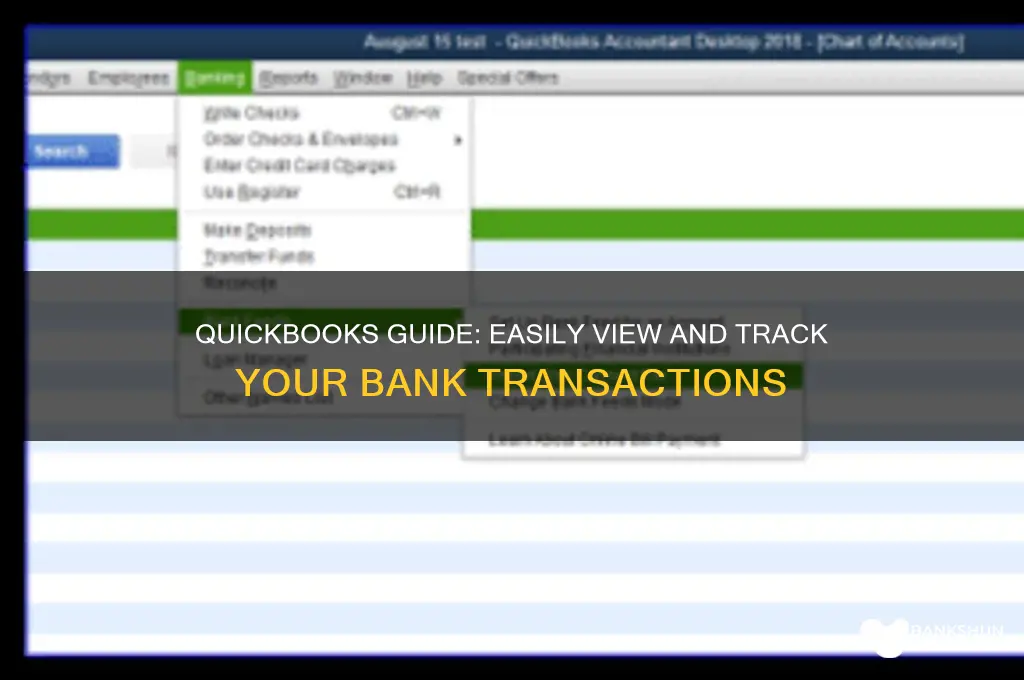

Navigating bank transactions in QuickBooks is essential for maintaining accurate financial records and ensuring seamless reconciliation. To view your bank transactions, start by logging into your QuickBooks account and accessing the Banking menu. From there, select the specific bank account you wish to review, and QuickBooks will display a list of recent transactions synced from your linked bank account. You can filter, categorize, and match these transactions to your records, ensuring everything is up-to-date. Additionally, QuickBooks allows you to manually add or edit transactions if needed, providing a comprehensive overview of your financial activities. This process simplifies tracking expenses, income, and cash flow, making it a vital tool for effective financial management.

Explore related products

What You'll Learn

![]()

Linking Bank Accounts to QuickBooks

Linking your bank accounts to QuickBooks is the first step toward seamless transaction tracking and financial management. By establishing this connection, you enable QuickBooks to automatically import and categorize transactions, saving you hours of manual data entry. This integration not only ensures accuracy but also provides real-time insights into your cash flow, helping you make informed business decisions. Whether you’re using QuickBooks Online or Desktop, the process is straightforward, though the steps may vary slightly depending on your version.

To begin linking your bank account, log in to your QuickBooks account and navigate to the "Banking" or "Transactions" tab. From there, select "Add Account" and search for your bank from the list of supported institutions. You’ll be prompted to enter your bank’s login credentials to securely connect the accounts. QuickBooks uses encryption to protect your data, so your financial information remains safe. Once connected, QuickBooks will start downloading recent transactions, typically up to 90 days’ worth, depending on your bank’s policies.

While linking accounts is generally smooth, occasional challenges may arise. For instance, some banks require multi-factor authentication, which QuickBooks supports but may require additional steps. If your bank isn’t listed, you can manually upload transactions via CSV or Excel files, though this method lacks automation. Another common issue is duplicate transactions, which can occur if you reconnect an account or if your bank sends data in batches. QuickBooks provides tools to identify and merge duplicates, ensuring your records remain clean.

A key benefit of linking bank accounts is the ability to reconcile transactions effortlessly. QuickBooks automatically matches downloaded transactions with existing entries in your books, flagging any discrepancies for review. This feature is particularly useful during month-end closings, as it reduces the risk of errors and ensures your financial statements are accurate. Additionally, linked accounts enable features like cash flow forecasting and expense tracking, which are invaluable for small businesses and freelancers.

In conclusion, linking bank accounts to QuickBooks is a game-changer for efficient financial management. It streamlines transaction tracking, enhances accuracy, and provides actionable insights into your business’s financial health. By following the simple steps outlined by QuickBooks and addressing potential challenges proactively, you can maximize the benefits of this integration. Whether you’re a seasoned QuickBooks user or new to the platform, this feature is essential for maintaining organized and up-to-date financial records.

Delinking Aadhaar from IDBI Bank: A Step-by-Step Guide

You may want to see also

Explore related products

$49

![]()

Reconciling Transactions in QuickBooks

Once you’ve entered the statement details, QuickBooks displays a list of transactions for the selected period. Here’s where the real work begins: mark each transaction in QuickBooks that also appears on your bank statement. This step requires attention to detail, as unmatched transactions could indicate errors, such as missed entries or duplicates. For instance, if a $500 deposit is on your statement but not in QuickBooks, you’ll need to investigate whether it was overlooked or incorrectly categorized. QuickBooks simplifies this by allowing you to filter transactions by date, amount, or type, making it easier to spot discrepancies.

A common challenge during reconciliation is handling uncleared transactions—those recorded in QuickBooks but not yet reflected on your bank statement. These often include outstanding checks or deposits in transit. QuickBooks provides a dedicated section for these transactions, allowing you to exclude them from the reconciliation process temporarily. However, it’s crucial to monitor these regularly; transactions older than 30 days may warrant further investigation to ensure they aren’t lost or misrecorded.

To streamline future reconciliations, consider these practical tips: first, reconcile accounts monthly to catch discrepancies early. Second, use QuickBooks’ Match feature to automatically pair transactions with similar amounts and dates, reducing manual effort. Finally, leverage the Reconciliation Discrepancy Report to identify and resolve unmatched transactions efficiently. By adopting these practices, you’ll not only maintain accurate records but also save time and reduce stress during the reconciliation process.

In conclusion, reconciling transactions in QuickBooks is more than a routine task—it’s a safeguard for your financial integrity. By following these steps and leveraging QuickBooks’ tools, you can ensure your books remain accurate and up-to-date. Remember, consistency is key; regular reconciliation transforms a potentially daunting task into a manageable, even automated, part of your financial workflow.

Crafting a Creative Book Shaped Bank: DIY Guide for Beginners

You may want to see also

Explore related products

$90

![]()

Filtering and Sorting Transactions

QuickBooks' filtering and sorting tools are your secret weapon for taming the transaction jungle. Imagine sifting through hundreds of entries to find that one elusive coffee shop charge from last Tuesday. Without filters, it's like searching for a needle in a haystack. But with a few clicks, you can isolate transactions by date range, amount, payee, or even specific keywords in the memo field. Need to see all transactions over $100? Done. Want to review only deposits from a particular client? Easy. This level of granularity transforms a chaotic list into a manageable, actionable dataset.

Let's say you're reconciling your business account and need to match QuickBooks transactions with your bank statement. Start by sorting transactions chronologically, ensuring they align with the statement's order. Then, apply filters to highlight uncleared transactions or those with discrepancies. For instance, filter for amounts between $50 and $100 to spot potential errors or missing entries. This methodical approach not only speeds up reconciliation but also minimizes the risk of overlooking critical details.

But filtering isn't just about finding what you're looking for—it's also about excluding what you're not. Suppose you're analyzing monthly expenses but want to exclude transfers between accounts. Use the "Exclude" filter to remove these entries, providing a clearer picture of actual spending. Similarly, if you're tracking income from a specific service, filter out unrelated revenue streams to focus solely on relevant data. This targeted approach ensures your analysis is precise and actionable.

A pro tip: combine sorting and filtering for maximum efficiency. For example, sort transactions by date and then filter for a specific payee to track payments over time. Or sort by amount and filter for a particular category to identify your largest expenses. This dual approach allows you to slice and dice your data in ways that reveal trends, anomalies, or opportunities for optimization. Mastering these tools turns QuickBooks from a mere record-keeper into a powerful financial analyst.

Finally, don't overlook the "Save Custom Filter" feature—a time-saver for recurring tasks. If you frequently review transactions for a specific client or expense category, save your filter settings for one-click access in the future. This not only streamlines your workflow but also ensures consistency in your reporting. By leveraging filtering and sorting effectively, you transform QuickBooks into a dynamic tool that adapts to your unique financial needs, making transaction management less of a chore and more of a strategic advantage.

Boost Your SpotMe Limit: A Guide to CHIM Bank Strategies

You may want to see also

Explore related products

![]()

Identifying Unmatched Transactions

Unmatched transactions in QuickBooks can disrupt your financial accuracy, but identifying them is the first step to resolving discrepancies. Start by navigating to the Banking tab and selecting Banking from the left menu. Here, you’ll see a list of transactions downloaded from your bank. QuickBooks automatically matches these with existing entries in your register, but some may remain unmatched due to differences in dates, amounts, or payees. To spot these, look for transactions without a checkmark in the Matched column or those highlighted in blue, indicating they’re new and unmatched.

Analyzing unmatched transactions requires a systematic approach. Begin by comparing the transaction details in QuickBooks with your bank statement. Pay attention to rounding differences, split transactions, or manual entries that might not align perfectly. For example, a $25.99 purchase might appear as $26 in QuickBooks due to rounding. Use the Find Unmatched feature by clicking the three dots next to a transaction and selecting Find Unmatched. This tool helps isolate transactions that QuickBooks couldn’t pair, allowing you to manually review and categorize them.

Persuasive action is key when dealing with unmatched transactions. Instead of ignoring them, take the time to investigate. Unmatched entries could indicate errors in data entry, missing transactions, or even fraudulent activity. For instance, a recurring subscription charge might not match if the vendor changed their billing name slightly. By addressing these promptly, you maintain the integrity of your financial records and avoid compounding issues in future reconciliations.

Comparatively, QuickBooks offers tools like Rules and Categories to streamline the matching process. Set up rules for recurring transactions, such as automatically categorizing your monthly internet bill under “Utilities.” This reduces the number of unmatched transactions over time. Additionally, leverage the Reconcile feature to ensure all transactions align with your bank statement. While this process is more time-consuming, it’s essential for catching discrepancies early and maintaining accurate financial records.

Practically, here’s a tip: use the Add button to manually create missing transactions if you identify gaps. For example, if a deposit isn’t showing up, enter it directly into the register and match it to the corresponding bank transaction. Be cautious, though—double-check dates and amounts to avoid duplications. Regularly reviewing unmatched transactions not only keeps your books clean but also provides insights into spending patterns or billing inconsistencies. By mastering this process, you transform a potential headache into a proactive financial management tool.

Ally Bank Savings: Minimum Balance Requirements and Benefits

You may want to see also

Explore related products

![]()

Exporting Transaction Reports

QuickBooks offers a robust feature for exporting transaction reports, allowing users to analyze bank transactions outside the platform using tools like Excel or Google Sheets. To begin, navigate to the Reports tab and select Banking Summary or Transaction Detail reports. Customize the date range to filter transactions, then click Run Report. Once the report is generated, locate the Export button, typically found in the top-right corner, and choose your preferred format—CSV, Excel, or PDF. This process ensures you have a portable, detailed record of transactions for deeper analysis or record-keeping.

While exporting is straightforward, understanding the nuances of each file format can enhance usability. CSV files are ideal for quick imports into spreadsheet software but lack formatting. Excel files retain column widths, fonts, and formulas, making them better for presentations or further manipulation. PDFs are best for static, shareable documents that preserve the report’s appearance. For instance, if you’re sharing transaction data with a financial advisor, a PDF ensures the data remains unchanged. Choose the format based on your end goal—analysis, sharing, or archiving.

A common pitfall when exporting transaction reports is overlooking the customization options before exporting. QuickBooks allows you to add or remove columns, such as transaction type, memo, or cleared status, directly in the report view. For example, if you’re reconciling accounts, include the Cleared column to track which transactions have been matched with bank statements. Failing to customize the report beforehand can result in exporting unnecessary data or missing critical details, requiring additional manual adjustments post-export.

For businesses managing multiple accounts, exporting transaction reports in bulk can save time. QuickBooks permits exporting reports for all accounts simultaneously by selecting the All Accounts option in the report filter. However, this approach generates a large dataset, which can be cumbersome to analyze. A practical tip is to export reports for individual accounts separately, then consolidate them in a master spreadsheet. This method maintains clarity and allows for account-specific annotations, such as categorizing transactions for tax purposes or identifying discrepancies.

Finally, consider automating the export process for recurring needs. QuickBooks Online users can leverage third-party apps like Zapier or QuickBooks’ own automation tools to schedule regular report exports. For instance, set up a weekly export of transaction reports to a cloud storage service like Google Drive or Dropbox. This ensures stakeholders always have access to the latest data without manual intervention. Automation not only saves time but also reduces the risk of human error, making it an invaluable strategy for businesses with high transaction volumes.

Accessing Cuba's Internet Banking: A Step-by-Step Guide for Users

You may want to see also

Frequently asked questions

To view bank transactions in QuickBooks Online, go to the Banking menu, select the account you want to view, and all transactions will be displayed. You can filter by date, type, or status for easier navigation.

Yes, in QuickBooks Desktop, go to the Banking menu, select Reconcile, and choose the account. Click on Locate Discrepancies and then Show Reconciled Transactions to view them.

Use the Search bar at the top of QuickBooks and enter the transaction details (e.g., amount, date, or payee). Alternatively, go to the Banking menu, select the account, and use the filters to narrow down the results.