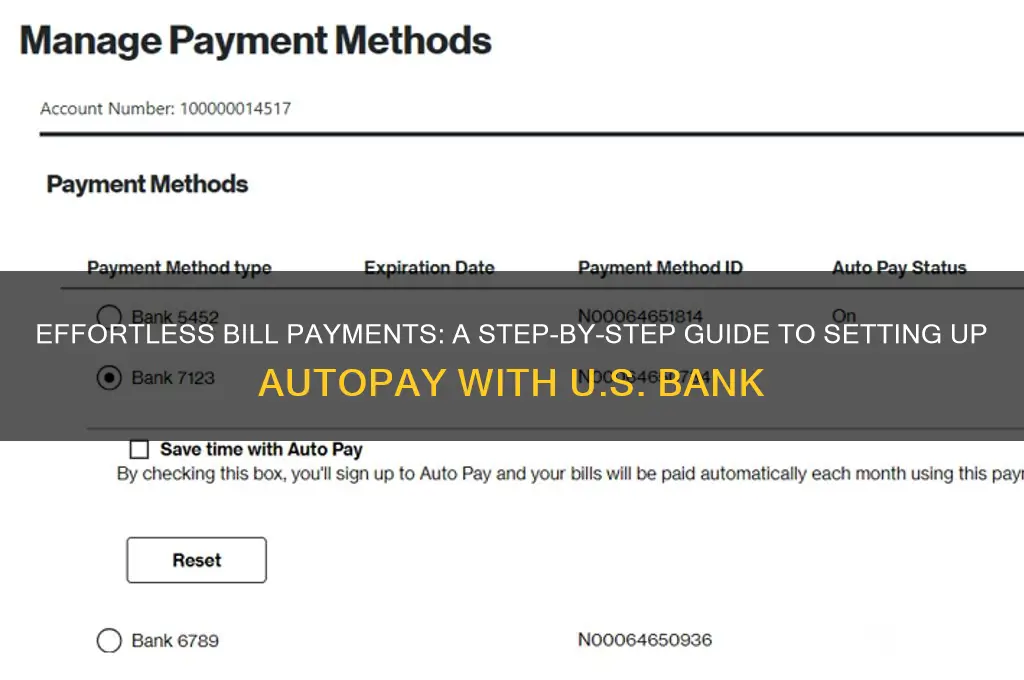

Setting up autopay with a U.S. bank is a convenient way to ensure timely payments for bills, loans, or other recurring expenses, reducing the risk of late fees and improving financial management. Most U.S. banks offer autopay services through their online banking platforms or mobile apps, allowing customers to schedule automatic payments directly from their checking or savings accounts. To begin, log in to your bank’s online portal, navigate to the bill pay or autopay section, and follow the prompts to add payees, set payment amounts, and choose a payment schedule. You’ll typically need the payee’s account number and other relevant details, such as the biller’s address or electronic payment information. Once set up, autopay can be easily managed or adjusted as needed, providing peace of mind and streamlining your financial routine. Always review your bank’s terms and conditions to understand any fees or limitations associated with autopay services.

| Characteristics | Values |

|---|---|

| Eligibility | Must have a valid U.S. Bank account and online banking access. |

| Setup Channels | Online Banking, Mobile App, Phone Banking, or In-Branch. |

| Payment Types | Credit cards, loans, mortgages, and other U.S. Bank accounts. |

| Frequency Options | Monthly, bi-weekly, weekly, or custom schedules. |

| Payment Timing | Payments are typically processed on the due date or a chosen date. |

| Notification System | Email or text alerts for upcoming payments and confirmations. |

| Modification/Cancellation | Can be modified or canceled online or via customer service before cutoff. |

| Security Features | Encrypted transactions and two-factor authentication (2FA) for login. |

| Fees | No additional fees for setting up autopay. |

| Processing Time | Payments are processed within 1-2 business days. |

| Customer Support | Available via phone, chat, or in-branch for assistance. |

| Compatibility | Works with U.S. Bank accounts and select external accounts. |

| Documentation Required | Account details and payment information for setup. |

| Minimum Payment Option | Can set up for minimum payments or full amounts. |

| Error Handling | Notifications for failed payments and retry options. |

| History Access | Payment history available in online banking and mobile app. |

Explore related products

What You'll Learn

- Enable Autopay Online: Log in, find billing, select autopay, enter details, confirm setup

- Choose Payment Source: Link checking, savings, or card for autopay transactions

- Set Payment Schedule: Select frequency (monthly, bi-weekly) and due date preferences

- Verify Account Details: Double-check account and routing numbers for accuracy

- Review Terms & Conditions: Understand fees, cancellation policies, and autopay rules

![]()

Enable Autopay Online: Log in, find billing, select autopay, enter details, confirm setup

Setting up autopay through your U.S. bank’s online platform streamlines bill payments, reducing the risk of late fees and saving time. The process is straightforward but requires attention to detail to ensure accuracy. Begin by logging into your bank’s online portal using your credentials. Most banks offer a secure, user-friendly interface accessible via desktop or mobile app. Once logged in, navigate to the billing or payments section, typically found under account management or services. This is where you’ll locate the autopay setup option, often labeled as "recurring payments" or "automatic bill pay."

Selecting autopay is the next critical step. Banks usually provide options to choose the frequency of payments (e.g., monthly, quarterly) and the account from which funds will be deducted. For instance, if you’re paying a credit card bill, ensure the linked checking account has sufficient funds to avoid overdraft fees. Some banks allow you to set up multiple autopay schedules for different payees, such as utilities, loans, or subscriptions. Be mindful of due dates and processing times, as payments may take 1–3 business days to post, depending on the bank and payee.

Entering payment details demands precision. You’ll need the payee’s name, account number, and payment address. For digital payments, a biller code or payee ID may be required. Double-check these details to avoid errors, as incorrect information can lead to failed payments or delays. Many banks offer a payee search feature to auto-populate details, reducing manual input mistakes. If you’re setting up autopay for a loan or mortgage, confirm the payment amount aligns with your agreement to avoid underpayment penalties.

The final step is confirming the setup. Review all entered information, including payment frequency, amount, and linked account. Some banks provide a summary page or email confirmation for your records. Test the autopay by monitoring your account for the first scheduled payment. If it fails, contact your bank immediately to troubleshoot. Practical tips include setting up payment alerts to notify you when autopay is processed and periodically reviewing autopay schedules to ensure they align with your financial situation. By following these steps, you can confidently enable autopay and enjoy the convenience of automated payments.

Understanding Bank Routing Numbers: How Many Digits Are There?

You may want to see also

Explore related products

![]()

Choose Payment Source: Link checking, savings, or card for autopay transactions

Selecting the right payment source for autopay is a pivotal decision that shapes your financial management. U.S. Bank allows you to link a checking account, savings account, or credit/debit card for autopay transactions, each with distinct advantages and trade-offs. Checking accounts are the most common choice due to their liquidity and direct link to everyday spending, but savings accounts can be ideal for those who want to ensure funds are always available for specific bills. Credit cards, while less conventional, offer rewards or cashback opportunities, though they require vigilant monitoring to avoid interest charges. Understanding these options ensures your autopay setup aligns with your financial goals and habits.

Consider the liquidity and purpose of each account when making your choice. A checking account is typically the go-to option because it’s designed for frequent transactions and has fewer restrictions on withdrawals. For instance, if you’re setting up autopay for monthly utilities or subscriptions, linking your checking account ensures seamless payments without dipping into savings. However, if you’re using autopay for predictable, larger expenses like rent or insurance, a savings account might be preferable, especially if you’ve earmarked those funds specifically for such payments. Just be mindful of federal regulations like Regulation D, which limits certain savings account withdrawals to six per month, though U.S. Bank may waive this restriction for autopay transactions.

For those seeking to maximize rewards, linking a credit card to autopay can be a strategic move. Many credit cards offer cashback, points, or miles for every dollar spent, turning routine bills into opportunities for earning. However, this approach requires discipline. Ensure the bill amount is paid off in full each month to avoid accruing interest, which can negate any rewards earned. Additionally, verify that the merchant or service provider doesn’t charge convenience fees for credit card payments, as these can offset the benefits. Debit cards, while similar to checking accounts, may offer fewer protections and rewards, making them a less appealing option for autopay.

Practical tips can streamline your decision-making process. Start by reviewing your monthly budget to identify which account has consistent funds for autopay. If you’re using a savings account, set up a buffer to avoid overdraft fees or penalties for exceeding withdrawal limits. For credit card users, automate the payment of the credit card bill from your checking account to ensure timely repayment. U.S. Bank’s online platform often provides a side-by-side comparison of linked accounts, helping you visualize which account best suits your needs. Finally, periodically reassess your payment source, especially after significant financial changes like a job switch or increased expenses.

In conclusion, choosing the right payment source for autopay is a balance of convenience, financial strategy, and risk management. Whether you prioritize liquidity, rewards, or fund segregation, U.S. Bank’s flexibility in linking checking, savings, or card accounts empowers you to tailor autopay to your lifestyle. By weighing the pros and cons of each option and implementing practical safeguards, you can ensure autopay becomes a tool for financial efficiency rather than a source of stress.

Manufactured Homes: Banks' Take on Loans and Insurance

You may want to see also

Explore related products

![]()

Set Payment Schedule: Select frequency (monthly, bi-weekly) and due date preferences

Setting up autopay through your US bank requires careful consideration of your payment schedule, particularly the frequency and due date. This decision hinges on aligning your financial obligations with your income cycle and budgeting habits. For instance, if you receive bi-weekly paychecks, opting for bi-weekly payments can synchronize your cash flow, ensuring funds are available when payments are deducted. Conversely, monthly payments might suit those with fixed monthly incomes or larger, less frequent expenses.

The choice between monthly and bi-weekly payments isn’t just about convenience—it impacts your financial health. Bi-weekly payments, for example, result in 26 half-payments annually, effectively adding one extra full payment toward your principal balance each year. This can significantly reduce interest costs over time, particularly for loans like mortgages. However, this approach requires consistent cash flow to avoid overdraft fees or missed payments. Evaluate your financial stability before committing to a faster payment cadence.

Selecting the right due date is equally critical. Aim for a date that falls a few days after your paycheck clears or when your account balance is typically at its highest. For example, if you’re paid on the 1st and 15th of each month, scheduling payments for the 5th or 20th ensures funds are available. Avoid dates near recurring expenses, such as rent or utility bills, to prevent overdrafts. Most banks allow you to adjust due dates within a specific window, providing flexibility to adapt to changing financial circumstances.

Practical tips can streamline this process. First, review your bank’s autopay policies to understand any limitations or fees. Second, set up payment reminders a few days before the due date to monitor your account balance. Third, periodically reassess your payment schedule, especially after significant financial changes like a job switch or salary increase. Finally, leverage budgeting tools or apps to track cash flow and ensure your chosen frequency and due date remain sustainable.

In conclusion, selecting the right payment frequency and due date for autopay is a strategic decision that balances cash flow, financial goals, and personal habits. By aligning payments with your income cycle, optimizing due dates, and staying proactive, you can maximize the benefits of autopay while minimizing risks. This tailored approach not only simplifies bill management but also contributes to long-term financial stability.

KYC in Banking: What It Stands For and Why It Matters

You may want to see also

![]()

Verify Account Details: Double-check account and routing numbers for accuracy

A single misplaced digit can derail your autopay setup, triggering late fees, service disruptions, or even overdraft charges. Account and routing numbers are the GPS coordinates of your financial transactions — accuracy is non-negotiable. Before finalizing autopay enrollment, treat these numbers like a high-stakes password: verify, re-verify, and verify again.

Step 1: Locate the Numbers with Precision

Your account number (typically 10–12 digits) and routing number (9 digits) are found on the bottom of a paper check or within your bank’s online portal. If using a mobile app, navigate to the account summary section, where these details are often displayed under a "Direct Deposit" or "Account Information" tab. Pro tip: Avoid copying numbers from old statements or screenshots; always source them directly from an official, up-to-date document.

Step 2: Cross-Reference for Consistency

Banks occasionally update routing numbers during mergers or system upgrades. Cross-check your numbers against the bank’s official website or a recent statement. For added certainty, call your bank’s customer service line and ask a representative to confirm the details verbally. This dual-verification method acts as a financial spell-check, catching errors before they compound.

Step 3: Beware of Typos and Transposition

The human eye is notoriously fallible when scanning sequences of numbers. A common pitfall is transposing digits (e.g., typing "35" instead of "53"). To mitigate this, read the numbers aloud as you enter them, or use the "write-and-compare" method: jot down the numbers by hand, then re-enter them from your note. This tactile approach forces your brain to re-process the information, reducing slip-ups.

The Cost of Inaccuracy: A Cautionary Tale

A misplaced routing number can send your autopayment to the wrong bank entirely, while an incorrect account number may result in a rejected transaction or, worse, a payment to someone else’s account. In 2022, the CFPB reported that 12% of autopay errors stemmed from input mistakes, with consumers losing an average of $50–$200 in fees per incident. This isn’t just about money — it’s about maintaining trust with service providers and avoiding the administrative headache of rectifying errors.

Final Takeaway: Treat Verification as a Ritual

Think of account verification as the safety harness of autopay setup. It takes less than 5 minutes but provides indefinite protection against costly mistakes. Pair this step with a calendar reminder to re-verify numbers annually, especially if you’ve switched banks or accounts. In the automated world of finance, this manual check is your last line of defense — use it rigorously.

Master the Art of Rolling Quarters for Bank Deposits Easily

You may want to see also

![]()

Review Terms & Conditions: Understand fees, cancellation policies, and autopay rules

Before setting up autopay with your US bank, scrutinize the terms and conditions to avoid unexpected costs or complications. Fees are a critical component—some banks charge for autopay setup, while others impose penalties for missed payments or account changes. For instance, a $5 service fee might apply if your account balance falls below a specified threshold during autopay processing. Understanding these charges upfront ensures you’re not blindsided later. Additionally, look for hidden costs like expedited payment fees or charges for international transactions, even if autopay is domestic.

Cancellation policies are equally important, as they dictate how and when you can stop autopay without penalties. Most banks require a 3–5 business day notice to cancel, but some may enforce a 30-day waiting period. Failure to comply could result in duplicate payments or overdraft fees. For example, if you cancel autopay mid-billing cycle, the bank might still process the payment, leaving you responsible for reimbursement. Knowing these rules empowers you to manage your finances proactively and avoid unnecessary stress.

Autopay rules vary widely across banks, so understanding the specifics is crucial. Some institutions allow partial payments, while others require the full amount. Certain banks may also restrict autopay to specific account types, such as checking accounts, excluding savings or credit cards. For instance, if you attempt to autopay a loan from a savings account, the transaction could be declined, triggering late fees. Familiarize yourself with these limitations to ensure seamless transactions and maintain a positive financial standing.

A practical tip is to create a checklist of key terms to review: fees, cancellation windows, payment types, and account restrictions. Highlight ambiguous language and contact customer service for clarification. For example, if the terms state "processing times may vary," ask for typical processing durations to plan accordingly. This proactive approach not only safeguards your finances but also builds confidence in your autopay setup. Remember, informed decisions today prevent costly mistakes tomorrow.

Does PNC Bank Offer Round-Up Savings Options for Customers?

You may want to see also

Frequently asked questions

To set up autopay with U.S. Bank, log in to your online banking account, navigate to the "Bill Pay" section, select the payee you want to set up autopay for, choose the "Recurring Payments" option, and follow the prompts to schedule your payments.

Yes, you can set up autopay for most types of bills, including utilities, credit cards, loans, and more, as long as the payee accepts electronic payments through U.S. Bank’s bill pay system.

To change or cancel autopay, log in to your online banking account, go to the "Bill Pay" section, find the scheduled payment, and select the option to edit or delete the recurring payment.

U.S. Bank typically does not charge a fee for using autopay through their bill pay service, but it’s always a good idea to check your account terms or contact customer service to confirm.

Set up autopay at least 3-5 business days before the due date to ensure the payment is processed and delivered on time, as processing times may vary depending on the payee.